chapter 31 - bankruptcy law

1/36

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

37 Terms

the bankruptcy code and goals

bankruptcy relief is provided under federal law

federal bankruptcy laws = the bankruptcy code (aka the code)

bankruptcy law in the united states has 2 main goals

to protect a debtor by given them a fresh start without creditor’s claims

to ensure equitable treatment of creditors who are competing for a debtors assets

the law attempts to balance the rights of the debtor and of the creditors

bankruptcy courts

bankruptcy proceedings are held in federal bankruptcy courts, which are under the authority of U.S. district courts

bankruptcy courts follow the federal rules of bankruptcy procedure rather than the federal rules of civil procedure

a bankruptcy court can conduct a jury trial if the appropriate district court has authorized it and the parties to the bankruptcy consent

types of bankruptcy relief

the bankruptcy code is contained in title 11 of the untied states code

four chapter set fourth the types of relief that debtors can seek:

chapter 7 provides for liquidation proceedings (individuals and businesses)

liquidation = the sale of the nonexempt assets of a debtor and the distribution of the funds received to creditors

chapter 11 governs reorganizations of businesses

chapter 12 provides for repayment plans for family farmers and family fishermen

chapter 13 provides for repayment plans for individuals with reliable income

a debtor need not be insolvent to file for bankruptcy relief

anyone obligated to a creditor can declare bankruptcy

special requirements for consumer-debtors

consumer-debtor- one whose debts result primarily from the purchase of goods for personal, family, or household use.

the bankruptcy code requires that the clerk of the court provide consumer-debtors with:

written notice of the general purpose, benefits, and costs of each chapter under which they might proceed

information on the types of services available from credit counseling agencies

liquidation proceedings - chapter 7

liquidation under chapter 7 of the bankruptcy code:

the most familar type and is often referred to as ordinary or straight bankruptcy

works as follows:

a debtor turns all assets over to a bankruptcy trustee

bankruptcy trustee= a person appointmed by the court to manage the debtor’s funds in a bankruptcy proceeding

the trustee sells the nonexempt assets and distributes the proceeds to creditors

with certain exceptions, the debtor is granted a discharge of the remaining debts

discharge = the termination of a bankruptcy obligation to pay debts

generally “any person” includes individuals, partnerships, and corporations- may be a debtor in a liquidation proceeding

a straight bankruptcy can be commenced by the filing of either an voluntary or involuntary petition in bankruptcy

petition in bankruptcy = the document that is filed with a bankruptcy court to initiate bankruptcy proceedings

voluntary - the debtor files the petition

involuntary = one or more creditors files a petition to force the debtor into bankruptcy

exceptions: these cannot be debtors in a liquidation bankruptcy (chapter 7)

railroads

insurance companies

banks

savings and loans associations

investment companies licensed by the Small Business Administration

credit unions

voluntary bankruptcy

to bring a voluntary petition in bankruptcy, the debtor files official forms designated for that purpose in the bankruptcy court

the law now requires that before debtors can file a petition they must receive credit counseling from an approved nonprofit agency within the 180 day period proceeding the date of filing

a consumer-debtor who is filing for liquidation bankruptcy must

confirm the accuracy of the petitions contents

state in the petition, at the time of filing, they they understand the relief available under other chapters of the code and choose to proceed under chapter 7

attorneys representing consumer-debtors must:

file an affidavit stating that they have informed the debtors of the relief available under each chapter of the bankruptcy code

reasonably attempt to verify the accuracy of the consumer-debtors petitions and schedules

chapter 7 schedule (voluntary bankruptcy petition)

a list of both secured and unsecured creditors, their addresses, and the amount of debt owed to each

a statement of the financial affairs to the debtor

a list of all property owned by the debtor, including property that the claims is exempt

a list of current income and expenses

a certificate of credit counseling

proof of payments received from employers within 60 days prior to the filing of the petition

a statement of the amount of monthly income, itemized to show the amount is calculated

a copy of the debtor’s federl income tax return for the most recent year ending immediately before the filing of the petition

the official forms must be

completed accurately

sworn under oath and

signed by the debtor

to conceal assets or knowingly supply false info on these schedules is a crime under the bankruptcy laws

with the exception of tax returns, failure to file the required schedules within 45 days after the filing of the petition will result in an automatic dismissal of the petition

a debtor may be required to file a tax return at the end of each taz year while the case is pending to provide a copy to the court

substantial abuse - means test (chapter 7 - voluntary bankruptcy)

