REG

1/98

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

99 Terms

When is a taxpayer considered married filing jointly versus single for tax purposes?

Taxpayers are considered married (and can file jointly) if they are legally married on the last day of the tax year.

Taxpayers are considered single if they are not married or legally separated by the last day of the year.

Key point: Marital status on December 31 determines filing status, not whether they lived together during the year.

How does the dependent child requirement differ for Qualifying Surviving Spouse (QSS) versus Head of Household (HoH) filing status?

Qualifying Surviving Spouse:

Dependent child must live with the taxpayer for the entire year (whole year).

Child must be a biological, adopted, or stepchild who meets the Qualifying Child test.

Head of Household:

Dependent child (or other qualifying person) must live with the taxpayer for more than half the year (not the entire year).

The dependent must be a qualifying child or relative who meets dependency rules and relationship requirements.

Key Point:

QSS requires the child in the home the entire year, HoH requires a qualifying person living in the home for more than half the year.

What does the CARES acronym stand for in the Qualifying Child dependent test, and what are the key requirements for each?

CARES is a mnemonic to remember the Qualifying Child tests:

C – Close Relative: Child must be your son, daughter, stepchild, foster child, sibling, or a descendant of these.

A – Age Limit: Under 19, or under 24 if a full-time student, or any age if totally disabled.

R – Residency and Filing Requirement: Must live with you for over half the year; must be U.S. citizen or resident of U.S./Canada/Mexico; cannot file a joint return (unless only to get a refund).

E – Eliminate Gross Income Test: No gross income limit applies to qualifying children.

S – Support Test: Child must not provide over half of their own support (scholarships excluded if full-time student & child of taxpayer).

SUPORT summarizes the tests to claim a Qualifying Relative:

S – Support Test: Taxpayer must provide more than half of the dependent’s total support.

U – Under Gross Income Limit: Dependent’s taxable gross income must be below the threshold (e.g., $4,700 for 2023).

P – Precludes Dependent Filing a Joint Return: Dependent cannot file a joint return unless it's solely for a refund.

O – Only Citizens or Residents: Dependent must be a U.S. citizen, resident of U.S./Canada/Mexico, or U.S. national.

R – Relative Test: The dependent must be related to the taxpayer (closely related family members) or

T – Taxpayer Lives With Individual All Year: If not a relative, the dependent must have lived with the taxpayer for the entire year.

All these tests must be met to claim a qualifying relative.

Children of Divorced Parents — Who Can Claim the Child as a Dependent?

The parent who has custody for the greater part of the year claims the child as a dependent.

This is determined by the time test (where the child spends more than half the year), not the divorce decree.

It does NOT matter who provides more than half of the child's support.

If custody is equal (50/50), the parent with the higher adjusted gross income (AGI) claims the child.

Are free goods or services provided by anemployer to employees taxable income? Whenare discounts taxable?

Free goods/services are generally taxableincome at fair market value unlessspecifically excluded.

If employer sells goods to employees at adiscount, not taxable if discount does notexceed employer’s cost.

Any discount below employer’s cost =>excess amount is taxable income.

If employer sells services at a discount,discount up to 20% of fair market value isnontaxable; excess is taxable income.

Small or minimal fringe benefits (deminimis), like free coffee or snacks, are nottaxable.

When is interest on U.S. Series EE Savings Bondstax-exempt?

Flashcard Back:

Interest on U.S. Series EE Savings Bonds is tax-exempt if all the following conditions are met:

Used to pay for qualified higher educationexpenses (tuition, fees) for taxpayer,spouse, or dependents (reduced by tax-freescholarships)

Taxpayer is over age 24 when bond wasissued

Bonds are owned solely by the taxpayer orjointly with spouse (no child co-owners)

Married taxpayer filing jointly

Taxpayer’s modified AGI is within theallowable limits (phased out at higherincome)

What is the ex-dividend date, and how does itaffect whether you receive a dividend?

Ex-dividend date is the cutoff date to beentitled to the next dividend.

To receive the dividend, you must purchasethe stock before the ex-dividend date.Buying on or after this date means nodividend.

Qualified Dividends Holding Period:

To get the preferential tax rate ondividends, you must hold the stock for morethan 60 days during the 120-day periodthat starts 60 days before the ex-dividenddate.

Example:

Ex-dividend date: June 30

120-day period: May 1 (60 days before) toAugust 29 (60 days after)

Buy stock on June 1 (before June 30) →eligible for dividend

Hold stock more than 60 days after June 1→ sell after August 1 for qualified dividendtax rate

Sell on July 1 (only 30 days held) → dividendtaxed at ordinary income rates (non-qualified)

Flashcard: When Are Early Withdrawals Penalty-Free from 401(k), Traditional IRA, and Roth IRA?

& Traditional IRA:

Age 59½ or older — no 10% penalty

Exceptions (HIMDEADDA):

H: Homebuyer (first-time, up to$10,000)

I: Insurance (unemployed payinghealth premiums)

M: Medical expenses (exceeding 7.5%AGI)

D: Disability

E: Education expenses (qualifiedhigher education)

A: IRS levy

D: Death (beneficiaries)

D: Substantially equal periodicpayments (SEPP)

Roth IRA:

Contributions withdrawn anytime tax- andpenalty-free

Earnings withdrawn penalty-free if:

Age 59½ or older

Roth IRA held for at least 5 years ("5-year rule")

Exceptions like Traditional IRA(HIMDEADDA) apply to earningswithdrawals before 59½

Trump Accounts

What is it?

Tax-deferred investment account forchildren under age 18 with a Social Securitynumber.

Functions like a traditional IRA but withspecial rules until the child turns 18.

No distributions allowed before the yearthe beneficiary turns 18.

After age 18, treated like a traditional IRA(including early withdrawal penaltiesbefore 59½).

Earnings are taxed as ordinary incomewhen distributed.

Contributions with basis (e.g., made byparents or the child) are nontaxable ondistribution.

Contributions without basis (employer orfederal government) are taxable ondistribution.

Employer and federal contributions areexcluded from income but do not establishbasis.

Maximum annual contribution: $5,000 (nodeduction allowed).

Federal program grants $1,000 contributionat birth (for eligible children born 2025–2028).

Flashcard: Taxable Portion of Annuity Payments

Fixed-Term (Fixed Period) Annuity:

Expected Value = Payment amount ×Number of payments

Exclusion Ratio = Original investment ÷Expected Value

Nontaxable portion per payment =Exclusion Ratio × Payment amount

Taxable portion per payment = Paymentamount – Nontaxable portion

Example:

Investment = $60,000, Payments = $750 × 120months = $90,000 expected value

Exclusion Ratio = 60,000 ÷ 90,000 = 2/3 (66.7%)

Taxable portion per payment = $750 × (1 – 2/3) =$250 (approx)

Lifetime (Life) Annuity:

Use IRS life expectancy factor (months)based on age

Nontaxable portion per payment = Originalinvestment ÷ Life expectancy factor

Taxable portion per payment = Paymentamount – Nontaxable portion

After expected payments are reached, allsubsequent payments are fully taxable

Example:

Investment = $60,000, Life expectancy = 260months

Nontaxable portion = $60,000 ÷ 260 = $230.77

Taxable portion = Payment – $230.77

Divorce Date Impact on Alimony Taxability &Payment Shortfall Allocation

Divorce/separation agreement executedon or before December 31, 2018:

Alimony received is taxable income torecipient

Alimony paid is deductible by payor

Divorce/separation agreement executedafter December 31, 2018:

Alimony received is NOT taxable

Alimony paid is NOT deductible

Payment shortfall allocation:

Payments due for both child supportand alimony are first applied to childsupport obligation

Remaining payments, if any, apply toalimony

Example: If $5,000 owed ($3,000 childsupport + $2,000 alimony) but only$4,000 paid, $3,000 covers childsupport fully, $1,000 applies toalimony

How are Social Security benefits taxed?

