Microeconomics

5.0(5)

Studied by 325 peopleCard Sorting

1/145

Earn XP

Description and Tags

Last updated 5:26 AM on 5/24/23

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

146 Terms

1

New cards

What is the basic economic problem?

Unlimited wants with finite resources

2

New cards

What are the three fundamental questions?

1. What to produce

2. How to produce

3. For whom to produce

3

New cards

Opportunity Cost

The next best alternative forgone.

This arises since there is a cost/ sacrifice of one product when a choice is made.

This arises since there is a cost/ sacrifice of one product when a choice is made.

4

New cards

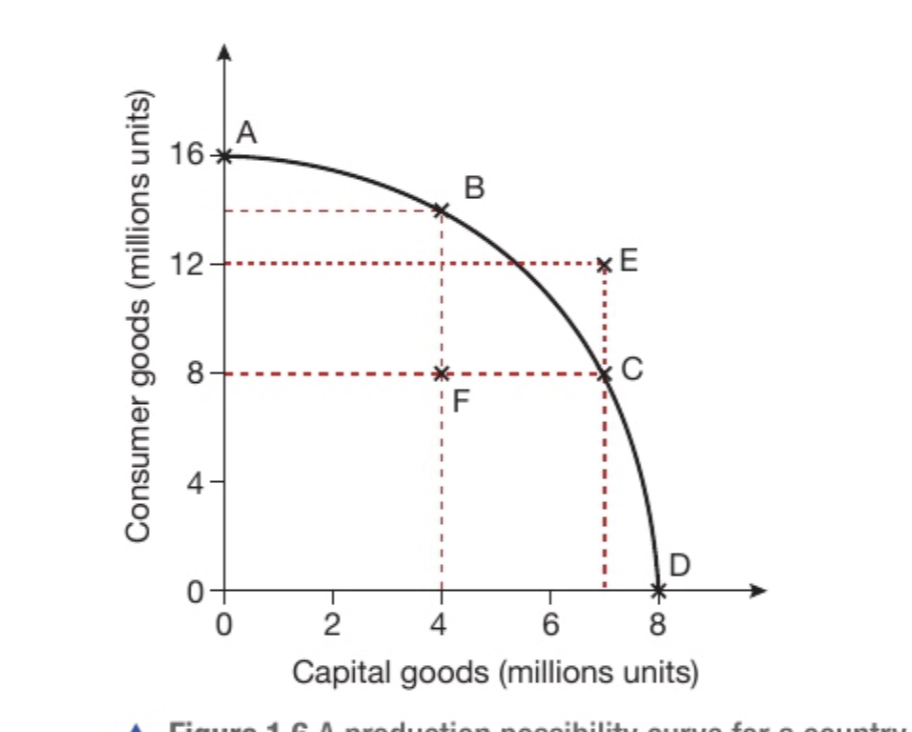

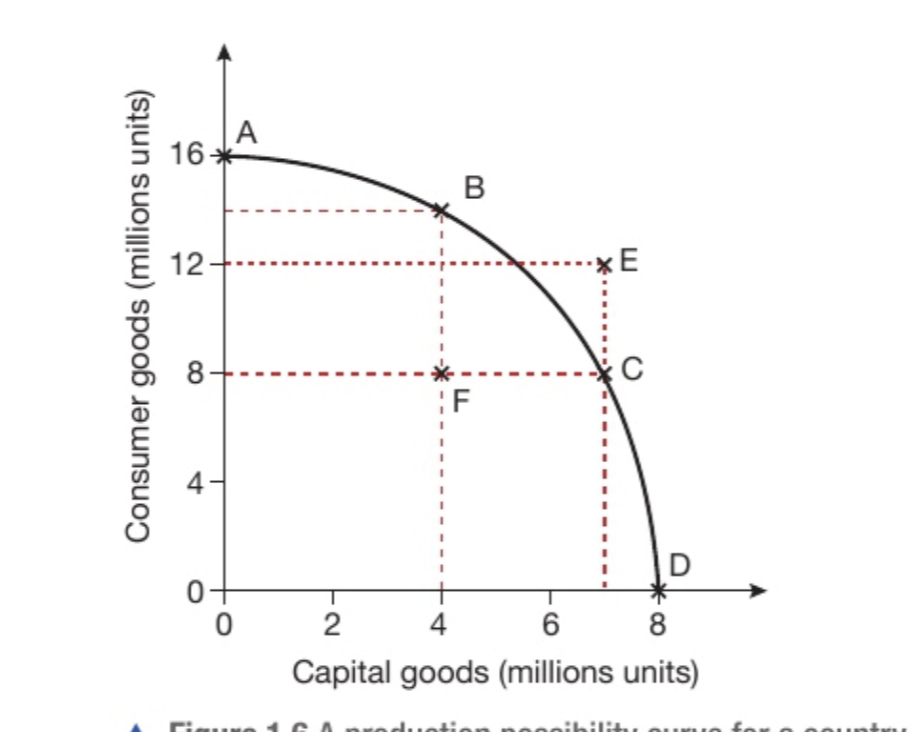

What does a PPC represent?

The maximum production combinations of two goods when goods are fully employed.

5

New cards

What is occuring at point E?

E is an impossible combination. This point lies outside the PPC so this country does not have the resources to produce at point E.

6

New cards

What is occurring at point F?

8 million consumer goods and 4 million capital goods. However this combination is inside the PPC which shows that resources are underemployed in this country.

7

New cards

What can cause a shift in the PPC?

When the production of goods increases in general this is knows as economic growth. (economic growth = increases level of output by the nation)

8

New cards

How does new technology cause economic growth?

New technology benefits businesses since it is much faster and more accurate making it more reliable in production. This will eventually lead to more output.

9

New cards

10

New cards

11

New cards

12

New cards

What do consumers tend to maxmise?

Their benefit (whatever gives them the most satisfaction)

* best quality for same price

* cheapest price for same quality

* best quality for same price

* cheapest price for same quality

13

New cards

What to businesses tend to maximise?

Their profit (best financial results)

* always set highest possible price

* cheapest raw materials for same quality

* always set highest possible price

* cheapest raw materials for same quality

14

New cards

What might cause a consumer to not always maximise their benefit?

1. difficulty calculating benefit

2. developing buying habits (brand loyalty)

1. irrationality develops overtime as someone buys a product habitually

