Chapter 12 Firms in Perfectly Competitive Markets

1/90

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

91 Terms

as more firms enter a market, the profit market for each individual firm will _______________

shrink

firms in perfectly competitive markets ___________ the price of the product

cannot control

firms in perfectly competitive markets ______________ to earn an economic profit in the long run

are unable

three charesteristics of a market

-number of firms in the industry

-the similarity of the good and services produced throughout the industry

-the ease with which new firms can enter the industry

monopolistic competition

a large number of firms selling products that are differentiated

oligopoly

very few firms selling very similar products

monoply

one firm that controls an entire market

perfectly competitive market

a large number of firms selling almost identical products with no barriers to competition

if a firm in a perfectly competitive market tries to raise the price of a product__________________

it will lose sales because consumers will buy from other firms for a lower price

price taker

a buyer or seller who is unable to effect the market price of a product

most individual firms in a perfectly competitive market don't have power over price in a market because _____________

the market supply curve will not shift enough to change the overall market price by even 1 cent

an individual firm in a perfectly competitive market on a supply-demand curve is represented by

a horizontal line

an entire market for a product in a perfectly competitive market on a supply-demand curve is represented by

a downward sloping demand curve

profit

Total revenue- total cost

for any level of output, a firm's average revenue is _________

equal to the market price

marginal revenue formula

change in total revenue / change in quantity

in a perfectly competitive market, a firms price is equal to ________________

average revenue and marginal revenue

marginal cost

the increase in total cost as result of producing another unit of output

profit maximizing level of output

level of output where marginal revenue equals marginal cost

the marginal revenue curve for a perfectly competitive firm is the same as its _______________

demand curve

optimal decisions are made ____________

at the margin

the profit maximizing level of output is

where the difference between total revenue and total cost is greatest OR where marginal revenue equals marginal cost

for a firm in a perfectly competitive market ______________

price is equal to marginal revenue

Profit formula

(Price - average total cost) X Q

on a supply-demand curve, a firm is making economic profit if _______________

average total revenue is greater than average total cost

to maximize economic profit, a firm should keep producing outputs until ________________

marginal cost is greater then or equal to marginal revenue

on a supply demand curve, a firm breaks even when __________________

price is equal to average total cost

on a supply demand curve, a firm experiences an economic loss when, _______________

price is below average total cost

P > ATC

firm is making profit

P = ATC

firm is breaking even

P < ATC

firm is producing at a loss

when a firm is experiencing economic loss, maximizing profits means

minimizing losses

a firm facing short term losses faces what two options

-continue to operate at a loss

-stop production by shutting down temporarily

if a firm decides to temporarily stop production, it will face losses equal to it's ________________

fixed costs (mortgage, employee wages, utilities,)

a firm can reduce losses by continuing to operate if ____________

total revenue is greater than variable costs

sunk cost

a cost that has already been paid and cannot be recovered

the decision to continue operations or shut down is determined by _________________

whether total revenue is greater or less than variable costs

as long as a firms revenue is greater than its variable costs_________________

it should continue to operate to minimize losses

when a firm in a perfectly competitive market and experiencing losses, one option that is NOT availible is

raising prices

a perfectly competitive firm's marginal cost curve is equal to ________________

its supply curve

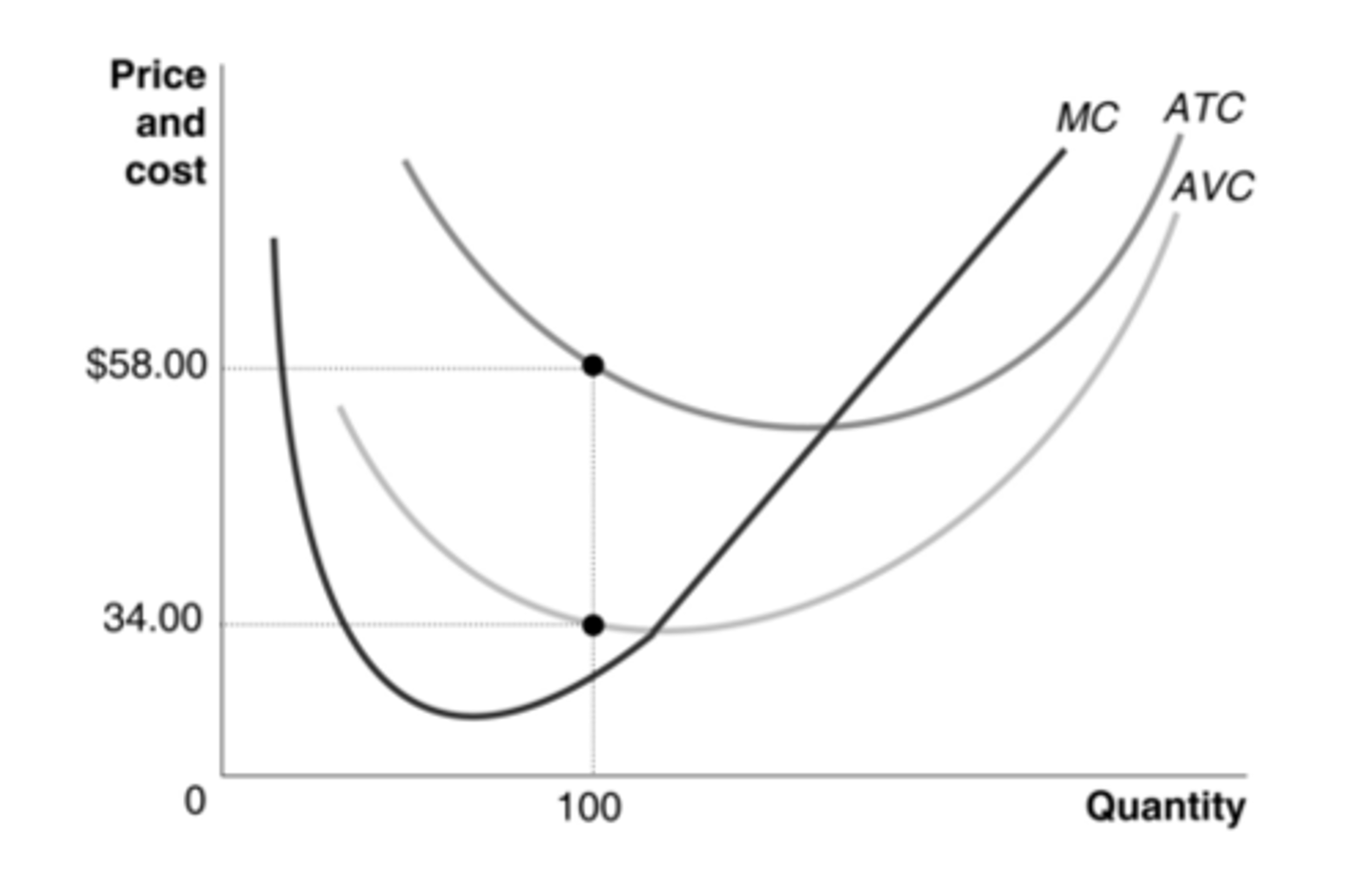

shutdown point

the minimum point on a firm's average variable cost curve. if the price drops to or below this point, the firm should temporarily stop production

the market demand curve is determined by __________

adding up the quantity demanded by each consumer in the market at each price

the market supply curve is determined by _____________

adding up the quantity supplied by each supplier in the market at each price

market supply curve can be calculated by

multiplying the amount of suppliers in the market by the amount produced per each supplier

economic profit

a firms revenues minus all of its explicit and implicit costs

accunting costs

only includes explicit costs

whens firms in a market experience economic profit in the short run,

more firms will enter the market, increasing market supply and drive profits to zero in the long run

what type of profit is the better indicator of a firms economic health?