Back:

Taxable amount depends on ModifiedAdjusted Gross Income (MAGI) and filingstatus.

Calculate MAGI = AGI + Tax-ExemptInterest + 50% of Social Security benefits.

Taxability Thresholds:

Low Income: MAGI ≤ $25,000 (single) or ≤$32,000 (MFJ) → No tax on benefits.

Middle Income: MAGI between $25,000–$34,000 (single) or $32,000–$44,000 (MFJ)→ Up to 50% of benefits taxable.

High Income: MAGI > $34,000 (single) or >$44,000 (MFJ) → Up to 85% of benefitstaxable.

Maximum taxable amount = 85% of SocialSecurity benefits.

Use IRS worksheets to determine exact taxableportion, but generally know the range and max.

Tuition Reduction Tax Rules for GraduateTeaching & Research Assistants

Tuition reductions are taxable if they arecompensation for teaching or researchduties (i.e., payment for services).

Reduction only excludable if it is "inaddition to pay" (not compensation).

Graduate student tuition reductions tied towork = taxable income.

Undergrad assistants have broaderexclusion rules (tuition reductions generallyexcluded even if part of pay).

Foreign-Earned Income Exclusion (FEIE) — KeyRules

Allows U.S. citizens/residents workingabroad to exclude up to $120,000 (2026amount) of foreign-earned income fromU.S. taxable income.

Must meet either:

• Bona Fide Residence Test — resident of aforeign country for an entire tax year, or

• Physical Presence Test — present inforeign country 330 full days in any 12-month period.Exclusion limited to actual foreign-earnedincome minus the foreign housing exclusion(max housing exclusion = 16% of FEIE).

Excluded income still affects tax ratecalculations on other income.

Eligible taxpayers must file IRS Form 2555 toclaim.

Early Withdrawal Penalty on 1099-INT — TaxTreatment

Bank reports full interest earned on 1099-INT, even if part is forfeited due to earlywithdrawal penalty.

You must include full interest income onyour tax return (cannot net penalty againstinterest).

The early withdrawal penalty is deductedas an adjustment to arrive at AGI (above-the-line deduction).

This adjustment reduces your gross incometo reflect interest actually received,preventing double taxation of forfeitedinterest.

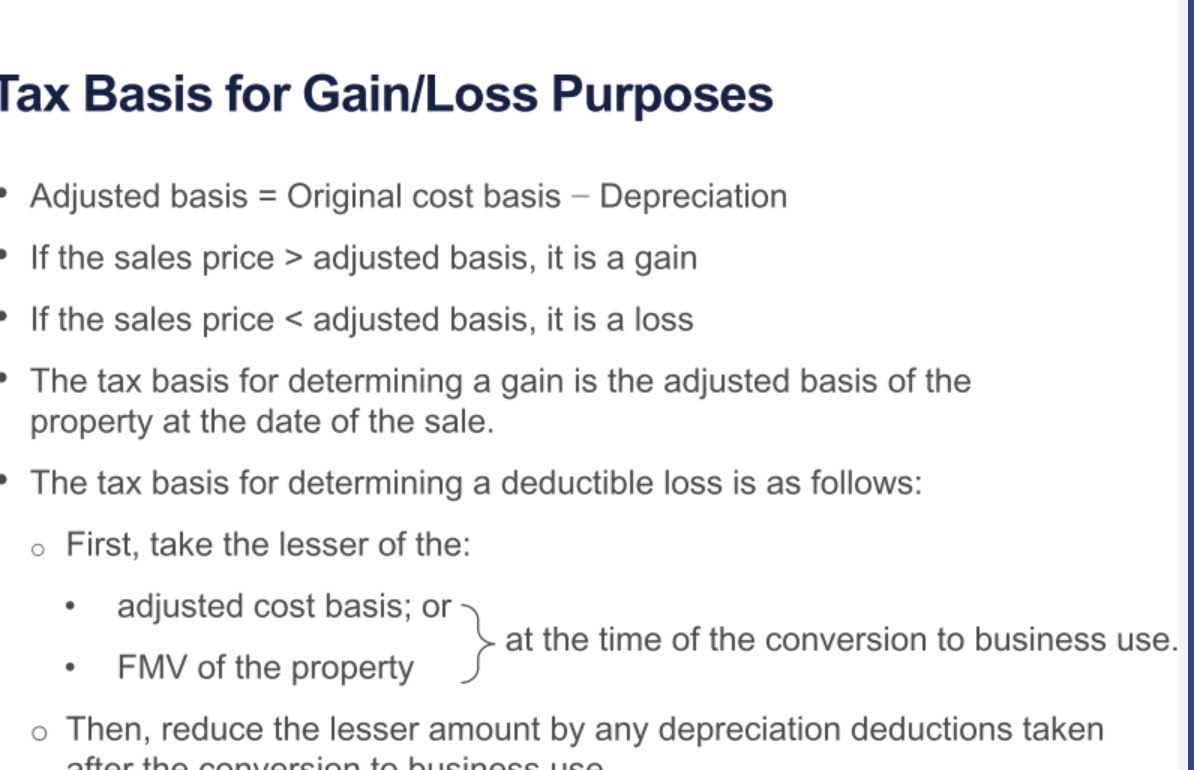

When is a rental property classified as apersonal/rental residence for tax purposes?

A property is considered a personal/rentalresidence if:

It is rented for 15 or more days during theyear, and

The owner uses it for personal purposes forthe greater of:

More than 14 days, or

More than 10% of the total daysrented.

If personal use exceeds this threshold, expensesmust be prorated between rental and personaluse, and losses may be limited.

What is the excess business loss limitation forindividual taxpayers?

It limits the deductible business loss for theyear to the sum of business income plus athreshold amount ($256,000 for single taxpayersin 2026; $512,000 for married filing jointly). Anybusiness loss exceeding this limit is notdeductible currently but carried forward as a netoperating loss (NOL). This limitation applies afterthe tax basis limitation and includes all businessincome and losses from sole proprietorships,rentals, and flow-through entities.

A guaranteed payment is a salary or other payment to a partner that is not calculated with respect to partnership income.

TRUE

What are the key rules and qualifications for HSAdeductions?

HSA Contribution Deduction:

Deducted above the line (adjustmentfor AGI), reducing gross income.

Not deductible as an itemizeddeduction on Schedule A.

Qualification Requirements:

Must be covered by a High-Deductible Health Plan (HDHP).

2026 minimum deductible: $1,700(self-only), $3,400 (family).

