ECON 151/151G

0.0(0)

Studied by 1 personCard Sorting

1/50

Earn XP

Description and Tags

Last updated 10:33 AM on 9/16/22

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

51 Terms

1

New cards

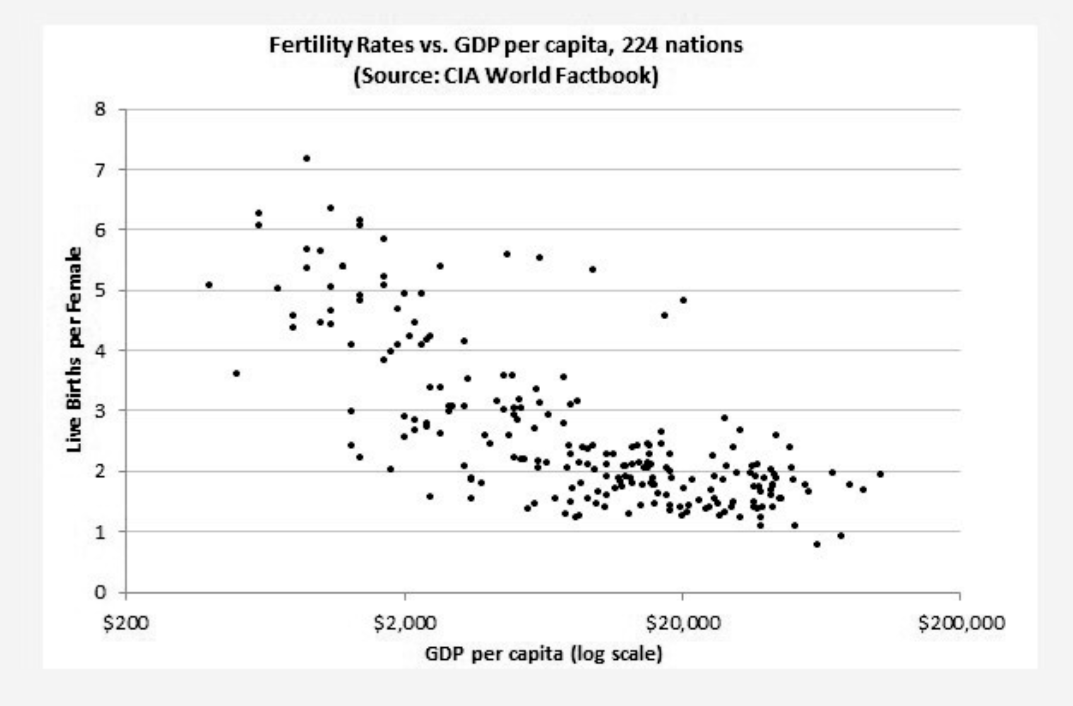

NZD GDP

- Small due to population size

- Countries with higher GDP have higher purchasing power

- Countries with higher GDP have higher purchasing power

2

New cards

Purchasing Power

- Ability to buy things

3

New cards

Less children in richer countries

- Less children => less costs => higher quality of life

Children can receive the best education and support

- People are wanting more qualifications => more studying and working much harder. Less time for children

Children can receive the best education and support

- People are wanting more qualifications => more studying and working much harder. Less time for children

4

New cards

Opportunity cost

- Value of an activity/goods/service given up in order to get something else

- Not all needs can be satisfied

- Everything is scarce

- Choices have to be made

- Value of the next best alternative

- Not all needs can be satisfied

- Everything is scarce

- Choices have to be made

- Value of the next best alternative

5

New cards

Low birth rates

- When the population becomes "older" on average (fewer young people)

- Retirement benefit comes from taxes

- Not enough young people => not enough salary/tax for benefit

- Raises retirement age

- Retirement benefit comes from taxes

- Not enough young people => not enough salary/tax for benefit

- Raises retirement age

6

New cards

Cost-Benefit Principle (Marginalism)

- Take an action if and only if the extra benefits are at least as great as the extra cost

