Lecture 4: AI in Accounting and Auditing

1/13

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

14 Terms

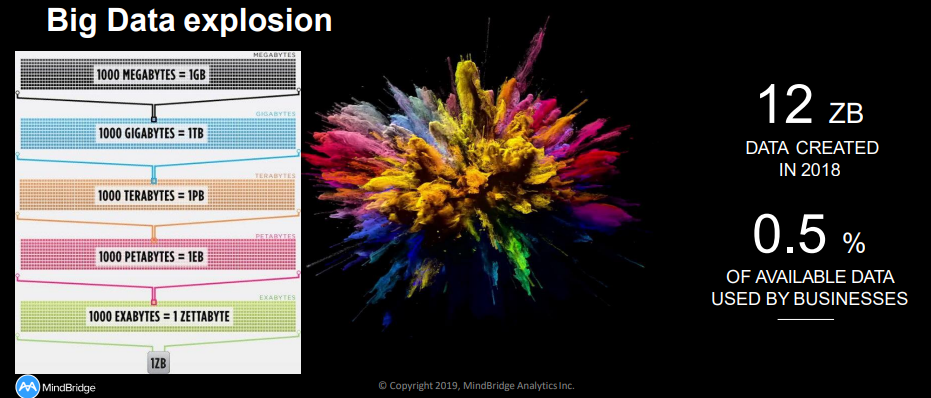

What is Big Data?

No unified definition:

Data exceeding the level of efficient manageability within traditional DB

Process of analyzing a large volume of diverse data, in any variety of form, using ground-breaking apparatus to identify opportunities to improve overall value

Common trait: large population of data

Components: volume, variety, velocity, veracity

New to accounting and audit industry: no formal means to evaluate it, has not applied it in assessments

Correlations vs. causation

Examples of Big Data

GPS receiver in your cell phone

Cash registers when you make a purchase • Cameras in public places

Your car

Your digital photos

Your IoT devices

Sensors

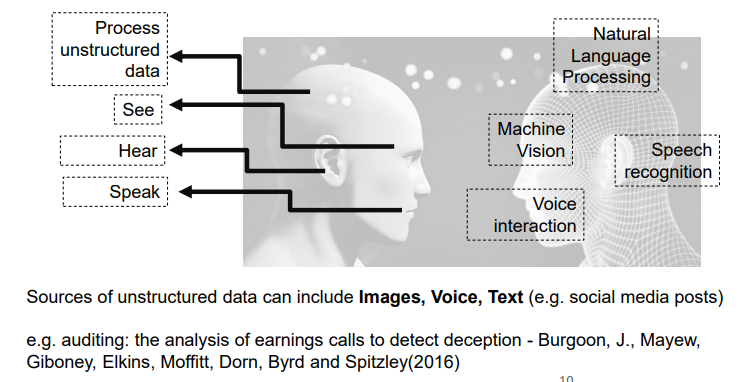

Artificial Intelligence

Artificial intelligence is the use of a computer to model intelligent behavior with minimal human intervention

Intelligence exhibited by machines

A machine mimics ‘cognitive’ functions that humans associate with other human minds

Machines & computer programs are capable of problem solving and learning, like a human brain

Definition: “Intelligence exhibited by machines. A flexible rational agent that perceives its environment and takes actions that maximize its chance of success at some goal. the term ‘artificial intelligence’ is applied when a machine mimics ‘cognitive’ functions that humans associate with other human minds, such as ‘learning’ and ‘problem solving’”

