What is Economics? Chapter 1 (copy)

1/43

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

44 Terms

What is Economics?

the study of how people allocate their limited resources to satisfy their unlimited wants (economic problem).

it is a study of scarcity and choice

Economic Problem

people are faced with limited resources and unlimited wants

consists of choice and scarcity

Scarcity

Anything that has a price is relatively scarce (economic good)

Problem of choice

Making choices when confronted by scarcity involves a trade-off

Three basic economic questions

Production

What to produce?

How to produce?

production technique (labour or capital

Distribution

For whom to produce?

Price mechanism

Why is Economics a Social Science?

Uses scientific methods to investigate and analyse human behaviour.

Types of Resources (3) / factors of production

Natural Resources

supplied from the natural environment

Human Resources

the quality or quantity of the labour force

labour (physical & mental) and enterprise (coordination & management)

Capital

man-made resources which assists the production of goods & services

can be referred to as an investment

Microeconomics

deals with the economic problem from an individual (smaller) perspective

studies how markets and prices work to allocate resources between all the competing industries in the economy

Macroeconomics

deals with the economic problem from society’s POV (large)

concerned with the performance of the whole economy

production, price levels, employment

Social Science

studies the behaviour of people and the choices they make in response to the economic problem

scientific method is used to identify the principles that govern economic behaviour

Ceteris Paribus

‘all other things constant’ - independent variables are kept constant in the hypothesis and observation

Used to isolate the cause and effect of each seperate variable

Economic Model

a simplified representation of economic reality showing the relationship between certain economic variables.

describes what is happening ib an economy, simulate what has happened and forcast what might happen

Rational Self-Interest

people make rational decisions following a logical process in order to compare the benefit and costs.

used by economists to explain human (behaviour) purchasing

Positive economics

can be proven true or false, or tested objectively

“what is…”

can be used to build theories & models which can be put into practice

Normative economics

are subjective statements, opinion rather than facts

“Should…”

Involves a value judgment

Relative Scarcity

resources re limited relative to society’s unlimited wants

Once we satisfy a want there will always be another to take its place

Can be proven true or false

Free Good

not considered scare as it doesn’t have a price

we do not need to make a choice and can consume an unlimited amount (air)

Opportunity Cost and Trade-offs

Every decision involves a choice between one course of action and another, a trade off

the value of the best alternative foregone

represents the real or economic cost of a decision

it is not always financial

Marginal analysis

compares the additional benefits derived from an activity with the extra cost incurred

it makes sense to allocate resources as long as the marginal benefits exceed the marginal costs.

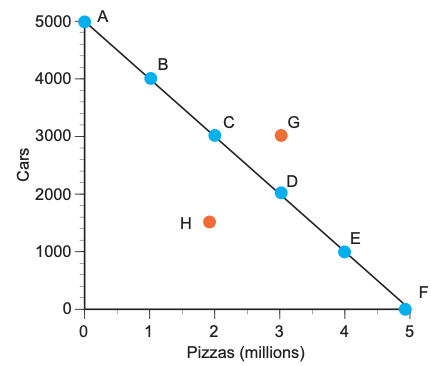

Production Possibility Frontier

Shows all the combinations of goods and services that can be produced by an economy given the available resources and the level of technology

PPF assumptions

resources are fixed

technology is fixed

the economy produces just 2 products

What the PPF shows

When we graph a PPF it shows the maximum and ideal output given the fixed resources and technology

Point H is attainable but inefficient

Point G is unattainable as we don’t have enough resources

the basic economic problem, scarcity and choice

Economic Growth

refers to an increase in the capacity of an economy to produce goods and services

result of an increase in the quantity of resources or an improvement of their quality

investment increases economic growth

consumption only lasts short periods of time

Economic Systems

how a county’s resources are allocated to deal with the economic problem

Must answer the three economic questions

For whom

What

How

determine the allocation of resources and distribution of income

Capitalist/free enterprise economy

Free market

All resources are owned privately, decisions made by the owners in their self-interest

Planned or Command economy

Resources are owned by the state and decisions are made by planning authorities

Most of the time are communist communities

government spends OTHERS money - no care

Mixed Economy

Most economies are mixed, combining elements of both

The government still has important role in providing goods and services

scarcity does not mean

shortage

natural resources

“gifts of nature” water, air

Human resources

quantity and quality of the labour force

types of human resources

Labour

Physical or mental effort applied in the production of a good/service

Enterprise

the coordination and management of production by an entrepreneur.

Ideas/social skills needed to create good/services

Capital resources

man-made resources which assists human resources in the production of goods/services.

social overhead capital

basic infrastructure of the economy. transport, communications

investment “engine of economic growth”

creation of new capital goods

principle of decreasing marginal benefit

as you consume more of something the extra or additional benefit you get declines

net benefits

total benefits and total costs

optimal number

where the net benefits are largest

keep allocating resources until we maximise the net benefits

Why is the PPF sloped downwards

trade-off, to produce more of one good production must decrease for another good

scarcity

what does a straight line PPF mean

constant oppurtunity cost

movement along the curve of PPF

opportunity cost of changing production

law of increasing opportunity cost

As more of one good is produced opportunity cost increases since resources are not equally productive at producing both goods

economic growth will cause PPF to

shift right

lower rate of economic growth

where more resources are voted to producing consumption goods

frontier only moves a short distance right

market economy

both government and private sector determine allocation of resources

consumer is considered sovereign

spending determines what is produced

shortages and surpluses are rare, prices will always adjust to ‘clear the markey’

most efficient because prices reflect relative scarcity