Economic methodology and the economic problem

1/55

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

56 Terms

What is economics?

The study of how people allocate scarce resources for production, distribution and consumption

What type of science is economics?

a social science - studies societies and human interactions

What is a positive statement?

A statement of fact that can be scientifically tested to see if it is correct or incorrect - objective

What is a normative statement?

A statement that includes a value judgement and can’t be refuted just by looking at the evidence - subjective

What is a need?

Something that is necessary for human survival e.g food

What is a want?

Something that is desirable but not necessary for survival e.g a phone

What is the central purpose of economics?

To produce goods and services to satisfy people’s needs and wants

Define economic welfare

The economic well-being of an individual, a group within society, or an economy

Define production

A process, or set of processes, that converts inputs into output of goods

What is a capital good?

A good which is used in the production of other goods or services

What is another term for a capital good?

Producer good

What is a consumer good?

A good which is consumed by individuals or households to satisfy their need or wants

Define factors of production

inputs into the production process

What are the four factors of production?

Capital

Enterprise

Labour

Land

Capital

goods that can be used in the production process e.g equipment, buildings, money

What is the reward/incentive for capital?

Interest from the investment

Labour

human capital, which is the workforce of the economy e.g people, time

What is the reward/incentive for labour?

wages

Land

natural resources e.g oil, coal, wheat water

What is the reward/incentive for land?

rent

Enterprise

Managerial ability. The entrepreneur is someone who takes risks, innovates, and uses the factors of production e.g ‘spark’, risk-taker, decision-maker

What is the reward/incentive for enterprise?

Profit- an incentive to take risks

What is the law of diminishing marginal returns?

a concept where at least one factor of production is fixed, showing that as an additional input is added, the additional product gained falls

What is a renewable resource?

A resource that can be replenished as it is used e.g solar

What is a non-renewable resource?

A resource that is scarce and runs out as it is used e.g oil

What is another word for a non-renewable resource?

Finite resource

What are free goods?

Goods that do not use up any factor inputs when supplied e.g fresh air. They have no opportunity costs

What is the fundamental economic problem?

How best to make decisions about the allocation of scarce resources among competing uses so as to improve and maximise human happiness and welfare

Define scarcity

When the demand for a good or service is greater than the availability of the good or service

What is an economic agent?

An entity that engages in economic activity e.g producers, consumers and governments

What is rationing?

A way of allocating scarce goods and services when market demand out-weighs the available supply e.g by age

Define opportunity cost

The cost of giving up the next best alternative

What are the key economic decisions?

What to produce? How to produce it? To whom the goods should be allocated to?

Why is the environment a scarce resource?

As there are limited natural resources on earth

What is economic methodology?

It involves the application of tested economic theories to explain real-world economic behaviour

What is a free market economy? Add an example

An economy without government intervention or regulation e.g US

What are features of a free market economy?

The market allocates resources

They are driven by the profit motive

The private sector dominates

There is limited role for state (government)

What is a command economy? Add an example

A system in which a central government makes all economic decisions e.g China

What are features of a command economy?

Most resources are state owned

Planning allocates resources

Little role for market prices

What is a mixed economy? Add an example

An economy that accepts both private businesses and nationalised government services e.g UK

What are features of a mixed economy?