A bankruptcy court can dismiss a chapter 7 petition if it consitutes a “substantial abuse” of bankruptcy law

means test used to determine a debtor’s eligibility for chapter 7:

the purpose of the test is to keep upper-income people from abusing the bankruptcy process by filing for chapter 7 instead of chapter 13

under the means test, the debtors average income in recent months is compared with the median income in the geographic area in which the person lives

if it below the median income- qualify to file under chapter 7

if it is above median income - further calcutions must be made to determine the debtor’s future disposable income

future disposable income estimated amoutn is used to determine whether the debtor will have income that could pay for unsecured debts

if so, chapter 7 can be dismissed for substancial abuse

additional grounds for dismissal (chapter 7 - voluntary bankruptcy)

in addition to dismissing a debtor’s voluntary petition for chapter 7 relief for: substancial abuse (fail means test) or for failure to provide the necessary documents within the specified time

a court might also dismiss if the debtor

has been convicted of a violent crime or a drug trafficking offensee

fails to pay post petition domest-support obligations, including child and spousal support

order for relief (chapter 7 - voluntary bankruptcy)

if the voluntary petition for bankruptcy is found to be proper, the filing of the petition will itself constitute an order for relief

order for relief = a court’s grant of assistance to be a complainant

once a consumer-debtors voluntary petition has been filed, the trustee and creditors must be given notice of the order for relief by mail not more than 20 days after entry of the order

involuntary bankruptcy (chapter 7)

occurs when the debtor’s creditors force the debtor into bankruptcy proceedings

cannot be filed against

a charitable insitition

a farmer

the code provides penalties for the filing of frivolous petitions against debtors

the petitioning creditors may be required to pay the costs and attorney’s fees incurred by the debtor in defending against the peition

if filed in bad faith, damages can be awarded for injury to the debtor’s reputation

punitive damages may also be awarded

requirements

if the debtor has 12+ creditors

three or more of these creditors having unsecured claims totaling at least $18,600 must join in the petition

if a debtor has fewer than 12 creditors

one or more creditors having a claim totaling $18,600 or more may file

order for relief

if the debtor challenges the involuntary petition, the bankruptcy court will enter an order for relief if, after hearing, it finds either:

the debtor is not paying debts as they come due OR

a general receiver, assignee, or custodian took possession of, or was appointed to take charge of, substantially all of the debtor’s property within 120 days before the filing of the petition

if the court grants an order for relief, the debtor must supply the same information in the bankruptcy schedules as in a voluntary bankruptcy

automatic stay

in bankruptcy proceedings, the suspension of almost all litigation and order action by creditors against the debtor or the debtor’s property

the stay:

is effective the moment the debtor files a petition in bankruptcy

prohibits creditors from taking any act to collect, assess, or recover a claim against the debtors that arose before the filing of the petition

continues until the bankruptcy proceeding is closed or dismissed

if a creditor knowingly violates the automatic stay, any injured party, including the debtor, is entitled to recover actual damages, costs, and attorney’s fees

punitive damages may be awarded as well

exceptions to the automatic stay

domestic-support obligations, including any debt owed or recoverable by

a spouse or former spouse

a child of the debtor or that child’s parent or guardian

a gov unit

domestic proceedings against the debtor related to:

divorce

child custody or visitation

domestic violence

support enforcement

investigations by a securities regulatory agency

certain statutory liens for property taxes

requests for relief from the automatic stay

a secured creditor or other party in interest can petition the bankruptcy court for relief from the automatic stay

if requested, the stay will automatically terminate 60 days after the request, unless the curt grants an extension of stay or the parties agree otherwise

secured property (automatic stay)

the automatic stay on secured property terminates 45 days after the creditor’s meeting unless the debtor redeems or reaffirms certain debts

the debtor cannot keep the secured property, even if they continue to make payments on it, without reinstating the rights of the secured party to collect on the debt