3. influence and trends

4. limited information

15

New cards

What might cause a business to not always maximise their profit?

1. alternative business objectives (customer care)

2. operating as charities

3. social enterprise to improve wellbeing

4. limited information

16

New cards

What kind of relationship do demand and price have?

inverse relationship

17

New cards

What happens to demand curve when price changes

There is a movement along the curve

18

New cards

What happens to the demand curve when a non price factor affects it?

There is a shift in demand

19

New cards

What factors can shift demand?

“PASIFIC”

P-population

A-advertising

S- substitutes (the price of)

I- income

F- fashion

I- interest rates

C- complements (the price of)

P-population

A-advertising

S- substitutes (the price of)

I- income

F- fashion

I- interest rates

C- complements (the price of)

20

New cards

Will increased advertising shift demand to the right? Why?

Yes. Demand increases with more advertising. This is since it increases awareness and influence to buy this product.

21

New cards

Will increased income shift demand to the right? Why?

Yes if it is a normal good. This is when disposable income rises, and demand for goods will rise. Income rising will decrease demand for inferior goods.

22

New cards

Will increased fashion/tastes (for a good) shift demand to the right? Why?

Buying season for something being more favourable and trend for a good or service increasing will lead to increased demand for it. This is influenced by social change.

23

New cards

Will increased price of a subsitute shift demand to the right? Why?

The increased price of a substitute will shift demand to the right since consumers will maximise benefits and opt for a better price for a similar quality good.

24

New cards

Will increased price of a compliment shift demand to the right? Why

Increased price of a complement will shift demand to the left since some goods are purchased together. When two goods are used together, increasing price of a complement will decrease the demand of the original good or service.

25

New cards

Will increased population shift demand to the right? Why

Yes when there are more people, more people want goods and services so this will shift demand to the right?

26

New cards

What is the relationship between supply and price?

A proportionate relationship.

