RISK INS / 4.1 & 4.2

1/24

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

25 Terms

Premium principles depend exclusively on

Assumptions

Uninsurable Risk

We will assume that X is a bounded non-negative random variable.

Most premium principles can also be applied to unbounded and possibly negative claims.

When the result is an infinite premium, the risk at hand is uninsurable.

Premium Principles

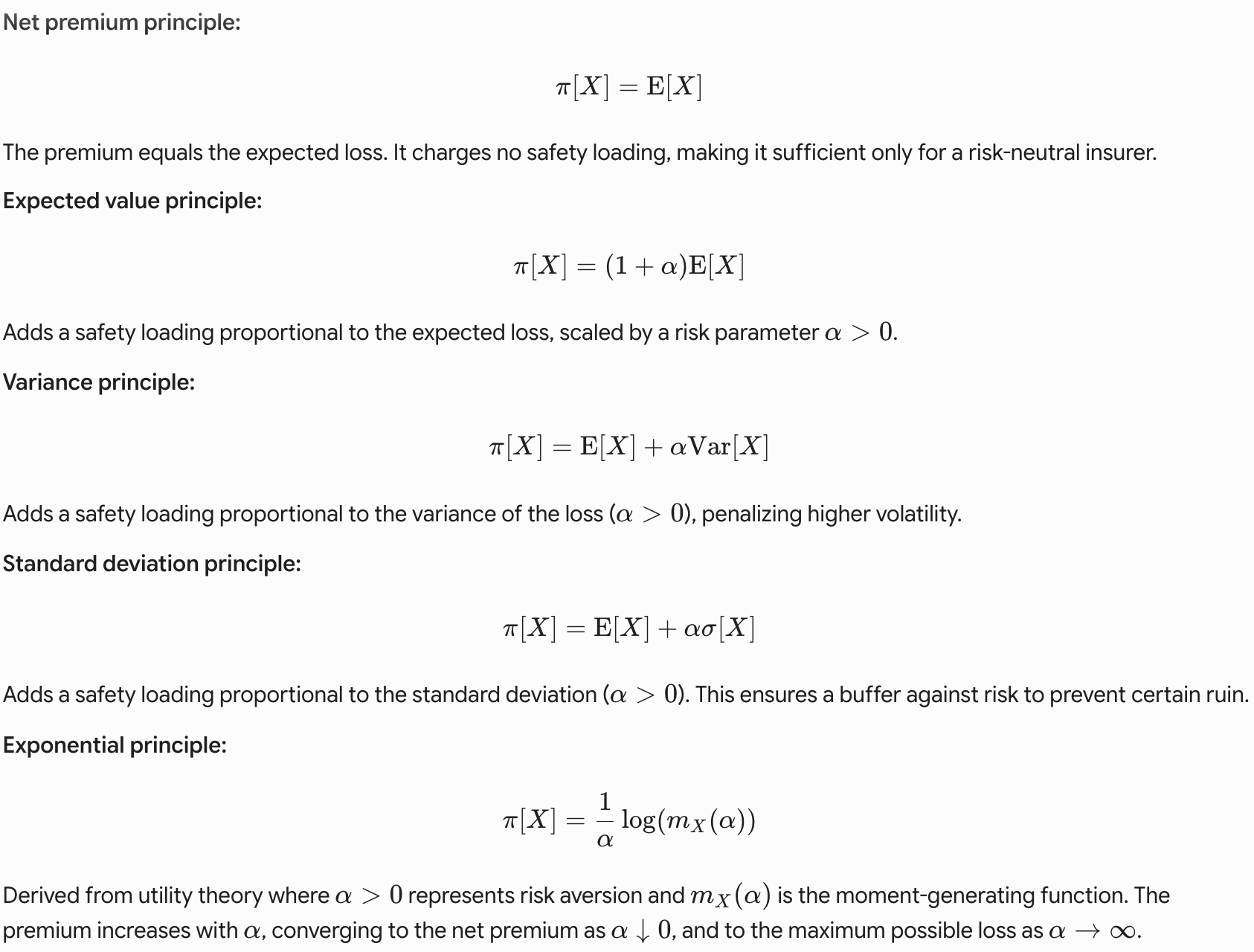

Net Premium

Expected Value Principle

Variance Principle

Standard Deviation Principle

Exponential Principle

Premium Principles