bad faith (automatic stay)

if the debtor had 2+ bankruptcy petitions dismissed during the prior year, the code presumes bad faith

in such a situation, the automatic stay does NOT go into effect until the court determines that the petition was filed in good faith

estate of bankruptcy (chapter 7)

on the commencement of liquidation proceeding under chapter 7, an estate in bankruptcy is created

the estate consists of all the debtor’s interests in property currently held, wherever located

property aquired to the filing of the petition becomes property of the estate

property acquired after the filing of the petition remains the debtor’s

exception - certain after-acquired property to which the debtor becomes entitled within 180 days after filing may become pary of the estate such as

gifts

inheritances

property settlements (from divorce)

life insurance death proceeds

the bankruptcy trustee (chapter 7)

Appointment: Trustee appointed promptly after order for relief.

Duties: Collect estate, convert to cash, distribute fairly, protect debtor & unsecured creditors.

Accountability: Trustee must properly administer estate.

Powers Deadline: Must exercise powers within 2 years of order.

Substantial Abuse Review

Review debtor’s filings for abuse.

Within 10 days after first creditors’ meeting: state if case presumed abusive (means test).

If abuse presumed:

Options: File motion to dismiss/convert or explain why not.

Domestic-Support Notice: Trustee must notify domestic-support claim holder.

Trustee’s Powers

Strong-arm: Demand turnover of debtor’s property.

Avoidance Powers:

Voidable Rights: Use debtor’s rights (fraud, duress, etc.).

Preferences:

Insolvent debtor.

Transfer for preexisting debt within 90 days before filing (1 year for insiders, 2 years if fraudulent).

Transfer gave creditor more than bankruptcy payout.

Exceptions:

Recent service payments (15 days).

Ordinary business payments.

Property transfers ≤ $7,575 (until 4/1/25).

Domestic-support payments.

If property sold to innocent third party: trustee can’t recover property but can claim value from creditor.

Fraudulent Transfers:

Within 2 years before filing.

Intent to hinder/delay/defraud creditors.

exemptions (chapter 7)

an individual is tentiteled to exempt certain property from a chapter 7 bankruptcy

federal exemptions under bankruptcy code

can be limited for up to a specified dollar amount that changes every 3 years

a portion of equity in the debtor’s home (the homestead exemption)

motor vehicles up to a certain value (usually just one vehicle)

reasonably necessary clothing, household goods and furnishings, and household appliances (the aggregate value not to exceed a certain amount)

jewelry, up to a certain amount

tools of the debtor’s trade or profession, up to a certain value

a portion of unpaid but earned wages

pensions

public benefits, including public assistance(welfare), social security, and unemployment compensation, accumulated up to a certain amount

property that is not exempt under fed law includes

final accounts

cash

family heirlooms

collections of stamps and coins

second cars

vacation homes

state exemptions

individual states have the power to pass legislation precluding debtors from using the federal exemptions within the state

in those states (majority) debtors may only use state, not federal, exemptions

in the rest of the states, debtor’s may choose either the exemptions provided under state law or the federal exemptions

creditors meeting and claims

within 40 days after the order for relief has been granted, the trustee must call a meeting of the debtor’s creditors

the debtor is required to attend (unless excused by the court) and to submit to examination under oath by the creditors and the trustee

each creditor files a proof of claim within 90 days of the creditors meeting with:

the creditor’s name and address

the amount that the creditor asserts is owed to the creditor by the debtor

when the debtor has no assets, creditors are instructed not to file a claim

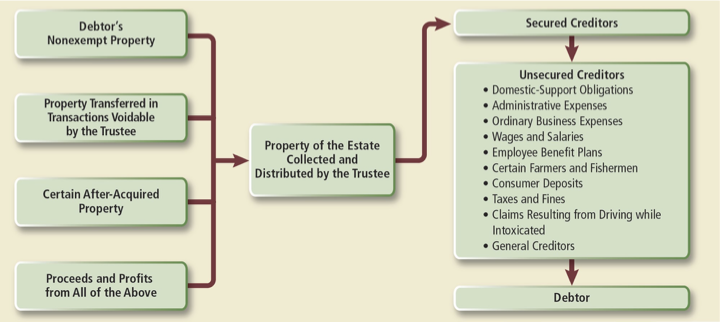

distribution of property - distribution to secured creditors

the code requires that consumer-debtors file a statement of intention with respect to secured collateral. they can either:

pay off the debt and redeem the collateral

claim the collateral is exempt

reaffirm the debt and continue making payments (reaffirmation agreement)

surrender the collateral property to the secured party, who can either:

accept it in full satisfaction of the debt or

sell it and use the proceeds to pay off the debt - if the collateral is insufficient to cover the debt owed, the secured creditor becomes an unsecured creditor for the deficiency

distribution of property - distribution to unsecured creditors

bankruptcy law estabishes an order of priority for payment of debts owed to unsecured creditors

claims for domestic-support obligations, such as child support and alimony, have the highest priority among unsecured creditors, so these claims must be paid first

distribution of property - general

each class, or group, must be fully paid before the next class is entitled to any of the remaining proceeds

if there are insufficient proceeds to fully pay all the creditors in a class, the proceeds are distributed proportionally

once funds run out, classes in lower priority groups will receive nothing

Collection and Distribution of Property in Most Voluntary Bankruptcies

discharge (chapter 7)

from the debtor’s point of view, the primary purpose of liquidation is to obtain a fresh start thru a discharge of debts

a discharge voids, or sets aside, any judgement on a discharged debt and prevents any action to collect it

exceptions:

certain debts, however, are not dischargeable in bankruptcy

certain debtors may not qualify to have all debts discharged in bankruptcy

exceptions to discharge

claims that are not dischargeable in bankruptcy include the following

claims for back taxes accruing within 2 years prior to bankruptcy

claims for amounts borrowed by the debtor to pay federal taxes or any non-dischargeable taxes

claims against property or funds obtained by the debtor under false pretenses or by false representations

claims by creditors who were not notified of bankruptcy

claims based on fraud or misuse of funds by the debtor while acting in a fiduciary capacity or claims involving the debtor’s embezzlement or larceny

domestic support obligations and property settlements as provided for in a separation agreement or divorce decree

claims for amounts due on a retirement account kloan

claims based on willful or malicious conduct by the debtor forward another or the property of another

certain gov fines and penalties

student loans, unless payment of the loans imposes an undue hardship on the debtor and the debtor’s dependents

consumer debts of more than a specified amount ($725 in 2021) for luxury goods ore services owed to a single creditor incurred within 90 days of order to relief

Cash advances totaling more than a threshold amount ($1,000 in 2021) that are extensions of open-end consumer credit obtained by the debtor within seventy days of the order for relief

Judgments against a debtor as a result of the debtor’s operation of a motor vehicle while intoxicated

Fees or assessments arising from property in a homeowners’ association, as long as the debtor retained an interest in the property

Taxes with respect to which the debtor failed to provide required or requested tax documents

objections to discharge

grounds for denial of discharge by a bankruptcy court based on the debtor’s conduct include the following:

the debtor’s concealment or destruction of property with the intent to hinder, delay, or defraud a creditor

the debtor’s fraudulent concealment or destruction of financial records

the grant of a discharge to the debtor within 8 years before the petion was files

the debtor’s failure to complete the required consumer education course

the debtor’s involvements in proceedings in which the debtor could be found guilty of a felony

when a discharge is denied -the debtor’s assets are distributed to the creditors, but the debtor remains liable for the unpaid portion of all claims

revoked: a discharge may be revoked within one year if it is discovered that the debtor acted fraudulently or dishonestly during the bankruptcy proceeding

if that occurs, a creditor whose claim wasn’t satisfied in the distribution of the debtor’s property can proceed with their claim against the debtor

reaffirmation of debt

reaffirmation agreement - an agreement between a debtor and a creditor in which the debtor voluntarily agrees to pay a debt dischargeable in bankruptcy

a debtor cannot retain secured property while continued to pay without entering into a reaffirmation agreement

procedures

to be enforceable, reaffirmation agreements must be made before the debtor is granted a discharge and must include disclosures

