Understanding Fraud: Types, Prevention, and Detection

1/186

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

187 Terms

Fraud

Wrongful deception for financial or personal gain.

Ponzi Scheme

Returns to investors come from new investors.

Confidence

Critical element for successful fraud.

Employee Fraud

Fraud committed against an organization by employees.

Fraud on Behalf of Organization

Fraud typically committed by executives.

Occupational Fraud

Misuse of occupation for personal enrichment.

ACFE

Association of Certified Fraud Examiners.

Asset Misappropriation

Theft or misuse of organizational assets.

Corruption

Fraudsters misuse influence for personal benefit.

Fraudulent Financial Statements

Falsification of an organization's financial records.

Employee Embezzlement

Most common occupational fraud type.

Vendor Fraud

Fraud perpetrated by vendors against organizations.

Customer Fraud

Fraud committed by customers against organizations.

Direct Fraud

Employee steals cash or assets directly.

Indirect Fraud

Employee takes bribes or kickbacks.

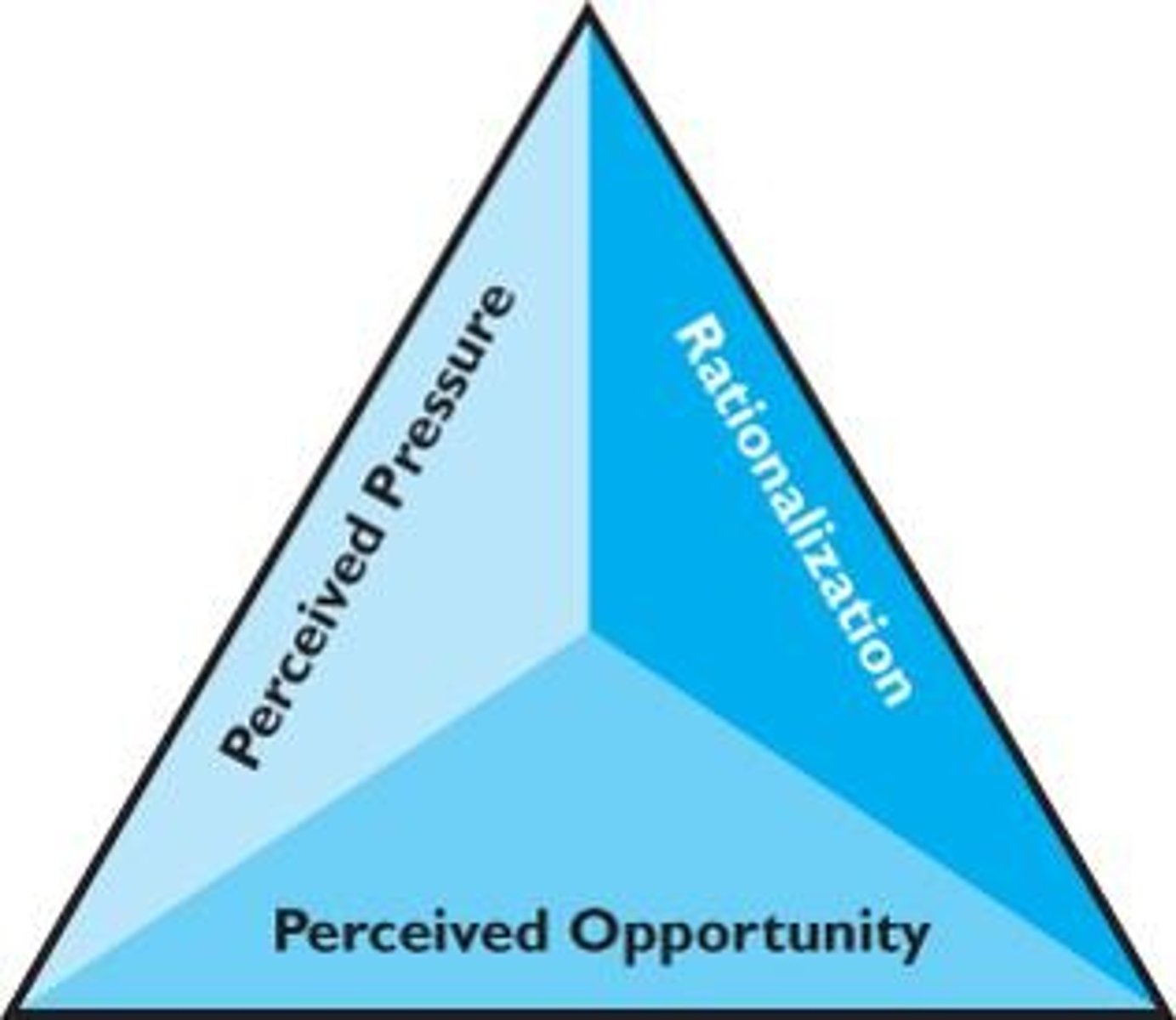

Fraud Triangle

Three elements: pressure, opportunity, rationalization.