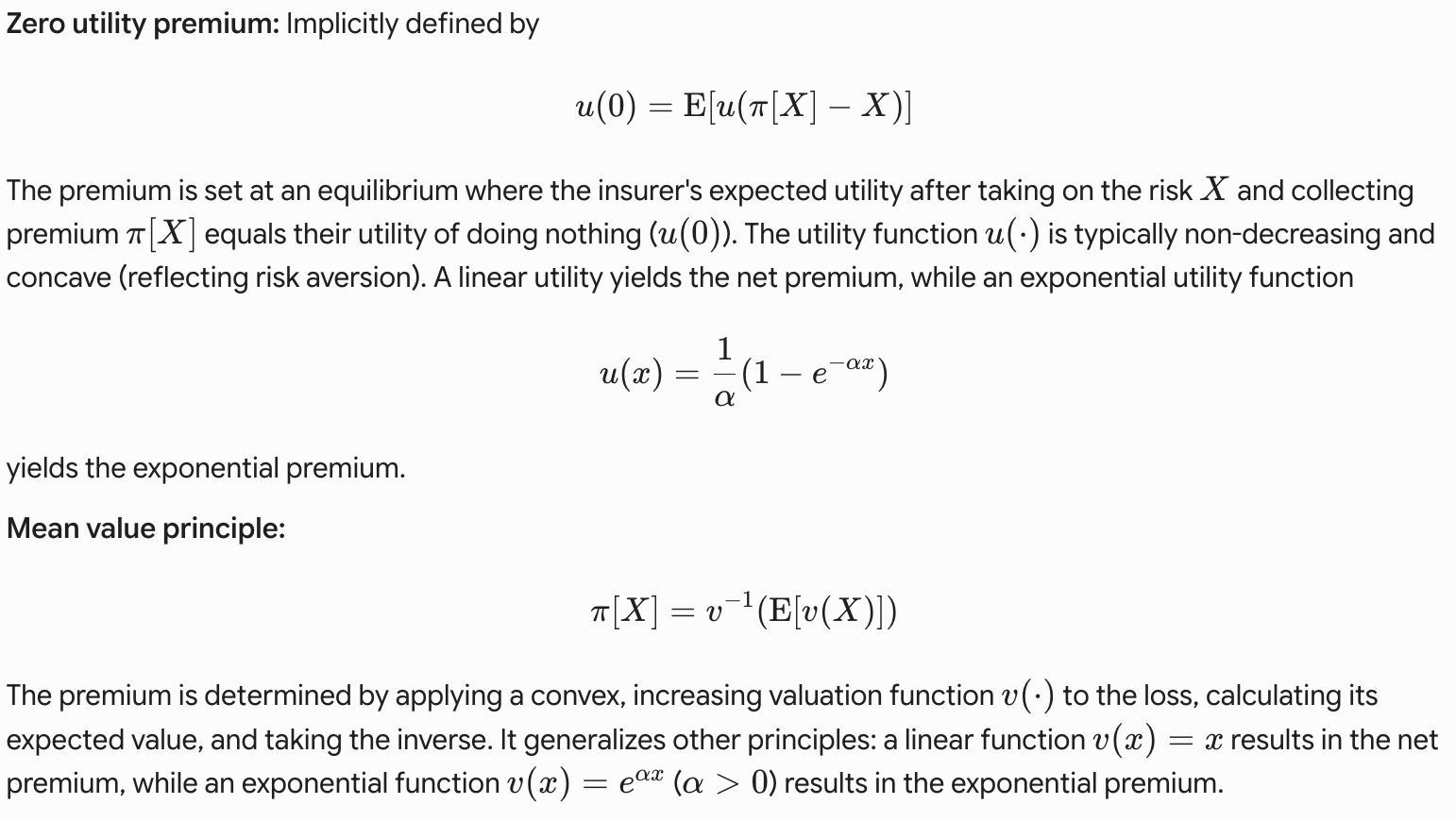

Zero Utility Premium

Mean Value Principle

In these two premium principles, the ‘parameter’ is a function

Premium Principles

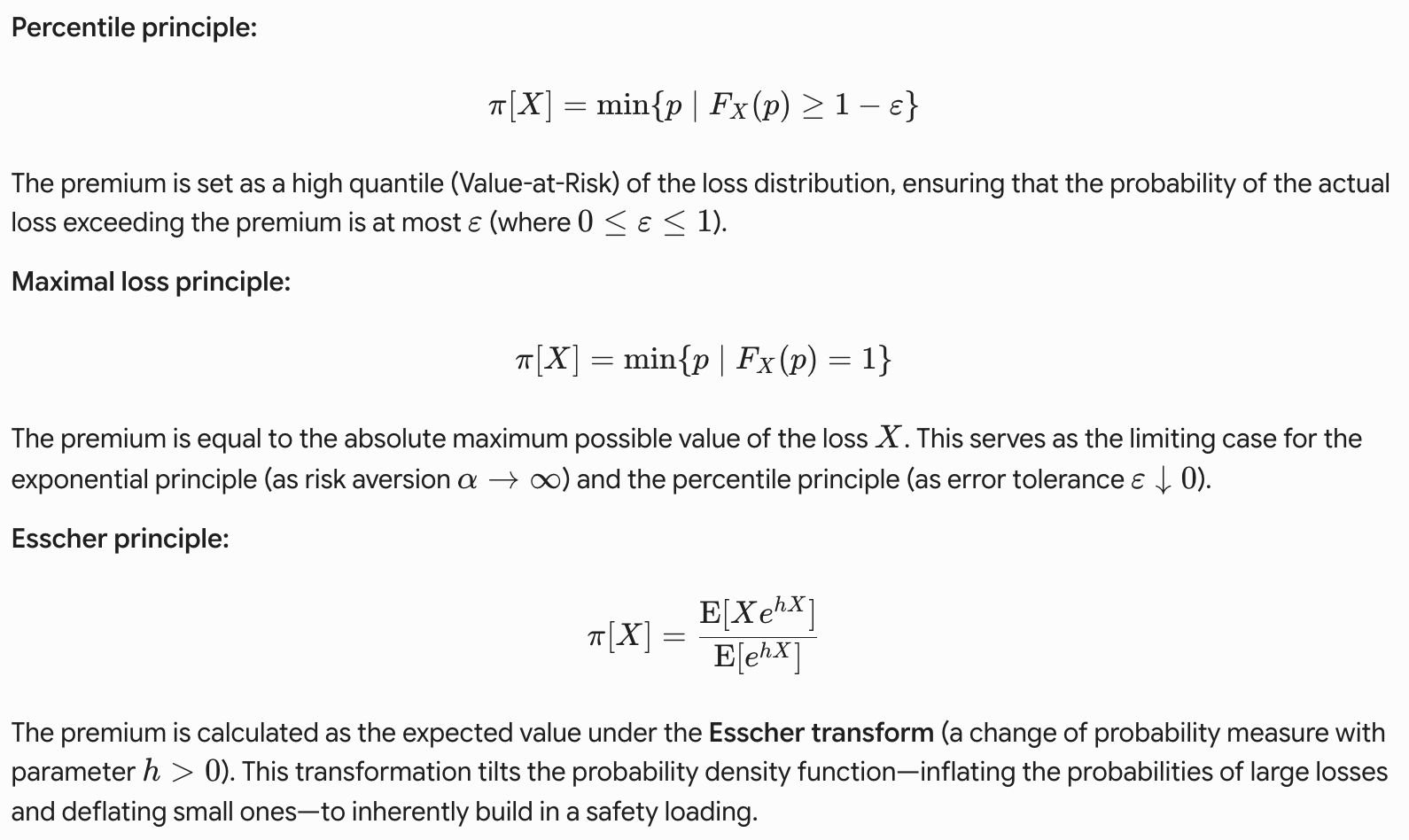

Percentile Premium

Maximal Loss Principle

Esscher Principle

