chapter 1-3 macro

1/53

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

54 Terms

Why do economics exist?

To deal with the scarcity of resources and human wants.

study of how countries use resources to satisfy their unlimited needs or the individual want/

scarcity

imbalance of unlimited human wants and limited resources

Opportunity cost

cost of making a choice. it’s the next best alternative, subjective.

marginal analysis

the way desicions are made (based on current knowledge, hence marginal.) about deciding costs and benefits. The outcome benefits will be higher than the opportunity cost. MB >>MC

Incentive

something that encourages a change of behavior. The raised price of chocolate is an incentive not to buy chocolate.

three fundamental questions of market capital system

what to produce — decided by costumer behavior

how to produce— firm decision

for whom to produce— aka income, quantity and market value of resources owned. dollar votes.

economics interactions

gains of trade

market move through equilbrium

resources used up efficiently

markets lead to equilibrium

government involvement

Trade

done when marginal benefits for both parties is greater than their marginal costs. This happens b/c of specilizations.

markets move toward equilbirum

equilibrium is state where there’s no change. markets stop moving when they can’t be better off than they already are.

resources

using resources as efficiently and every opportunity to better oneself. Operating efficiently means someone has to to be worse off.

equity

hard to measure. To have equity, we sacifice efficiency

as long as gains exist,

people will exploite them/

governments involvement to make markets competeitive

welfare of society

level of consumption and good people enjoy

standard of living

cost of living

dollar amount of goods and services for a standard of living

economics flutations

rise of fall of production in the economy. the business cycle.

recession and expansion + unemployment and inflation

another person’s spending is another person’s income

a person spending on a good causes income of the reproducing the good increases

trade off

comparison of costs and benefits.

Positive economics

objective statements that can be proven right or wrong

normative economics

determining desirabilities of outcome based on valued judgement. Ex: should taxes be lowered to raise consumer spending to get out of a resession?

slope of ppc

= the oppertunity cost of horizontial axes.

rise/ run = a/b = opportunity cost of b

allocative economy

prioritize goods that consumers want in correct quanity. market capital economy may not achieve this.

differing abilities in producing various goods & services in that country.

specialization

Types of resources

Land is the bounty of the Earth: includes natural resources such as oil, coal, minerals, etc.

Labor includes both physical and mental human effort

Capital are the tools, equipment, and factories

Human capital is the educational achievements and skills of the labor force (which increase labor productivity).

Entreprenurship is the ability to organize resources & take risks to develop new ways of production and new products.

Technology

knowledge of how to poduce goods and services

When resources are specialized..

the opportunity cost becomes bigger.

why is a country ppc curved?

Because of the oppertunity cost is bigger due to specialization

a ppc curve going outward right?

means increases in resources and tech improved standard of living, The position is depedent on the country’s resources and tech

If technology only improves for one good (a new fishing technique increases the catch with same amount of ships) then the PPF will shift out from that axis only.

this does not mean we can only produce more of that good. it frees up more resources to put into other goods

Comparative advantage

refers to an ability to produce a good or service at a lower opportunity cost than another

Absolute Advantage

is the ability to produce more than another, given the same resources.

law of increasing opportunity cost

resources are not equally suited for all types of production

Markets

Are a mechanism that brings buyers and sellers together to exchange goods, services, and resources. It is a device for allocating and rationizing goods

two types of markets

Product market: where consumer goods are bought and sold. Business firms are the seller, consumers are the buyers

Resource market: where the resource services are bought and sold. Resource owners(consumers) are the sellers and business firms are the buyers

demand

relationship between the price and the quantity demanded of a good

quanity demanded

amount of an item that buyers are willing and able to purchase over a certain time period, at a specific price, ceteris paribus.

normal good

Buy more of a good when income increases

Inferior good

Buy less of that good when income increases

Subsitute

Two goods that perform the same function (interchangeable)

complements

Two goods that perform the same function (interchangeable)

Law of demand

price and quanity demanded of a good are inversely related

demand schedule

A list of possible prices with the corresponding quantity demanded at that price

demand curve

As the price of a good decreases, buyers are willing and able

to purchase more of this good, all other variables constant

relative price

price of the one you want/ other good= relative price of what you want

$4 for unit of blackberry/ 2$ for unit of strawberry= 2 strawberry for blackberry

what causes demand to change

taste and preference, expectation, price, market consumers availablity

profit equation

Profit = Revenue – Cost = (Price x Quantity) - Cost

what influences supply

1. Price of the good

2. Price of inputs (resources)

3. Technology

4. Prices of other goods that can be produced by the firm (for multi-good firms)

5. Expectations of future price

6. Number of Firms

7. Taxes and Subsidies on the good

law of supply

The price and quantity supplied of a good are directly related

supply schedule

A list of possible prices with the corresponding quantity supplied at that price

Equilibrium

At rest, no tendency to change, forces in balance.

Market equilbrium

−the price, once reached, when there will be no tendency to change.

Also the price the market comes to rest at and where there are forces in balance.

There are no more unexploited opportunities

quanity demanded = quanity supplied

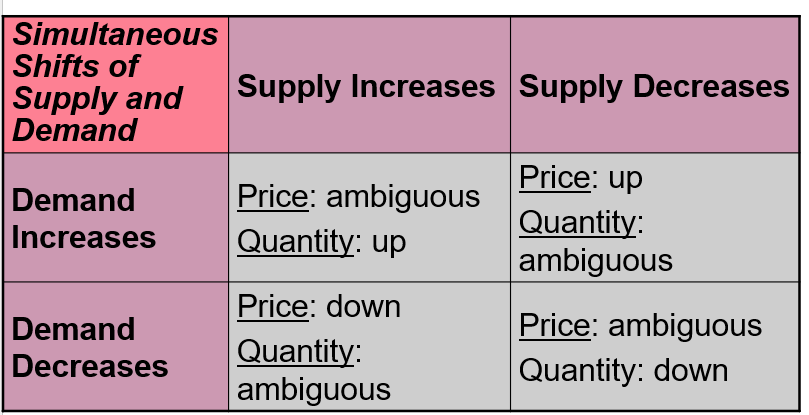

demand supply expectations