Maximum out-of-pocket limitsalso apply ($8,500 self-only,$17,000 family).

No HSA contributions allowed oncecovered by Medicare Parts A or B.

Contributions can be made bytaxpayer or employer (employercontributions are excluded fromincome).

Contribution Limits (2026):

$4,400 for individual coverage

$8,750 for family coverage

Additional $1,000 catch-up if age 55or older

Distributions:

Tax-free if used for qualified medicalexpenses (including OTC meds,hearing aids, etc.).

Non-qualified withdrawals are taxableand subject to a 20% penalty.

When are attorney fees deductible for taxpurposes?

Attorney fees are generally not deductibleas an adjustment or itemized deduction.

Exception: Attorney fees paid in certaindiscrimination cases (age, sex, racialdiscrimination) or whistleblower cases maybe deductible as an adjustment for AGI.

The deductible amount is limited to theincome included from the judgment relatedto the case.

Attorney fees related to divorce, childsupport, or general legal matters are NOTdeductible.

Attorney fees are not deductible even ifthey relate to alimony or child supportpayments.

Key Point:

Only attorney fees tied directly to certaindiscrimination or whistleblower judgmentsqualify for an above-the-line deduction.

Being available for rent counts as rental use. Idlemonths are excluded only if the property is notavailable for rent or personal use.

TRUE

IRA Contribution Limits and MFJ DeductionPhase-Outs (2026)

Annual IRA Contribution Limits (combinedfor all IRAs):

Under age 50: $7,500 per person

Age 50 or older: $8,500 per person(includes $1,000 catch-up)

Married Filing Jointly: $15,000 or$17,000 if both spouses 50+

Traditional IRA Deduction Phase-OutRanges (if participating in employer plan):

Participant spouse: $129,000 –$149,000 AGI

Non-participant spouse (married toparticipant): $242,000 – $252,000 AGI

If neither spouse participates in anemployer plan:

Full deduction allowed, no AGI phase-out

Married Filing Separately (MFS) Phase-Out:

$0 – $10,000 AGI (very limited or nodeduction above $10,000)

Flashcard: SEP IRA vs SIMPLE IRA vs Solo 401(k)for Self-Employed Taxpayers

Feature | SEP IRA | SIMPLE IRA | Solo 401(k) |

|---|---|---|---|

Who CanContribute? | Employeronly (owner&employees) | Employerandemployeecontributions | Self-employedonly (no full-timeemployees) |

MaxContribution(2026) | Lesser of25% of netSE income or$72,000(owner:effectively20% after SEtaxdeduction) | Lesser of100% of netSE income or$17,000 +catch-up ifage 50+ | Lesser of20% of netSE incomeor $72,000 +catch-up ifage 50+ |

Catch-UpContributions | No catch-upallowed | Yes, $4,000(age 50–59)or $5,250(age 60–63) | Yes, $8,000(age 50–59)or $11,250(age 60–63) |

EmployeesAllowed? | Yes | Yes | No (owneronly) |

ContributionType | Employercontributionsonly | Employerandemployeecontributions | Employeedeferrals +employercontribution |

DeductionType | Above-the-lineadjustment | Above-the-lineadjustment | Above-the-lineadjustment |

Let me know if you want it even more concise ora different style!

For the current year, Jennifer has self-employment net income of $50,000 before any SEP IRA deduction and no other earned income for the year. The total amount of self-employment tax related to Jennifer's earnings was $7,064. What is the maximum amount Jennifer may deduct for contributions to her SEP IRA for the year?

A. OPTION A. | $9,294 | |

B. OPTION B. | $72,000 | |

C. OPTION C. | $8,587 | |

D. OPTION D. | $10,000 |

Your answer is incorrect, the correct answer is A.

Explanation

Choice "A" is correct. The maximum annual deductible amount for self-employed individuals to a SEP IRA is the lesser of $72,000 (2026) or 20 percent of net earnings. "Net earnings" is defined as net self-employment income minus 50 percent of self-employment (S/E) taxes.

Net self-employment income | 50,000 |

|

50% of self-employment taxes | (3,532) | [$7,064 × 50%] |

Self-employment earnings before SEP IRA | 46,468 |

|

Times 20% | × .20 |

|

Calculated SEP IRA Deduction | 9,294 |

|

The 20 percent of self-employment earnings is less than the maximum of $72,000 (2026), so the SEP IRA deduction is $9,294.

TRUE

Both spouses must take either standarddeduction or itemized deductions; if oneitemizes, the other must also itemize.

TRUE

Who qualifies as a dependent for medicalexpense itemized deductions on Schedule A?

Filing taxpayer

Spouse

Dependent who receives more than half oftheir support from the taxpayer

No gross income limit applies for medicalexpense purposes (unlike regulardependent rules)

Must meet all other dependency testsexcept the gross income test

Can include relatives who don’t live withthe taxpayer if support test is met

Cannot be just a friend—even if livingtogether, must meet dependency criteria

Also joint return does not create an issue

Front:

SALT Deduction Phaseout Rules (2026) — Whatare the limits and phaseout details?

SALT deduction limit: $40,400 (aggregateof state/local income, property, and salestaxes) for all filers except MFS.

If MAGI > $505,000, deduction is phasedout by 30 cents per $1 over threshold.

Minimum SALT deduction cannot bereduced below $10,000 after phaseout.

Applies only to state, local, and foreign (ifapplicable) taxes; federal taxes are notdeductible.

How do you calculate the deductible personalcasualty loss on nonbusiness property?

Determine Loss Amount:

- Calculate the decrease in FMV = FMVbefore casualty – FMV after casualty

- Loss = lesser of:

> adjusted basis (cost - depreciation) OR

> decrease in FMVSubtract any insurance or reimbursementreceived.

Apply the $100 floor per casualty event:

- Subtract $100 from the loss amount afterinsurance.Apply the 10% of AGI floor on aggregatelosses:

- Total all casualty losses (after $100 floorand insurance recovery)

- Subtract 10% of AGI from the total to getthe deductible amount.Only losses from federally declareddisasters qualify.

What are the key rules for deducting homemortgage interest on a tax return?

Deductible on qualified residence interestfor a principal residence plus one secondhome (used 14+ days personally).

Interest is deductible on up to $750,000 ofqualified home-related indebtedness forSingle, HoH, Surviving Spouse, or MFJ filers.

For Married Filing Separately (MFS), the limitis $375,000.

Qualified indebtedness must be:

Incurred to buy, build, or substantiallyimprove the home, and

Secured by the home.

Home equity loan interest is deductibleonly if the funds are used for homeacquisition/improvement and counttoward the total $750K limit.

Interest on any mortgage debt above theselimits is personal interest and notdeductible.

Mortgage insurance premiums onacquisition debt qualify as deductibleinterest.

Points paid on purchase loans are fullydeductible immediately; points onrefinancing must be amortized over the lifeof the loan.

What is the 0.5% AGI floor rule for charitablecontributions, and how do carryovers of excesscontributions work?

0.5% AGI Floor:

Charitable contributions are deductibleonly to the extent that they exceed 0.5% ofAGI (Adjusted Gross Income).Example: AGI $100,000 → first $500 ofcontributions nondeductible.