These premium principles are chiefly of theoretical importance

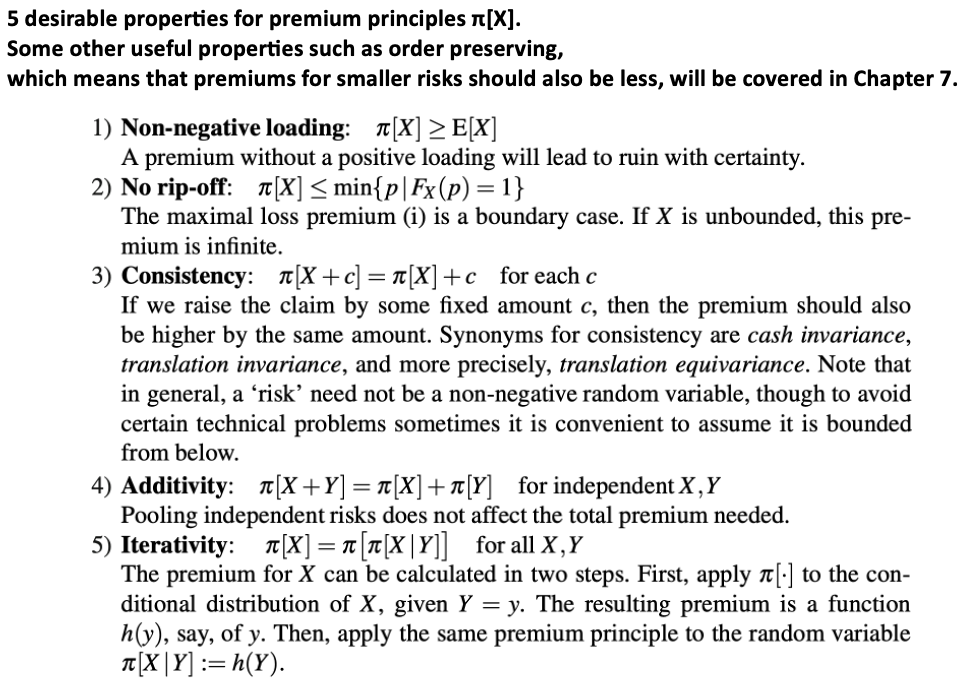

Properties of Premium Principles

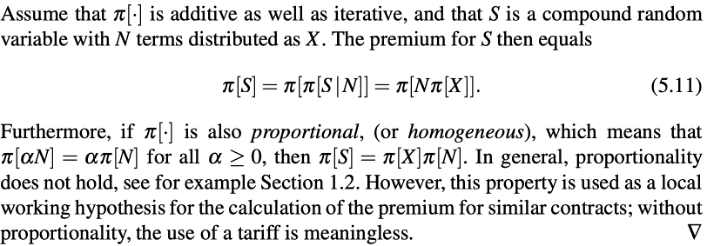

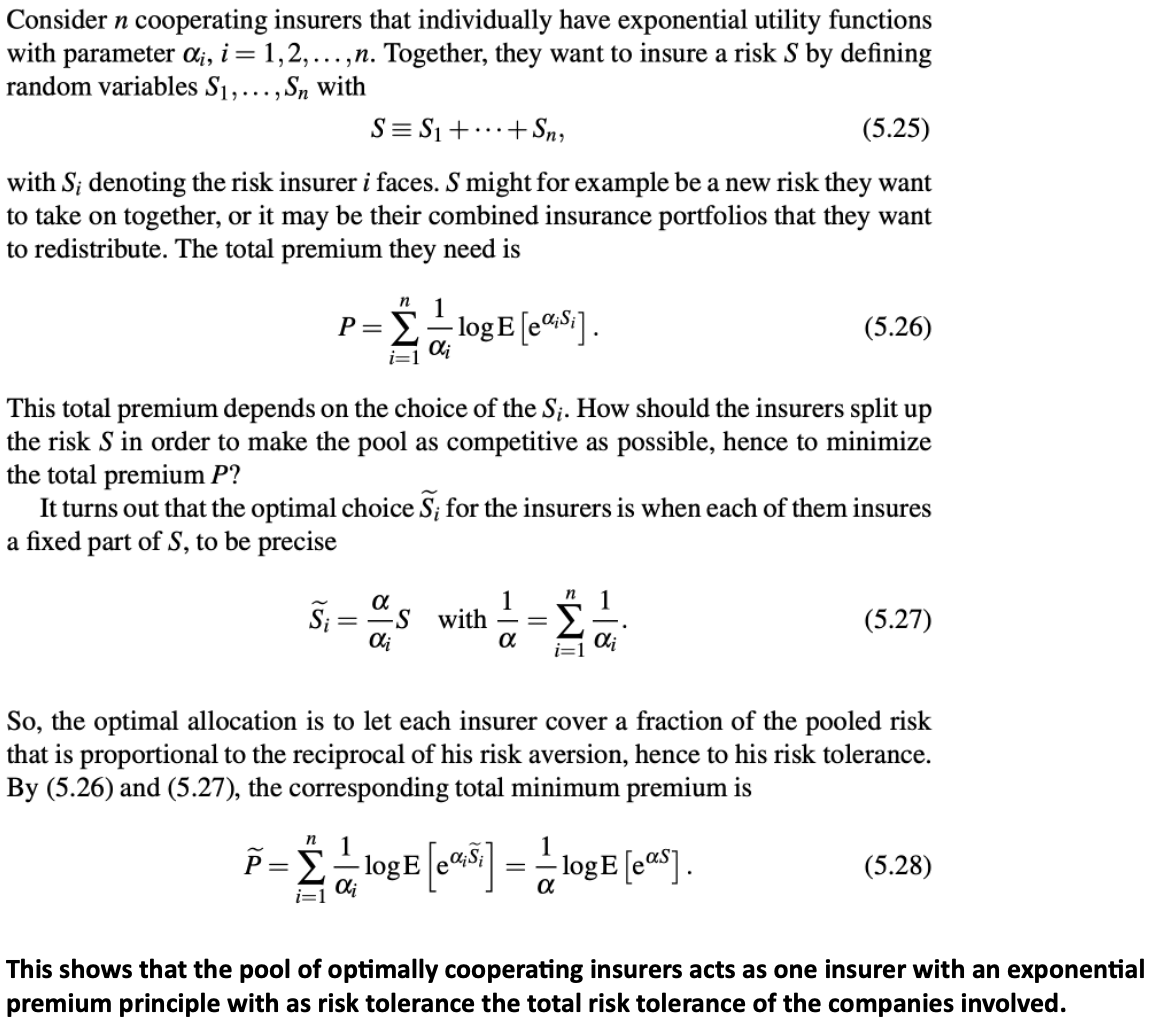

If π is additive as well as iterative, and S is a compound r.v. with N terms distributed as X

