Economics Exam 1

5.0(1)

5.0(1)

Card Sorting

1/54

Earn XP

Description and Tags

Study Analytics

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

55 Terms

1

New cards

Marginal

means “extra” or “additional”

2

New cards

Marginal Analysis

* The comparison of marginal benefits and marginal costs, usually for decision making

* Basically weighing the pros and cons

* For example: Should you buy a 1/2 carat diamond of a 1-carat diamond?

* The marginal cost of the larger diamond is the added expense beyond the cost of the smaller diamond.

* The marginal benefit is the perceived lifetime pleasure (utility) from the larger stone.

* If the marginal benefit of the larger diamond exceeds its marginal cost (and you can afford it), buy the larger stone.

* But if the marginal cost is more than the marginal benefit, you should buy the smaller diamond instead- even if you can afford the larger stone.

* Basically weighing the pros and cons

* For example: Should you buy a 1/2 carat diamond of a 1-carat diamond?

* The marginal cost of the larger diamond is the added expense beyond the cost of the smaller diamond.

* The marginal benefit is the perceived lifetime pleasure (utility) from the larger stone.

* If the marginal benefit of the larger diamond exceeds its marginal cost (and you can afford it), buy the larger stone.

* But if the marginal cost is more than the marginal benefit, you should buy the smaller diamond instead- even if you can afford the larger stone.

3

New cards

Marginal Cost

* The extra (additional) cost of producing 1 more unit of output

* Equal to the change in *total cost* divided by the change in output

* Impacts the producer

* It is always downward sloping

* Equal to the change in *total cost* divided by the change in output

* Impacts the producer

* It is always downward sloping

4

New cards

Marginal Benefit

* A maximum amount a consumer is willing to pay for an additional good or service.

* It is also the additional satisfaction or utility that a consumer receives when the additional good or service is purchased.

* Tends to decrease as consumption of the good or service increases

* It is also the additional satisfaction or utility that a consumer receives when the additional good or service is purchased.

* Tends to decrease as consumption of the good or service increases

5

New cards

When should you consume more?

When its marginal benefit exceeds its marginal cost

6

New cards

When should you consume less?

When the marginal cost exceeds the marginal benefit

7

New cards

When should you not consume?

When the marginal benefit and the marginal cost are equal to one another.

8

New cards

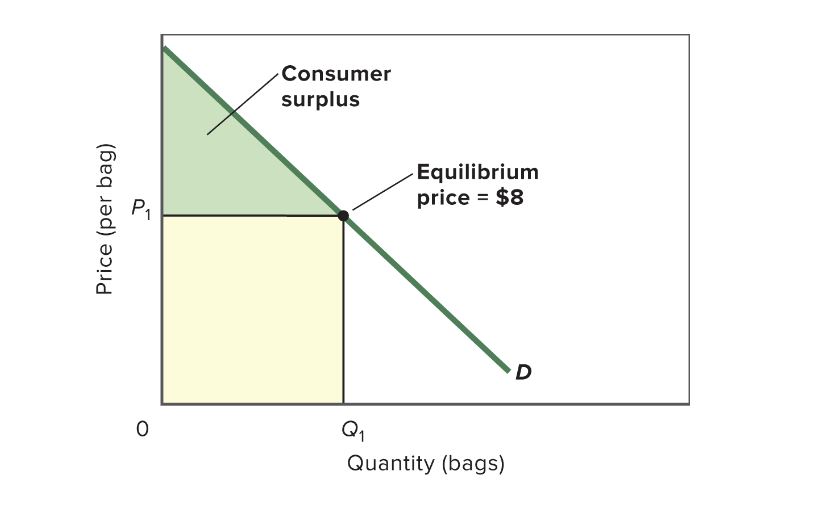

Consumer Surplus

* The difference between the maximum price a consumer is (or consumers are) willing to pay for an additional unit of a product and its market price

* The share of the total surplus that is received by a consumer or consumers in a market is called this

* On a graph: Triangular area __below__ the demand curve and __above__ the market price