* when price goes up so does supply

* when price goes up so does supply

27

New cards

What happens to supple curve when price changes

A movement along the curve

28

New cards

What happens to the supply curve when a non-price factor changes?

A shift in the curve

29

New cards

What non price factors will affect supply?

“PINTSWC”

P-Productivity

I-Indirect tax

N-Number of firms

T-Technology

S-Subsidies

W-Weather

C-Cost of production

P-Productivity

I-Indirect tax

N-Number of firms

T-Technology

S-Subsidies

W-Weather

C-Cost of production

30

New cards

What is the effect of indirect tax on supply?

Indirect taxes are levied on spending and goods or services. When indirected tax is imposed supply will decrease and shift to the left.

* can be imposed on producers if their production methods harm the environment

* can be imposed on producers if their production methods harm the environment

31

New cards

What is the effect of subsidies on supply?

A subsidy is when the government give money to a business in form of a grant.

* can encourage production of a particular product

* Subsidising=increased supply

* can encourage production of a particular product

* Subsidising=increased supply

32

New cards

What is the effect of changing technology on supply?

New technology and advancement can help production by being more efficient. This will reduce cost of production or increase yield. This will increase supply.

33

New cards

What is the effect of weather on supply?

When conditions are good: Increased supply

In the event of natural disaster or bad conditions seasonally: Decreased supply

In the event of natural disaster or bad conditions seasonally: Decreased supply

34

New cards

What is equilibrium price?

Price at which supply and demand are equal

35

New cards

What is total revenue?

Total revenue is the amount of money generated from the sale of goods (price x quantity sold)

36

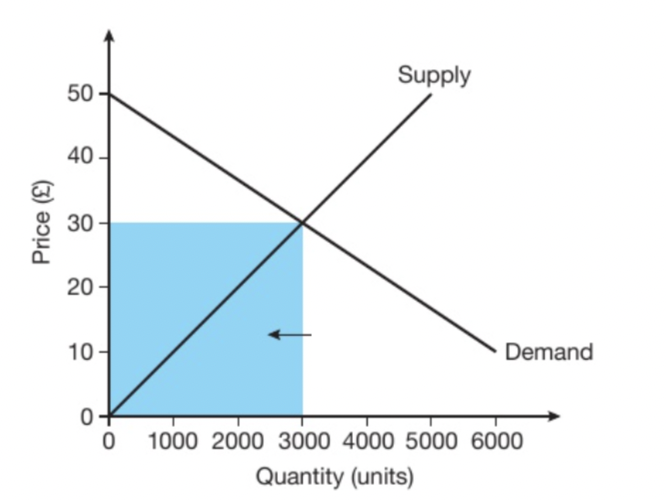

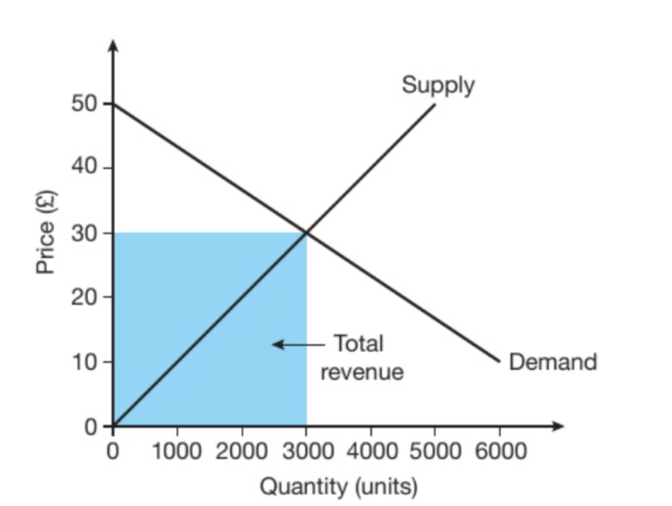

New cards

What does this blue box represent?

