ACCT 201 Chapter 9 : Flexible Budgets and Performance Analysis

1/17

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No study sessions yet.

18 Terms

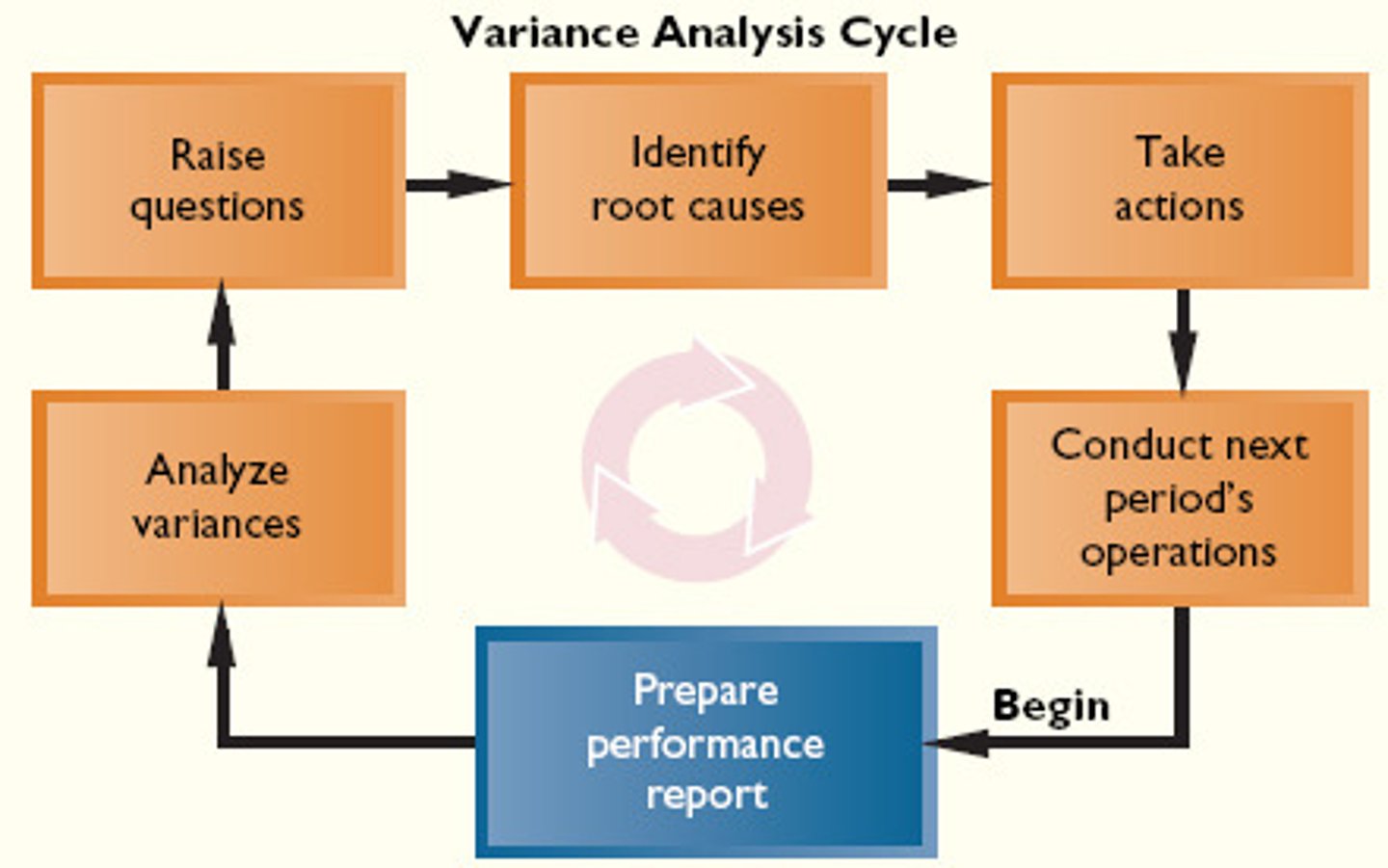

Variance Analysis Cycle

prepare performance report

analyze variances

raise questions

identify root causes

take actions

conduct next period's operations

Characteristics of flexible budget

Planning budgets are prepared for a single, planned level of activity

Performance evaluation

Performance evaluation is difficult when actual activity differs from the planned level of activity

Characteristics of Flexible Budgets Part 2

1.May be prepared for any activity level in the relevant range.

2.Show costs that should have been incurred at the actual level of activity, enabling "apples to apples" cost comparison.

3.Help managers control costs.

4.Improve performance evaluation.

Deficiencies of the Static Planning Budget

The greatest disadvantage of the static budget is its lack of flexibility. If a company establishes a budget based on a certain level of sales volume and that volume increases, it can't allocate additional resources to keep up.

