Economics (Terms)

1/25

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

26 Terms

The size of the bid-offer spread that the dealer offers to clients depend on what factors

Primary Factors

1. The currency pair involved: Liquidity in major currency pairs is generally higher than

that in less popular pairs.

2. The time of the day: The interbank market is most liquid when major trading centers

are open.

3. Market volatility: If market volatility is high, bid-offer spreads will be high.

Secondary Factors

1. The size of the transaction: The larger the transaction size, the wider the bid-offer

spread.

2. The relationship between the dealer and the client: In order to secure regular business

from the client in foreign exchange as well as in other asset classes, the dealer may offer

tight bid-offer spreads.

3. Client’s credit profile: If the client has a poor credit history, the dealer may offer a wider

bid-offer spread.

International parity conditions

Covered interest rate parity

Uncovered interest rate parity

Forward rate parity

ex-ante version of PPP

international Fisher effect

Covered interest rate parity

states that an investment in a foreign money market

instrument that is completely hedged against exchange rate risk should yield exactly the

same return as an otherwise identical domestic money market investment.

Uncovered interest rate parity

states that the expected return on an un-hedged foreign

currency position should equal the return on a similar domestic currency investment

Forward rate parity

states that the forward exchange rate will be an unbiased predictor of the future spot exchange rate if covered interest rate parity and uncovered interest rate parity hold

ex-ante version of PPP

states that ‘expected’ changes in spot exchange rates are driven by ‘expected’ inflation differentials:

international Fisher effect

states that if uncovered interest rate parity and ex ante PPP hold, the foreign-domestic nominal yield spread is determined solely by the foreign domestic expected inflation differential.

Current vs Capital Account

Current account reflects trade in goods/services; capital account reflects financial/investment flows

• Current account balance must be matched by an equal and opposite capital account balance.

• Current account balance has a long-term impact on exchange rates.

• Investment/financing decisions have a short-term impact on exchange rates.

The flow supply/demand channel

A current account surplus indicates high demand for the domestic currency which would cause the currency to appreciate. Over time the currency would lose its competitiveness resulting in a decline in exports and rise in imports, making the surplus hard to maintain. The opposite would be true in the case of deficits

The portfolio balance channel

Current account balances result in a shift of wealth from deficit running countries to surplus running countries. As countries with significant surpluses realize that their level of foreign reserves is much higher than required, they may attempt to reduce their foreign currency reserves, putting them under downward pressure

The debt sustainability channel

Countries that run persistent current account deficits will see their foreign debt levels rising gradually. However, there should be an upper limit to the amount of foreign debt a country can take. If investors see the foreign debt levels of a country rising to unsustainable levels, they would see a currency depreciation necessary in order to narrow the current account deficit and take the foreign debt to a more manageable level.

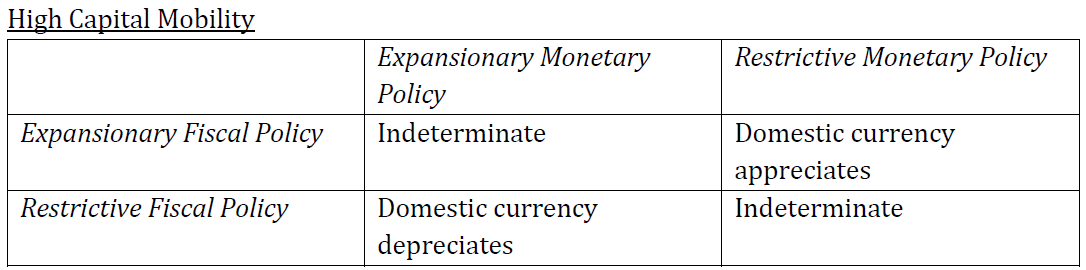

The Mundell-Fleming model - High Capital Mobility

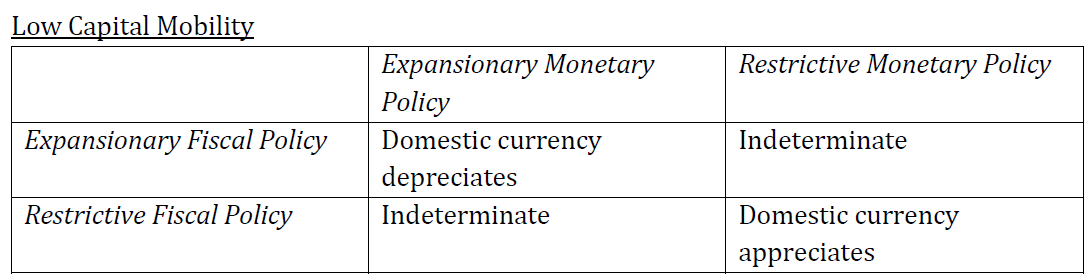

The Mundell-Fleming model - Low Capital Mobility

Basic monetary approach

Assumes that PPP holds at all times, therefore an increase in money supply results in an increase in inflation and a depreciation of the domestic currency

Dornbusch model

As money supply increases in the short run, price levels will not increase, rather, the higher money supply will cause short-term interest rates to decline, leading to a capital outflow which in turn will cause the domestic currency to depreciate below its long-term equilibrium value. In the long run, as domestic interest rates rise, the currency will appreciate and the exchange rate will move in line with its long-term equilibrium value.