Total revenue

37

New cards

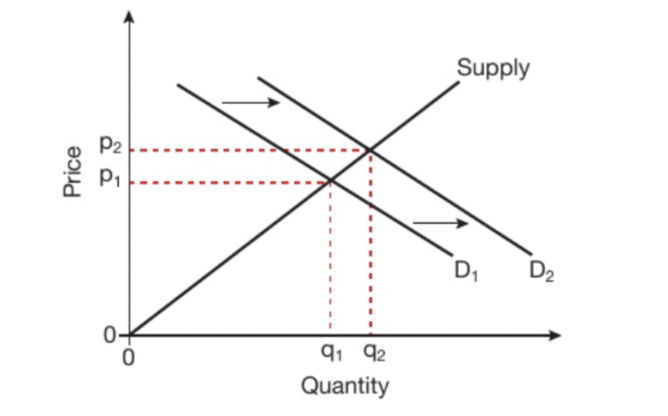

What will a shift in demand do to the equilibrium?

If demand increases then the price will rise. If the demand curve shifts to the right (D2), P AND Q will rise (p1-p2 and q1-q2)

38

New cards

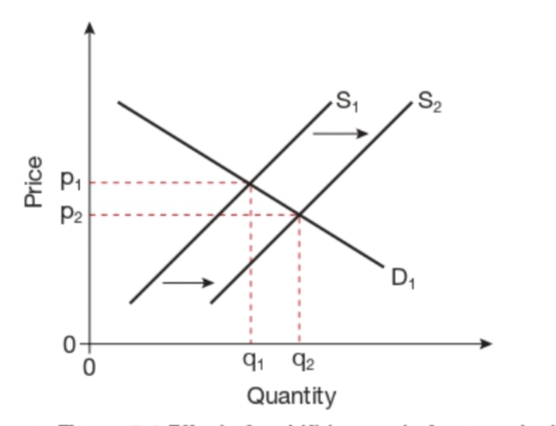

What will a shift in supply do to the equilibrium?

When supply increases the price of equilibrium will decrease. If supple curve shifts to the right (S2), P AND Q will fall ( p1-p2 and q1-q2)

39

New cards

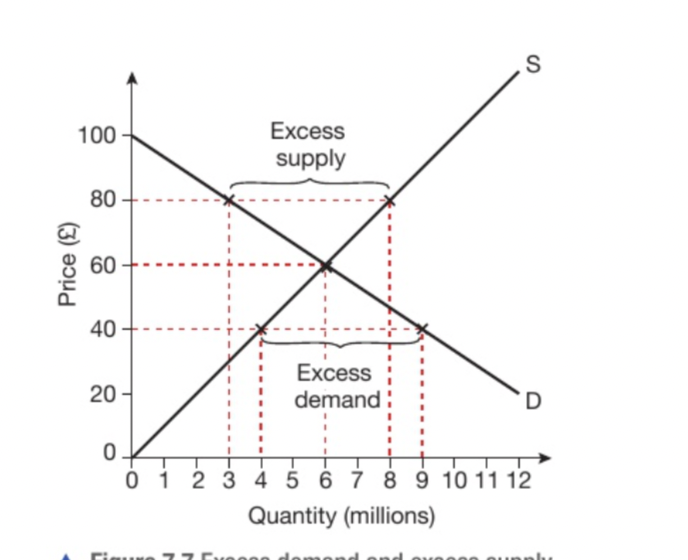

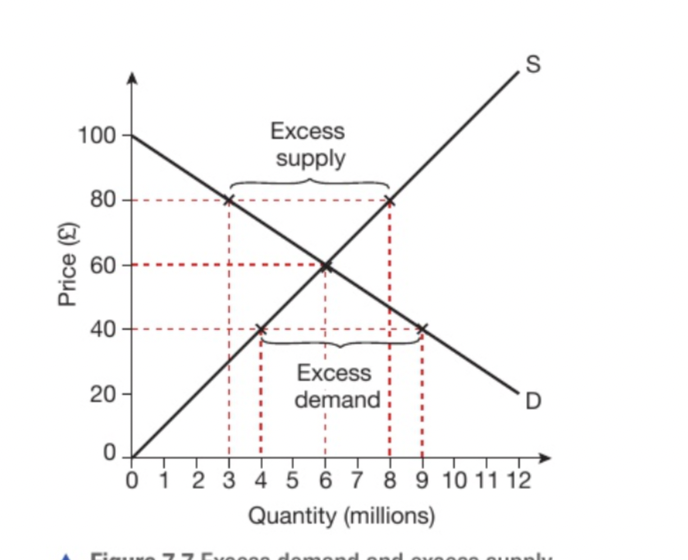

What is excess demand?