economic profit

economic loss

when a firm experiences total revenue less than its total cost, including all implicit costs

as long as price is above average variable costs _____________

a firm will continue to stay in business in the short run

as firms enter a market, the market price ______________

drops

as firms exit a market, the market price _______________

rises

long run competitive equilibrium

the situation in which entry and exit of firms has caused the typical firm in that industry to break even

long run average cost curve

shows the lowest cost a firm is able to produce a given quantity of output in the long run

long run competitive equilibrium point

the market price that will always eventually be restored as firms enter and exit a market

in the long run, a perfectly competitive market will supply whatever amount of a good consumers demand at a price ________________________

determined by the minimum point om the typical firms average total cost curve

industries with upward sloping long run supply curves are called

increasing cost industries

industries with downward sloping long run supply curves are called

decreasing cost industries

decreasing cost industires

cost of producing a product decreases as the industry expands

increasing cost industries

typically in areas where the supply of input is limited (natural resources, land, etc)

the cost of producing a product increases as the industry expands

productive effiency

the situation where a good or service is produced at the lowest possible cost

in the long run, only the _____________ benefit from cost reductions

consumers

allocative efficiency

every good or service is produced up to the point where the last unit provides a marginal benefit to the consumer equal to the marginal cost to produce it

If the average total cost curve is above the demand curve, then this firm is

having economic losses

the firm will decrease its output and suffer losses

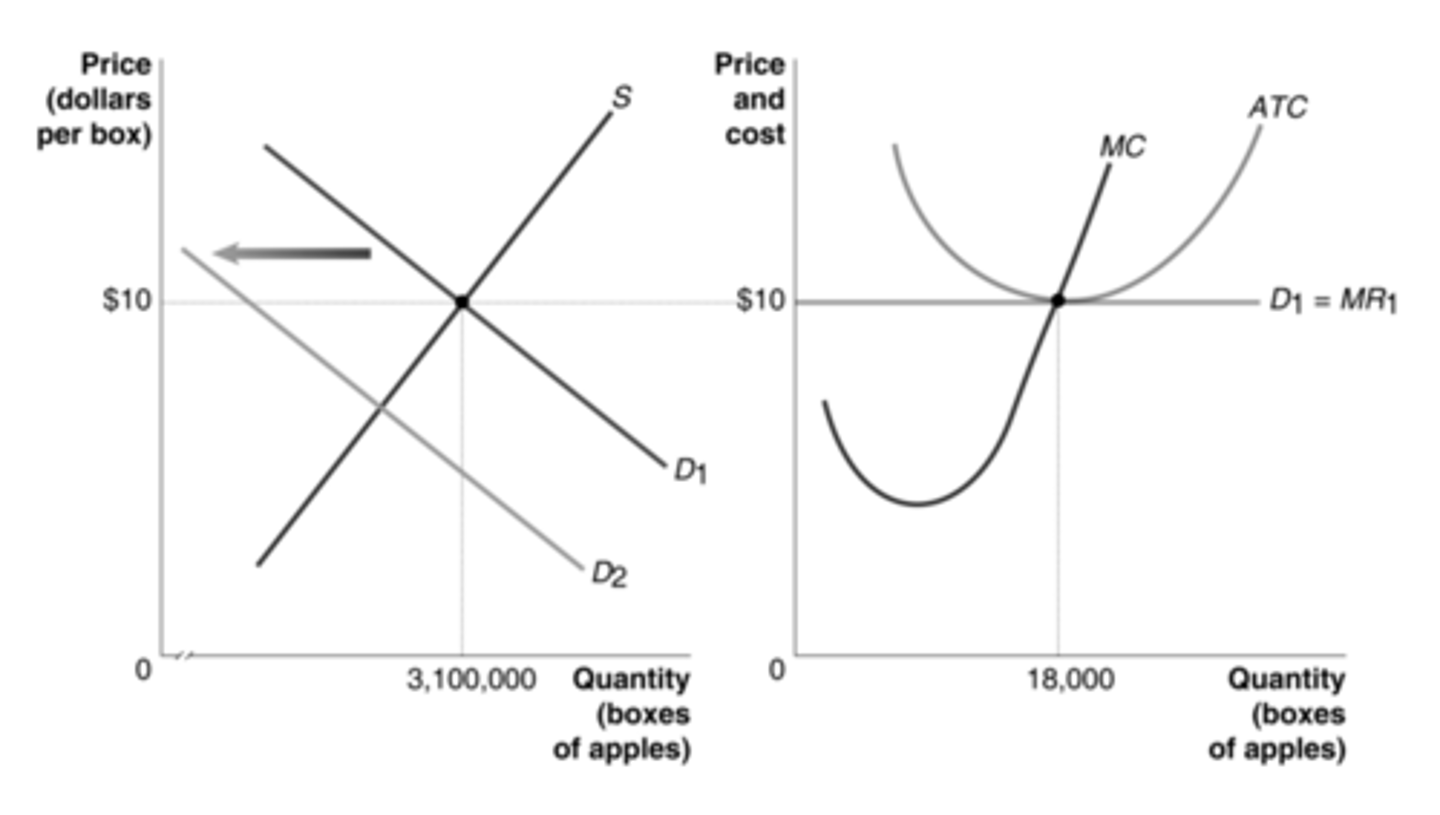

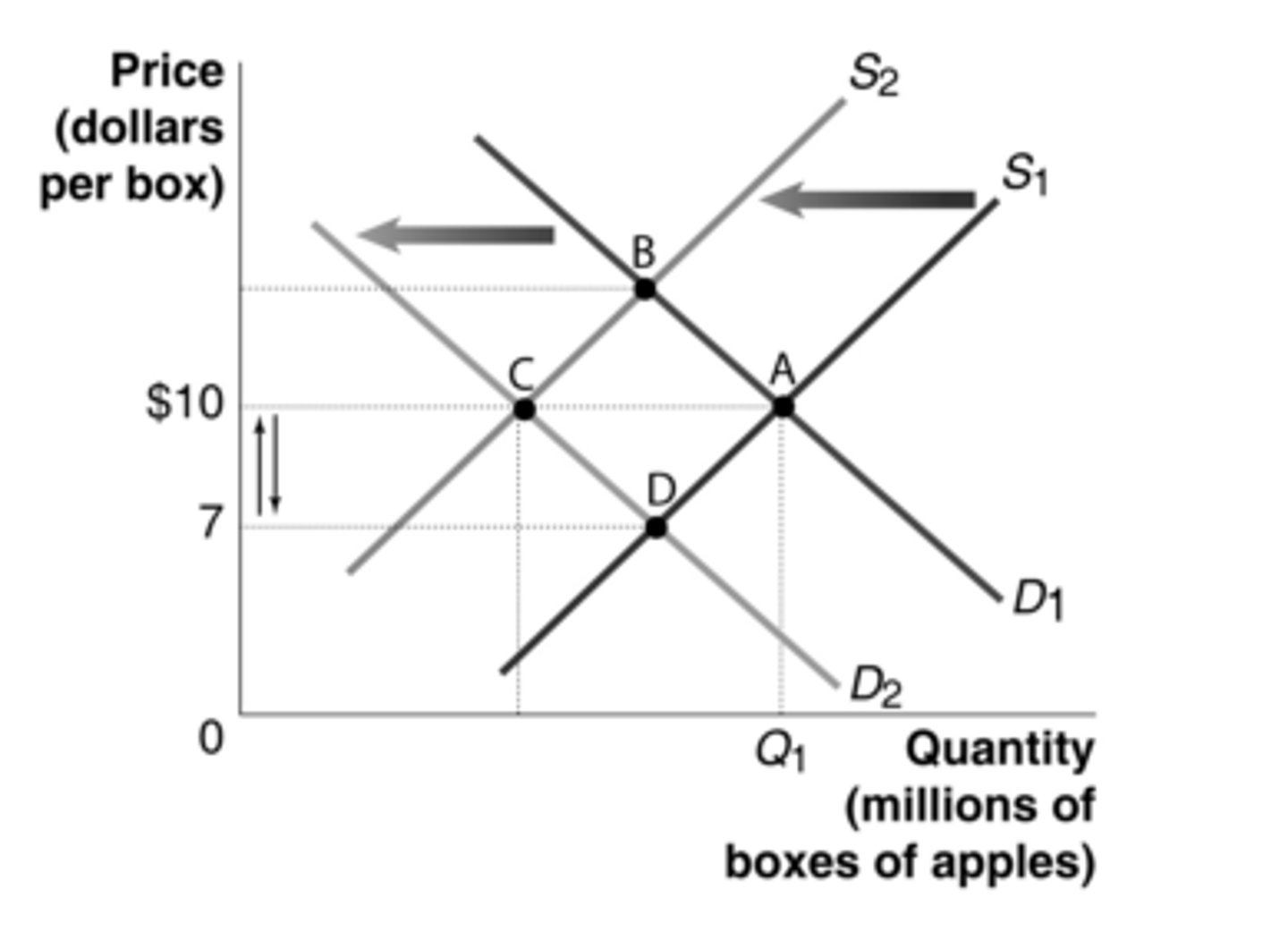

As the market demand shifts to the left, how will the firm's level of output change?

If the average total cost curve is above the demand curve, then this firm is:

having economic losses

demand curve 2

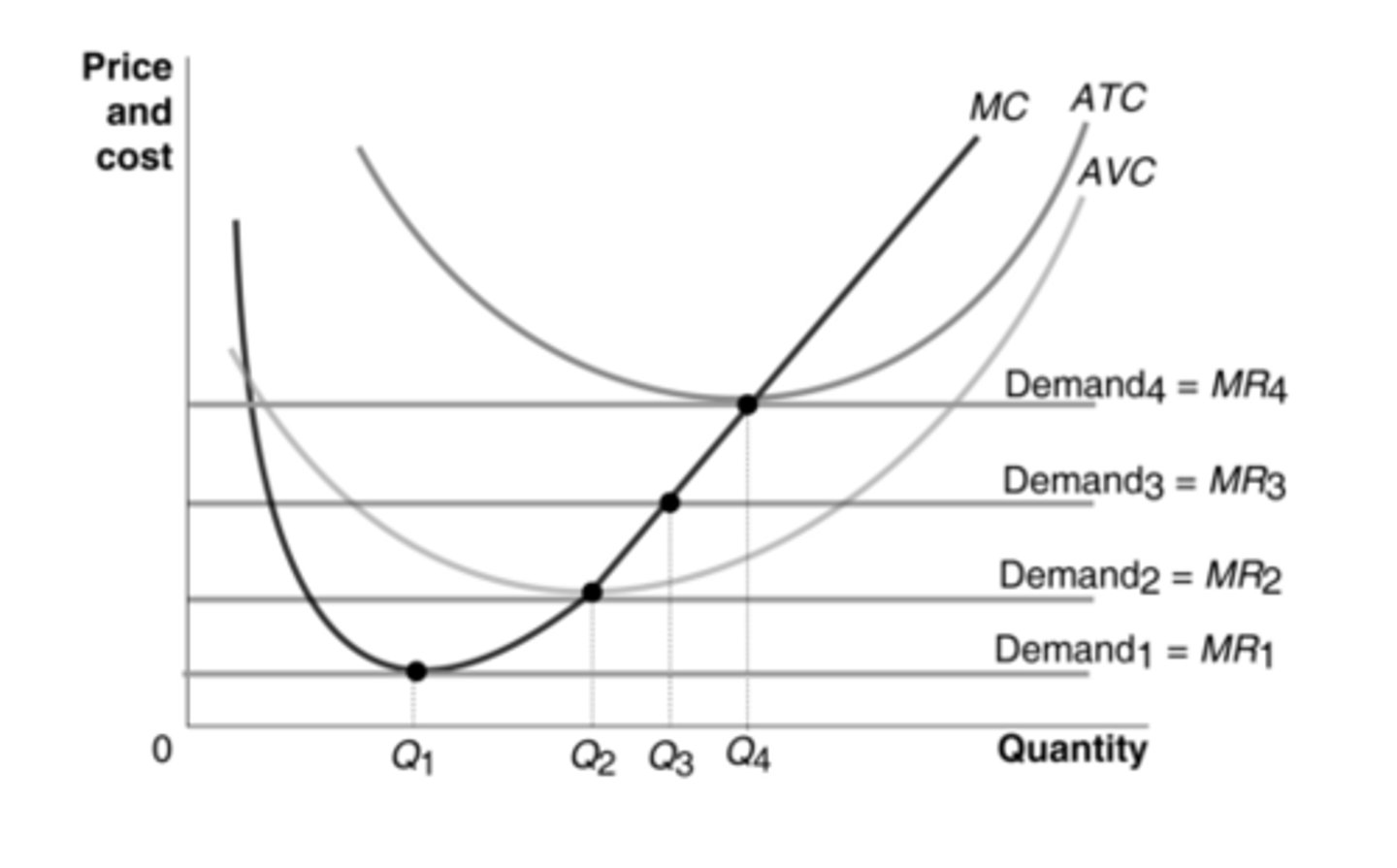

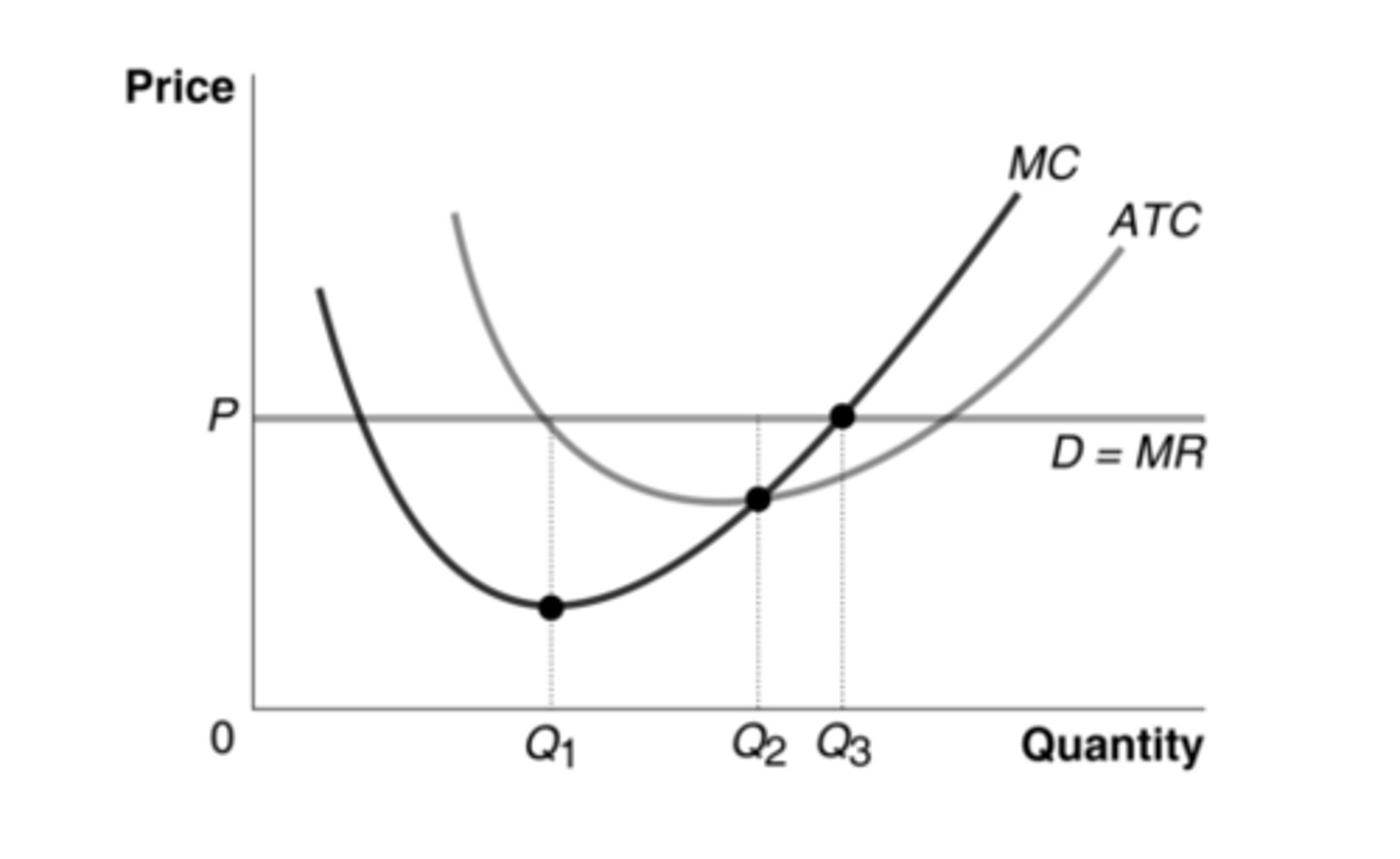

According to the graph, which demand curve is associated with the shutdown point for this perfectly competitive firm?

the graph on the left

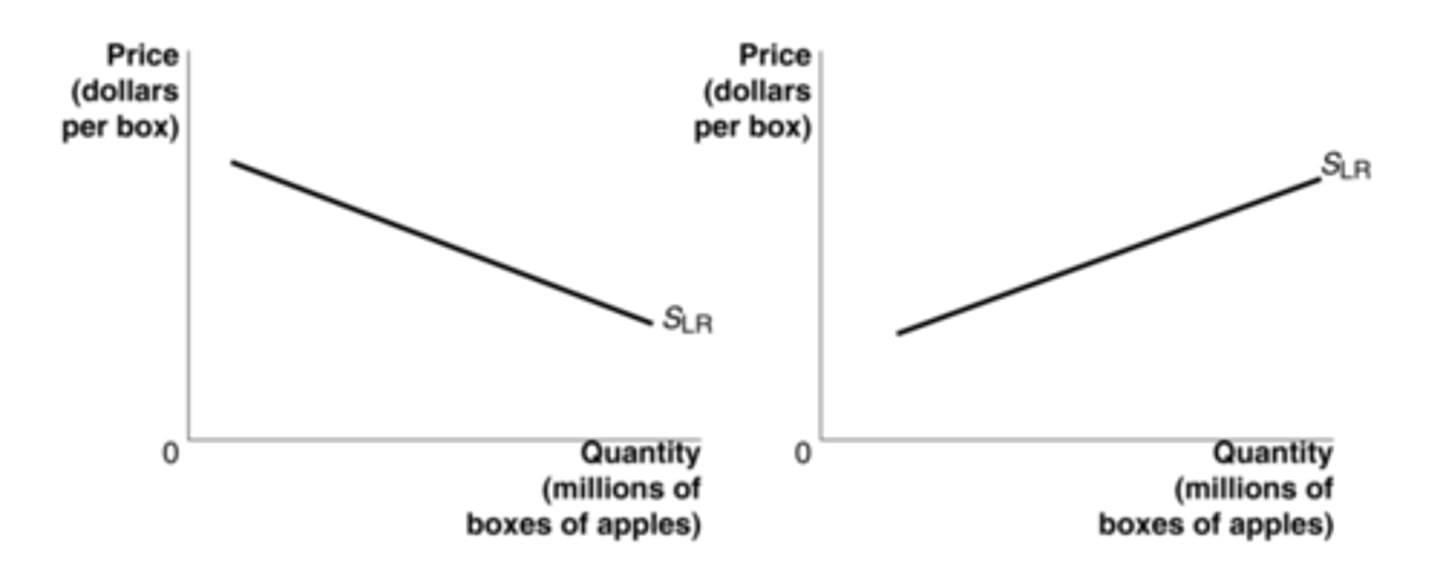

Which graph best depicts an industry in which the firm's average costs decrease as the industry expands production?

point d

According to the graph the shut-down point corresponds to:

point D is the short-run equilibrium and point C is the new long run equilibrium

In this graph, the market is initially in long-run equilibrium at point A. If this is a constant-cost industry, after the decrease in demand, which point is likely to be a short-run equilibrium and which point is likely to be the next long-run equilibrium?