Mix of state and private ownership

Government intervention in markets

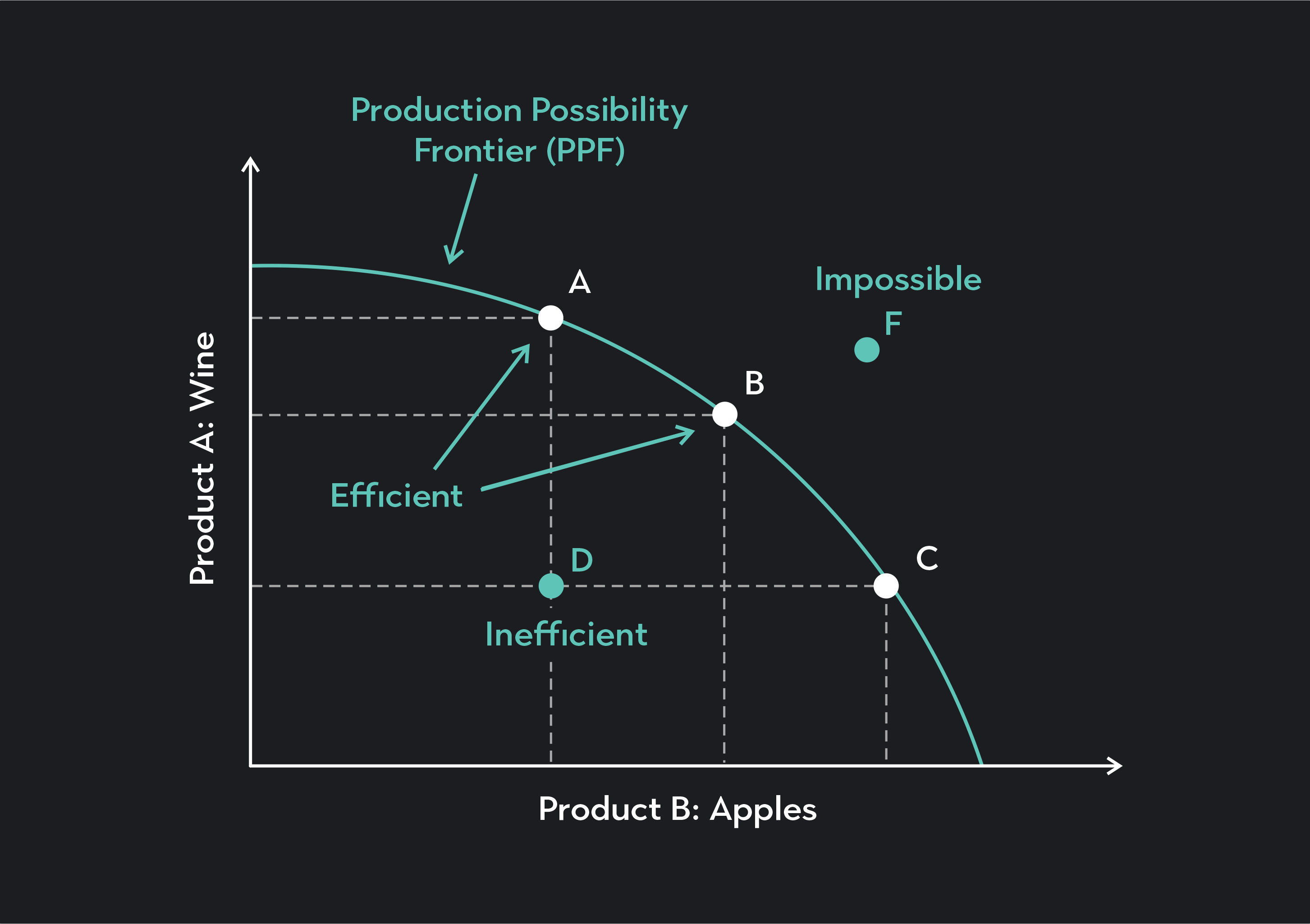

What is a production possibility frontier (PPF)?

a curve that shows various combinations of two goods or services attainable when all resources are fully and efficiently employed

Define productively efficient

When a firm is using all its resources in the most efficient way possible producing the maximum output with the minimum input

What part of a PPF is productively efficient?

All the points on the curve

What part of a PPF is productively inefficient?

Points inside the curve, not all resources are being fully utilised

What does it mean when a point is outside the PPF?

The combination is not yet attainable with the current resources

What is allocative efficiency?

When the particular mix of goods a society produces represents the combination that society most desires

What can cause a PPF to shift outwards?

Change in the quantity or quality of factors of production

Change in technology

Trade between countries

What can cause a PPF to shift inwards?

Resource depreciation

Recourse depletion

What is resource depreciation?

machinery falling apart due to not being maintained

What is resource depletion?

resources destroyed due to things like war and natural disasters

What does a straight line PPF mean?

It means there is a constant opportunity cost

What does a curved PPF mean?

It means there is an increasing opportunity cost

Define economic growth

the increase in the potential level of real output the economy can produce over a period of time

Define unemployment

when not all of those who are able and willing to work are employed

Define full employment

when all who are able and able to work are employed