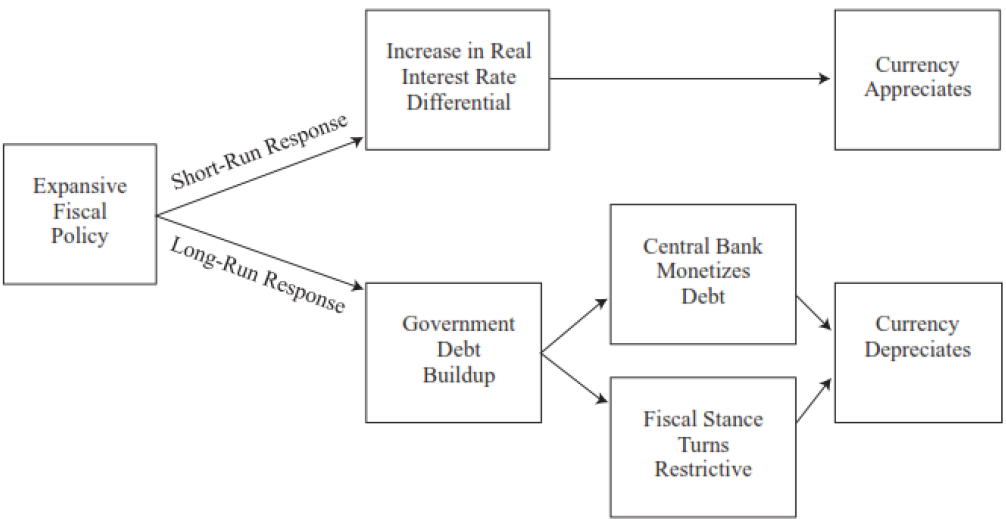

The portfolio balance approach

The Mundell-Fleming model focuses on the short-run; it does not consider the long-run impact of budgetary imbalances. The portfolio balance approach addresses this limitation

The effectiveness of government intervention depends on

the ratio of central bank FX reserves and FX turnover. If the ratio is low (developed market) then government intervention will have low impact.

Under the mundell fleming model, is fiscal/monetary more effective in high/low capital mobility?

Monetary → High Capital Mobility

Fiscal → Low Capital Mobility

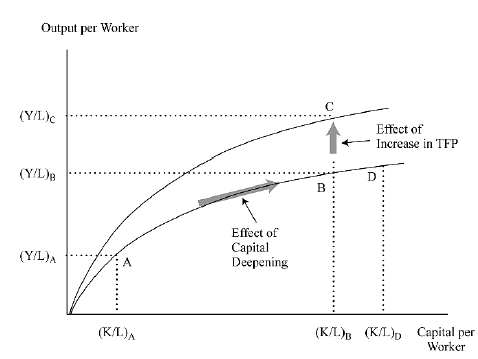

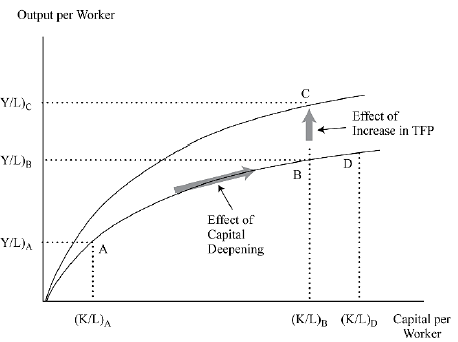

Capital deepening

means an increase in the capital to labor ratio. It is shown by a move along the production function from point A to point B. Adding more and more capital to a fixed number of workers increases per capita output but at a decreasing rate.

Technological progress

represented by an increase in total factor productivity, causes an upward shift in the entire production function. As a result, the economy can produce higher output per worker for a given level of capital per worker. This is shown by the move from B to C

Absolute convergence

implies that developing countries, regardless of their particular

characteristics, will eventually catch up with the developed countries and match them in

per capita output

Conditional convergence

implies that convergence is conditional on the countries having

the same saving rate, population growth rate and production function. If these conditions

hold, the model implies convergence to the same level of per capita output as well as the

same steady state growth rate.

Club convergence

implies that only rich and middle-income countries that are members of the club (countries which develop appropriate legal, political and economic systems; open

trade and capital flow)are converging to the income level of the richest countries of the

world. Countries with the lowest per capita income in the club grow at the fastest rate.

However, countries outside the club without appropriate institutional structures may fall

into a non-convergence trap

Classical Model (also called Malthusian Theory)

Growth in real GDP per capita is temporary.

• Rise in real GDP per capita above subsistence level results in a population explosion.

• And the real GDP per capita returns to subsistence level.

Neo-Classical Model

• In the steady state capital per worker and output per worker grow at equal

sustainable rates.

• Long-run per capita growth depends on exogenous technological progress.

• Capital deepening has no impact on growth rate or on the marginal product of

capital.

• There will be a convergence of per capita income in developing and developed

countries.

Endogenous Growth Theory

• Focus on explaining technological progress rather than treating as exogenous.

• It states that there is no reason why incomes of developed and developing countries

should converge.

• A higher saving rate can lead to a permanently higher growth ra