- Costs and benefits are not just money

- Costs and benefits are not just money

7

New cards

Marginal Cost

- Increase in total cost from one addition unit of activity

8

New cards

Marginal Benefit

- Increase in total benefit from one additional unit of activity

9

New cards

Sunk costs

- Cannot be recovered

Examples: time, paying for something you don't like

Examples: time, paying for something you don't like

10

New cards

Correlation vs Causation

- If two things go together, it does not mean one causes the other

- Sometimes the correlations are purely coincidental

- Sometimes the correlations are purely coincidental

11

New cards

Correlation

- Relation between two things

12

New cards

Causation

- One thing makes another thing happen

13

New cards

Ceteris Paribus

- When looking at an effect of X on Y, only look at what happens to Y when X changes and everything else is constant

- ONLY CHANGE ON THING AT A TIME

- ONLY CHANGE ON THING AT A TIME

14

New cards

Occam's Razor

- Make as few assumptions or involve as few other variables as possible

15

New cards

Role of assumptions

- Models are simplifications of reality, making simplifying assumptions

- Real world is too complex, need models which focus on important part of reality

- Real world is too complex, need models which focus on important part of reality

16

New cards

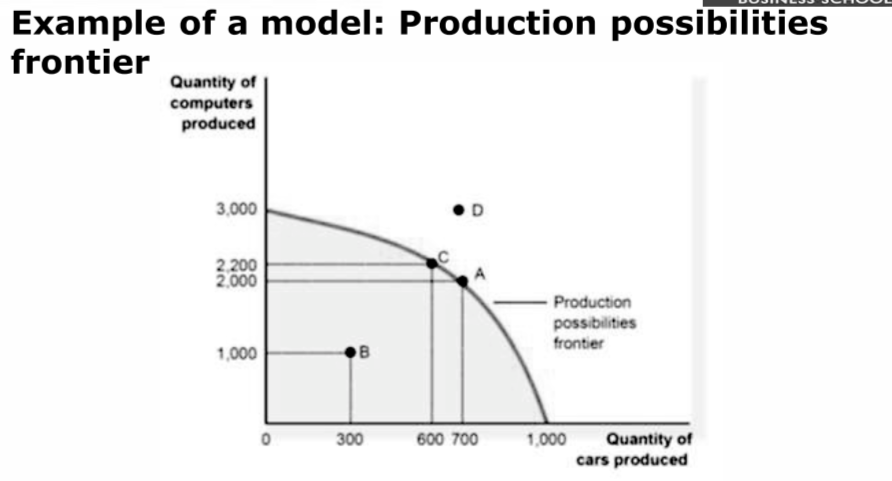

Production Possibilities Frontier (PPF)

- A graph that shows various combinations of output that the economy can possibly product given the available factors of production and the available production technology

- Simplifying assumption: economy produces only two goods

- An economy producing on the PPF is efficient

- Graph shows tradesoffs (produce more of one good and less both the other)

Example:

- Cannot produce outside the graph

- Point D is impossible (not enough resources)

- Point B is not utilising all resources

- Point C/A are ideal points, pick either more computers or more cars produced

- Simplifying assumption: economy produces only two goods

- An economy producing on the PPF is efficient

- Graph shows tradesoffs (produce more of one good and less both the other)

Example:

- Cannot produce outside the graph

- Point D is impossible (not enough resources)

- Point B is not utilising all resources

- Point C/A are ideal points, pick either more computers or more cars produced

17

New cards

Interdependence

- Relying on others to produce what we consume, which requires trade

18

New cards

Grains from trade

- Leave the specialist to do the things

- Get the best quality item for the best price

- Get the best quality item for the best price

19

New cards

Absolute Advantage (AA)

The comparison among producers of a good according to their productivity

- held by producer who can produce the good using the least amount of resources in absolute terms

- held by producer who can produce the good using the least amount of resources in absolute terms

20

New cards

Comparative Advantage (CA)

The comparison among producers of a good according to their opportunity cost

- held by the producer who can produce it at the lowest opportunity cost (this is what economy uses!)

- held by the producer who can produce it at the lowest opportunity cost (this is what economy uses!)