the agreement must be signed and filed with the court, along with the disclosures, and the court may need to approve the agreement to make sure it is in the best interest of the debtor

reorganizations - chapter 11

bankruptcy proceeding most commonly used by corporate debtors

the creditors and the debtor formulate a plan under which the debtor pays a portion of the debts and is discharged of the remainder

the debtor is allowed to continue in business

most debtors who are eligible for chapter 7 relief are eligible for relief under chapter 11

congress has established a “fast track”. chapter 11 procedure for small-business debtors whose liabilities do not exceewd a specified amount (about 3 mill) and who do not own or manage real estate. the fast track

enables a debtor to avoid the appointment of a creditors’ committee

shortens the filing periods

relaxes certain other requirements and is less costly(shorter and simpler)

same principles that govern the filing of a liquidation (chapter 7) petition apply to reorganization (chapter 11) proceedings

the case may be brought voluntarily or involuntarily

the automatic-stay provision and its exceptions (such as substantial abuse) apply in reorganization

workouts (chapter 11)

workout agreement - a formal contract between a debtor and their creditors in which the parties agree to negotiate an out-of-court payment plan for the amount due on the loan instead of proceedings to foreclosure

workouts have several advantages:

they are more flexible

they are more conductive to a speedy settlement

they avoid the various administrative costs of bankruptcy proceedings

best interest of the creditors (chapter 11)

once a chapter 11 petition has been filed, a bankruptcy court can dismiss or suspend proceedings at any tome, after notice and hearing, when:

it would better serve the interests of the creditors

there is no reasonable likelihood of rehabilitation under reorganization or

there is an inability to effect a plan or an unreasonable delay by the debtor that may harm the interests of creditors

debtor in possession (chapter 11)

on entry of the order for relief, the debtor generally continues to operate the business as a debtor in possession

debtor in possession (DIP) - in chapter 11 bankruptcy proceedings, a debtor who is allowed to continue in possession of the estate in property (the business) and to continue business operations

the DIP’s role is similar to that of a trustee in a liquidation bankruptcy

the court however, may appoint a trustee (often referred to as a receiver) to operate the debtor’s business if

gross mismanagement of the business is shown

appointing a trustee is in the best interest of the estate

creditors committees (chapter 11)

as soon as practicable after the entry of the order for relief, a creditor’s committee of unsecured creditors is appointed

the committee can consult with the trustee or DIP concerning the administration of the case or the formulation of th eplan

no orders affecting the estate will be entered without the consent of the committee or after a hearing in which the judge is informed of the committee’s position

businesses with debts of less than a specified amount that do not own or manage real estate can avoid creditor’s committees (fast track)

the reorganization plan (chapter 11)

a reorganization plan to rehabilitate the debtor is a plan to conserve and administer the debtor’s assets in the hope of an enventual return to successful operation and solvency

the plan must be fair and equitable and must do the following:

designate classes of claims and interests

specify the treatment to be afforded to the classes of creditors

the plan must provide the same treatment for all claims in a particular crisis

provide an adequate means for the plan’s execution

provide for payment of tax claims over a 5-year period

the plan need not provide for full repayment of unsecured creditors, they can receive percentage of amount owed

filing the plan

only the debtor may file a plan within the first 120 days after the date of the order for relief

if the debtor does not meet the deadlien or obtain an extension, any party may propose a plan

acceptance of the plan

once the plan has been developed, it is submitted to each class of creditors for acceptance

for the plan to be adopted, each class must accept it

a class has “accepted” the plan when a majority of the creditors in the class, representing 2/3s of the amount of the total claim, vote to approve it

confirmation of the plan - powers of the court

confirmation is conditioned on the debtor’s certifying that all post petition domestic support obligations have been paid in full

even when all classes of creditors accept the plan, the court may refuse to confirm if it is not “in the best interests of the creditors”

cram-down provision - the bankruptcy code allows a court to confirm a debtor’s reorganization plan even though only oneclass of creditors has accepted it

however, it must be demonstrated that the plan

does not discriminate unfairly against any creditors and

is fair and equitable

discharge (chapter 11)

the law provides that confirmation of a plan does not discharge an individual debtor

for individual debtors the plan must be completed before discharge will be granted, unless the court orders otherwise

for all other debtors, the court may order discharge at any time after the plan is confirmed

on discharge, the debtor is given a reorganization discharge from all claims not protected under the plan

this discharge does not apply to any claims that would be denied discharge under liquidation (chapter 7)

subchapter 5 bankruptcy (chapter 11)

created in 2020 to make reorganization bankruptcies more accessible to small businesses earning a profit but requiring help to pay down their debt.