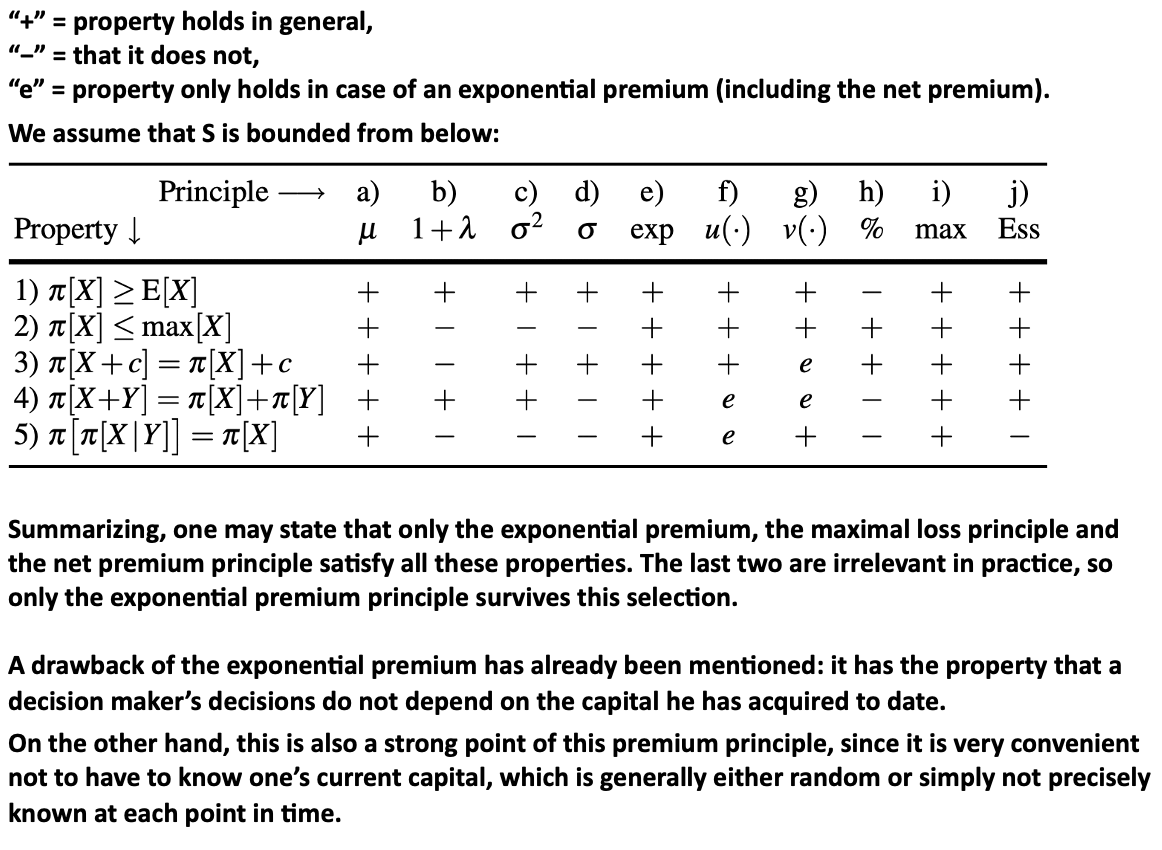

Premium Principle (Properties) Summary

Premium Reduction by Coinsurance

Bonus-Malus Systems

Introduction

A Generic Bonus-Malus System

Bonusmalus Scale

A Generic Bonus-Malus System

Introduction

A Generic Bonus-Malus System

How to determine Premium?

& Bonusmalus Scale

A Generic Bonus-Malus System

Ex post factor

Fixed ex ante

A Generic Bonus-Malus System

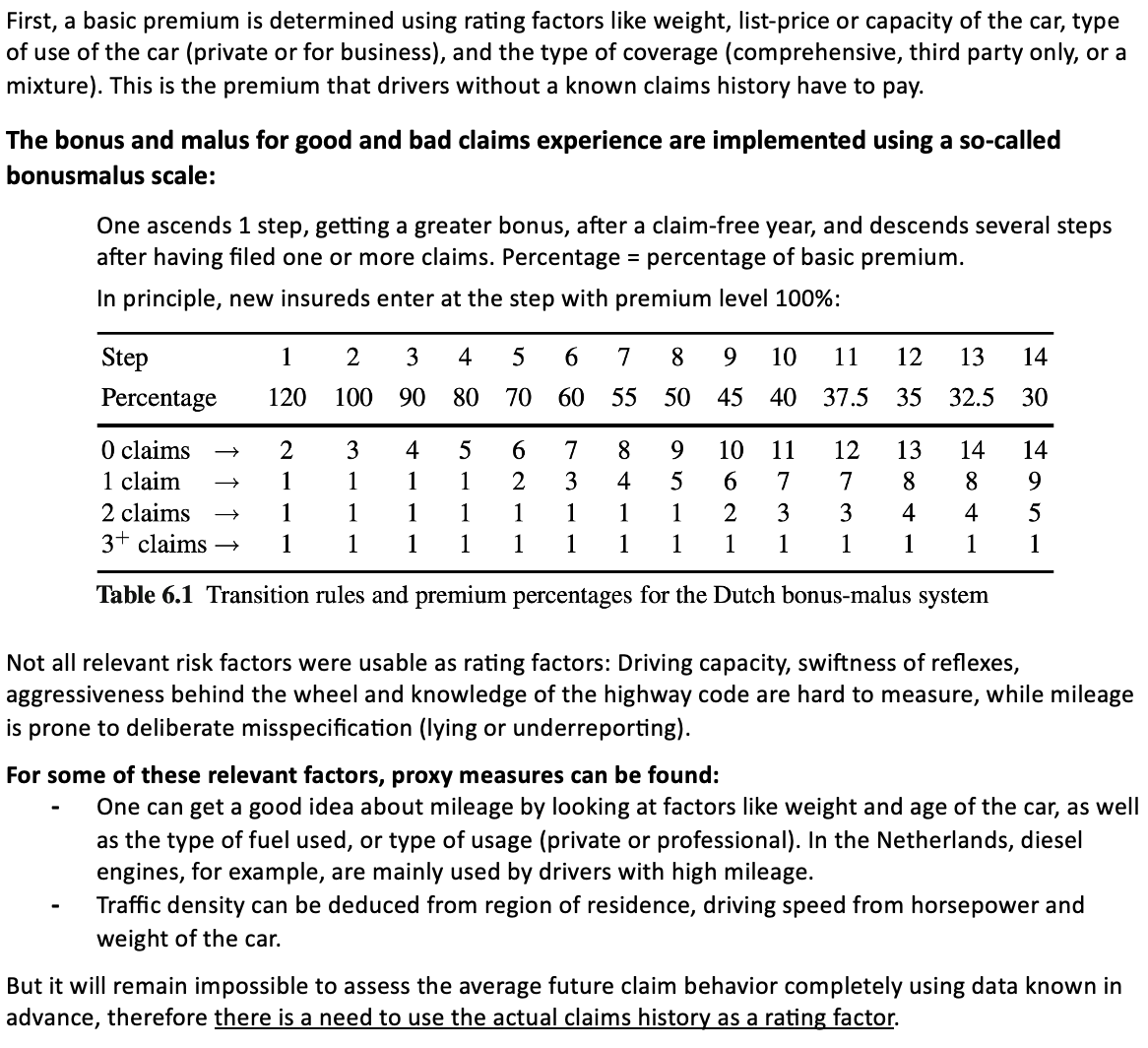

In the investigation, the following was found:

Note on bonus-malus system

Bonus-Malus Systems

Markov Analysis

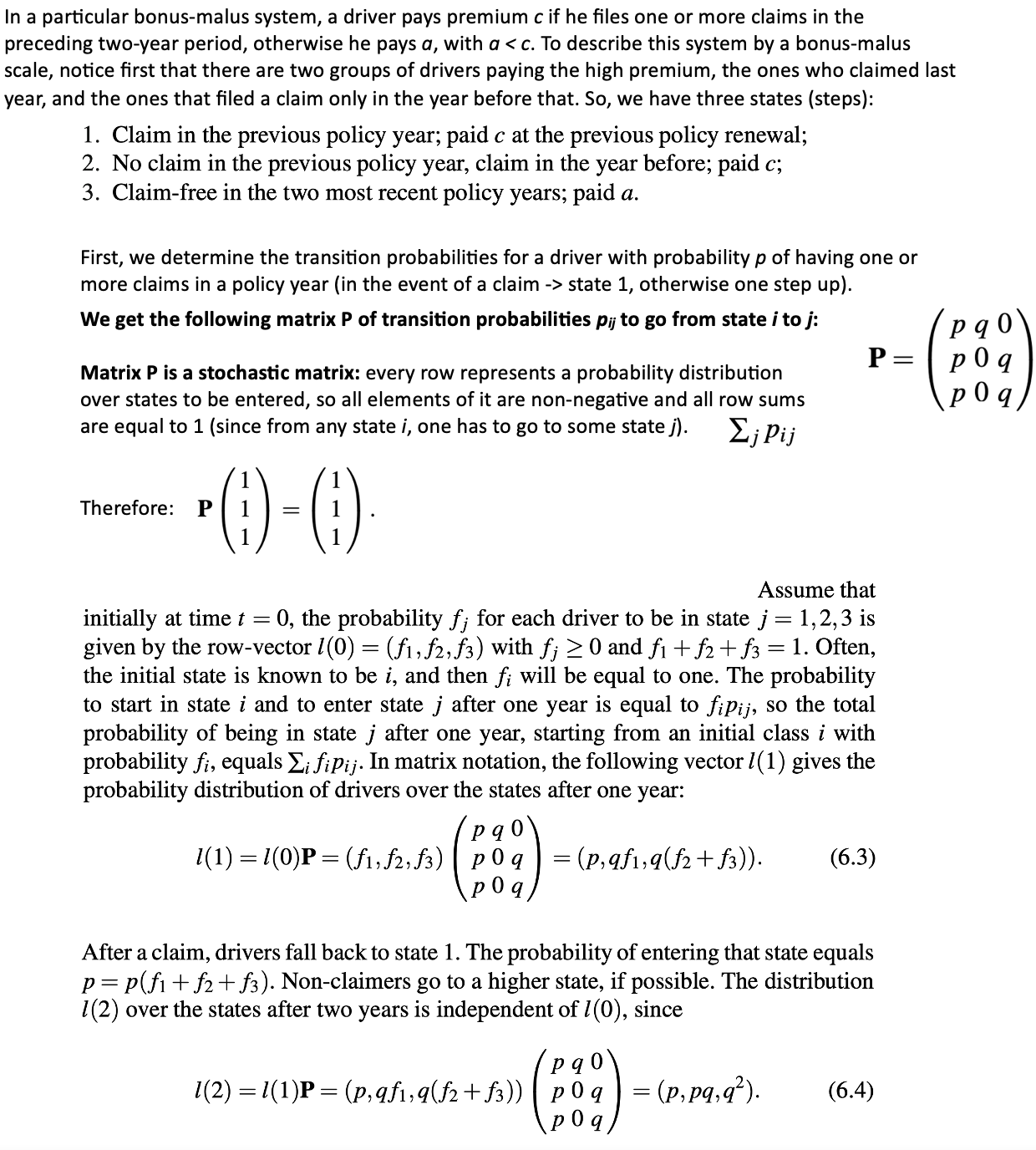

Bonus-Malus Systems: Markov Analysis

Transition Matrix

Bonus-Malus Systems: Markov Analysis

