Introductory Economics: Lesson 3-6

1/55

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

56 Terms

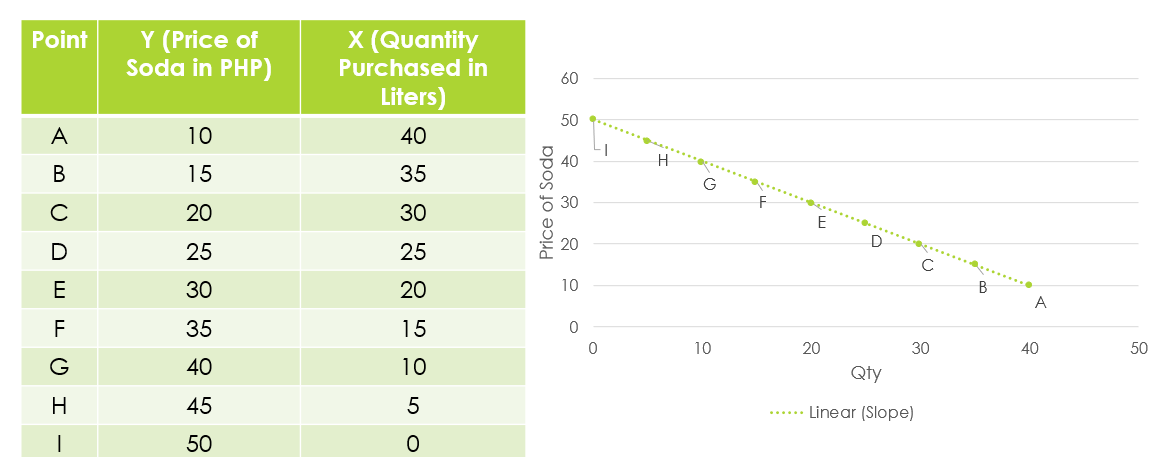

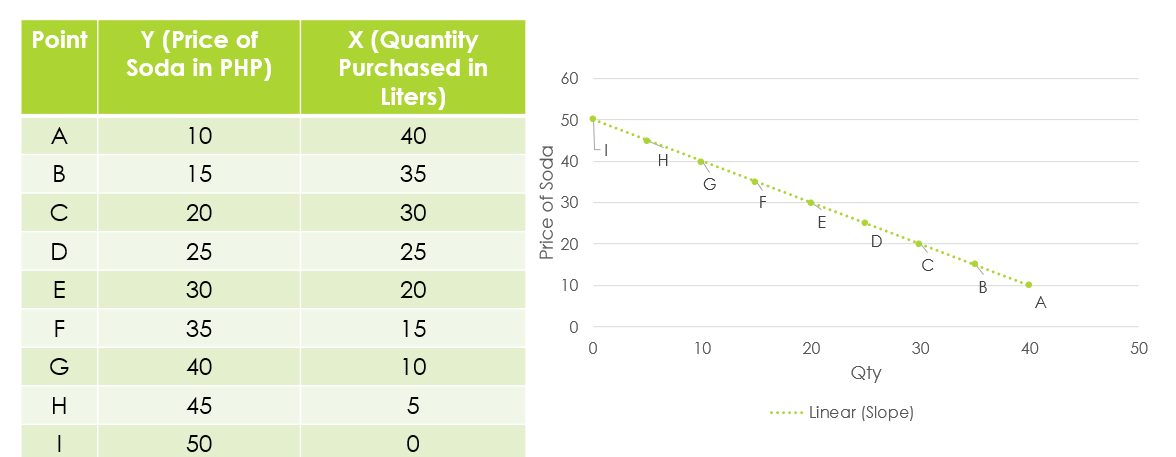

Law of Demand

The concept that there is an opposite relationship between process for goods and services and the quantity the consumers are willing to purchase in a specific time.

Law of Demand

Can be shown as a downward sloping due to the inverse relationship of variables, say prices and quantity.

Changes in demand

An increase or decrease in the quantity demanded at each possible price.

Change in quantity demanded

A movement between points along a stationary demand curve.

Decrease in Price

Increase in quantity demanded

Change in nonprice determinant

Increase in Demand

What are the Nonprice determinants of demand?