allows filers under subchapter 5 of chapter 11 to

force creditors to accept court-approved repayment plans of 3-5 years

use plan to reduce unsecured debt not backed by collateral

benefits

no creditor approval required

no disclosure needed

expenses paid in installments

small business operations

only the small business owner can file the plan (not creditors)

qualifications

total debt cannot exceed a specific amount (about 3 mill - subject to change)

debt cannot be owed to companies insiders

at least 50% of outstanding debt must come from business activities recommendations to the court to confirm the plan

trustee - a special trustee will be named to monitor the plan and make recommendations to the court to confirm the plan

bankruptcy relief under chapter 12 and chapter 13

the code provides for

family-farmer and family-fisherman debt adjustments (chapter 12) and

indivudals’ repayment plans (chapter 13)

procedure for filing chapter 12 and 13 plans is very similar but chapter 13 is more common

individuals repayment plans - chapter 13

an individual with regular income who owes debts not exceeding specified amount may file for a chapter 13 repayment plan

the limit for fixed unsecured debts is about $465,000

the limit for fixed secured debts is about $1.4 mill

among those eligible are

salaried employees

sole propietors

individuals who live on welfare, social security, fixed pensions, or investment income

partnerships and corporations are excluded

repayment plans are less expensive and less complicated than reorganization (chapter 11) or liquidation (chapter 7)

filing the petition

a chapter 13 repayment plan case can be initiated only by:

the debtors filing of voluntary petition or

court conversion of a chapter 7 petition

a trustee who will make payments under the plan must be appointed

on the filing of a repayment plan petition, the automatic stay takes effect

the stay applies to all or part of the debtor’s consumer debt

the stay does not apply to:

any business debt incurred by the debtor

any domestic support obligations

good faith requirement - the bankruptcy code imposes the requirement of good faith on a debtor at both the time of the filing of the plan

the repayment plan

a plan of rehabilitation by repayment must provide for the following:

the turning over to the trustee of such future earnings or income of the debtor as is necessary for execution of the plan

full payment thru deferred cash payments of all claims entitled to priority, such as taces

identical treatment of all claims within a particular class

the repayment plan may provide either for the payment of all obligations in full or for the payment of a lesser amount

if the debtor fails to make timely payments under the plan the court can either:

convert the case to a chapter 7 bankruptcy or

dismiss the petition

in putting together a repayment plan, a debtor must apply to means test to identify the amount of disposable income that will be available to repay creditors after appropriate deductions

the length of the payment plan can be 3 or 5 years, depending on debtor’s families income

if the income is greater than the median family income in the relevant geographic area under the means test, the term of the proposed plan must be three years

discharge - chapter 13

after the debtor has completed all payments, the court grants a discharge of all debts provided for by the repayment plan

generally, all debts are dischargeable except for the following

allowed claims not provided for by the plan

certain long-term debts provided for by the plan

certain tax claims and payments on retirement accounts

claims for domestic support obligations

debts related to injury or property damage caused while driving under the influence of alcohol or drugs

on order granting discharge is final as to the debts listed in the repayment plan

chapter 12 - family farmers and fisherman

goal = help relieve economic pressure on small farmers and commerical fisherman

definitions

a family farmer is one whose gross income is at least 50% farm dependent, debts are at least 50% farm related

total debt for a family farmer must not exceed a specific amount (around $11 mill in 2022)

a family fisherman is one whose gross income is at least 50% dependent on commercial fishing operations, debts are at least 80% related to commercial fishing

total debt for a family fisherman must not exceed a certain amount (around $2.3 mill in 2022)

a partnership or close corporation that is at least 50% owned by the farmer or fisherman’s family can qualify as a family farmer or family fishermen