profit in the short run

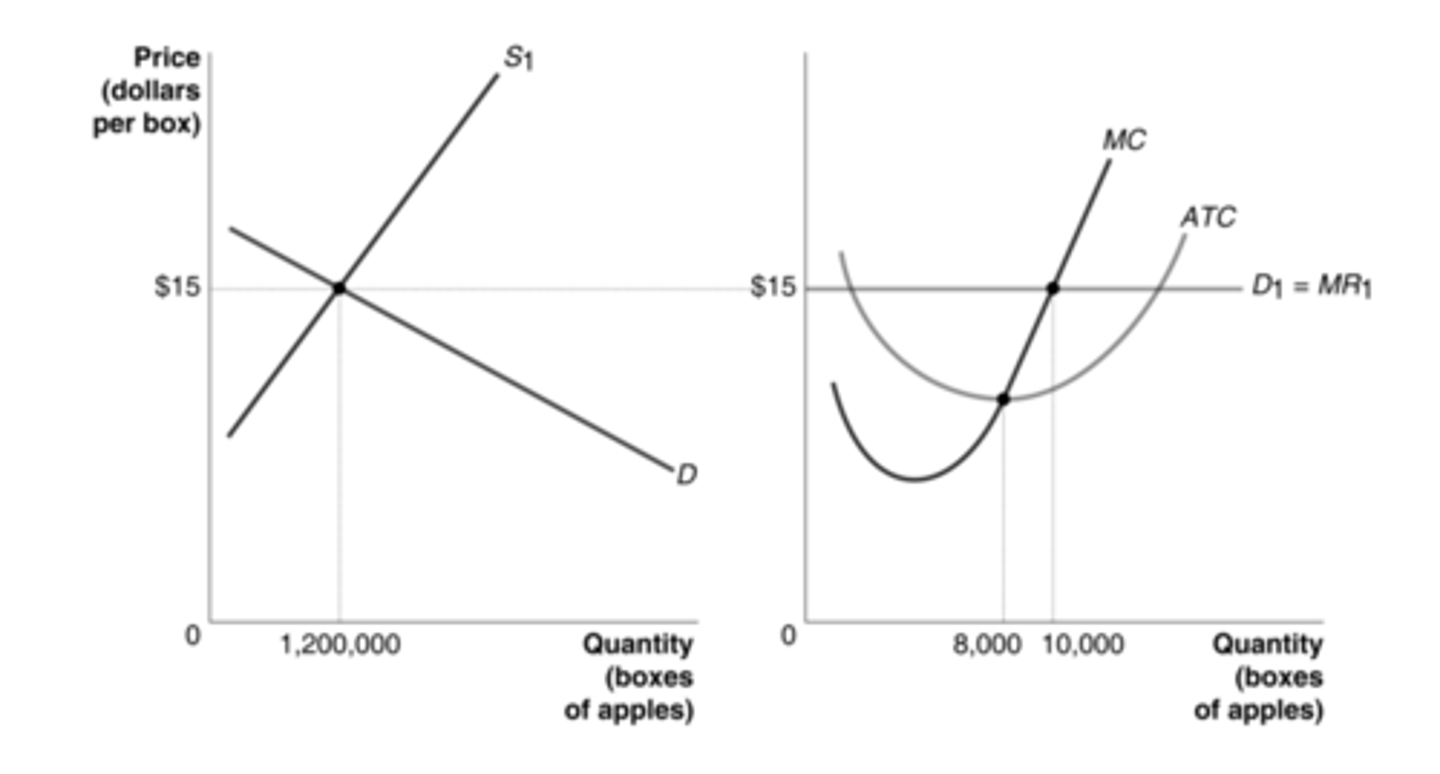

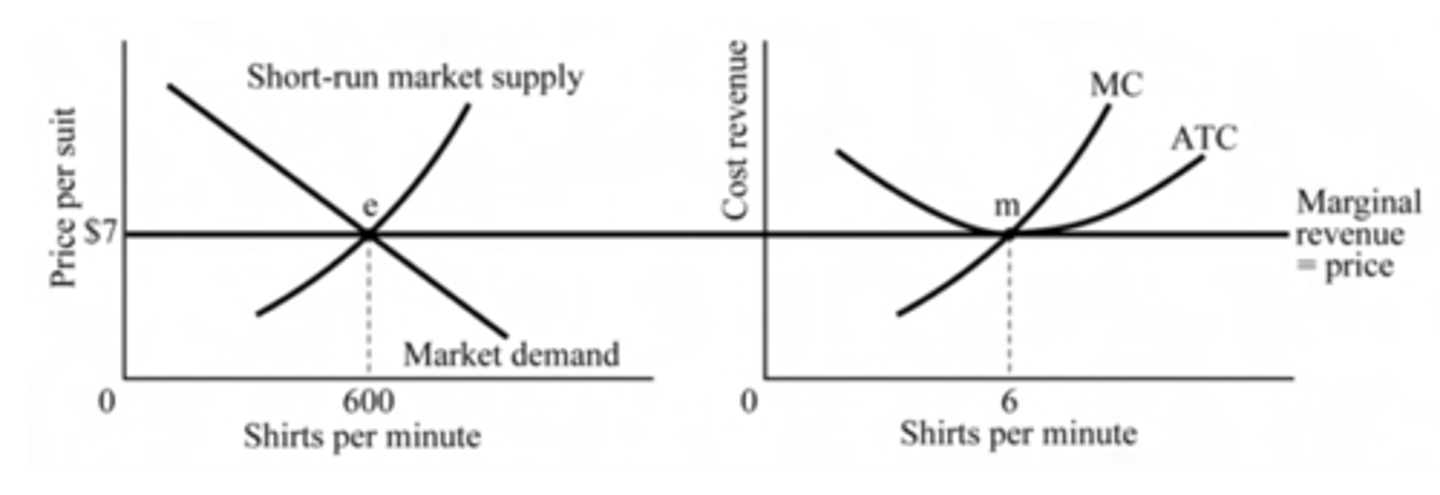

The perfectly competitive firm represented in the graph on the right is experiencing a __________.

Q3

In reference to the graph, at what level of output does this perfectly competitive firm maximize profit?