Apply after applying AGI ceiling limits(e.g., 60%, 50%, 30%).

Carryover Rules:

Contributions exceeding the AGIceiling can be carried forward up to 5years.

Carryovers are applied first-in, first-out after current year contributions.

Carryovers retain the originalproperty type classification (cash,ordinary income property, LTCGproperty).

The 0.5% floor disallowed amount canonly be carried forward if there is alsoa carryover from exceeding theceiling limits.

If no carryover due to ceiling limitsexists, amounts disallowed by thefloor cannot be carried forward.

If personal property increases in value is it considered LTCG for charity purposes

Yes, for charitable contribution purposes,personal property is considered long-termcapital gain (LTCG) property only if:

It has been held for more than one year(long-term),

And it has increased in value (appreciated)since purchase.

If those conditions are met, the donor cangenerally deduct the fair market value (FMV) atthe time of donation, subject to the 30% of AGIlimit for LTCG property.

If the personal property depreciated in value orwas held one year or less, it is treated asordinary income property, and the deduction islimited to the lesser of FMV or the donor’s basis(usually cost), with a 50% of AGI limit.

So appreciation and holding period both matterfor classifying the property for the charitablededuction.

In short:

Held > 1 year AND appreciated = LTCGproperty; deduct FMV

Held ≤ 1 year or depreciated = Ordinaryincome property; deduct lesser of FMV orbasis

How do you calculate the 2/37 limit onitemized deductions for taxpayers in the 37% taxbracket?

A:

If you are in the 37% tax bracket, your itemizeddeductions must be reduced by:

Take the smaller amount of:

Your total itemized deductions, or

The amount by which your taxableincome plus your itemized deductionsis over the 37% tax bracket startingpoint.

Multiply that smaller amount by 2 dividedby 37 (which is about 0.054).

Subtract this reduction from your originalitemized deductions to get your alloweditemized deductions.

Example:

AGI: $700,000

Itemized deductions: $100,000

37% bracket starts at: $640,600

Taxable income = AGI – itemizeddeductions = $700,000 – $100,000 =$600,000

Step 1: Calculate excess over threshold:

600,000+100,000−640,600=59,400600,000+100,000−640,600=59,400

Step 2: Pick the smaller:

Smaller of $100,000 or $59,400 is $59,400.

Step 3: Multiply by 2/37:

59,400×237=3,21159,400×372=3,211

Step 4: Allowed itemized deductions:

100,000−3,211=96,789100,000−3,211=96,789

A charitable contribution is not allowed for the value of services rendered to a charity.

TRUE

A contemporaneous written acknowledgement is required for donations of $250 or more.

TRUE

Flashcard: QBI Deduction Limitation & NetCapital Gain

What is the limitation on the Section 199AQualified Business Income (QBI) deduction?

A:

The QBI deduction is limited to the lesser of:

20% of the taxpayer’s combined QBI fromall qualifying businesses; or

20% of the taxpayer’s taxable incomebefore the QBI deduction, reduced by netcapital gain.

Q: What is meant by net capital gain for the QBIdeduction limitation?

A:

Net capital gain = the excess of net long-termcapital gains over net short-term capital losses,after netting all capital gains and losses (bothlong-term and short-term). It also considersqualified dividend income. This amount issubtracted from taxable income when applyingthe QBI overall limitation to exclude capitalgains from the deduction calculation.

How do QBI deduction limitations differbetween Specified Service Trade or Businesses(SSTBs) and Qualified Trade or Businesses(QTBs)?

TaxableIncomeRange | QTB (QualifiedTrade or Business) | SSTB (SpecifiedService Trade orBusiness) |

|---|---|---|

BelowThreshold | Full 20% QBIdeduction allowed,no limitationsapply | Full 20% QBIdeductionallowed, nolimitations apply |

WithinPhase-OutRange | QBI deductionallowed butsubject towage/propertylimits | QBI deductionphases out,limited to somepercentagebased on income |

AboveThreshold | QBI deductionallowed but limitedby W-2 wage andqualified propertybasis | No QBI deductionallowed (phasedout completely) |

Key Points:

SSTB: Includes businesses in health, law,accounting, consulting, financial services,etc.

QTB: Any business NOT classified as anSSTB (engineering and architecturalservices are QTB).

For SSTBs, taxable income over thethreshold means no QBI deduction.

For QTBs, even above the threshold, QBIdeduction is still available but limited bywages and property.

This distinction is crucial when calculating ordetermining eligibility for the QBI deductionunder Section 199A.

Architectural services and engineering firms are specifically excluded from the definition of an SSTB.

TRUE

This keeps the QBI deduction aligned withordinary taxable income, excluding thepreferential capital gains and qualified dividendincome.

So, to clarify:

STCG: No, not part of net capital gain here.

LTCG: Yes, included after netting out STCL.

Qualified dividends: Yes, included in netcapital gain.

That’s the basis for the overall QBI deductionlimit calculation.

TRUE

Deduction for services is not allowed as a charitable deduction

TRUE

QBI deduction is not allowed for businesses conducted outside the US

TRUE

Child and Dependent Care Credit — Key Rulesand Phaseouts

Purpose: Nonrefundable credit to offsetwork-related care expenses for qualifyingpersons.

Qualifying Persons:

Dependent child under 13

Disabled dependent (any age, meetssupport test)

Disabled spouse unable to care forself

Earned Income Requirement:

Both spouses must have earnedincome (unless spouse is full-timestudent or incapacitated)

Eligible Expenses:

Babysitter, day care, nursery school(NOT elementary school)

Maximum qualifying expenses:

$3,000 for 1 qualifying person

$6,000 for 2 or more qualifyingpersons

Credit Percentage (based on AGI):

Maximum 50% if AGI ≤ $15,000

Phaseout from 50% ↓ 35% for AGI$15,001–$45,000 (1% decrease per$2,000 over $15K)

Phaseout from 35% ↓ 20% for AGI$45,001–$75,000 (or $150,000 MFJ) (1%decrease per $2,000 over $75K)

Minimum 20% if AGI > $75,000($150,000 MFJ) — credit never below20%

Maximum Credit:

$1,500 for one dependent (50% ×$3,000)

$3,000 for two or more dependents(50% × $6,000)

At minimum 20% rate: $600 (1dependent) or $1,200 (2+ dependents)

Example:

AGI $110,000, two qualifying children, expenses$3,600 + $3,800 = $7,400

Eligible expenses capped at $6,000 × 20% creditrate = $1,200 credit

AOTC vs LLC — Key Differences and Eligibility

Feature | AmericanOpportunity TaxCredit (AOTC) | LifetimeLearning Credit(LLC) |

|---|---|---|

EligibleEducation | First 4 years ofundergraduateeducation | Undergraduate,graduate, andprofessionalcourses (no limiton years) |

EnrollmentRequirement | Must be enrolledat least half-time for at leastone academicperiod | No minimumenrollment; part-time studentsqualify |

MaximumCredit | Up to $2,500 pereligible studentper year | 20% of up to$10,000 qualifiedexpenses pertaxpayer (max$2,000) |

CreditCalculation | 100% of first$2,000 + 25% ofnext $2,000 ofexpenses | 20% of qualifiedexpenses (max$10,000 totalexpensescombined) |

Refundable? | 40% refundable(up to $1,000) | Nonrefundable(can only reducetax liability) |

Number ofYears | Limited to 4 taxyears pereligible student | Unlimitednumber of years |

StudentStatus | Must not havecompleted first4 years of highereducation | No limit oncompletionstatus |

Phaseout(MAGI, MFJ) | Phases outbetween$160,000 and$180,000 | Phases outbetween $80,000and $90,000 |

Per Studentor PerTaxpayer | Per student(each eligiblestudent canqualify) | Per taxpayer (allstudents’expensescombined) |

Example:

AOTC is better for undergrads in first 4years with half-time enrollment.