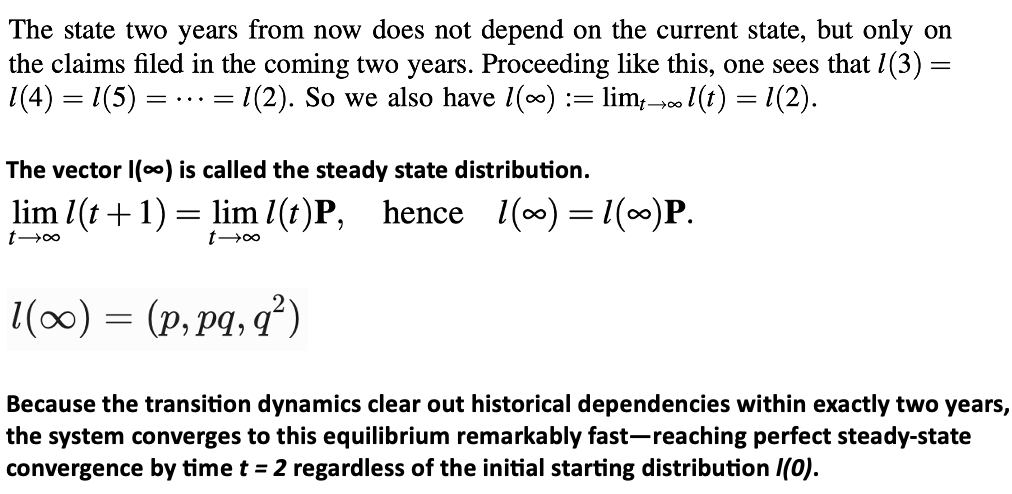

Steady State Distribution

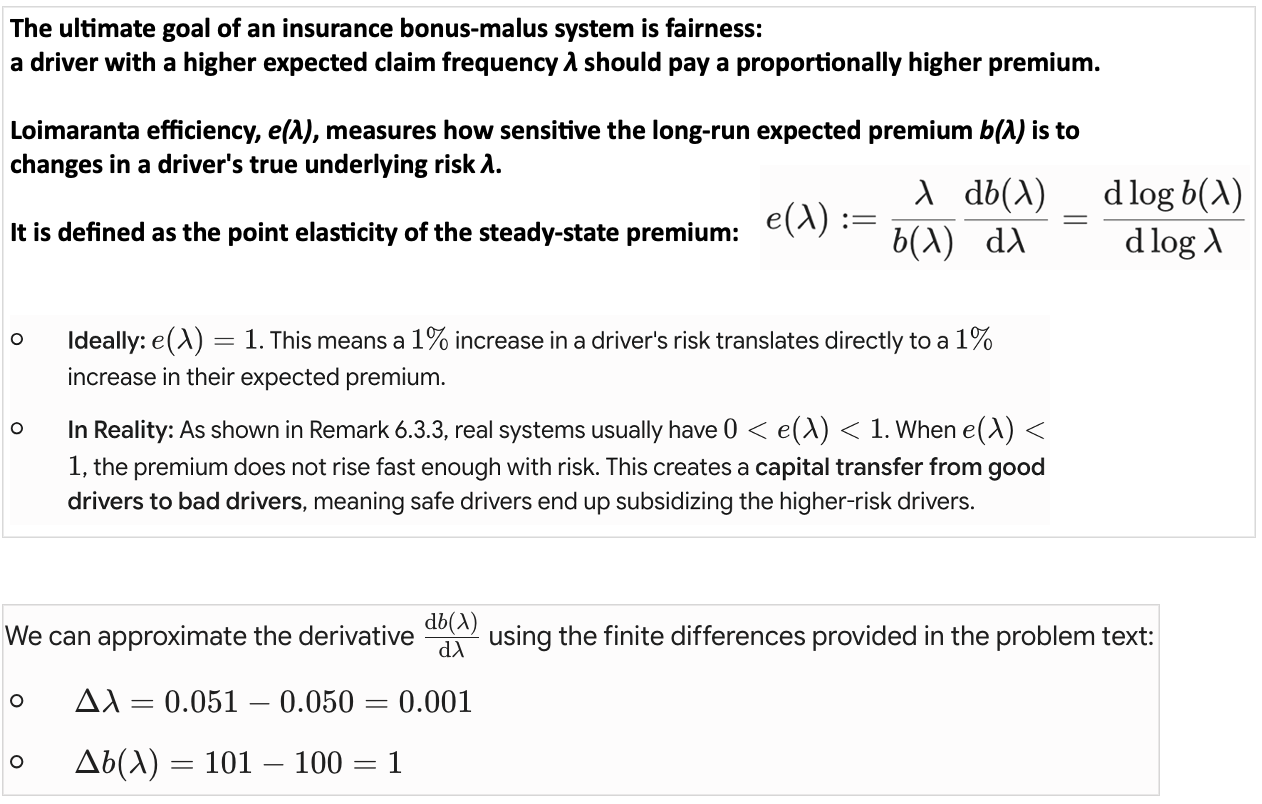

Loimaranta Efficiency

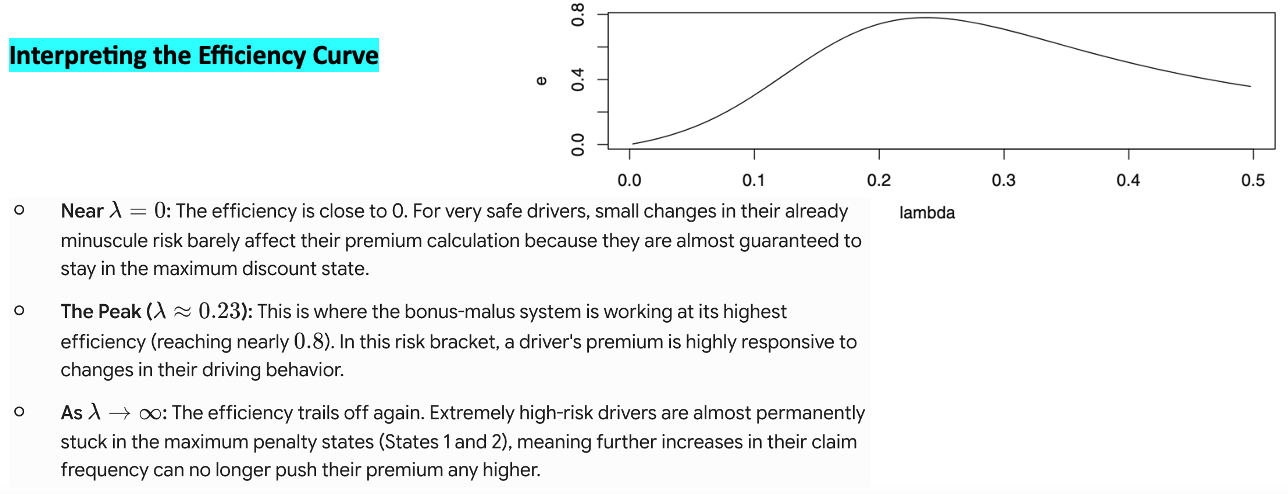

Interpreting the Efficiency Curve

Finding Steady State Premiums & Loimaranta efficiency