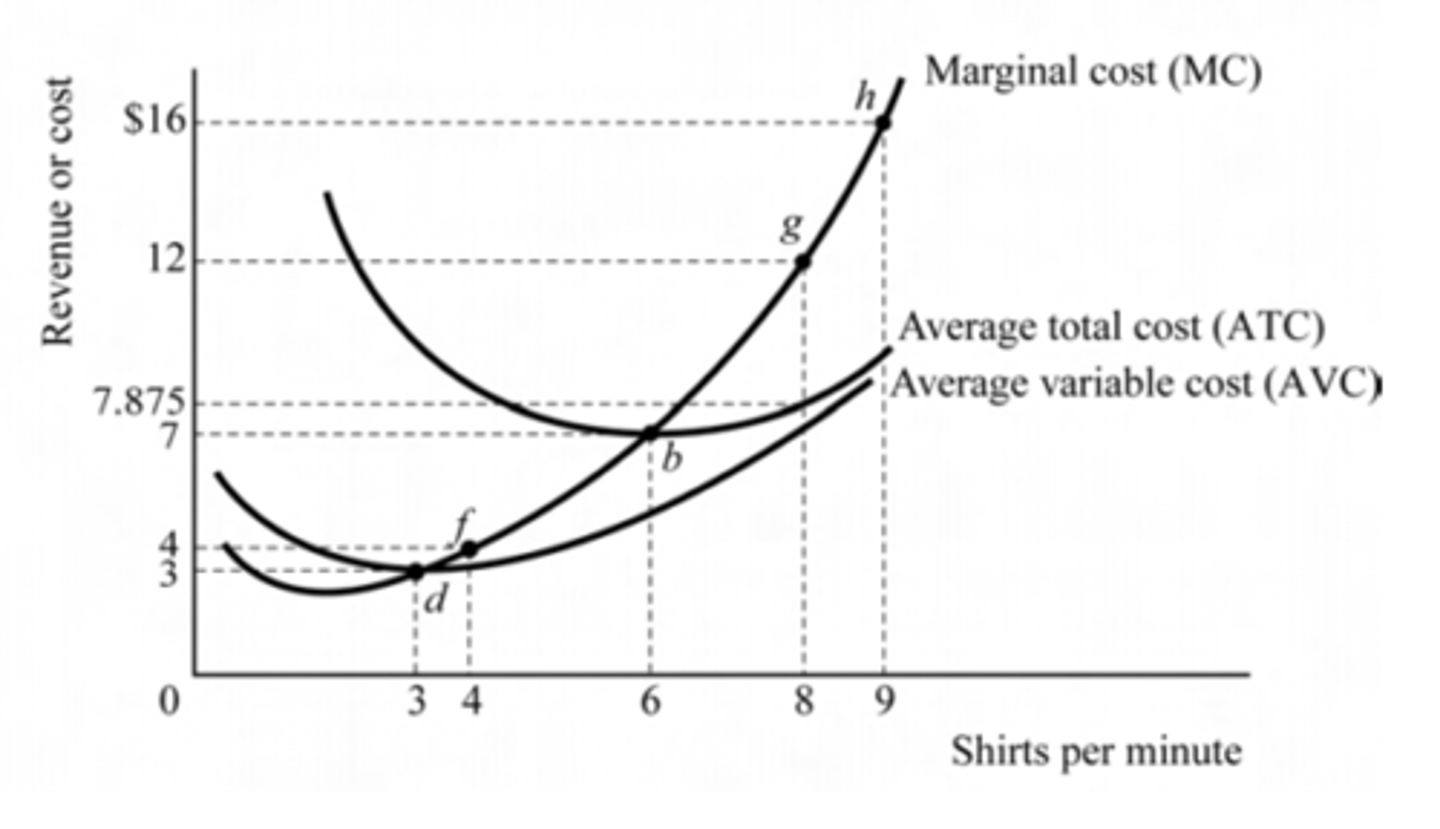

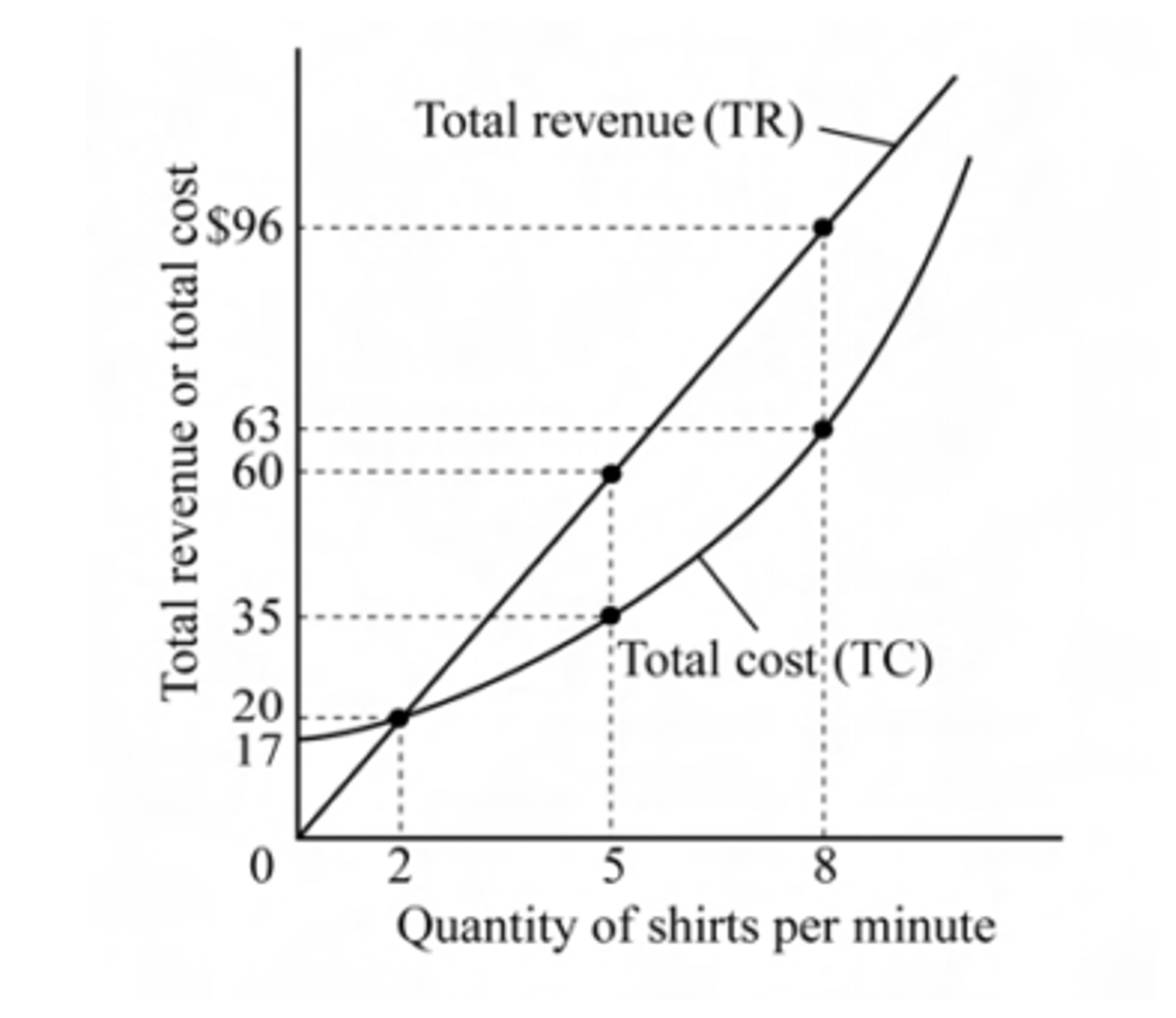

8 shirts per minute

According to the graph, which level of output maximizes profit?

In perfect competition, the marginal revenue is the same as:

price

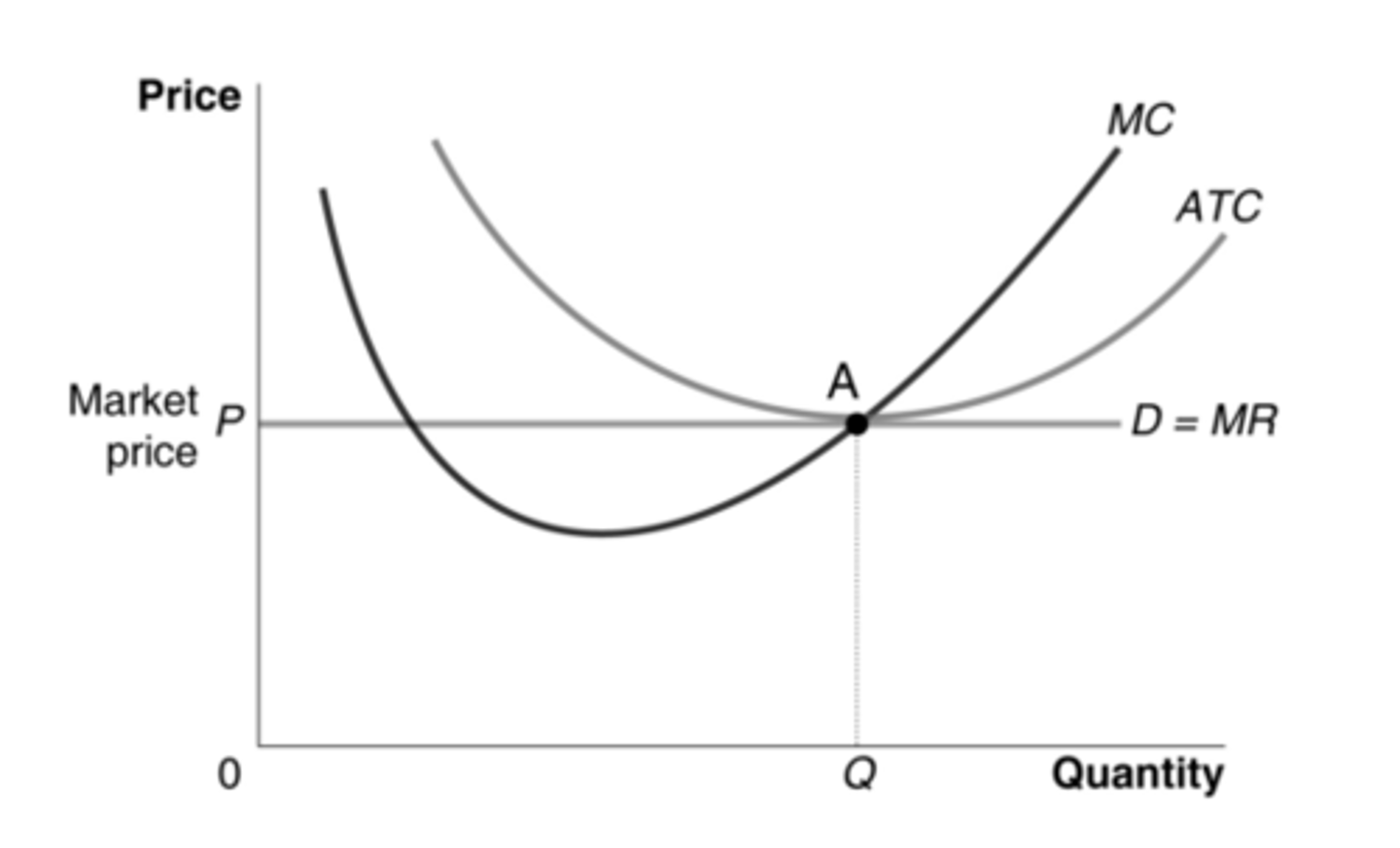

the firm earns 0 economic profit

According to the graph, if a perfectly competitive firm is producing at point A, which of the following is true?