Where demand for a good will exceed supply leading to a shortage. This exists when price is set below equilibrium price.

40

New cards

What is excess supply?

Where supply for a good will exceed demand leading to unsold goods. This exists when price is set abve equilibrium price

41

New cards

What is the formula to calculate price elasticity of demand?

Price elasticity of demand = Percentage change in quantity demanded/Percentage change in price

* minus signs signify that the demand falls but elasticity is only based on the number

* minus signs signify that the demand falls but elasticity is only based on the number

42

New cards

Define PED and PES

* Price elasticity of demand is the responsiveness of quantity demanded to a change in price

* Price elasticity of supply is the responsiveness of quantity supplied to a change in price

* Price elasticity of supply is the responsiveness of quantity supplied to a change in price

43

New cards

Define elastic demand

elastic demand is when a change in price results in a proportionately larger change in quantity demanded due to more responsiveness.

44

New cards

Define inelastic demand

inelastic demand is when a change in price results in a proportionately smaller change in quantity demanded due to lower responsiveness.

45

New cards

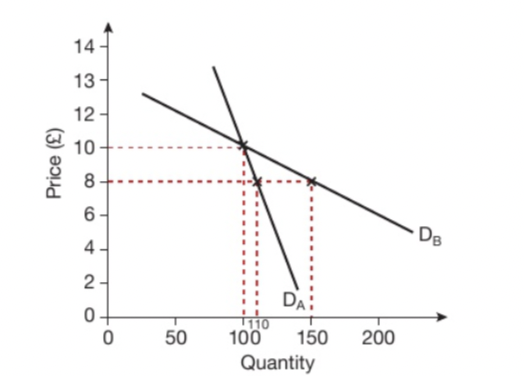

Which of the two graphs is elastic and which is inelastic?

graph dA is inelastic and graph dB is elastic

46

New cards

What are the numerical values of elasticity?

>1 = elastic

1=unitary

<1=inelastic

0=perfectly inelastic

∞=perfectly elastic

1=unitary

<1=inelastic

0=perfectly inelastic

∞=perfectly elastic

47

New cards

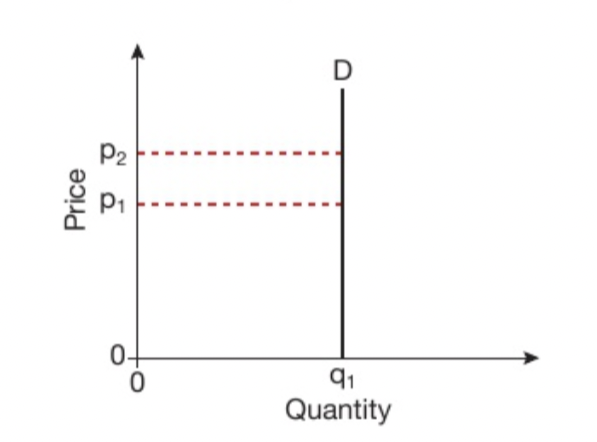

What is this the graph for?

perfectly inelastic(0)

48

New cards

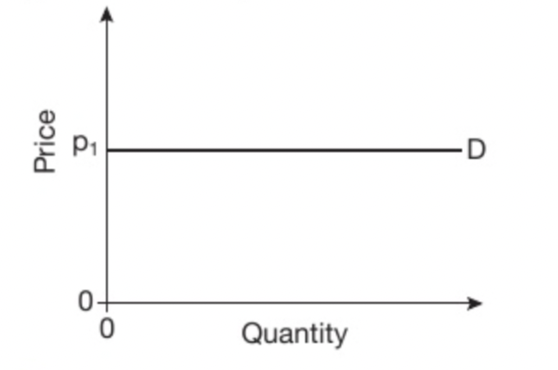

What is this the graph for?

perfectly elastic(∞)