* Calculate the area of a triangle: 1/2bh

* The share of the total surplus that is received by a consumer or consumers in a market is called this

* On a graph: Triangular area __below__ the demand curve and __above__ the market price

* Calculate the area of a triangle: 1/2bh

9

New cards

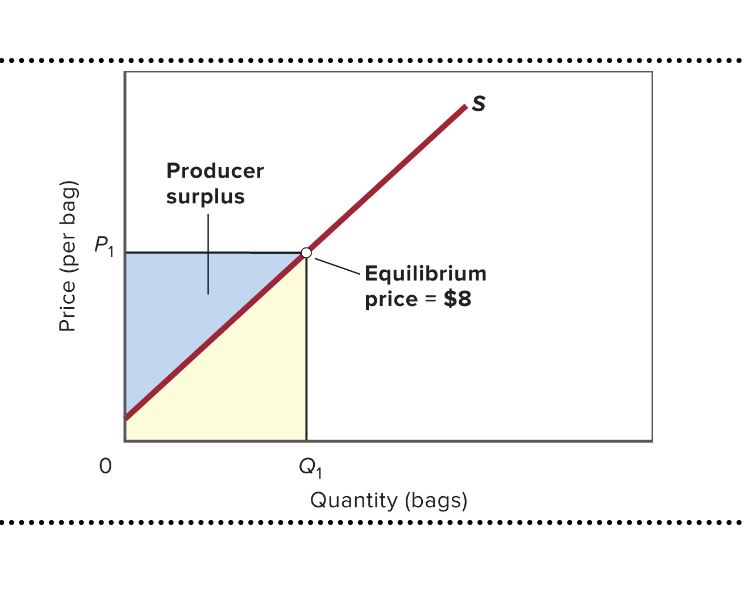

Producer Surplus

* The difference between the actual __price__ a producer receives (or producers receive) and the minimum price that a consumer would have to pay the producer to make a particular unit of output available.

* On a graph: the triangular area __above__ supply curve and __below__ the market price

* On a graph: the triangular area __above__ supply curve and __below__ the market price

10

New cards

How do you calculate consumer/producer surplus and find your utility (happiness)?

Consumer and producer surpluses are calculated as the areas of the triangle below and above and below and above.

11

New cards

What is the economizing problem all economies/people face?

* Individuals: The need to make choices because economic wants exceed economic means

* They must decide what to buy and what to forgo

* Society: Society has limited or scarce economic resources, meaning all natural, human, and manufactured resources that go into the production of goods and services.

* They must decide what to buy and what to forgo

* Society: Society has limited or scarce economic resources, meaning all natural, human, and manufactured resources that go into the production of goods and services.

12

New cards

When an economist states you are acting rationally what does that mean?

* Simply means that when you make a choice, you will choose the thing you like best.

* As long as you’re doing what you want given your situation, you’re acting rationally

* As long as you’re doing what you want given your situation, you’re acting rationally

13

New cards

What is the invisible hand?

The tendency of competition to cause individuals and firms to unintentionally but quite effectively promote the interests of society even when each individual or firm is only attempting to pursue its own interests.

14

New cards

What does the word “utility” mean in economics?

* The want-satisfying power of a *good* or *service*; the satisfaction or pleasure a consumer obtains from the consumption of a good or service (or from the consumption of a collection of *goods* and *services*).

* Happiness

* Happiness

15

New cards

Opportunity Cost & Use in a Sentence

* To obtain more of one thing, society sacrifices the opportunity of getting the next best thing that could have been created with those resources

* Sentence: If we got free donuts, it would not be free since we are sacrificing our time.

* Sentence: If we got free donuts, it would not be free since we are sacrificing our time.

16

New cards

Characteristics of a Market System?

* An economic system in which individuals own most economic resources and in which markets and prices serve as the dominant coordinating mechanism used to allocate those resources; capitalism.

* Also known as a mixed economy

* Characterized by the private ownership of resources, including capital, and the freedom of individuals to engage in economic activities of their choice to advance their well-being.

* Self-interest is the driving force

* Specialization, the use of advanced technology, and the extensive use of capital goods are common features.