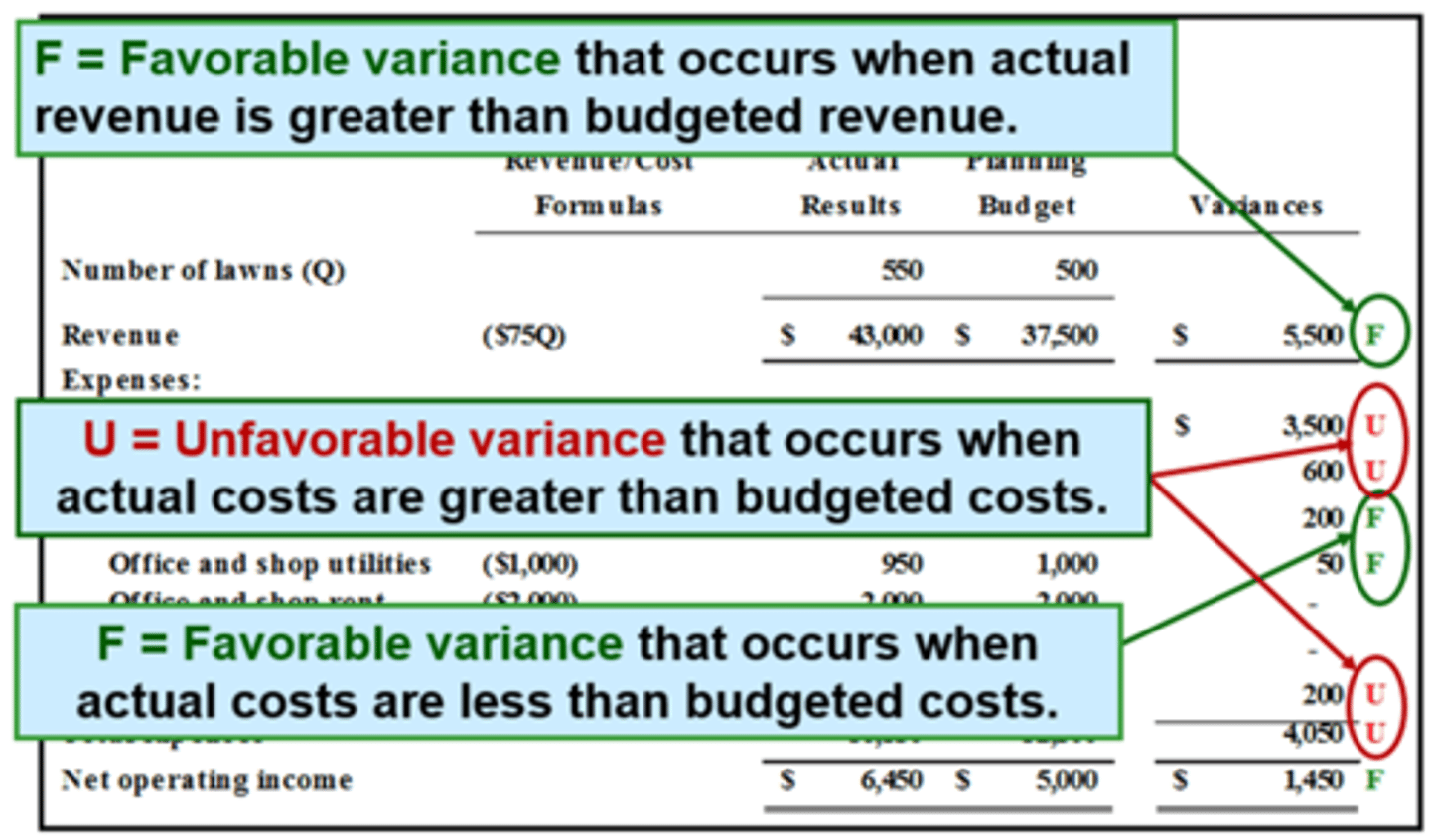

Larry's Lawn Service

The actual level of activity is greater than the planned level of activity. Therefore, actual variable costs are likely to be higher than planned variable costs regardless of Larry's managerial efficiency.

"How much of the cost variances are due to higher activity, and how much are due to cost control?"

we need to flex the planning budget to accommodate the actual level of activity.

Total variable costs change in direct proportion to changes in inactivity.

Total fixed costs remain unchanged within the relevant range.

Activity Variance

difference between planning budget and flexible budget

flexible budget

a projection of budget data for various levels of activity

Actual Revenue and Flexible Budget Revenue

the difference is a revenue variance

actual cost - flexible budget cost

the difference is a spending variance

Revenue Variance

The difference between the actual revenue for the period and how much the revenue should have been, given the actual level of activity. A favorable (unfavorable) revenue variance occurs because the revenue is higher (lower) than expected, given the actual level of activity for the period.

Spending Variance

the difference between the actual amount of the cost and how much a cost should have been, given the actual level of activity

flexible budget and planning budget

Activity variances are found by

Actual budget and flexible budget

Revenue and spending variances

Favorable/Unfavorable Variance

F=higher income, U=lower income when comparing budget and actual results.

*Flexible Revenue can be seen as actual when looking at planning budget.

Planning Budget

a budget created at the beginning of the budgeting period that is valid only for the planned level of activity