Regional Concept #3: Inventory Costing Methods and Principles

1/22

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

23 Terms

Merchandise Inventory (MI)

Largest asset reported on balance sheet and income statement.

Costing an Item

Determining the cost associated with a specific item.

Inventory Record

Form used to record periodic inventory information.

Stock Record

Shows type, quantity received, sold, and balance.

Stock Ledger

File containing stock records for all merchandise.

Consistent Reporting

Same inventory costing method used each fiscal period.

FIFO

First-in, first-out inventory costing method.

LIFO

Last-in, first-out inventory costing method.

Weighted Average

Costing method using total COGA divided by units.

Specific ID

Costing method for large-ticket items based on purchase.

Cost of Goods Available for Sale (COGA)

Beginning inventory plus purchases available for sale.

Ending Inventory (EI)

Value of unsold inventory at the end of period.

Gross Profit (GP)

Net sales minus cost of goods sold (COGS).

Net Sales (NS)

Total sales revenue after returns and allowances.

Lower of Cost or Market

Inventory recorded at lower of cost or market value.

Conservatism Principle

Assets should not be overstated on financial statements.

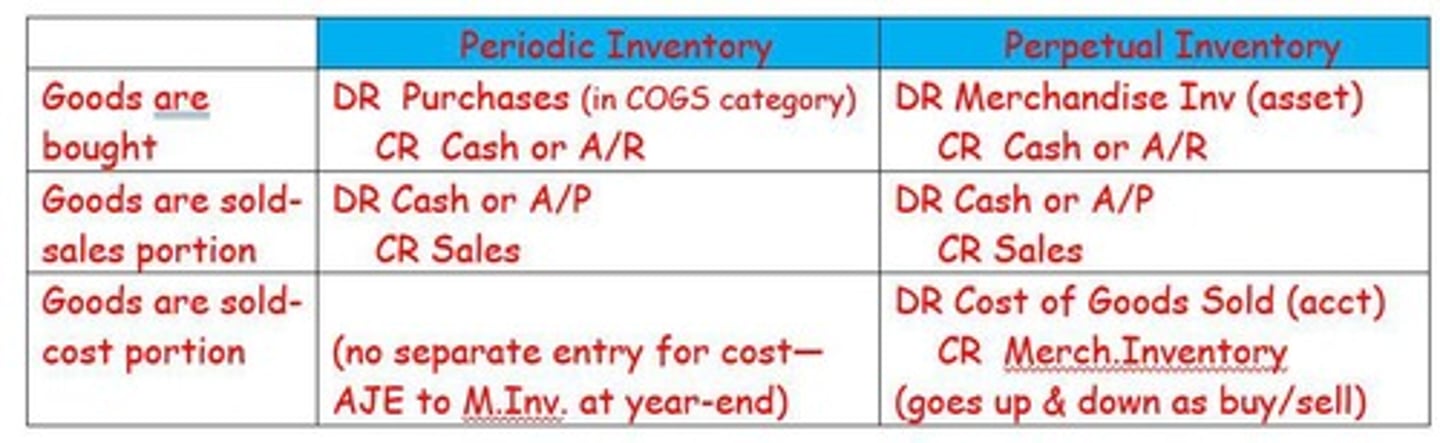

Periodic Inventory Method

Physical counting of inventory at specific intervals.

Perpetual Inventory Method

Continuous tracking of inventory levels and costs.

Gross Profit Method

Estimates ending inventory using gross profit percentage.

COGS

Cost of goods sold during a specific period.

Inventory Agents

Specialists hired to conduct inventory counts.

Universal Product Codes (UPCs)

Barcodes used for tracking inventory items.

Physical Inventory

Actual counting, weighing, or measuring of inventory.