21

New cards

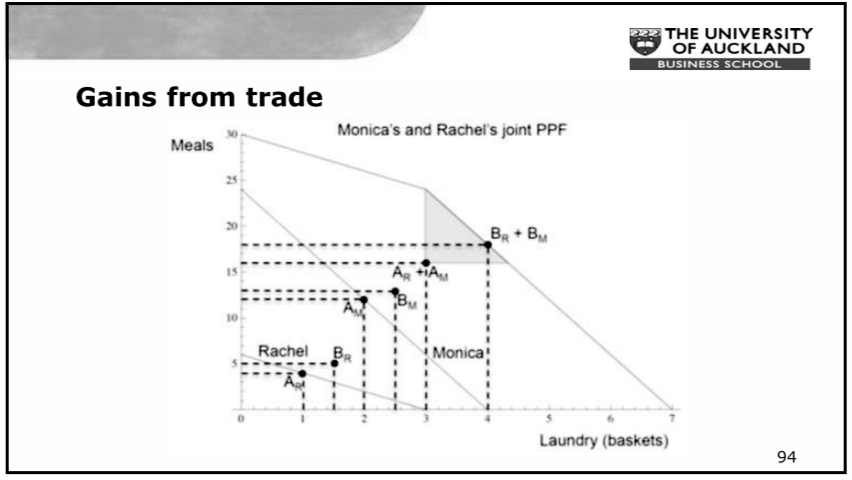

Gains from Trade - Application

- Combine both trader's PPF to find who should make how many

22

New cards

Topic 2

Topic 2 - Demand, supply, and market equilibrium

23

New cards

Market Equilibrium

- Equilibrium may change if demand and/or supply changes

24

New cards

Demand

- Consumers wanting to buy

25

New cards

Supply

- Sellers want to sell

26

New cards

Elastic

- Sensitive to price

- Will make a decision depending on the price

- Will make a decision depending on the price

27

New cards

Inelastic

Insensitive to price

- Will pay for given price (e.g. gas)

- Will pay for given price (e.g. gas)

28

New cards

Market

- A group of buyers and sellers of a particular good or service

- Buys determine demand

- Sellers determine Supply

- Can be real (shopping centres) or online (TradeMe/NZ Stock Exchange)

- Buys determine demand

- Sellers determine Supply

- Can be real (shopping centres) or online (TradeMe/NZ Stock Exchange)

29

New cards

Market Price

- Exchange goods and services for money

- Tells us how many dollars we receive per unit sold and how much $ we must give up per unit bought

- Assume people are "price-takers" (cannot negotiate price)

- Tells us how many dollars we receive per unit sold and how much $ we must give up per unit bought

- Assume people are "price-takers" (cannot negotiate price)

30

New cards

Quantity Demanded

Amount of a good that buyers are willing and able to purchase at every price

31

New cards

Determinants of Demand

Consumer Income - ability to pay

Prices of related goods - willingness to pay

Substitutes - Cook and Pepsi, Driving vs taking the bus

Complements - hamburgers and burger buns, cars and tyres

Tastes - willingness to pay; how much you value the good

Prices of related goods - willingness to pay

Substitutes - Cook and Pepsi, Driving vs taking the bus

Complements - hamburgers and burger buns, cars and tyres

Tastes - willingness to pay; how much you value the good

32

New cards

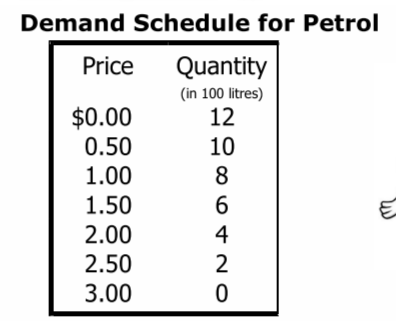

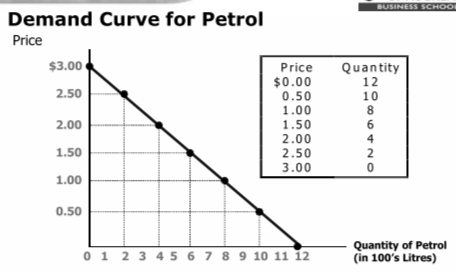

Law of Demand

- states there is an inverse relationship between price and quantity demanded

- demand schedule is a table that shows the relationship between price of a good and quantity demanded