* Also known as a mixed economy

* Characterized by the private ownership of resources, including capital, and the freedom of individuals to engage in economic activities of their choice to advance their well-being.

* Self-interest is the driving force

* Specialization, the use of advanced technology, and the extensive use of capital goods are common features.

17

New cards

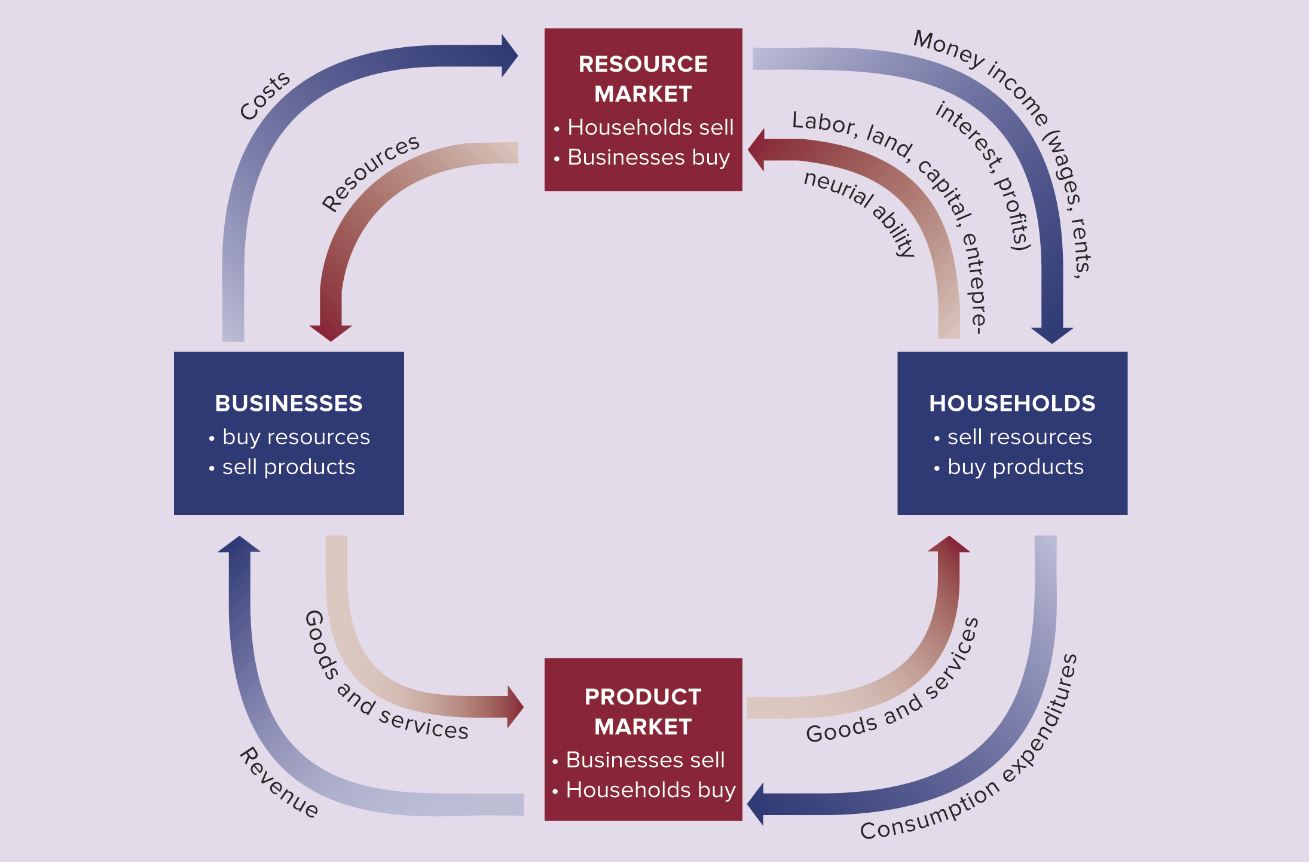

Circle Flow Model

Illustrates the flows of resources and products from households to businesses and from businesses to households, along with the corresponding monetary flows.

