Economics Exam Revision

1/66

Earn XP

Description and Tags

Microeconomics, Macroeconomics & Globalization

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

67 Terms

Definition of economics

The study of society’s optimal use of scarce resources (land, labour capital)

Needs

Things necessary for survival

Wants

things that are desired but not essential

Economic resources

land, labour, capital, entrepreneurship skills

Land

natural resources (water, soil, trees)

Labour

human resources (employees)

Capital

man-made resources (machinery)

Entrepreneurship Skills

skill and talent to combine the other resources (factory owner)

Opportunity cost

The cost forgone of the next best option when the best option is selected

Objective of consumers

to maximise their own economics welfare (satisfaction or utility)

Objective of firms

to maximise their profits

Objective of government

to maximise the welfare of their citizens

Types of economic systems

traditional, capitalism, planned, mixed

Traditional economic system

self-sufficient, barter, exchange of goods and services

Capitalism economic system

people are free to choose the way they will allocate their resources to gain the highest return

Planned economic system

decisions in regard to resource allocation are made by a central planning agency (e.g. Cuba)

Mixed

some elements of both planned a capitalist (e.g. China)

Basic economic questions

How will it be produced?

What will be produced?

For whom will it be produced for?

Definition of market

Where goods and services are bought and sold at prices negotiated between the buyer and seller. Markets attempt to solve the economic problem by allocating scarce resources to meet wants.

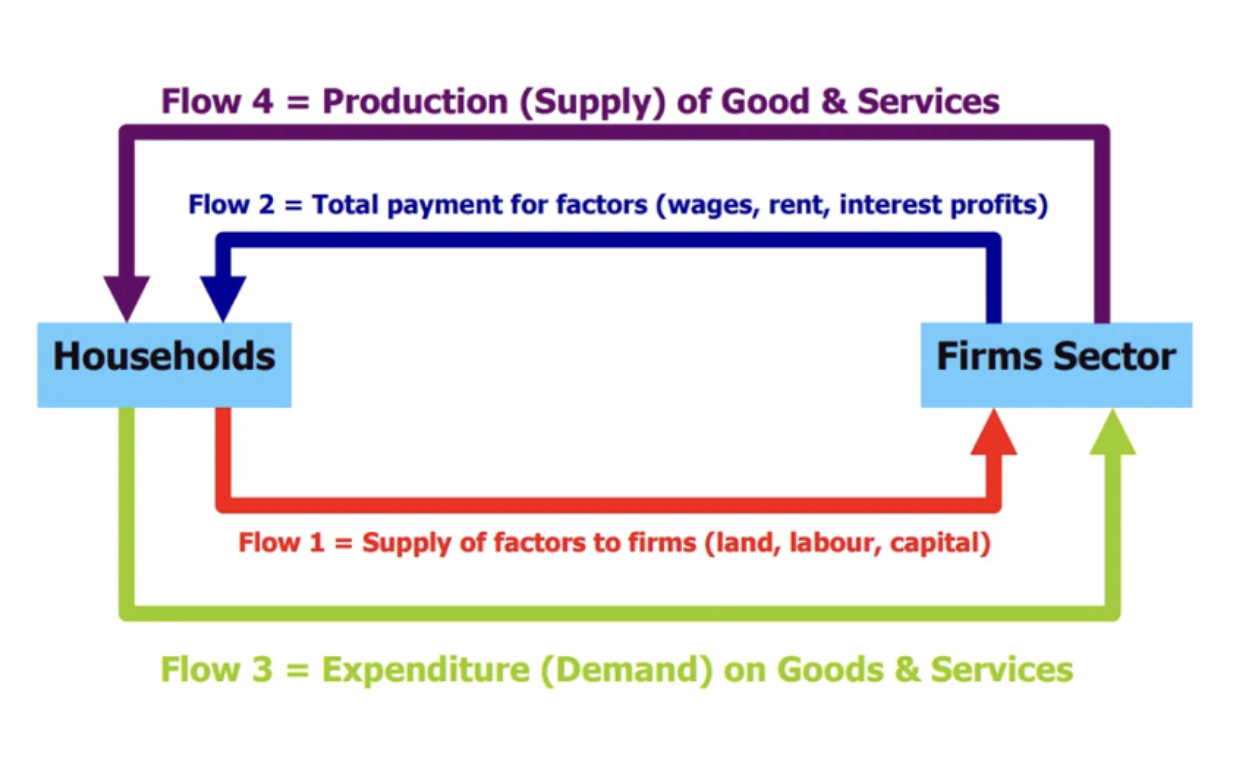

Circular flow of income

Assumption of perfect competition

All people act in a rational manner to maximise their standard of living

There are many buyers in the market, and there are many sellers

Products can only be distinguished by price

Buyers and sellers have perfect knowledge of the market

Resources are perfectly interchangeable

There is no government intervention

The law of demand

As price decreases, demand increases

Definition of demand

Demand refers to the consumer's willingness and ability to purchase a good or service at a given price over a given time.