8 units of output

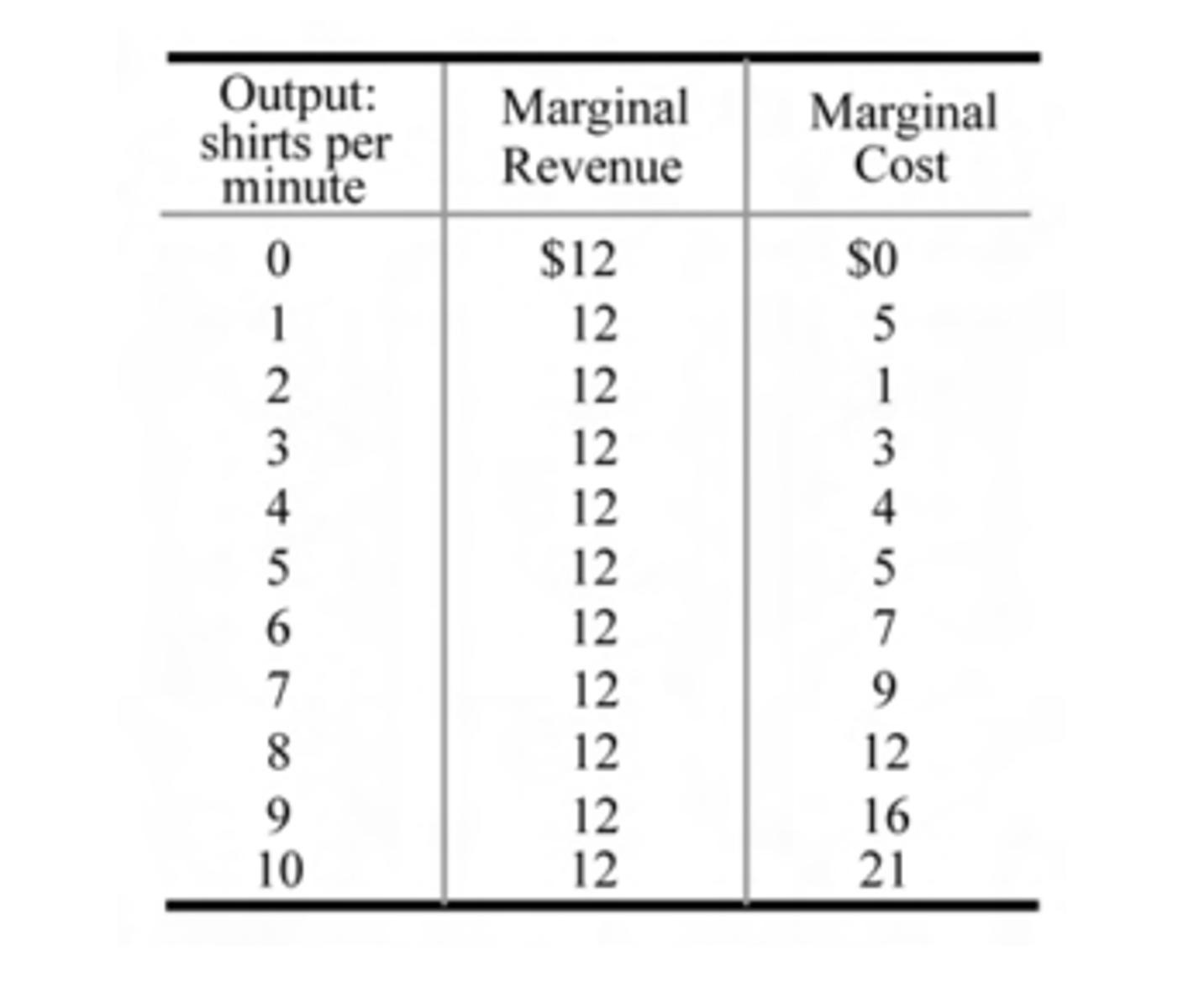

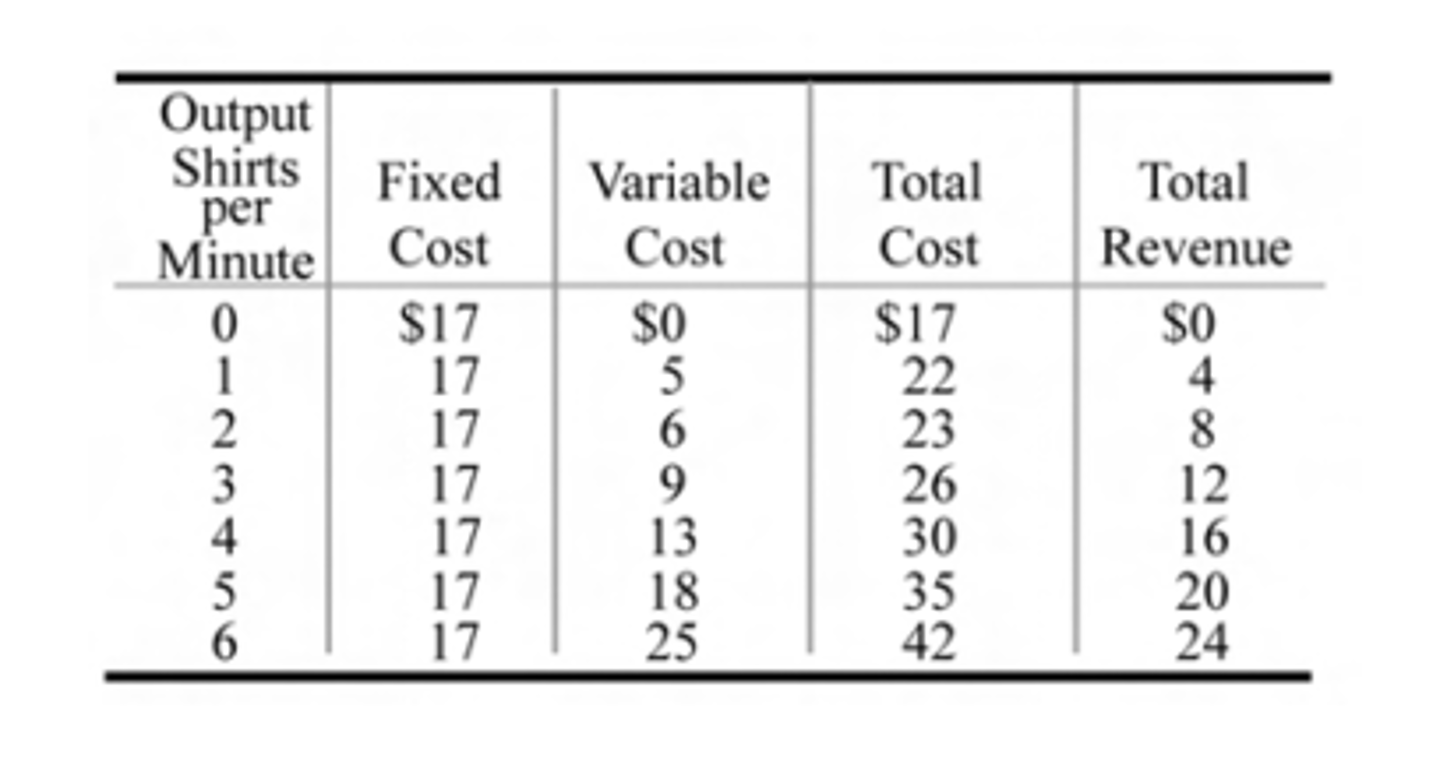

According to the data in the table, what level of output maximizes profit?

