Break-Even Analysis

1/24

Earn XP

Description and Tags

Business Management Chapter 32

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

Methods of Break-even Analysis

Table method

Graphical method

Calculation method

Table format

Quantity sold

Fixed costs

Variable costs

Total costs

Total revenue

Profit/Loss

Fixed Costs (FC)

Costs that do not vary with output or sales in the short term

Why are assets not part of fixed costs?

Fixed costs are constant whatever the amount of goods produced.

Also they are of recurring nature where business have to pay for these costs over the years.

Fixed costs and variable costs are also found in the statement of profit or loss.

Example includes rent, salaries, insurance and depreciation.

Technological investment and purchase of assets do not fulfil fixed costs because:

they are assets (and not expenses)

they are found in the statement of financial position (not profit or loss)

the "cost" is also once off and is not of recurring nature

they can also be "sold" so their value is not expensed away like all fixed costs

Their depreciation value are the true fixed costs.

Variable Costs (VC)

costs which vary with output (e.g. wages, materials per product)

VC = cost per unit x no. of products

Total Revenue (TR)

Total income from the sale of all units of a product during a given time period

TR = no. of products x price

Total Costs (TC)

TC = FC + VC

Profit

Profit = TR - TC

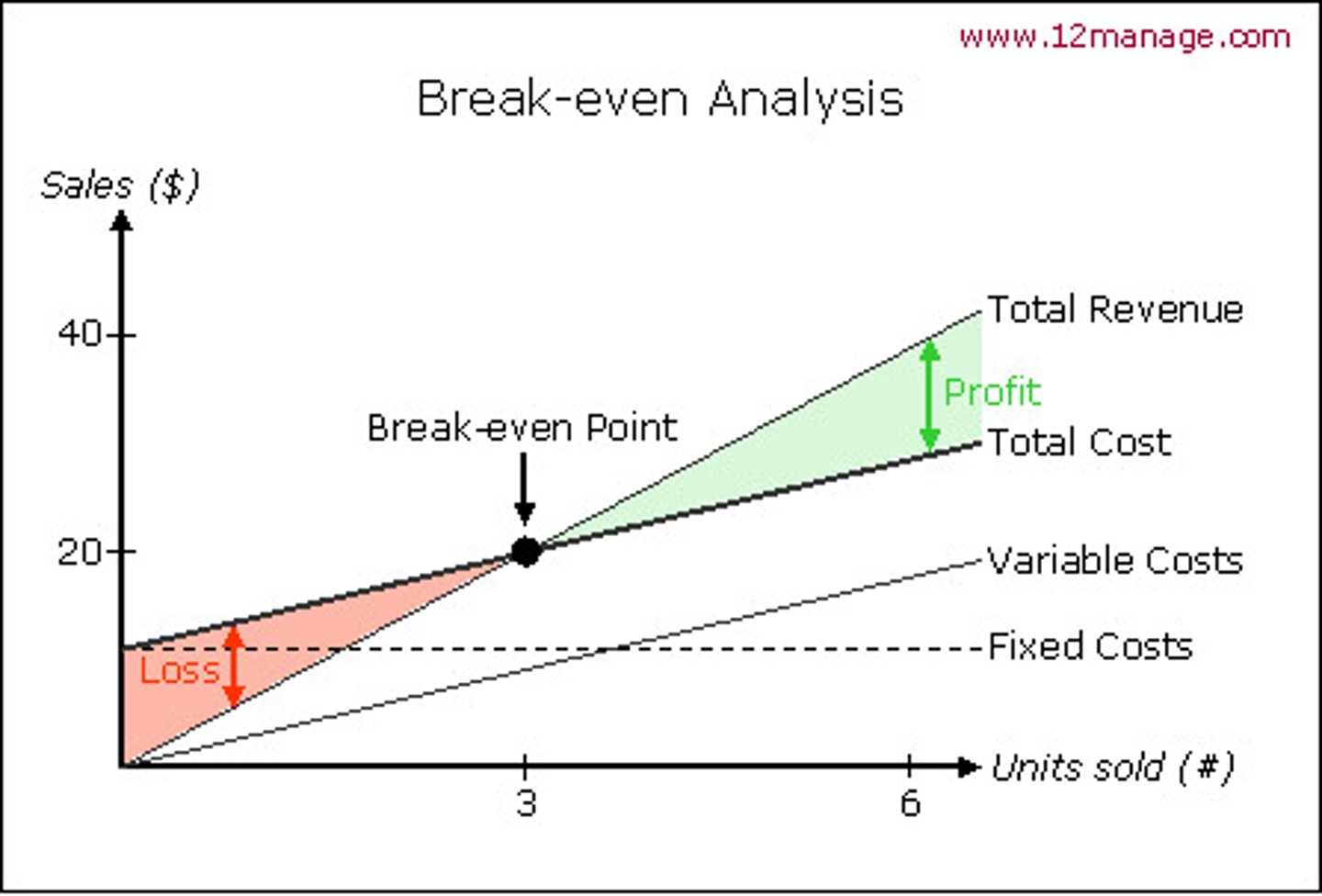

Break-even

Sales revenue of business covers all of its production costs

Profit = 0

Total revenue = Total cost

Break Even Quantity (BEQ)