18

New cards

What is an Economic System (define it)?

* A particular set of institutional arrangements and a coordinating mechanism for solving the __*economizing problem*__

* A method of organizing an economy of which the __*market system*__ and the __*command system*__ are the two general types.

* A method of organizing an economy of which the __*market system*__ and the __*command system*__ are the two general types.

19

New cards

How do economic systems differ?

Economic systems differ as to (1) who owns the factors of production (2) the method used to motivate, coordinate, and direct economic activity.

20

New cards

What is the primary driver that regulates the market system?

Prices drive the market system

21

New cards

What are the 5 fundamental questions?

* What are we going to make

* In a market economy - dollar votes will produce what we make

* How are we going to make it?

* That is up to the business, going to try and make it as cheap as possible in order to increase their profit margin

* Who is going to make them?

* How will the system consider changes?

* In a market economy - dollar votes will produce what we make

* How are we going to make it?

* That is up to the business, going to try and make it as cheap as possible in order to increase their profit margin

* Who is going to make them?

* How will the system consider changes?

22

New cards

Why is the market economy considered efficient?

* Not equitable

* Because we are trying to maximize our individual utility or individual firm utility.

* Invisible hand

* Competing for your money

* Maximizing their firm utility

* We as individuals are trying to maximize our own utility

* Because we are trying to maximize our individual utility or individual firm utility.

* Invisible hand

* Competing for your money

* Maximizing their firm utility

* We as individuals are trying to maximize our own utility

23

New cards

What was the main problem with the Barter system and how has money fixed it

* Coincidence of wants

* You need to have the good that the person you are buying from wants.

* You need to have the good that the person you are buying from wants.

24

New cards

Under a market system, what does freedom enterprise mean?

* It means you have the freedom to start any business you want, even if its dumb as hell

* Free will

* Free will

25

New cards

What do we mean when we say your “dollar votes”?

* The “votes” that consumers cast for the production of preferred products when they purchase those products rather than the alternatives that were also available

26

New cards

What is a market?

Any institution or mechanism that brings together buyers (demanders) and sellers (suppliers) of a particular *good* or *service*

27

New cards

What is the law of demand?What is the relationship it has with price and quantity?

* The principle that, other things equal, an increase in a product’s *price* will reduce the *quantity* of it demanded, and conversely for a decrease in price

* Inverse Relationship

* As price goes up, my quantity demanded goes down

* Inverse Relationship

* As price goes up, my quantity demanded goes down

28

New cards

What is the law of supply? What is the relationship it has with price and quantity?

* The principle that, other things equal, an increase in the *price* of a product will increase the *quantity* of it supplied, and conversely for a price decrease,

* Direct relationship

* Direct relationship

29

New cards

Complementary Goods

Products and *services* that are used together. When the *price* of one falls, the demand for the other increases (and conversely).

30

New cards

Substitute Goods

Products or *services* that can be used in place of each other. When the *price* of one falls, the *demand* for the other product falls; conversely, when the price of one product rises, the demand for the other product rises.

31

New cards

Price Floor

A legally established minimum *price* for a *good*, or service. Normally set at a price above the *equilibrium price.*

* Know market equilibrium on graph and price floor and ceiling

* Know market equilibrium on graph and price floor and ceiling

32

New cards

Price Ceiling

A legally established maximum *price* for a *good*, or *service*. Normally, set at a price below the *equilibrium price.*

