theme 3 : monopolies

1/11

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

12 Terms

assumptions of a monopoly

can only be established where there is a single seller in the market i.e. there are no close substitutes - therefore market demand is equal to the firms demand curve

high barriers to entry - new entrants to the market find it impossible to match the costs and prices of the established firm in the industry, only remain a monopoly if these barriers exist

in the uk a firm is classified as a monopoly if it has more than 25% of the total market

main barriers to entry that uk supermarkets have

land purchases / land holding : may be used to prevent rivals from opening shops close by which means smaller firms can’t expand

if a company has dominance over a local market, may prevent other firms from being close to maintain dominance

putting pressure on suppliers : can put pressure on suppliers and transfer the risk and cost disadvantages to suppliers instead of having it themselves

total revenue curve

price on y axis

output on x axis

upside down ‘u’ shape

average and marginal revenue curve

price on y axis

output on x axis

average revenue curve is a downward sloping curve

marginal revenue curve falls at twice the rate and becomes negative

how are the total revenue curve and the average and marginal revenue curve related

the peak of the total revenue curve plotted down is where the marginal revenue curve becomes negative

see notes from 20/01/25 to see graph

when is total revenue maximised

maximised where MR is 0

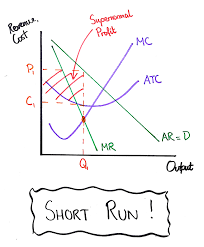

abnormal profit making monopoly in the short run

price on y axis

output on x axis

abnormal profit is the red box

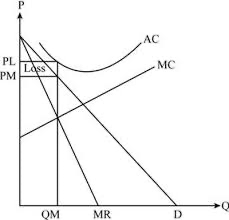

loss making monopoly

price on y axis

output on x axis

price from demand curve is lower than profit maximising price so firm makes a loss

summary of a monopoly

a pure monopoly is the sole supplier in an industry

as a result, the monopolist can take the market demand curve as its own demand curve

a monopolist therefore faces a downward sloping AR curve

with an MR curve falling at twice the rate of AR

where is profit maximised

where MR = MC

equilibrium profit maximising output point

this is where you track down from MR = MC

consumers will be willing to pay the price up for this output

perfectly competitive firms vs monopolise

perfectly competitive firms operate with allocate efficiency which means their output is where MC=P

monopolies set their output where MR=MC if they are profit maximising