AI Attempts to Mirror Human Capabilities

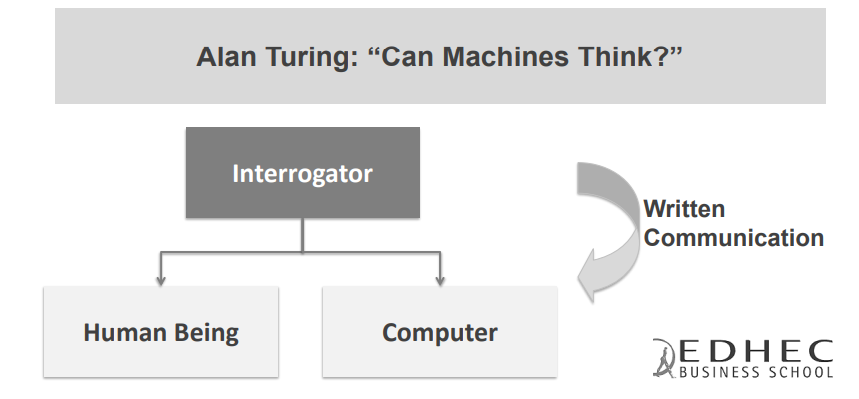

The Turing Test

Evolution of AI

Dreyfus (1964) classifies traditional Artificial Intelligence (AI) work into four main areas:

Game playing

Problem solving

Language translation

Pattern recognition

Two decades later, in 1984, that original optimism hit a rough patch, leading to the collapse of a crop of A.I. start-up companies in Silicon Valley, a time known as “the A.I. winter

Early 80s: focus of AI shifted from basic paradigms and pure logical development to the identification and formalization of human expertise

This led to the area of Expert Systems (ES)

Areas of AI 1990’s

Natural Languages

Expert Systems

Cognition and Learning

Computer Vision

Expert Systems (ES)

Expert Systems became the most popular area of AI and eventually the basis of many commercial, semi-commercial and prototype systems

Vasarhelyi, M. A. “Expert Systems in Accounting and Auditing,” in Artificial Intelligence in Accounting and Auditing, Vols. 1 to 6 , Markus Wiener Publishing Inc., New York. (1989 to 2002)

AI Enablers

Faster technology

Larger yet cheaper storage

Computerization

High level of investments by industry (Google, Baidu, Microsoft, etc.)