LLC works for graduate study or part-timecourses; max $2,000 credit total regardlessof number of students.

Key Differences: 529 Plan vs Coverdell EducationSavings Account (ESA)

Feature | 529 Plan | Coverdell ESA |

|---|---|---|

Purpose | Save forqualifiedhighereducationexpenses | Save for qualifiededucationexpenses (K-12 andhigher education) |

ContributionLimits | No federallimit; state-set limits,often veryhigh | $2,000 perbeneficiary peryear |

Age Limit forBeneficiary | No age limit | Must be under age18 to contribute;distributions mustbe used before age30 (except forspecial needs) |

QualifiedExpenses | Tuition, fees,books,supplies,equipment,room &board (ifenrolled half-time) | Tuition, fees,tutoring, books,room & board,supplies,equipment —includeselementary &secondaryexpenses |

TaxTreatment | Earningsgrow tax-free;distributionstax-free if forqualifiedexpenses | Earnings grow tax-free; distributionstax-free forqualified expenses |

IncomeLimits forContributions | Nonefederally | Phase-out forcontributors withAGI $95,000–$110,000 (single),$190,000–$220,000(MFJ) |

Control ofAccount | Usuallycontrolled byaccountowner (oftenparent) | Controlled byaccount owner(usually parent);designatedbeneficiary can bechanged to afamily member |

Uses | Primarilyhighereducation;some K-12 insome states | K-12 and highereducationexpenses |

RolloverRules | Can rolloverto anotherqualifiedbeneficiary | Rollovers allowedto another familymember withoutpenalty |

Penalty forNonqualifiedDistribution | Earningsportion taxedplus 10%penalty | Earnings portiontaxed plus 10%penalty |

Summary:

529 Plans are flexible with high contributionlimits, mainly for college expenses,sponsored by states.

Coverdell ESAs have lower contributionlimits, cover K-12 costs, and have agerestrictions but offer broader qualifiedexpenses.

Use this to choose the best education savingsvehicle based on needs and limits!

Credit for the Elderly and/or PermanentlyDisabled — Key Rules & Calculation

Eligibility:

Age 65 or older; OR

Under 65 & retired due to total &permanent disability with taxabledisability income

Base Amount (depends on filing status &age/disability):

Single or Qualifying Surviving Spouse:$5,000

Married Filing Jointly (both qualified):$7,500

Married Filing Jointly (one qualified):$5,000

Married Filing Separately (qualifiedindividual): $3,750

If under 65 with disability income lessthan $5,000, base limited to lesser of$5,000 or actual disability income (or$3,750 if MFS)

Calculation Steps:

Start with the base amount.

Reduce by the nontaxable portion ofSocial Security and other excludablepensions/annuities.

Reduce further by 50% of AGIexceeding thresholds:

Single: $7,500

MFJ: $10,000

MFS: $5,000

Multiply remaining amount by 15%.

Credit Limits:

Nonrefundable (cannot exceed taxliability).

Example:

Peter, single, 68 years old, AGI $8,060.

Base: $5,000

Less nontaxable Social Security: $3,120

Excess AGI: $8,060 − $7,500 = $560 → 50% × $560= $280

Balance: $5,000 − $3,120 − $280 = $1,600

Credit: 15% × $1,600 = $240

Adoption Credit — Key Rules and Limits

Purpose: Nonrefundable tax credit forqualified adoption expenses to offset taxliability dollar-for-dollar.

Maximum Credit:

For 2026, up to $17,670 of qualifiedexpenses per child (inflation-adjustedannually).

Qualified Expenses Include:

Adoption fees

Court costs

Attorney fees

Travel expenses (if directly related toadoption)

Excludes medical expenses andadopting a spouse’s child or surrogateparenting arrangements.

Timing Rules:

Domestic adoptions: Credit claimed inyear after payment until adoptionfinalized. Expenses paid in yearadoption finalizes claimed that year.

Foreign adoptions: No credit untiladoption is finalized; all expensesclaimed in year of finalization orthereafter.

Refundable Portion:

Up to $5,120 (2026) is refundable; restis nonrefundable.

Carryforward:

Unused nonrefundable credit can becarried forward up to 5 years.

Phaseout:

Phased out for taxpayers with MAGIover $265,080 (2026) fully phased outat $305,080.

Interaction with Employer AdoptionAssistance:

Employer adoption assistance (up to$17,670) excluded from incomeseparately; cannot claim credit onexpenses reimbursed by employer.

What is the Safe Harbor rule related to tax withholding and estimated tax payments?

Safe Harbor rules help taxpayers avoidunderpayment penalties by meeting either ofthese payment thresholds:

90% of the current year's tax liability paidthrough withholding and estimatedpayments; OR

100% of prior year's tax liability (110% if AGI> $150,000).

For individuals with a prior-year tax liability of $0,the safe harbor is effectively met by paying $0,so no penalty applies.

Taxpayers only need to satisfy one of these rules(the lesser amount) to avoid penalties.

What is the Kiddie Tax and how is it calculated?

Applies to:

Children under age 18, or

Full-time students age 18 to under 24who do not provide more than half oftheir own support and are claimed asdependents.

Taxed Income:

Applies only to the child’s unearnedincome (interest, dividends, capitalgains) above a threshold.

Earned income (wages) taxed at thechild’s own rates, not subject to KiddieTax.

Standard Deduction for Unearned Income:

$1,300 in 2024 (or greater of $1,300 orearned income + $400, up to standarddeduction limit).

Taxation Tiers for Unearned Income:

First $1,300: No tax

Next $1,300 (from $1,301 to $2,600):taxed at child’s tax rate

Unearned income above $2,600:taxed at parent’s marginal tax rate

Calculation Steps:

Calculate total unearned income.

Subtract $2,600 from unearnedincome to find net unearned incometaxed at parent's rate.

Apply standard deduction toremaining earned + unearned incometaxed at child’s rate.

Purpose: Prevents parents from shiftinginvestment income to children to avoidhigher tax rates.

Quick Example:

Child with $8,000 total income ($5,000 earned,$3,000 unearned):

$1,300 no tax,

$1,300 taxed at child’s rate,

$400 taxed at parents’ rate.