Perceived Pressure

Real or perceived pressure by the perpetrator.

Perceived Opportunity

Ability to conceal the fraud.

Rationalization

Justifying fraud as acceptable behavior.

Fire Triangle

Elements of fraud prevention: pressure, opportunity, rationalization.

Financial Pressures

Monetary issues causing stress leading to fraud.

Vice Pressures

Addictions or personal vices prompting fraudulent behavior.

Work-Related Pressures

Job stress or dissatisfaction influencing fraud.

Other Pressures

Various external factors contributing to fraudulent actions.

Fraud Opportunity Factors

Six factors increase chances of committing fraud.

Internal Control

Framework ensuring reliability, efficiency, and compliance.

COSO

Committee aiding businesses in internal control enhancement.

COSO Framework

Standard for auditing internal controls over financial reporting.

Control Environment

Foundation of internal control, influenced by management's tone.

Management's Role

Leads by example, modeling appropriate behaviors.

Effective Communication

Critical for conveying appropriate conduct and training.

Organizational Structure

Clear responsibilities enhance accountability and control.

Internal Audit Department

Cornerstone of governance, deters fraudulent activities.

Tone at the Top

Management's attitude towards internal controls affects culture.

Audit Trail

Documentation supporting transactions to detect fraud.

Control Activities

Procedures ensuring employee actions align with goals.

Segregation of Duties

Dividing responsibilities to reduce fraud risk.

Authorizations

System ensuring transactions are approved appropriately.

Physical Safeguards

Protecting assets from theft through physical means.

Independent Checks

Verification processes to ensure accuracy and compliance.

Documents and Records

Maintaining accurate records for accountability and auditing.

SAPID Acronym

Reminds of five control activities: S, A, P, I, D.

Preventive Controls

Activities designed to stop fraud before it occurs.

Detective Controls

Activities that identify fraud after it occurs.

Disciplining Fraud Perpetrators

Necessary to deter repeat offenses in fraud cases.

Audit Oversight

Board of Directors' role in monitoring management.

Compliance with Laws

Ensuring operations adhere to legal regulations.

Asymmetrical Information

One party has information that another lacks.

Fraud Power

Types of influence used by fraud perpetrators.

Reward Power

Convincing victims of benefits from fraud participation.

Coercive Power

Instilling fear of punishment for non-participation.

Perceived Expert Power

Influencing others based on claimed expertise.

Legitimate Power

Convincing others of one's rightful authority.

Referent Power

Relating to potential co-conspirators for influence.

COSO Framework

Five components for effective internal control systems.

Control Environment

Foundation of an organization's internal control system.

Risk Assessment

Identifying and managing areas of potential risk.

Control Activities

Policies and procedures to mitigate risks.

Information and Communication

Sharing relevant information for effective controls.

Monitoring Activities

Assessing internal control performance over time.

Segregation of Duties

Separating responsibilities to prevent fraud opportunities.

Authorization

Approval processes for transactions and activities.

IT Processing Controls

Controls over data processing and security.

General Controls

Controls over data center and network operations.

Application Controls

Controls for individual accounting applications.

Fraud Prevention

Activities aimed at stopping fraud before it occurs.

Fraud Detection

Identifying symptoms or indicators of fraud.

Ethical Maturity Model (EMM)

Framework explaining unethical decision-making.

Independent Checks

Auditor evaluations to detect fraud.

Fraud Symptoms

Indicators associated with potential fraudulent activity.

Fraud Detection Methods

Three primary ways to identify fraud.

Whistle-blower Mechanism

Anonymous reporting system for fraud suspicions.

Predication

Foundation for starting a fraud investigation.

Purpose of Investigation

To determine if fraud or error exists.

Types of Evidence

Classified by evidence type produced during investigations.

Testimonial Evidence

Information gathered from interviews and interrogations.

Documentary Evidence

Evidence from written or digital sources.

Physical Evidence

Tangible items linked to dishonest acts.

Personal Observation

Evidence sensed by investigators through observation.

Fraud Motivation Triangle

Search for pressures, opportunities, and rationalizations.