49

New cards

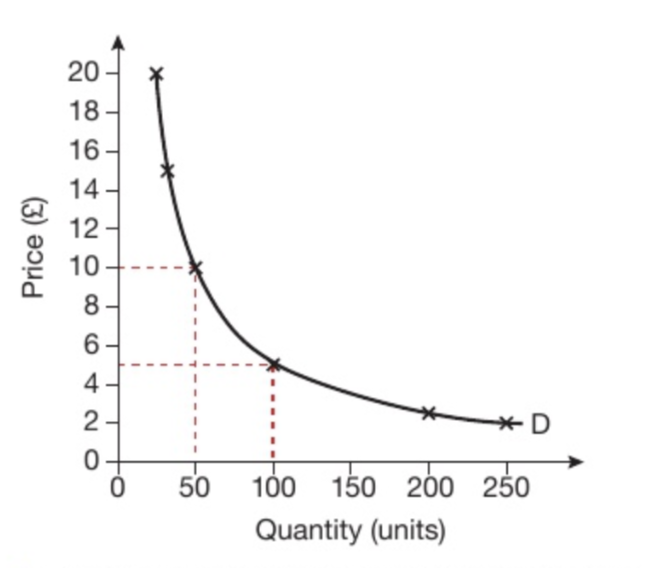

What is this the graph for?

unitary price elastic demand. This is a special case where revenue is always constant no matter the change in price.

50

New cards

What factors affect PED?

“PLANTS”

P-Proportion of income-more spent is more elastic

L-Luxury vs necessity

A-Addictive good-habitual buying means it becomes inelastic

N-No. of uses

T-Time period

S-Substitute availability

P-Proportion of income-more spent is more elastic

L-Luxury vs necessity

A-Addictive good-habitual buying means it becomes inelastic

N-No. of uses

T-Time period

S-Substitute availability

51

New cards

What are the factors that influence PES?

STEMPS

S- spare capacity

T- Time

E- Ease of Entry

M- Mobility of FOPS

P- production speed

S- stock

S- spare capacity

T- Time

E- Ease of Entry

M- Mobility of FOPS

P- production speed

S- stock

52

New cards

What is fixed cost?

Costs which do not vary with output (e.g. rent)

53

New cards

What is variable cost?

Costs that vary based on output (e.g. labour, raw material, fuel)

54

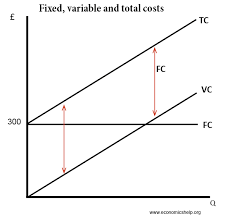

New cards

What is total cost + diagram?

Total fixed cost + Total variable Cost

55

New cards

What is total revenue?

The amount a firm receives from selling its output.

Total revenue = price x quantity

Total revenue = price x quantity

56

New cards

What is profit and loss?

Total revenue-total cost = profit

\

When this number is positive it is profit

When this number is negative it is loss

\

When this number is positive it is profit

When this number is negative it is loss

57

New cards

What is average cost?

The average cost is the total cost of production divided by output (Cost of producing a single unit of a good or service)

58

New cards

Define economies of scale

As firms grow larger average costs begin to fall

59

New cards

What are the 6 internal economies of scale?

“Really Fun Mums Try Making Pies”

R-Risk Bearing

F-Financial

M-Managerial

T-Technical

M-Marketing

P-Purchasing

R-Risk Bearing

F-Financial

M-Managerial

T-Technical

M-Marketing

P-Purchasing

60

New cards

Explain risk-bearing economies of scale

Large firms may have a wider range of products and sell into wider varieties of markets. This reduces risk of business.

61

New cards

Explain financial economies of scale

As firms grow larger they can access money more cheaply and with a wider variety of sources.

Large firms also have to ability to negotiate with banks for lower interest rates

Large firms also have to ability to negotiate with banks for lower interest rates

62

New cards

Explain managerial economies of scale

As firms expand they can afford specialist managers. This will improve efficiency as managers will work specifically with smaller sectors of the firm allowing them to oversee weaknesses.

63

New cards

Explain marketing economies of scale

Larger firms can afford to pay fixed marketing costs as they can be spread over more units of output. (e.g. they can run their own delivery service so the cost of paying a distributor is reduced)

64

New cards

Explain technical economies of scale

Larger firms can invest more in machinery making them more efficient. Larger companies may also use capital more regularly so they are making better use of their capital. This means AC will fall overtime.