Medical expenses are not eligible for adoption credit

True

An employee who has Social Security tax withheld in an amount greater than the maximum for a particular year may claim the excess as a credit against income tax, if that excess resulted from correct withholding by two or more employers. If only 1 employer- it must he reimbursed directly through that employer

True

A nonresident alien is not subject to NIIT tax

True

Under the tax law, receipt of non taxable stock dividend or stock splits requires tax payer to spread basis over both old and new shares

TRUE

Gifted Property: General Rules for Basis andHolding Period

Donee’s basis = Donor’s adjusted basis(rollover basis)

Donee’s holding period includes donor’sholding period

Exception (When FMV at gift date < Donor’sbasis):

Basis depends on sales price:

If sale price > Donor’s basis → useDonor’s basis (recognize gain)

If sale price < FMV at gift date → useFMV (recognize loss)

If sale price between FMV and Donor’sbasis → basis = sale price (no gain orloss)

Holding period starts on gift date if saleprice < FMV (loss scenario)

Otherwise holding period includes donor’sholding period

Additional Notes:

Gift tax paid by the donor may increasebasis but not tested on exam

Depreciable property basis for the donee =lesser of donor’s adjusted basis or FMV atgift date

At which date is the Fair Market Value (FMV)of inherited assets determined for basispurposes?

The FMV is generally taken at the date ofthe decedent’s death.

Alternatively, the Alternate Valuation Date(AVD) may be elected, which is the earlierof:

6 months after the date of death, or

The date the property is distributed (ifbefore 6 months).

This election is only available if it reduces theoverall estate tax liability.

What is the De Minimis Safe Harbor Rule forexpensing business assets?

Applies only if the business has a writtenaccounting policy to expense low-costpersonal property.

If the business has an Applicable FinancialStatement (AFS) (audited financials):

Can expense items costing up to$5,000 each.

Without an AFS:

Can expense items costing up to$2,500 each.

If the cost of an item exceeds the limit, theentire cost must be capitalized — no partial expensing allowed.

Useful life over 1 year does not negate therule if item cost and policy requirementsare met.

Use this to remember limits and conditions forimmediate expensing under tax law!

True

How are organizational and start-up costscapitalized and expensed for tax purposes?

Taxpayers can immediately expense up to$5,000 of both organizational costs andstart-up costs each.

The $5,000 expense allowance is reduceddollar-for-dollar when total costs exceed$50,000 for each category.

Costs above the allowed immediateexpense are capitalized as intangibleassets.

These capitalized costs are amortized over15 years (180 months) starting from themonth the business begins operations.

Only qualifying costs apply:

Organizational costs: legal,accounting, filing fees, organizationalmeetings (exclude costs related toissuing stock).

Start-up costs: expenses beforebusiness begins, like marketinvestigation, hiring employees(exclude costs after operations start).

Example:

Organizational costs = $26,000 → $5,000immediate expense + $21,000 amortizedover 180 months

Start-up costs = $52,000 → $3,000immediate expense (due to $2,000 phase-out) + $49,000 amortized over 180 months

When does the holding period begin for shares acquired through a non taxable stock dividend

The holding period for shares acquired through a non taxable stock dividend begins on the date the original shares were acquired

Section 1244 Stock Loss Rules

Applies to qualified small business stockissued by a private company.

Losses on Section 1244 stock are treated asordinary losses, not capital losses.

Ordinary loss treatment allows:

Full deduction against ordinaryincome in the year of loss (no $3,000capital loss limit).

Losses are not netted against capitalgains, preserving preferential capitalgains rates.

Deduction limits per year:

Up to $50,000 for single filers;

Up to $100,000 for married filingjointly.

Must be the original owner of the stock atissuance to qualify.

Provides tax advantage by offsettingordinary income instead of only capitalgains.

Section 1202 Small Business Stock (QSBS)Exclusion Rules

Must be original issue stock of a Ccorporation (not purchased from anothershareholder).

The corporation’s gross assets must be $50million or less at the time the stock isissued. 75 million of issued after July 4th, 2025

Stock must be held for more than 5 years to qualify for gain exclusion.

Gains exceeding the exclusion amount aretaxed at a maximum rate of 28%.

Applies only to C corporation stock, not Scorporations or partnerships.

If the exclusion percentage is less than 100 percent, the 28 percent capital gain rate applies to the non excluded portion of the qualified QSBS gain

The regular 0/15/20 percent capital gain rate only applies to gain that exceeds the maximum exclusion

C Corporation Capital Loss Carryback &Carryforward Rules

Capital losses can only offset capitalgains, never ordinary income.

Carryback allowed: Up to 3 years to offsetprior capital gains (subject to taxableincome limits).

Carryforward allowed: Up to 5 years tooffset future capital gains.

Capital losses carried to another year aretreated as short-term losses regardless oforiginal holding period.

If not used within carryback orcarryforward periods, the loss expires.

Different from NOLs, which typically carryforward indefinitely but can’t be carriedback post-2017 (except some exceptions).

What are the key rules for the gain exclusionon the sale of a personal principal residence?

Exclusion Limits:

$250,000 for single, separate filing, orhead of household

$500,000 for married filing jointly orcertain surviving spouses

Qualification Tests:

Owned the home for at least 2 of thelast 5 years before sale

Used the home as the principalresidence for at least 2 of the last 5years

Ownership and use periods do nothave to be continuous or overlap

Other Rules:

Gain above the exclusion amount istaxable capital gain

Losses on sale of personal residenceare not deductible

No requirement to reinvest proceedsto qualify

Exclusion can only be claimed onceevery 2 years

Q: What is the wash sale rule and how does itaffect loss recognition?

Definition:

A wash sale occurs when you sell a securityat a loss and buy the same or substantiallyidentical security within 30 days before orafter the sale date.Effect:

The loss on the sale is disallowed (notcurrently deductible).Adjustment:

The disallowed loss is added to the basis ofthe repurchased shares, deferring the lossuntil those shares are ultimately sold.Key Points:

The rule applies both to repurchasesbefore and after the sale within the30-day window.

A single repurchase can only triggerone wash sale—purchases cannot bedouble-counted for multiple washsales.

If no repurchase occurs within 30 daysbefore or after, the loss is fullyrecognized.

How is depreciation calculated under the mid-month convention for real estate in the year theproperty is acquired and in the year it is sold?

Acquisition year: Property is treated asplaced in service at the midpoint of theacquisition month, so you get a half-monthof depreciation for that month plus fullmonths after.

Disposal year: Property is treated asdisposed of at the midpoint of the disposalmonth, so you get depreciation for all fullmonths before plus a half-monthdepreciation for the disposal month.

This means half a month's depreciation isalways given for both the month ofacquisition and the month of disposition,regardless of the actual date in the month.

The mid-month convention smoothsdepreciation to simplify calculations forreal estate.

Flashcard: Qualified Production Property vs.Qualified Real Property (Section 179 & BonusDepreciation)

Qualified Production Property:

Includes tangible personal propertyused to produce tangible personalproperty (e.g., manufacturingequipment, machinery).

Eligible for both Section 179 and 100%Bonus Depreciation (if placed inservice in the year).

Has a recovery period ≤ 20 years.

Must be purchased and placed inservice, new or used (with somerestrictions).

Qualified Real Property (for Section 179):

Certain improvements tononresidential real property (e.g.,leasehold improvements, roofs, HVAC,fire/alarm/security systems).

Eligible for Section 179 (but stricterrules apply, must be depreciable realproperty improvements).