33

New cards

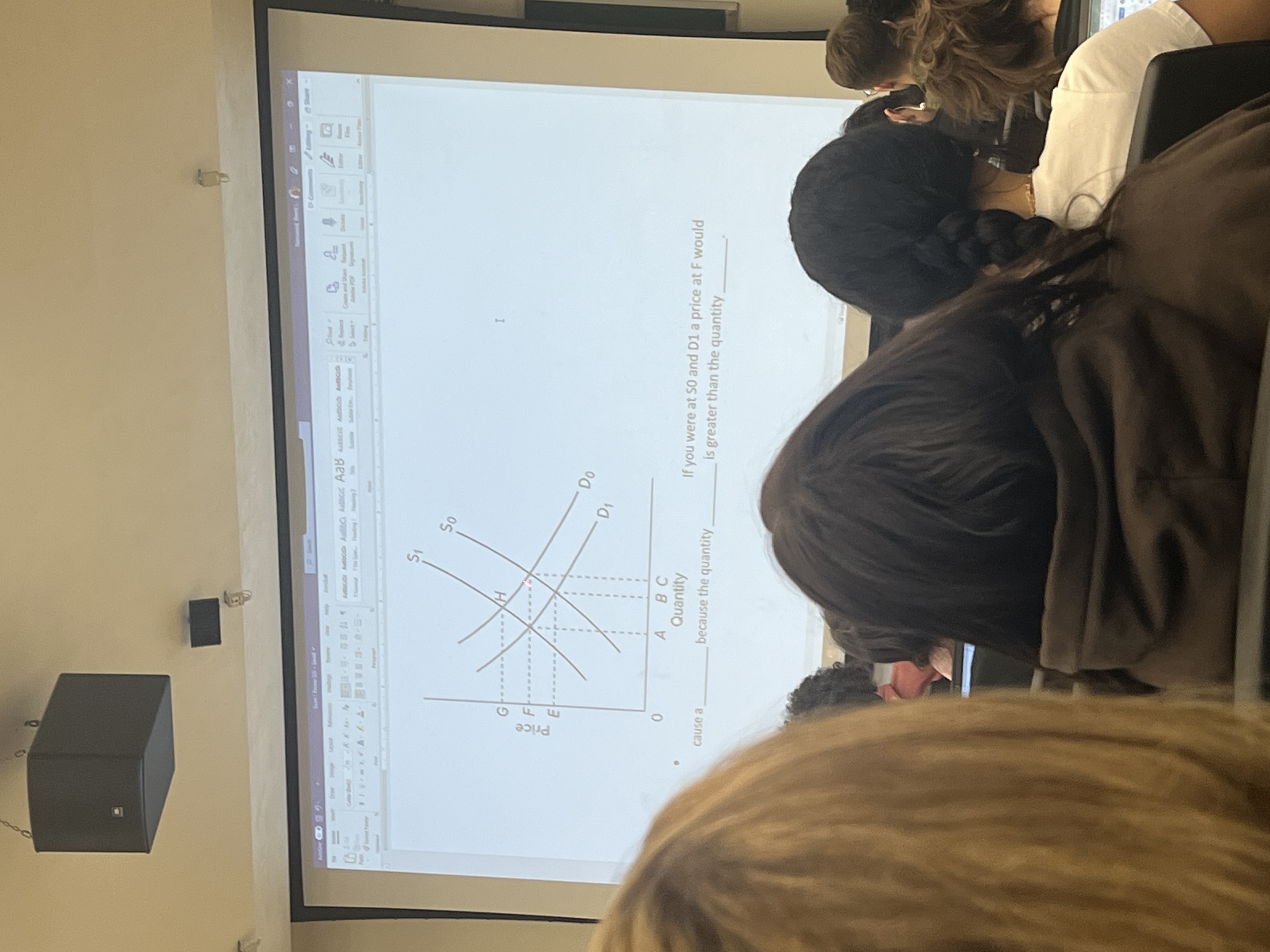

If supply increases and demand stays the same what happens to equilibrium price and quantity?

Equilibrium quantity goes up, and equilibrium price goes down.

34

New cards

If demand increases and supply stays the same what happens to equilibrium price and quantity

Equilibrium quantity goes up, and equilibrium price goes up

35

New cards

If demand increases and supply increases what happens to equilibrium price and quantity

Equilibrium quantity goes up, equilibrium price could go up, down or stay the same.

36

New cards

Normal Good

A *good* or *service* whose consumption increases when *income* increases and falls when income decreases, *price* remaining constant.