Deepmind developed AlphaGo

IBM Watson uses in healthcare

Deloitte and Kira systems in contract analysis

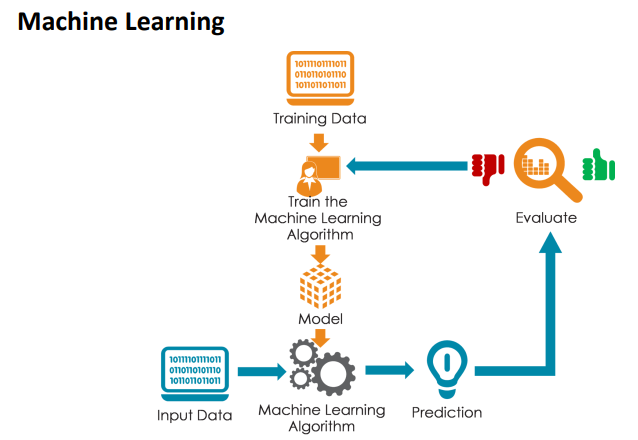

Machine Learning

Unsupervised Learning

No expert input, the computer identifies pattern in data and looks for outliers

Particularly useful where the human expert does not know what to look for

Does not require labeled data

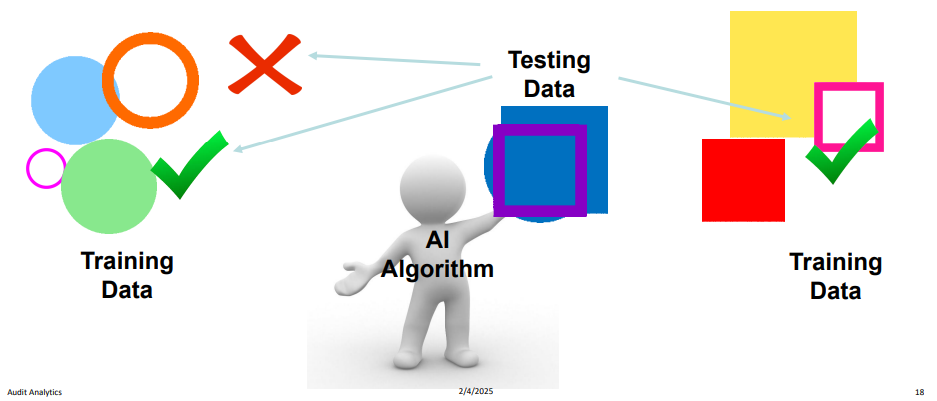

Supervised Learning

Human expert feeds the computer with training data

From that data the computer should learn the pattern

Requires labeled data

Reinforced Learning

Reinforced learning algorithm continuously learns from the environment in an iterative fashion

Uses rewards and punishments

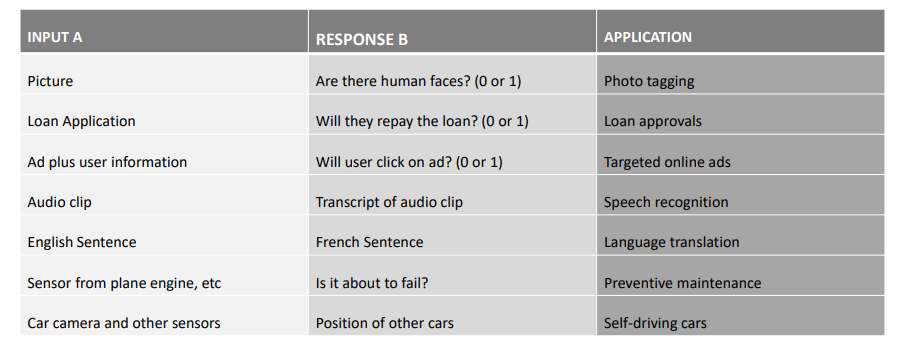

How Does AI work?

Examples of What Machine Learning Can Do

ML Applications in Accounting and Auditing

Expert systems and DSS (duplicate detection)

Predictive Analytics (profitability, bankruptcy)

Outlier detection (fraud, CSA, refunds)

User Segmentation (clustering)

Inventory analysis (drones, images)

Contract analysis (engagement letters)

Sentiment analysis (FS, ESG)

Automation (RPA and IPA)

Recommender systems (App recommender, BotVisor)

Risks and Concerns of AI

Accuracy

Bias

Explainability (Blackb)ox

Security

Privacy

Information spillover

De-skilling

Job loss

Select Considerations when Establishing AI Development

Several factors need to be considered when determining if an application meets the required standards or ethics and safety before implementation

(1) Trust and Accuracy

Accuracy of data inputs and output results

Over reliance on given information without due diligence on sources

Explainability and traceability of outputs

(2) Privacy and Security

Data collection with unclear use; will your sensitive data be made open to the public?

What surveillance applications of GPT will society deem ethical?

Cybersecurity concerns

(3) Fairness and Bias

Bias toward certain subgroups due to public training data

Bias in model can drive unfair outcomes in some business applications

Toxicity in responses requires ongoing management

(4) Legal and Regulatory

Potential copyright and IP infringement considerations

Liability of use

Compliance with regulations (existing and in development)

Where Are We Heading?

Innovation Mindset: Bryan’s Amazing Animals [Drones for Inventory Count]

Auditors perform periodic inventory counts and focus on the innovative practice of using drones and automated counting software to complete the inventory process

Using drone technology and automation to innovate inventory management and for auditing of inventory

EY has launched a global proof of concept to expand the use of drones in inventory observations as part of its digital audit capabilities

In order to enhance audit quality, this extensive pilot project will use pioneering industry technology to improve the accuracy and frequency of the inventory count data collection

While capturing images of the inventory can improve the evidence for the inventory counts, this alone does not necessarily improve the efficiency of the inventory process

Thus, an important complement to capturing images is to automate the identification and counting of the items in the image

To automate the identification of items, several companies have developed automated counting software