- demand schedule is a table that shows the relationship between price of a good and quantity demanded

33

New cards

Demand Curve

- Downward sloping line relating to price and quantity demanded

Downwards because:

- lower prices imply a greater quantity demanded

- diminishing marginal benefit (consume more of the same good, less happiness from extra units)

- opportunity cost

- income effect (prices go up, have less money to spend on everything and buy less goods)

- substitutions effect

Downwards because:

- lower prices imply a greater quantity demanded

- diminishing marginal benefit (consume more of the same good, less happiness from extra units)

- opportunity cost

- income effect (prices go up, have less money to spend on everything and buy less goods)

- substitutions effect

34

New cards

Ceteris Paribus

- All variables other than the ones being studied are assumed to be constant

- Demand curve slopes downward because lower prices imply greater quantity demanded

- Demand curve slopes downward because lower prices imply greater quantity demanded

35

New cards

Linear Demand curve

- The demand curve is most likely not linear but it is possible to approximate using a straight line

- Makes calculations easier

- Makes calculations easier

36

New cards

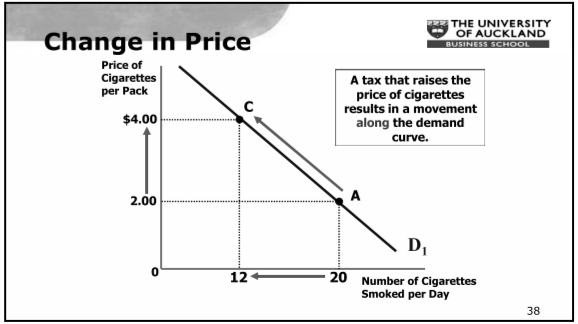

Change in Quantity Demanded

- Movement along the demand curve

- Caused by a change in price of a product

- Caused by a change in price of a product

37

New cards

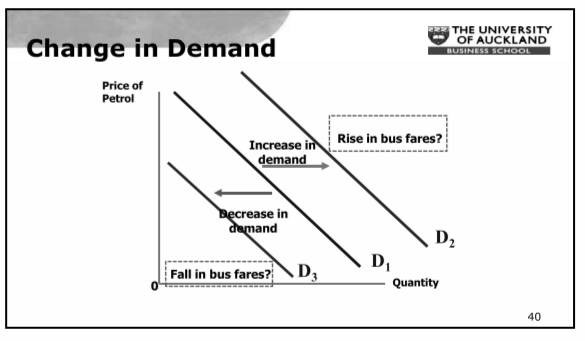

Change in Demand

- A shift in the demand curve, either to the left (decrease) or right (increase)

- Caused by a change in a determinant other than price

- Increase of consumer income will cause an increase in demand

- Caused by a change in a determinant other than price

- Increase of consumer income will cause an increase in demand

38

New cards

Substitutes and Complements

- When a fall in price of one good reduces the demand for another good, the two goods are substitutes

- When a fall in price of one good increases the demand for another good, the two goods are complements

- When a fall in price of one good increases the demand for another good, the two goods are complements

39

New cards

Rule of Thumb

- If the thing changes is one of the axis labels it will cause a MOVEMENT ALONG the curve

- If the thing that changes is not on the axis labels it will cause a SHIFT of the WHOLE CURVE

- If the thing that changes is not on the axis labels it will cause a SHIFT of the WHOLE CURVE

