econ 1021 midterm Luke (prob 2024) version b

1/33

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

34 Terms

Which one of the following correctly describes how price adjustment eliminates a surplus?

(A surplus occurs when the quantity supplied exceeds the quantity demanded at the current price. To eliminate a surplus, sellers lower the price.) As the price falls, the quantity demanded increases and the quantity supplied decreases.

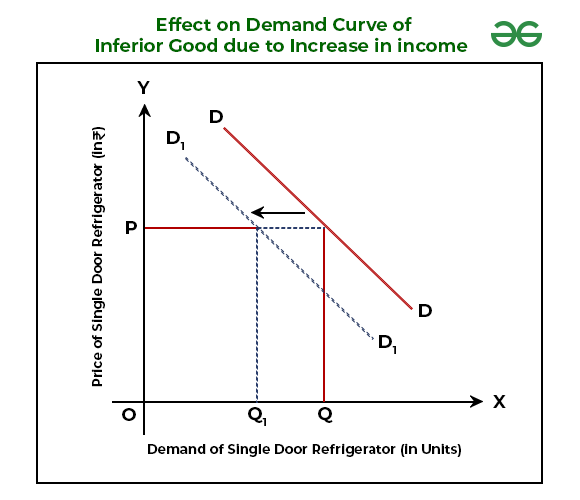

If A is an inferior good and consumer income rises, what happens to the equilibrium price and quantity?

(The demand for that good will decrease, causing the demand curve to shift to the left.) This decrease in demand leads to a lower equilibrium price and a lower equilibrium quantity in the market.

When the demand for the inferior good A increases, what happens to the the equilibrium price and quantity

Both the equilibrium price and equilibrium quantity will increase. This is because an increase in demand, regardless of whether the good is inferior or not, causes the demand curve to shift to the right, creates a shortage at the original price, which pushes the price upward (leading to a higher intersection with the supply curve). Consequently, consumers are willing and able to purchase more of the good at a higher price.

The law of supply tells us that other things remaining the same, as the cost of producing chocolates increase, what happens to the price of chocolates, because the producers are willing to supply less?

The law of supply describes the direct relationship between a good's price and the quantity producers are willing to supply, meaning as the cost to produce chocolates increases, producers are willing and able to supply less chocolate at each price point, shifting the supply curve to the left.

E) price of chocolate falls, the quantity of chocolate supplied decreases.

5) If Sam is producing at a point on his production possibilities frontier, then he

(KEEP IN MIND Every choice along the PPF involves a trade-off)

C) can increase the production of one good only by decreasing the production of the other.

Every choice along the PPF involves a trade-off, as producing more of one good requires sacrificing the production of another.

The Production Possibilities Frontier (PPF) represents the maximum output achievable with given resources and technology. Points on the frontier are efficient. To produce more of one good, you must sacrifice some of the other good because resources are scarce. This trade-off is the opportunity cost.

If Sam is producing at a point inside his production possibilities frontier, then he

A point inside the PPF represents an inefficient use of resources (e.g., unemployment or underemployment). From this point, it is possible to increase the production of both goods without sacrificing either, meaning the opportunity cost is zero until he reaches the PPF.

E) can increase production of both goods with zero opportunity cost.

If a large percentage drop in the price level results in a small percentage increase in the Qd

Price elasticity of demand measures the responsiveness of quantity demanded to a price change. If a large price drop leads to only a small increase in quantity demanded, the response is relatively insensitive, which defines inelastic demand.

DEMAND IS INELASTIC