The law of supply

As prices increase, supply will increase

Definition of supply

Supply refers to the quantity of goods/services

Intersection of supply and demand

The intersection of the demand and supply is equilibrium. This is where the supply is equal to the demand. Surplus is when the price is above the equilibrium price. Shortage is when the price is below the equilibrium price.

Non price factors of demand

taste, preference, fashion

Non price factors of supply

producers preference, level of technology, seasonal influence

Price factors of supply

price of other goods, taxes, cost of production

Price factors of demand

price of substitute goods, price of compliments, income

Shift left of the curve

Contraction

Shift right of the curve

Expansion

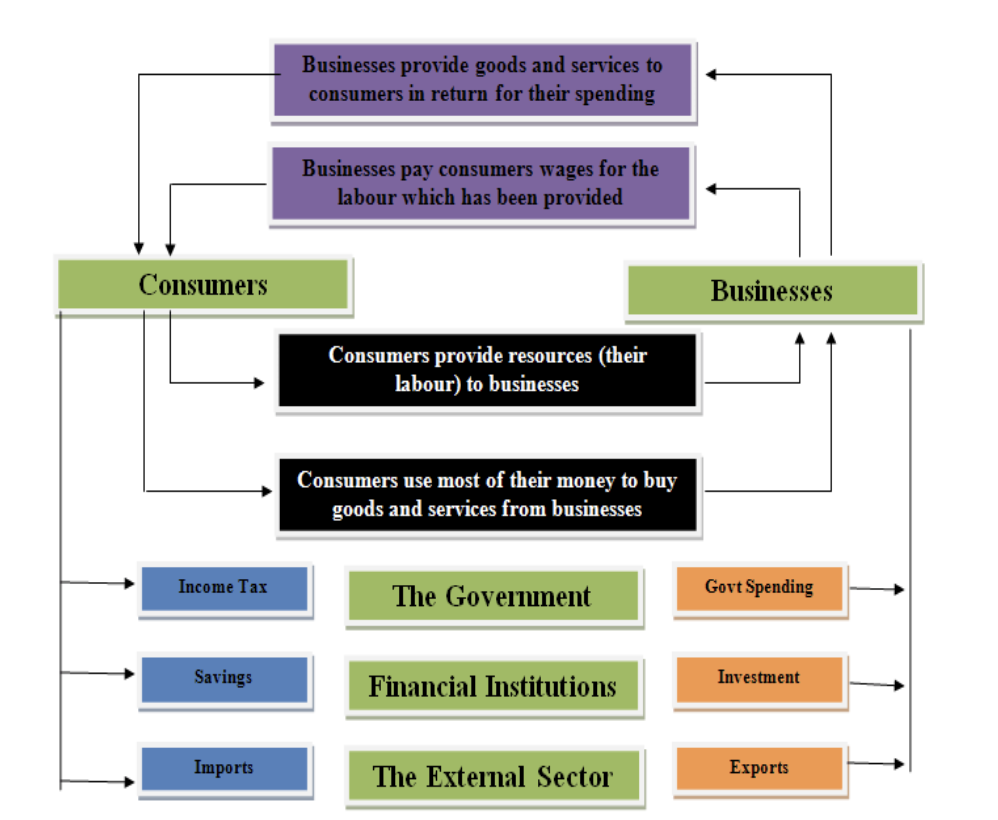

5 sector flow model

Macroeconomics goals

full employment, strong and sustainable economic growth, low and stable inflation

Inflation

The rate of increase in prices over a period of time (impacts: reduces demand, diminishes savings), goal inflation → 2%-3% per annum

Consumer price index

measure of average change over time in prices paid by urban consumers for a market basket of consumer goods and services

Unemployment definition

Those of the working age who are not employed, carrying out activities to seek employment during a specific period.