65

New cards

Explain purchasing economies of scale

As firms grow larger and they buy in larger quantities they can get cheaper rates.

* an example is bulk buying discounts

* an example is bulk buying discounts

66

New cards

Define external economies of scale

cost benefits that all firms within an industry can experience when the industry expands

67

New cards

What are the four external economies of scale?

“SACI”

S-skilled labour

A-access to suppliers

C-cooperation with other bussinesses

I-infrastructure

S-skilled labour

A-access to suppliers

C-cooperation with other bussinesses

I-infrastructure

68

New cards

Explain how skilled labour is an external economy of scale

When industry is concentrated in one area there will be a high amount of labour with work experience and training. As a result training cost is lowered and local schools may provide vocational courses.

69

New cards

Explain how infrastructure is an external economy of scale

When industry is concentrated in one area this will lead to facilities being accommodating for this industry (e.g. roads, railways, buildings)

70

New cards

Explain how access to suppliers is an external economy of scale

Established industry encourages suppliers to set up close by. This means all firms will benefit from increased accessibility to suppliers.

71

New cards

Explain how similar businesses in an area is an external economy of scale

When similar firms are near each other this leads to cooperation between them to increase benefit mutually. (e.g. sharing costs to reduce AC and cooperate on R n D

72

New cards

Define diseconomies of scale

Average costs will begin to rise when a firm grows too large

73

New cards

What are the diseconomies of scale?

“Bob Calls Linda Darling”

B- beuracracy

C-communication issues

L-lack of control

D-distance between senior and junior staff

B- beuracracy

C-communication issues

L-lack of control

D-distance between senior and junior staff

74

New cards

How is bureaucracy a diseconomy of scale?

Bureaucracy is when businesses use large numbers of departments and officials. If businesses grow too large they often become too bureaucratic so excessive amounts of time are spent making decisions which slow down movement in the firm. This also makes communication channels too long. When resources are overused in admin, AC will rise.

75

New cards

How is communication problems a diseconomy of scale?

When companies grow they may become MNC’s and this means that workers between company may have cultural and language barriers. Time differences also make organization challenging.

76

New cards

How is lack of control a diseconomy of scale?

Large businesses are difficult to control and coordinate so this will require more supervision which raises AC

77

New cards

How is distance between senior and junior staff a diseconomy of scale?

When a firm grows too big, relations may worsen as there may be too many layers of supervision between senior and junior staff. This leads to less acknowledgement of staff needs and leads to demotivation of workers.

78

New cards

What is competition?

Competition is the rivalry between firms when trying to sell goods for a particular market.

79

New cards

What are features of a competitive market?

* low barriers to entry-easy to enter the market

* products sold are homogeneous or close substitutes

* many buyers and sellers

* price takers-no firm can generally change price

* lots of accurate information about the products

* products sold are homogeneous or close substitutes

* many buyers and sellers

* price takers-no firm can generally change price

* lots of accurate information about the products

80

New cards

How do firms change and respond to competition?

COMPETITION LIMITS A FIRMS PROFIT:

* firms prefer dominating the market since competition creates pressure to be more efficient and innnovation.

* firms will try to keep: costs as low as possible, good customer service, low prices

* firms will also try to use product differentiation to make themselves seem better than rivals

\

* firms prefer dominating the market since competition creates pressure to be more efficient and innnovation.

* firms will try to keep: costs as low as possible, good customer service, low prices

* firms will also try to use product differentiation to make themselves seem better than rivals

\

81

New cards

How do consumers change and respond to competition?

The advantages of competitive markets to a consumer are: lower prices, better quality goods, and more choice.

82

New cards

Is competition good or bad for the economy?

* competition ensure resources are allocated efficiently

* efficiency and innovation will increase

* this increases overall standard of living

* efficiency and innovation will increase

* this increases overall standard of living

83

New cards

What are the advantages of being a small firm?