Also eligible for Bonus Depreciation asQualified Improvement Property (QIP)treated as 15-year property for bonusdepreciation purposes.

Land and buildings themselves arenot eligible for Section 179 or BonusDepreciation.

Key Points:

Section 179 is generally limited totangible personal property andcertain qualified real propertyimprovements.

Bonus depreciation applies toqualified property with a recoveryperiod ≤ 20 years, including QIPtreated as personal property forbonus purposes.

Section 179 deduction is limited bytaxable income; Bonus depreciation isnot.

Real property placed in service does not effect mid quarter convention

TRUE

For year of disposals half the deprecation is taken for assets subject to sale using half year convention

TRUE

Why are elevators and escalators not eligible forSection 179 expensing?

Elevators and escalators are classified asstructural components of a building. They arepermanently integrated into the building’sframework, not removable, and considered partof the building’s core infrastructure. Because ofthis, the IRS explicitly excludes them fromSection 179 eligibility, which only covers tangiblepersonal property and certain qualified realproperty improvements.

Section 197 intangible assets are depreciated over 15 years and not useful lives. Amortization does not start until business begins operations!

True

Intangible asset amortizarion rules (*****)

If acquired in businesses acquisition- always amortize over 180 months

If Purchased separately- amortize over useful or remaining life

Common MACRS Asset Classes for Depreciation

Flashcard Back:

3-Year Property:

Special tools, certain racehorses

5-Year Property:

Automobiles, taxis, trucks

Computers and peripheral equipment

Copiers, office machinery

7-Year Property:

Furniture, fixtures

Machinery and equipment

10-Year Property:

Boats, water transportationequipment

15-Year Property:

Land improvements (e.g., fences,sidewalks)

20-Year Property:

Farm buildings (non-residential)

Note:

Land itself is NOT depreciable.

Use the 200% declining balance methodfor 3, 5, 7, and 10-year property.

Use the 150% declining balance method for15 and 20-year property.

Always apply the Half-Year Conventionunless the Mid-Quarter Convention applies

Business Interest Expense Limitation & PrepaidInterest

Business interest expense deduction limitedto the sum of:

Business interest income

30% of adjusted taxable income (ATI)

Floor plan financing interest expense(debt to acquire inventory-backedmotor vehicles)

Small businesses (avg. annual grossreceipts ≤ $32 million for prior 3 years) areexempt from this limitation.

Disallowed business interest expense canbe carried forward indefinitely.

Prepaid interest must be allocated to theperiod it relates to; it is not deductibleupfront but amortized over the relevantperiods.

Interest on debt to purchase tax-exemptbonds is not deductible.

Executive Compensation Limits & Bonus AccrualDeductibility for C Corps

Flashcard Back:

Publicly held C corporations can deduct upto $1 million per covered employee (CEO,CFO, and three most highly compensatedofficers).

Compensation includes salary andnonperformance-based bonuses (e.g., year-end bonus).

Covered employees remain coveredemployees in future years, even if no longertop 5 compensated.

Bonuses paid by an accrual basis taxpayerare deductible in the tax year if:

All events establish liability withreasonable accuracy, and

Paid within 2.5 months after year-end(e.g., for 12/31 year-end, bonus mustbe paid by 3/15).

Accrued bonuses must meet these timingand liability criteria to be deductible.

What are the key differences in casualtyloss rules for business property versus personal-use property?

Business Property Casualty Loss:

No requirement for the disaster to befederally declared.

Deductible loss =

Partially destroyed: Lesser of(Decline in FMV or Adjustedbasis) minus insurancereimbursement.

Fully destroyed: Adjusted basisminus insurance reimbursement.

Loss is deductible as ordinary orcapital loss depending on asset type.

Personal-Use Property Casualty Loss:

Loss deductible only if from afederally declared disaster(presidential or federal declaration).

Deductible loss = Lower of Adjustedbasis (cost) or Decline in FMV at timeof disaster.

Additional limitations apply (such asitemized deduction rules andthresholds).

What are the key rules for C Corporationcharitable contribution deductions?

Deduction limited to 10% of adjustedtaxable income (ATI).

ATI is taxable income before deducting:

Charitable contributions,

Dividends-received deduction,

Net operating loss carrybacks,

Net capital loss carrybacks.

The first 1% of ATI is a floor—contributionsup to 1% of ATI are not deductible.

Contributions above 1% up to 10% of ATIare deductible.

Excess contributions (beyond 10%) can becarried forward up to 5 years.

Carryovers are added to current yearcontributions and subject to the same 1%floor and 10% ceiling each year.

Current year contributions deducted first,then carryovers used up to limit.

What are the key requirements for using the LIFOinventory method for tax and financialstatement purposes?

If a corporation uses LIFO for tax purposes,it must also use LIFO for its financialstatements (conformity rule).

The IRS requires consistency to preventmanipulation of taxable income.

The reverse is NOT required: Using LIFO forfinancial statements does not force LIFOfor tax.

When using LIFO, ending inventory isassumed to be composed of the earliest(oldest) acquired goods.

In periods of rising prices, LIFO results inhigher cost of goods sold and lowertaxable income compared to FIFO.

Dividends-Received Deduction (DRD)Outline

1. Purpose of DRD

Prevents triple taxation of corporateearnings

Applies to domestic corporations receivingdividends

2. Percentage Ownership & Corresponding DRD

0% to < 20% ownership → 50% deduction

20% to < 80% ownership → 65% deduction

80% or more ownership → 100% deduction

3. Holding Period to Qualify for DRD

Must hold stock for at least 46 days withina 91-day period

The 91-day period starts 45 days before theex-dividend date

4. How DRD Works (Triple Taxation Concept)

Income taxed at the investee corporationlevel (1st time)

Dividend income taxable at the investorcorporation level, but DRD mitigatesdouble tax (2nd time)

Income taxed again when dividends paidto individual shareholders (3rd time)

5. Taxable Income Limitation on DRD

DRD limited to the lesser of:

Applicable percentage of dividendsreceived, or

Applicable percentage of taxableincome before DRD, NOLcarryforward, or capital losscarryback

Exception: Limitation does not apply if fullDRD creates a net operating loss

6. Entities Not Eligible for DRD

Personal service corporations

Personal holding companies

S corporations (pass-through entities)

Dividends from certain entities alsoexcluded (banks, RICs, REITs, public utilities,tax-exempt corporations, cooperatives,DISCs)

7. Special 100% DRD Situations

Affiliated corporations (80% or moreownership, filing consolidated returns)

Small Business Investment Corporations(SBICs)

NOL Rules (Net Operating Loss) — CCorporations

NOL Created 2017 or Earlier

Carryback: 2 years

Carryforward: 20 years (expires if not used)

Offset: 100% of taxable income (even after2020)

2. NOL Created 2018-2020

Carryback: 5 years

Carryforward: Indefinitely (never expires)

Offset:

100% of taxable income for tax yearsthrough 2020

80% for tax years 2021 and beyond

3. NOL Created 2021 and Later

Carryback: None

Carryforward: Indefinitely

Offset: Limited to 80% of taxable income(starting year 2021 onward)

Notes:

Carrybacks are no longer tested on CPAexam, focus on carryforwards.