40

New cards

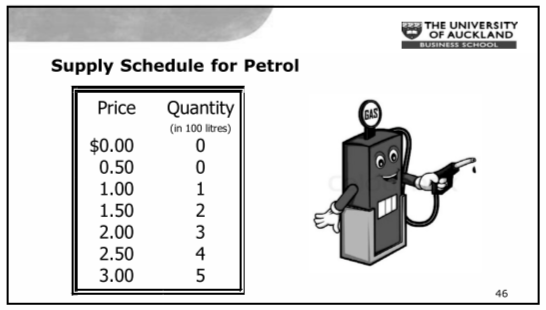

Supply

- Relationship between prices and quantity a firm can put on the market

- Technology and costs of production are major factors

- Law of Supply states that there is a positive relationship between price and quantity supplied

- Technology and costs of production are major factors

- Law of Supply states that there is a positive relationship between price and quantity supplied

41

New cards

Supply Schedule/Curve

- Upward sloping line relating price to the quantity supplied

Why:

- Market price is higher than the production price.

Why:

- Market price is higher than the production price.

42

New cards

Supply Determinants

- Cost of production

- Number of suppliers

- Technology

- Envrionment

- Number of suppliers

- Technology

- Envrionment

43

New cards

Change in Quantity Supplied

- Movement along the supply curve

- Caused by a change in market price of the product

- Caused by a change in market price of the product

44

New cards

Change in Supply

- A shift in the supply curve to the left (decrease) or right (increase)

- Cause by a change in determinant other than price

- Cause by a change in determinant other than price

45

New cards

Equilibrium Price

- The price that balances supply and demand. On graph the price at which supply and demand intersect.

- Sometimes called the Market clearing price

- Sometimes called the Market clearing price

46

New cards

Equilibrium Quantity

- The quantity that balances supply and demand. On graph its the quantity at which demand and supply intersects

47

New cards

Market Equilibrium

- Quantity demanded by consumers = quantity supplied by producers

- No tendency for market to move away from a stable equilibrium

- No tendency for market to move away from a stable equilibrium

48

New cards

Market Adjustment

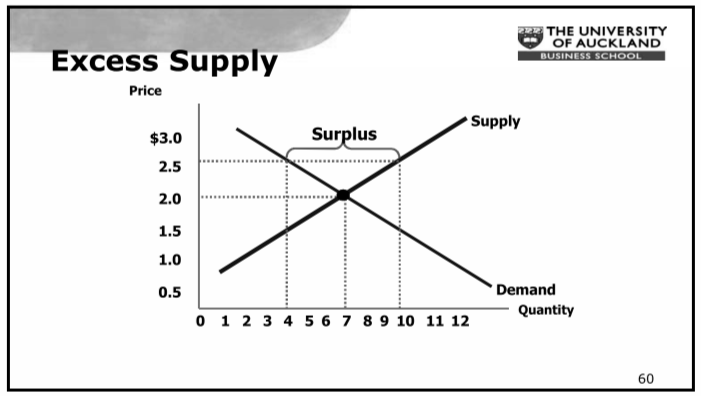

- Excess Supply (surplus) Qs>Qd

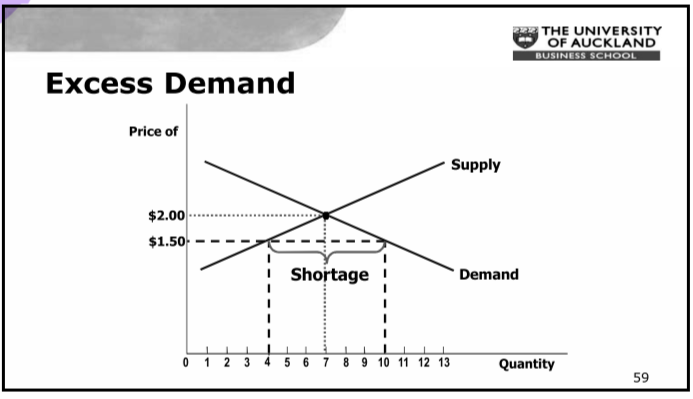

- Excess Demand (shortage) Qs<Qd

- Market forces will cause prices to adjust

- Excess Demand (shortage) Qs<Qd

- Market forces will cause prices to adjust

49

New cards

Excess Demand

50

New cards

Excess Supply

51

New cards

Page 91