* cater to niche markets

* flexibility-adapt to change as minimal decision makers

* personal service

* lower wage costs- do not belong to trade unions and pay can be restricted

* better communication

* innovation-due to competitve pressure

* flexibility-adapt to change as minimal decision makers

* personal service

* lower wage costs- do not belong to trade unions and pay can be restricted

* better communication

* innovation-due to competitve pressure

84

New cards

What are the disadvantages of being a small firm?

* Higher costs- small firms don’t benefit from EOS

* Lack of finance-limited resources and limited finance as they are considered riskier

* Difficult to attract staff

* Vulnerability-small firms have more difficulty surviving

* Lack of finance-limited resources and limited finance as they are considered riskier

* Difficult to attract staff

* Vulnerability-small firms have more difficulty surviving

85

New cards

What are the advantages of being a large firm?

* economies of scale

* large scale contracts

* market domination

* large scale contracts

* market domination

86

New cards

What are the disadvantages of being a large firm?

* Diseconomes of scale

* Motivation

* Motivation

87

New cards

What can change and influence the size of a firm?

* government regulation

* access to finance

* economies of scale

* desire to spread risk

* desire to take over competitors

* access to finance

* economies of scale

* desire to spread risk

* desire to take over competitors

88

New cards

Why do firms stay small?

* size of market

* nature of the market

* catering to niche markets

* diseconomies of scale

* nature of the market

* catering to niche markets

* diseconomies of scale

89

New cards

What is a monopoly

When one firm dominates the market

25% or more of the market

25% or more of the market

90

New cards

What are 4 key features about a monopoly?

* one business dominates the market

* unique product

* price-maker

* high barriers to entry

* unique product

* price-maker

* high barriers to entry

91

New cards

What are the main barriers to entry?

* high start up cost

* legal barriers

* patents- license to grant permission to be the sole producer of a product

* marketing budgets

* technology (specific to market)

* legal barriers

* patents- license to grant permission to be the sole producer of a product

* marketing budgets

* technology (specific to market)

92

New cards

What are the advantages to being a monopoly?

* efficiency

* innovation

* economies of scale

* innovation

* economies of scale

93

New cards

What are the disadvantages to being a monopoly?

* higher price

* restricted choice

* limited innovation- no incentive to innovate products

* inefficiency- no incentive to keep costs down

* restricted choice

* limited innovation- no incentive to innovate products

* inefficiency- no incentive to keep costs down

94

New cards

What is an oligopoly?

A market dominated by a few large firms

95

New cards

What are features of an oligopoly?

* few firms

* large firms dominate-highly influential and set price

* different products-substitutes but some differentiation and aimed at different market segments

* barriers to entry-discouraged entry by investment in brands

* collusion-restricts competition or price fixing

* non-price competition-avoid price wars through competing in advertisement, branding etc.

* price competition-price is usually the same for long periods of time to avoid price wars.

* large firms dominate-highly influential and set price

* different products-substitutes but some differentiation and aimed at different market segments

* barriers to entry-discouraged entry by investment in brands

* collusion-restricts competition or price fixing

* non-price competition-avoid price wars through competing in advertisement, branding etc.

* price competition-price is usually the same for long periods of time to avoid price wars.

96

New cards

Advantages of an oligopoly

* provides consumer with some choice

* non price competition leads to good quality goods and services

* EOS allows firms to benefit from AC and this allows for lower prices

* large firms have resources to invest in R n D → leading to investment

* Price wars are avoided so generally there is price stability

* non price competition leads to good quality goods and services

* EOS allows firms to benefit from AC and this allows for lower prices

* large firms have resources to invest in R n D → leading to investment

* Price wars are avoided so generally there is price stability

97

New cards

Disadvantages of an oligopoly

* price fixing and collusion

* price fixing can lead to extremely high prices

* if a market is shared out geographically there will be a lack of choice

* cartel

* price fixing can lead to extremely high prices

* if a market is shared out geographically there will be a lack of choice

* cartel

98

New cards

What is a cartel?

where a group of firms or countries join together and agree on pricing or output level of the market

99

New cards

What is the wage rate?

The price of labour

100

New cards

What factors affect the demand for labour?

* derived demand

* availability of substitutes- replacement with capital

* productivity of labour

* other employment costs

* availability of substitutes- replacement with capital

* productivity of labour

* other employment costs