Prior year NOLs do NOT create or increasecurrent year NOLs.

Charitable contributions cannot create orincrease an NOL.

DRD deduction calc

Includes charitable deduction and charitable carry forwards, DOES NOT INCLUDE, capital loss carry backs or NOL deductions

50%> ownership for C Corp shareholder rules

Expenses owed to >50% shareholder can’t be deducted until year included in shareholders income

A gain from an illegal activity is includible in income. To determine the gain, a deduction is permitted for cost of merchandise. Business expenses for operating an illegal business, other than the cost of merchandise, are not permitted as deduction

TRUE

What is the difference between Schedule M-1and Schedule M-3, and when is Schedule M-3required to be filed?

Schedule M-1:

Used by smaller corporations toreconcile book income to taxableincome.

Provides a summary-levelreconciliation of differences betweenfinancial (book) accounting and taxaccounting.

Schedule M-3:

Used by larger corporations (generallywith total assets of $10 million ormore).

Provides a detailed, line-by-linereconciliation of book income totaxable income, including temporaryand permanent differences.

Helps the IRS better understandcomplex book-to-tax differences.

When to file Schedule M-3:

Required for corporations with totalassets equal to or greater than $10million at the end of the tax year.

Usually replaces Schedule M-1 forthese large filers.

Mnemonic:

M-1 = Mini (summary reconciliation forsmall)

M-3 = Massive detail for Million+ assetcorporations

R&D Tax Credit Rules for C Corporations

Also called Credit for Increasing ResearchActivities

Calculated as 20% of the increase inqualified research expenditures over abase amount

Can also be computed using thealternative simplified credit method

Part of the General Business Credit andsubject to its limitation:

Credit cannot exceed net income tax(regular tax minus nonrefundablecredits) less 25% of net regular taxover $25,000

Qualified small businesses (under $5Mgross receipts and ≤5 years old) can use thecredit to offset employer portion of FICApayroll tax (up to $500,000/year)

Unused credit may be carried back 1 yearor carried forward 20 years

Estimated Tax Payments: Large vs. Non-LargeCorporations

Non-Large Corporations:

Taxable income never > $1 million in past 3years

Must pay lesser of:

100% of current year's tax, OR

100% of prior year's tax

Cannot use prior year method if: no taxowed last year or prior year < 12 months

Estimated payments due 4 times/year (4th,6th, 9th, 12th month)

Underpayment penalty if payments late &amount owed ≥ $500

Large Corporations:

Taxable income ≥ $1 million in any of past 3years

Must pay 100% of current year’s taxthrough estimated payments

Same due dates and penalty rules as non-large corporations

Foreign Tax Credit (FTC) Rules – Key Points

Available to U.S. domestic corporationsand individuals who pay or accrue qualifiedforeign income taxes.

Must choose annually: credit for foreigntaxes paid OR deduction for those taxes;cannot mix or double dip.

Goal: Prevent double taxation and keepeffective global tax rate ≤ U.S. tax rate (21%for corps).

Calculation Steps:

Foreign taxes paid (given).

Calculate U.S. tax on worldwidetaxable income (WTI × U.S. tax rate).

Find foreign income ratio (ForeignIncome ÷ WTI).

Multiply step 2 × step 3 = foreign taxcredit limitation.

FTC = Lesser of foreign taxes paid orlimitation.

Unused FTC can be carried back 1 year orforward 10 years.

Can't claim deduction if credit elected inthe same or future years for the sameforeign taxes.

What are the key differences between PersonalHolding Company (PHC) tax and AccumulatedEarnings Tax (AET) for C corporations?

Accumulated Earnings Tax (AET):

Applies to regular C corporationsretaining earnings above $250,000 (or$150,000 for personal service corps)without a valid reason.

Penalizes unreasonable retentionintended to avoid shareholderdividend taxation.

Tax rate: 20% on accumulatedearnings exceeding limit.

IRS-assessed during audit, not self-assessed.

Requires a demonstrated specificplan to avoid penalty.

Personal Holding Company Tax (PHC tax):

Applies to corporations >50% ownedby ≤5 individuals with ≥60% passiveincome (rents, dividends, interest,royalties).

PHCs are NOT subject to AET.

Tax rate: 20% on undistributed PHCnet income.

Self-assessed via Schedule 1120 PHwith Form 1120.

Penalty avoided if PHC nets income isfully distributed.

No underpayment of estimated tax penalty will be imposed if the total underpayment of tax for the year is less than $500

TRUE

No charitable contribution deduction is allowed in calculating the NOL

TRUE

S Corporation Formation Rules & Requirements

Must be a domestic corporation (no foreignentities)

All shareholders (voting & non-voting) mustconsent by signing Form 2553

Maximum of 100 shareholders (familymembers can be treated as oneshareholder)

Eligible shareholders: Individuals, Estates,Certain Trusts, Qualified Retirement Plans(ESOPs), and 501(c)(3) organizations

Ineligible shareholders: Corporations,Partnerships, Non-resident aliens, IRAs

Only one class of stock allowed(differences in voting rights allowed, but nopreferred stock)

S Corp must file Form 2553 for election;timing affects effective date

S Corp taxed as a flow-through entity—nocorporate level tax generally

New shareholders do not need to consentafter election is effective

Violation of shareholder rules causestermination of S Corp status

For S corps- members of the same family can count as 1 owner

TRUE

Flashcard Front:

S Corporation Election Deadline - March 15thRule

Flashcard Back:

For existing calendar-year corporations,filing Form 2553 by March 15 makes the Scorp election effective retroactively fromJanuary 1 of that year.

If filed after March 15, the election iseffective January 1 of the following year.

For fiscal-year corporations, filing by the15th day of the 3rd month of the fiscal yearmakes the election effective on the firstday of that fiscal year; otherwise, it iseffective the next fiscal year.

Filing on or before March 15 provides taxbenefits for the entire tax year under Scorp status; filing late delays benefits untilnext year.

For S Corp debt basis can only absorb losses, not distributions

TRUE

For S corps, increases reinstate debt basis first then stock basis

TRUE

For S Corps distributions may not reduce AAA below zero. However, AAA may be negative due to S corporation losses and deductions

TRUE

S corporations that are former C corporations with undistributed C corporation earnings and profits are restricted in the amount of passive investment income they can realize without terminating their S election. The restriction is 25 percent of total gross receipts from passive investment income. The S election is terminated if the S corporation has passive investment income greater than 25 percent of gross receipts for three consecutive years

TRUE

Fringe benefits paid by an S corporation are deductible by the S corporation only for non-shareholder employees and those employee-shareholders owning 2 percent or less of the S corporation. Other fringe benefits paid are deductible by the S corporation if included as part of gross income from the S corporation for the individual receiving the benefits (i.e., included as part of income on the shareholder's W-2).

TRUE

S corporation status can be revoked if shareholders owning more than 50% of the total number of issued and outstanding shares consent. The specific percentage of voting and nonvoting shareholders is not considered, only the total.

TRUE

Although an S corporation cannot have a C corporation shareholder, there is no restriction on an S corporation being a shareholder in a C corporation.

TRUE

Sec 179 depr is a non separately stated item that is not part of business net income

TRUE