Industrial Economics (1)

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

Perfect Competition Assumptions

1) There are many buyers and sellers

2) Firms produce homogeneous products

3) Perfect information

4) Easy entry and exit

5) Firms act independently

6) No transport costs

Perfect Competition Short Run

Horizontal demand curve - P = MR = AR

P is set at the supply and demand equilibrium

MC upward sloping - MC = MR is profit max. output

AC is U-shaped - intersecting MC below demand curve

Abnormal profits

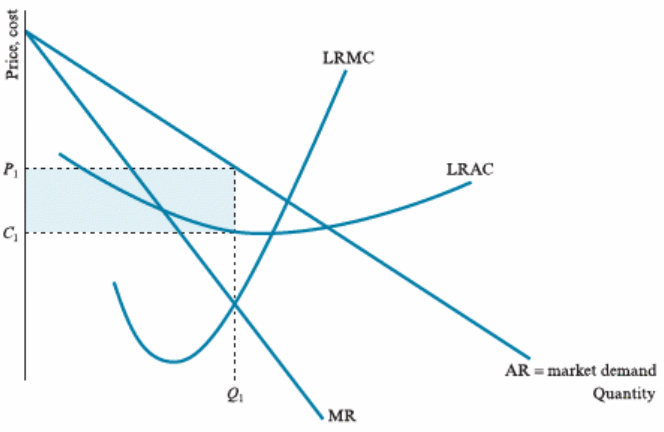

Perfect Competition Long Run

More firms enter due to abnormal profits - ↑ supply

Demand lowers until it is tangent with AC

Firms produce at min AC with no profit in the long run

Perfect Competition critiques

1) Unrealistic assumptions - product differentiation is a common fact

Monopolistic Competition (Chamberlin

1933) assumptions

Monopolistic Competition Short Run

Downward-sloping AR (demand)

MR below AR - steeper

MC upward sloping

Monopolistic Competition Long Run

Demand curve (AR) shifts down

AC tangent to AR at profit-maximising output - normal profits in the long-run

Chamberlin vs Dixit & Stiglitz

Chamberlin: Product differentiation is always better for society.

Dixit & Stiglitz: Disagree with Chamberlin. Considering total social surplus (Consumer Surplus + Firm Profits); more is not always better.

Bains definition of barriers to entry

Any obstacle to entry by new firms that allows incumbents to maintain prices that yield long-run abnormal profits.

Bains' 4 types of barriers to Entry

1) Product Differentiation Barriers - highly differentiated products and an established brand image (possibly created by advertising) (e.g. Coca-Cola)

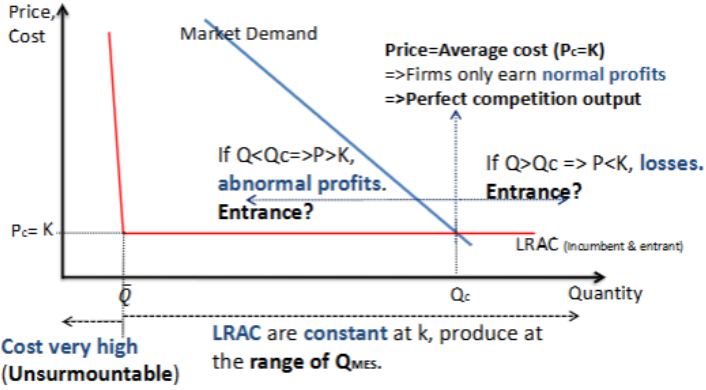

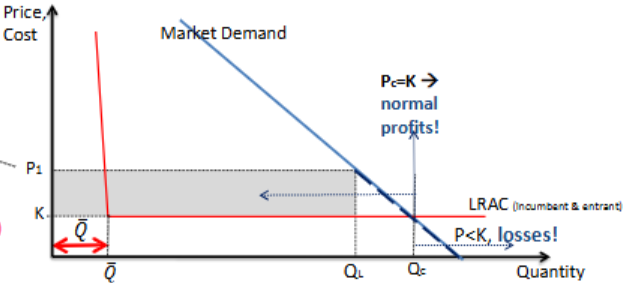

2) Scale Economies Barrier - Technical economies of scale (L-shaped Average cost curve) + Pecuniary economies of scale (Barriers generated by paying less for inputs) (e.g. Tescos)

3) Absolute Cost Advantage Barrier - produce any quantity of output at a lower cost

4) Initial Capital Requirement Barrier - start up costs

Bains definition of Limit Pricing

“The highest common price which the established sellers believe they can charge without inducing at least one potential entry”

Assumptions of Modigliani’s model of limit pricing (with economies of scale)

1) One incumbent and one potential entrant

2) Perfect information about the industry

3) Single homogenous product, perfect substitution

4) Economies of scale for both the incumbent and potential entrant (L-shaped LRAC curve)

Sylos’s Postulate

The entrant assumes that, when entering a new industry, incumbent firms will not respond to entry by changing their output levels

Limit Pricing Model (with economies of scale)

Incumbents output choice

> Incumbent chooses QL as it delivers abnormal profits and prevents entry:

Entrant needs a Q(bar) or higher to avoid high cost (exploit economies of scale)

If entrant produces Qe = Q(bar) then total market output would equal Qc (QL + Q(bar)) which means normal profits (NO ENTRY)

If entrants produce Qe = Q(bar) + 1 then total market output would be greater than Qc which means losses (NO ENTRY)