Which of the following is a characteristic of a perfectly competitive market?

there is a large number of buyers and sellers

A buyer or seller that is unable to affect the market price is called a __________.

price taker

Long-run equilibrium in perfect competition results in:

both allocative effiency and productive effiency

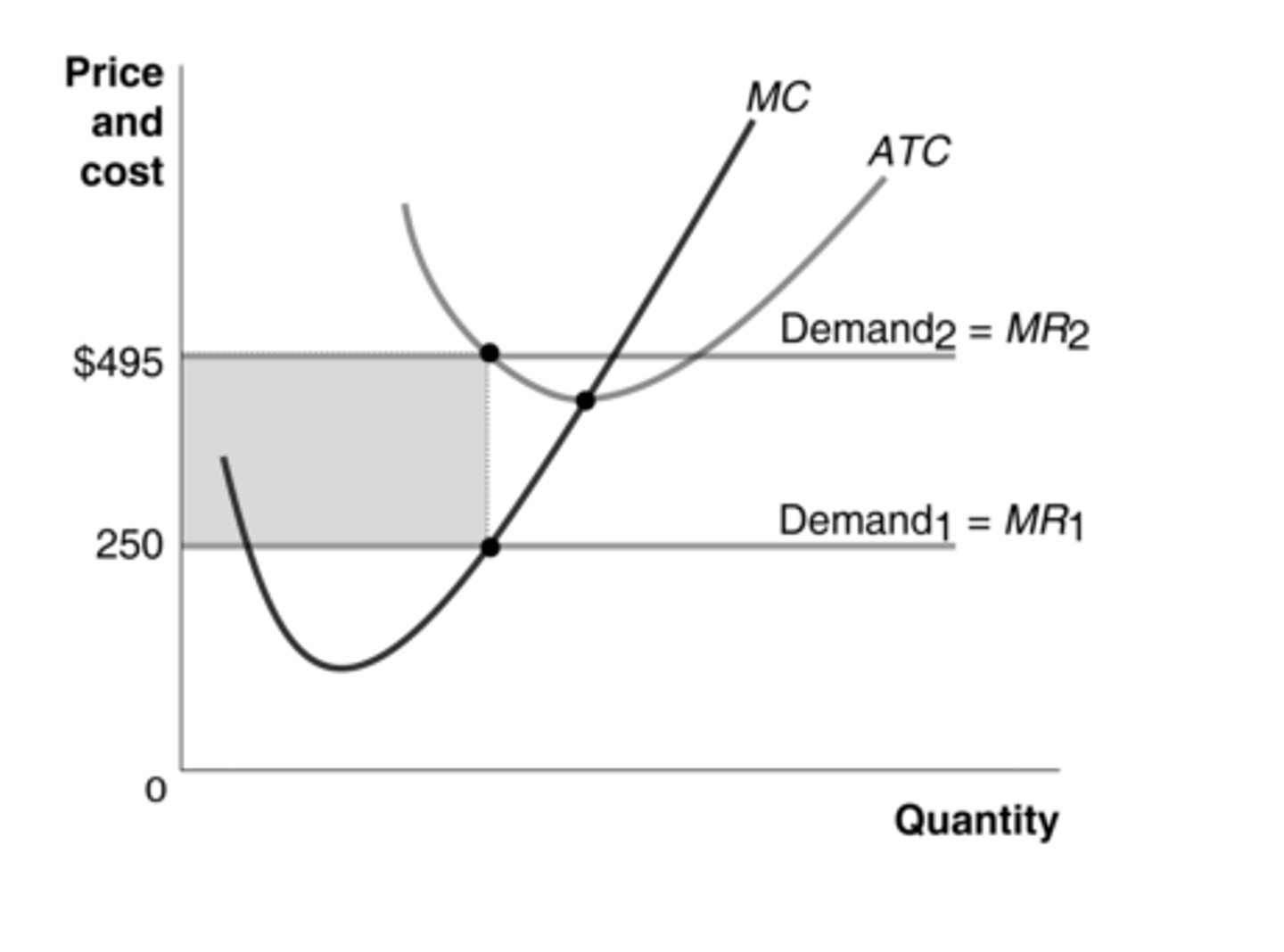

$250

At which price in this graph is the perfectly competitive firm earning negative economic profit?

What is the term given to a cost that has already been paid and cannot be recovered?

sunk costs

no other firms will enter this market

According to the graphs, which of the following is likely to happen in this market in the long run?

negative economic profit

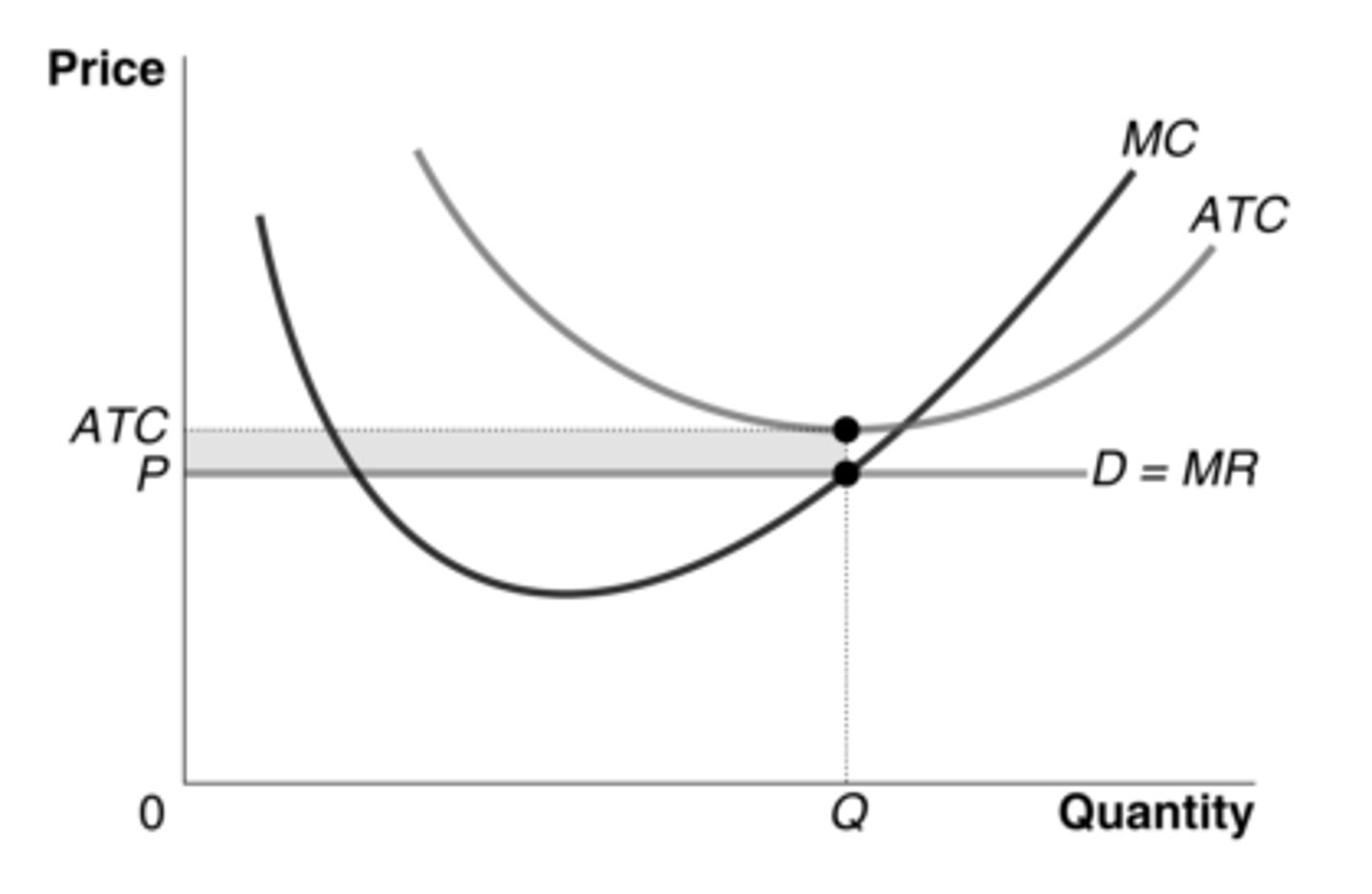

What does the shaded area in the graph represent for a perfectly competitive firm that produces at output level Q?

four units of output, although it would suffer a loss from doing so

According to the data in the table, when the price is $4, the firm would produce:

$2,400

According to the graph, what is the value of total fixed cost for this perfectly competitive firm?

A firm in perfect competition earns profit if:

price is greater than average total cost

In the short run, the firm should:

operate if price > average variable cost

In perfect competition, when a firm is making positive economic profit in the short run, then new firms enter the market causing the market supply curve to __________ and the market price to __________.

shift rightward, decrease

firms should always continue to operate ______________________

price is above variable cost

`

profit maximization can be achieved when

marginal revenue = marginal cost