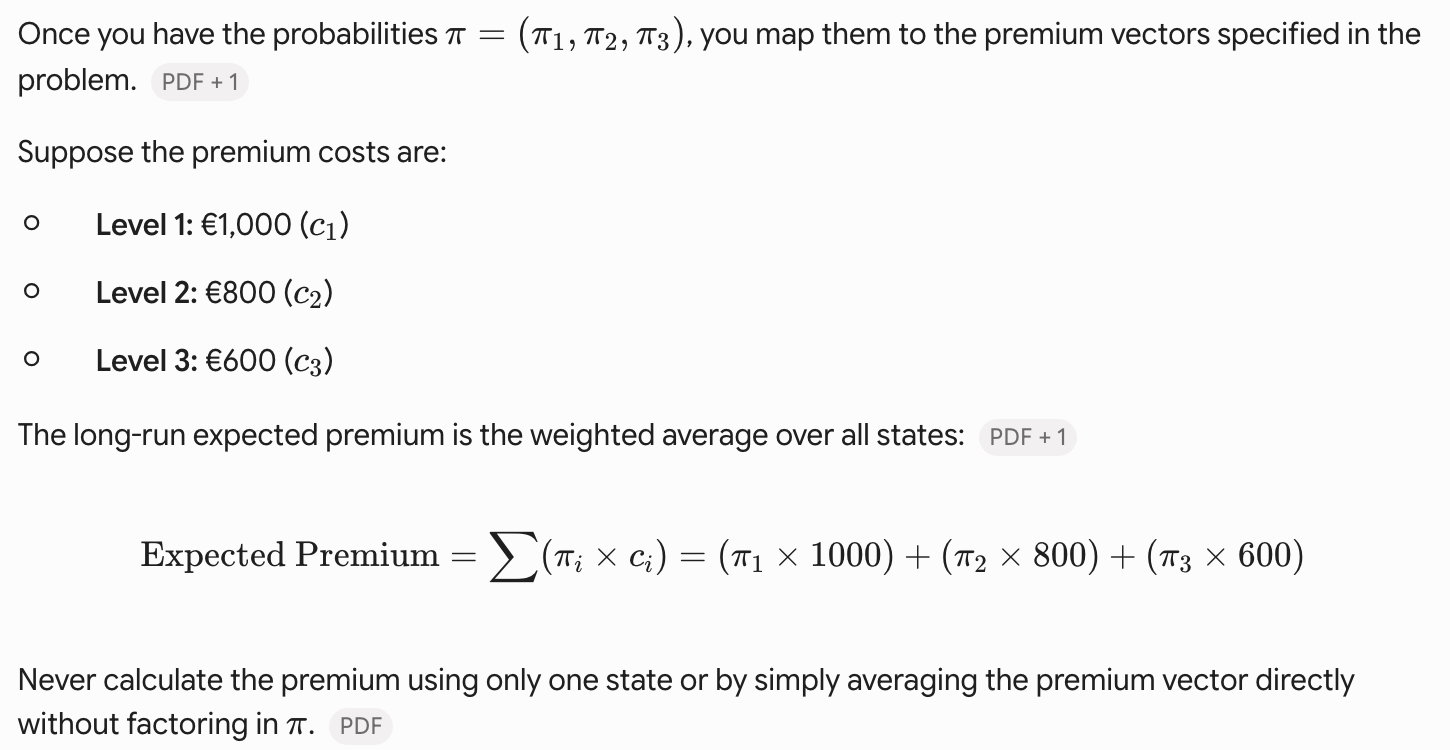

π = …

when dealing with Bonus-Malus systems modeled as Markov chains

Solving for the Stationary Distribution (π)

Calculating the Long-Run Expected Premium