Full employment

people who are both willing and able to find work are able to do so, aiming for unemployment between 4% and 5%.

Economic growth

more goods and services are produced/consumed in the country in this year than last year, hoping for a higher standard of living. The government aims to achieve a sustainable level of economic growth, having acceptable living standards but enough resources for the future. Goal economic growth → 3%-3.5% per annum

GDP

Gross domestic product is what measures economic growth, representing total volume/quantity of goods and services produced in Australia over a period of time.

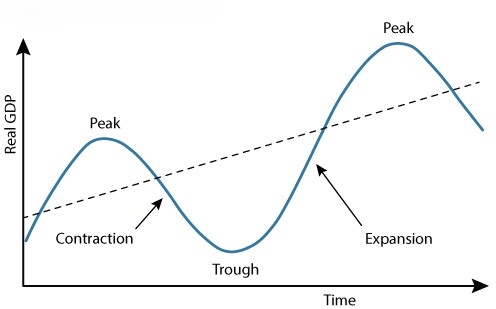

Business cycle/economic cycle

Types of unemployment

Frictional unemployment (including seasonal), Cyclical unemployment, Structural unemployment

Frictional unemployment

The unemployment due to people being in the process of moving from one job to another

Cyclical unemployment

The overall demand for goods and services in an economy cannot support full employment

Structural unemployment

A mismatch between the jobs available and the skill levels of the unemployed (often for the demand of specific types of labour/skills, e.g. laying off workers because they don’t have the necessary IT skills)

Globalisation

A process by which national and regional economies, societies, and cultures have become integrated through the global network of trade, communication, immigration and transportation.

Material living standards

The quality of peoples lives measured by their ability to purchase goods and services. If the economy is contracting, this means less people have a job (increase in unemployment), so those people will have less money to buy goods and services, meaning their material living standards will decrease.

Non material living standards

The quality of people’s lives as measured by a variety of, often intangible, indicators, such as happiness, health and level of education.

Imports

goods or services brought into a country (for e.g. Australia) from another country (for e.g the US)

Exports

good or service produced in one country (for e.g. Australia) and sold to a buyer abroad (for example, to China).

Benefits of trade

availability of goods and services, increased competition, productive efficiency, allocative efficiency, learning, access to markets, economies of scale, production costs, source of foreign exchange,

Drawbacks of trade

domestic job losses due to increased competition, potential for exploitation of resources and labor, and the risk of currency fluctuations impacting businesses

Types of trade protection

tariffs, quota, subsidies, administrative barriers

Tariffs

Tariffs are taxes put on imported goodsas they enter the domestic economy and haveto be paid by the individual or organisationimporting the goods.

Quotas

A quota is a method of trade protectionwhere a domestic government sets either avalue or a quantity limit on imported goods intothe domestic economy.

Subsidies

By subsidising domestic producers, governments are giving their producers a cost advantage over foreign producers, which acts as a trade barrier.

Administrative barriers

Administrative trade barriers occur when the government imposes excessive rules, regulations, and bureaucracy on imported goods.

Exchange rate definition

An exchange rate is the price of one country's currency compared to another country’s currency.

Currency appreciation

Currency gets stronger, imports are cheaper, exports are more expensive, tourists get more foreign currency

Currency depreciation

Currency gets weaker, imports are more expensive, exports are cheaper (better for exporters), tourists get less foreign currency

Economic integration

The economies of different countries move closer together in terms of their trading relationships and economic policy making.

Free trade

Where goods and services are exchanged across borders without tariffs or government regulations

Cause of inflation

Rising Production Costs: higher raw material costs, wage increases, or supply chain disruptions can cause businesses to raise prices to maintain profitability, driving up the overall price level.

Imbalance Between Supply and Demand:

When demand for goods and services outpaces supply, prices tend to rise as consumers compete for limited resources. This can be caused by increased consumer spending, government spending, or a rise in exports.

Effect of inflation

Higher Interest Rates:

Central banks often raise interest rates to curb inflation by making it more expensive to borrow money, which can slow down economic activity.

Economic Instability:

Inflation can create uncertainty in the economy, leading to reduced investment, saving, and consumer confidence.

Impact on Exports and Imports:

Higher inflation can make a country's exports more expensive in the global market, potentially harming trade competitiveness, and increase the cost of imported goods.

Goal inflation rate

2%-3% per annum

Goal unemployment rate

4-5%

Economic growth goal percentage

3-3.5%