Level of output where a business does not make either a profit or loss

BEQ = fixed costs / selling price - cost price (unique contribution)

Break-even point

Level of output at which total costs equals total revenue

remember to label with arrow!!! important to get marks

Margin of safety (MOS)

the amount by which the current output level exceeds the break-even level of output

MOS = total no. of products - BEQ

How to draw break even chart:

1) Title: Break even chart (underlined)

2) Axis: vertical - Sales/cost $ ('000), horizontal - Quantity '000

3) All lines

- FC: horizontal line

- VC: diagonal line from 0 to total VC

- TR: diagonal line from 0 to TR

- TC: diagonal line from FC to TC

4) BEP (MUST BE AT BEQ)

5) BEQ (dotted line)

6) Profit (bracket, TR - TC = P)

7) MOS (arrows, MOS = xx)

Total contribution

Unit contribution x Output

Contribution per unit

Contribution refers to the portion of unit sales revenue after per unit variable costs have been deducted. This portion is then available to be applied to fixed costs.

(Unique contribution)

selling price per unit - variable cost per unit

Target profit

value of profit that a firm aims to earn within a given time period

Target output

quantity of sales required for a firm to reach its target profit

Target profit output formula

Target output = (fixed costs + target profit) / contribution per unit

Revenue to achieve target profit formula

Target revenue = fixed costs + target profit / 1 - (variable cost per unit/price)

Target price

Amount customers need to pay per unit in order for the firm to break-even or reach a particular target profit

Break-even Target Price Formula

Break-even target price = (fixed costs/production level) + variable cost per unit

OR: (total cost + target profit)/quantity

Limitations of break even analysis

fully quantitative, ignores qualitative considerations, such as impact on employees who may need to work overtime in order to achieve break-even

doesn't take into account changes in external business environment which have direct impact on costs and revenues (e.g. inflation will increase production costs and wages)

prices are assumed to be constant but in real life they may not be constant (may change due to promotions and price discounts for loyal customers) costs are assumed to be constant but in real life they may not be constant (benefit from economies of scale as output increases → cheaper)

ideal for businesses that sell a single good or service (difficult for large range of goods as prices and production costs may differ)

relies on accuracy of cost and revenue data used to make predictions (inaccuracies and bias will invalidate results, difficult to allocate fixed costs accurately to various products in reality)

Graph issues:

TR may decrease

FC may not be entirely flat, incur additional costs

VC may fluctuate (economies of scale, diseconomies of scale)

there could be two BEQs (as TR decreases)

Qn: Explain how the introduction of new production methods will affect the total cost line in SSH's break-even chart.

The TC line will shift downwards (by $5000) [1].

The slope or gradient of the TC line will become flatter (less steep) [1].

Notes:

money and percentage should be in 2dp

dont assume the structure is fixed

read question carefully.

know the correct units. the units matter

Also please read the question very very carefully. For BE questions its very important that you know what figures are to be included and what not. In this case some students included the Fixed Asset costs and other made mistakes with the calculation of the Fixed Costs. Fixed Assets and Fixed Costs may sound the same but they are very different and needs to be treated very differently for your BEQ calculations. BEWARE!

Comment whether HH should outsource the production of meals to Meals Inc.

Based on the calculations above it may or may not be a good idea for HH to outsource to Meals Inc. Some of the reasons the students could comment on includes:

-The new BEQ at 14,400 does give the company a slightly larger margin of safety of 3600 (18,000-14400). And this might be a positive point. They would also own a higher profit of 14,400 (3600x4) an increase from 9000 before.

- There are however concerns about the quality of the meals being produced by Meal Inc and the increase in profits and MOS may not be considerable enough for HH to consider the decision to outsource. It should be also noted that outsourcing is not meant for the core activities of the business which in the case of HH would be the production of the meals.

Students can take either stand as long as they give an answer linking to HH and a discussion on outsourcing. They are highly encouraged to include the financial calculations in their answer.

[2 marks] for a comprehensive answer using the calculations similar to above

[1 mark] for an answer that is theoretical but shows some understanding of outsourcing.

Once again there were many who decided not to use the calculations from the previous section and that would have cost you marks. Also please be mindful that the question says ‘oursource’ so there must be something to do with that in your answer. Comment questions should not be treated like your definitions and be very brief.