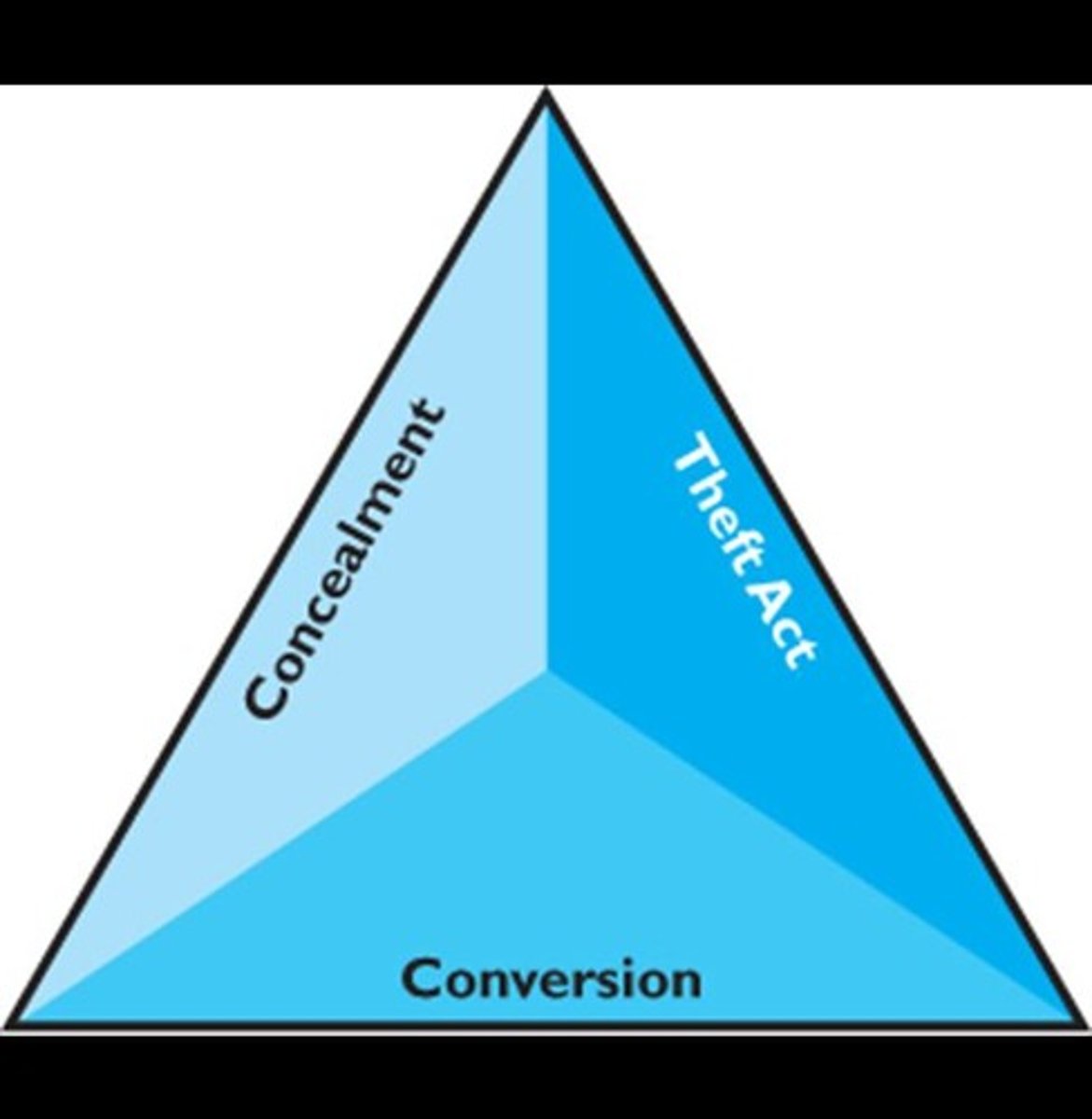

Fraud Elements

Three components: theft, concealment, and conversion.

Theft Act

Gathering information on how theft was committed.

Concealment

Focus on hiding methods used by perpetrators.

Conversion

Investigating how stolen goods are spent.

Internal Control Limitations

Factors that undermine effective fraud prevention.

Management Override

Management decisions that bypass internal controls.

Human Errors

Mistakes due to carelessness or misunderstanding.

Collusion

Employees collaborating to bypass internal controls.

Whistle-Blowing System Elements

Key features for effective reporting of misconduct.

Anonymity in Reporting

Protection against retribution for whistle-blowers.

Proactive Fraud Audits

Four steps to identify and investigate fraud risks.

Current Fraud Model

Four stages: incident, investigation, action, resolution.

Fraud

Deceptive act for personal gain.

Positive Tone at the Top

Management's commitment to ethical behavior.

Education and Training

Informing employees about fraud seriousness.

Integrity Risk Assessment

Evaluating potential fraud risks in operations.

Internal Control System

Processes to safeguard assets and ensure accuracy.

Reporting System

Mechanism for reporting suspected fraud incidents.

Monitoring System

Continuous oversight to detect fraud activities.

Proactive Fraud Detection

Methods to identify fraud before it occurs.