Number of Buyers

Tastes and Preferences

Income

Expectation of Buyers

Prices of Related Goods

Income

Normal and Inferior good

Prices of Related Goods

Prices of related good and complementary good

Law of Supply

The concept that there is a positive relationship between prices for goods and services and the quantity the suppliers are willing to produce in a specific time.

Law of Supply

Can be shown as an upward sloping curve due to the positive relationship of variables, say prices and quantity.

Changes in supply

An increase or decrease in the quantity supplied at each possible price.

Change in quantity supplied

A movement between points along a stationary supply curve.

What are the nonprice determinants of supply?

Number of Seller

Technology

Resource Prices

Taxes and Subsidies

Expectation of producers

Prices of other goods the firm could produce

Inverse Relationship

Law of Demand: Individual buyer’s curve

Law of Demand: Market demand curve

Inverse Relationship

Equilibrium

A market condition that occurs in any price and quantity where the quantity of demanded and quantity of supply meets.

Equilibrium Points

Signifies the most ideal price of a certain goods and services.

Equilibrium of Supply and Demand

Occurs normally in a competitive type of market where there are several sellers of the same good or services.

Equilibrium

No agent in the market dictates the price of a good or a service.

Price System

A rationing role that uses the forces of supply and demand to establish an equilibrium of desirable price.

Consumer Surplus

It is the value of the difference between the price the consumers are willing to pay and the actual price of the product.

Consumer Surplus

The volume of surplus is equal to the product of prices and the quantity purchased.

Producer Surplus

It is the value of the difference between the price the consumers are willing to sell and the actual selling price of the price of the product.

Producer Surplus

The volume of surplus is equal to the product of prices and the quantity produced.

Market Efficiency

Maximize the sum of consumer and producer surplus.

Market Efficiency

Net benefit is equals to consumer and producer surplus.

Deadweight Loss

In market efficiency, it is the net loss of consumer and producer surplus due to underproduction or overproduction.

Deadweight Loss

The area in the triangle where the demand or production is not implemented.

Deadweight loss

An opportunity cost/lost.

Changes in Market Equilibrium

Caused by the changes of supply and demand.

Changes in Market Equilibrium

The shift of demand or supply from its original conditions either a shift to the left or right.

Changes in Market Equilibrium

The causes of shifts can be due to the price or nonprice factors.

Repealing Laws of Supply and Demand

Government interventions to control and prevent prices from rising or falling to the equilibrium price.

Price Ceilings

In price control, it is the legal maximum price established per product by the government

Price Floors

In price controls, it is the legal minimum price established per product by the government.

Price Ceiling

In ceiling price, this causes limiting of production.

Price

In ceiling price, this is forced to increase since demand is higher than the supply.

Ceiling Price

Shortage of product

Price Floor

In floor price, this encourage production.

Price

In floor price, this is forced to decrease since the demand is lesser than the supply.

Floor Price

Surplus of product.

Market Failure

A condition in which there is too few or too many resources used in the production of goods and services.

Market Failure

Lack of competition and externalities

Wealth of the Nations, Adam Smith

People of the same trade seldom meet together even for merriment or diversion, but the conversation ends in a conspiracy against the public, or in some diversion to raise prices.

Market Failure: Lack of Competition

Seller collusion, government intervention, and restrictions

Promotes artificial scarcity that decreased supply.

Increases the price of a product

Own Price Demand Elasticity (E = d/p)

It is the responsiveness of the quantity demanded in the changes in the own product.

Income Elasticity (E1)

Refers to the sensitivity of the quantity demanded for a particular good to change in the real income of consumers who buy this good.

Cross Price Elasticity (Epr)

Refers to the sensitivity of the quantity demanded for the changes in the price of one good or another.

Own Price Demand Elasticities Factors

Number of suitable substitutes

Number of uses of the product

Expenditure share of the products

Relative location of price in the demand curve

E > 1

The established price in the higher demand curve is elastic. Quantity demanded is responsive to the changes in the price of the product itself.

E < 1

The established price in the lower demand curve is inelastic. Quantity demanded is not responsive.

Arc and Point Elasticity

Two ways of computing elasticities.

Arc Elasticity

Given two points in the curve.

Point Elasticity

Given the demand function. At least one point is given.

E = 1

Unitary Elasticity - we cannot say that it is responsive or not.