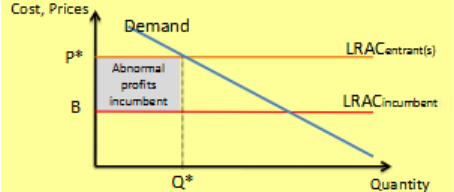

Modigliani’s model of limit pricing (with cost advantage)

> Same assumptions as the previous model

> But the incumbent has a cost advantage (e.g. due to a more efficient workforce)

> Incumbent set Q* and P* - if a potential entrant introduces a unit of output, it will push prices below its LRAC, making it unprofitable

3 Critiques of Modigliani’s Model

1) Ignores other barriers to entry, such as product differentiation - according to Bain had an important role

2) Sylos Postulate seems unrealistic - incumbent firms will change their outputs in response to entry

3) Perfect information about an industry is unrealistic

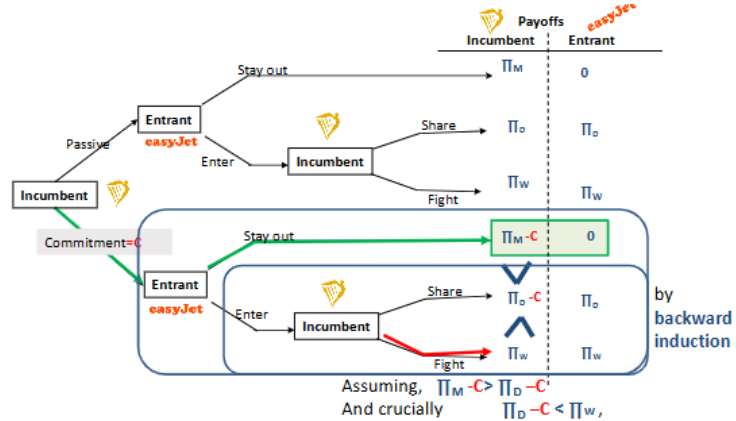

Dixit Model

In this model, investment by incumbents (e.g. advertising) can be seen as a sign of their willingness to fight for their market share (a sign of commitment), which can deter entrants.

Dixit Model Airline Industry Example

Can the incumbent remain passive and prevent entrance?

Yes if:

> the incumbent has a reputation for being tough (i.e. willing to fight a price)

> Imperfect information - not enough information about the incumbent’s commitment

Monopoly assumptions

1) A large number of buyers but only one seller

2) Complete product differentiation (no substitutes)

3) Only aims to maximise profits

4) No free entry at all

Monopoly graphically

> Monopolist supply (industry supply) = MC

> Industry demand = monopolist demand

> Profit maximisation: MR = MC

Monopolist Output (Q*m)

1) Profit = PQ - cQ

2) substitute P = a - Q into the profit function

3) Profit = (a - Q)Q - cQ, which becomes aQ - Q2- cQ

4) Derive the equations with respect to Q and get a - 2Q - c = 0

5) In the MR=MC form, it becomes a - 2Q = c

6) Isolating for Q, we get Q*m = 1/2(a - c)

Monopolist Profit (P*m)

1) Substitute Q*m into P = a - Q

2) We get P = a - 1/2(a - c); P = 2a - a + c / 2

3) P*m = a + c / 2

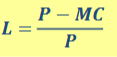

Lerner Index

> A way to assess the market power

> In Perfect competition (where P = MC), the Lerner Index is 0

> In a Monopoly (where P > MC or an extreme case where MC = 0), the Lerner index is greater than 0 or 1

Rocket and Feather hypothesis

> Another way to assess market power

> If a firm has a strong market power:

When cost increases (MC goes up) → Firm raises prices to keep mark-up P-MC

When costs fall (MC goes down) – Firm cuts prices slowly to enjoy a greater mark-up P - MC

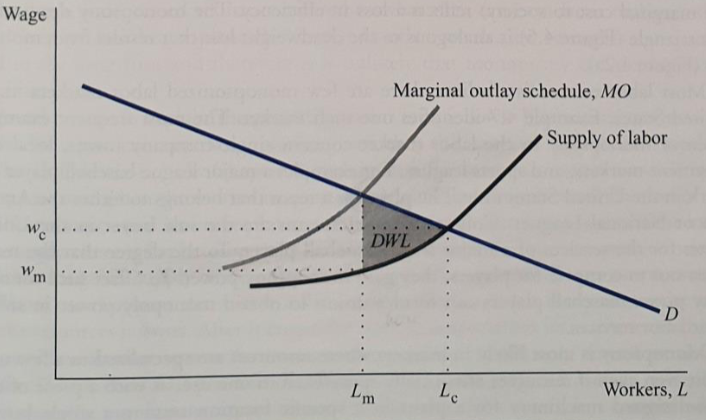

Monopsony

A market with only one buyer who can exert market power over a large number of sellers.

Monopsony assumptions

1) Single homogenous product

2) Single intermediary who trades this product in two markets: Producers Market and Final Market (e.g., Tesco)

3) Intermediary aims to maximise profits

4) NO-free entry-exit

5) Timing: producers announce their supply conditions, so the monopsony buyer sets the price.

Monopsony Graphically

> Monopsony hires workers (Lm) where D = MO

> Pays Wm wages which is lower than competitive wages

> DWL is the gap between the demand curve and supply curve at that unit of labour hired.