* When income goes up, demand goes up for a normal good

* When income goes up, demand goes up for a normal good

37

New cards

Inferior Good

A *good* or *service* whose consumption declines as income rises, *prices* held constant

* For an inferior good - income goes down, demand goes up

* For an inferior good - income goes down, demand goes up

38

New cards

Income Effects

A change in the quantity demanded of a product that results from the change in *real income* (purchasing power) caused by a change in the product’s *price*

* As your income goes OR purchasing power goes up (down) your demand goes up (down)

* As your income goes OR purchasing power goes up (down) your demand goes up (down)

39

New cards

Substitution Effects

* A change in the quantity demanded of a consumer good that results from a change in its relative expensiveness caused by a change in the good’s own price.

* The reduction in the quantity demanded of the second of a pair of substitute resources that occurs when the price of the first resource falls and causes firms that employ both resources to switch to using more of the first resource (whose price has fallen) and less of the second resource (whose price has remained the same)

* The reduction in the quantity demanded of the second of a pair of substitute resources that occurs when the price of the first resource falls and causes firms that employ both resources to switch to using more of the first resource (whose price has fallen) and less of the second resource (whose price has remained the same)

40

New cards

What is market failure?

The inability of a market to bring about the allocation of resources best satisfies the wants of society; in particular, the overallocation or under allocation of resources to the production of a particular good or service because of externalities or asymmetric information, or because markets fail to provide desired public goods

41

New cards

When does market failure occur?

* Occurs when/Causes:

* Externality

* Public goods (if a selection of the population that consumes the goods fails to pay but continues using the good as actual payers)

* Market control (when the buyer or seller possesses the power to determine the price of goods or services in a market)

* Imperfect information in the market (lack of appropriate information among buyers and sellers)

* Externality

* Public goods (if a selection of the population that consumes the goods fails to pay but continues using the good as actual payers)

* Market control (when the buyer or seller possesses the power to determine the price of goods or services in a market)

* Imperfect information in the market (lack of appropriate information among buyers and sellers)

42

New cards

Positive Externalities

A benefit obtained without compensation by third parties from the production or consumption of sellers or buyers.

Ex. A beekeeper benefits when a neighboring farmer plants cover. Also known as an external benefit or a spillover benefit

Ex. A beekeeper benefits when a neighboring farmer plants cover. Also known as an external benefit or a spillover benefit

43

New cards

Negative Externalities

A cost imposed without compensation on third parties by the production or consumption of sellers or buyers.

Ex. A manufacturer dumps toxic chemicals into a river, killing fish prized by sports fishers. Also known as an external cost or spillover cost.

Ex. A manufacturer dumps toxic chemicals into a river, killing fish prized by sports fishers. Also known as an external cost or spillover cost.

44

New cards

How to correct externalities that cause market failures?

* You can tax it or subsidize it to shift the demand or supply curve

* positive externalities - subsidize it

* negative externalities - tax it

* positive externalities - subsidize it

* negative externalities - tax it

45

New cards

Under Allocation of Resources

Marginal cost < Marginal benefit produce/consume more

46

New cards

Over Allocation of Resources

Marginal cost > Marginal benefit produce/consume less

47

New cards

Positive externalities are generally _____produced and negative externalities are generally ______ produced

* Under/Over

* Positive externality examples - public schools

* Negative externality examples - pollution

* Positive externality examples - public schools

* Negative externality examples - pollution

48

New cards

Public goods

A good or service that is characterized by nonrivalry and non-excludability.

* These characteristics typically imply that no private firm can break even when attempting to provide such products. As a result, they are often provided by governments, who pay for them using general tax revenues

* These characteristics typically imply that no private firm can break even when attempting to provide such products. As a result, they are often provided by governments, who pay for them using general tax revenues

49

New cards

Private good

A good or service that is individually consumed and that can be profitably provided by privately owned firms because they can exclude nonpayers from receiving the benefits

50

New cards

Principal-agent problem

When there is adverse selection for a good or service. People that buy insurance are the ones that need it, so they drive worse.

51

New cards

Special Interest Effect

Any political outcome in which a small group (“special interest”) gains substantially at the expense of a much larger number of persons who each individually suffers a small loss

* When you lobby to your own special interests

* When you lobby to your own special interests

52

New cards

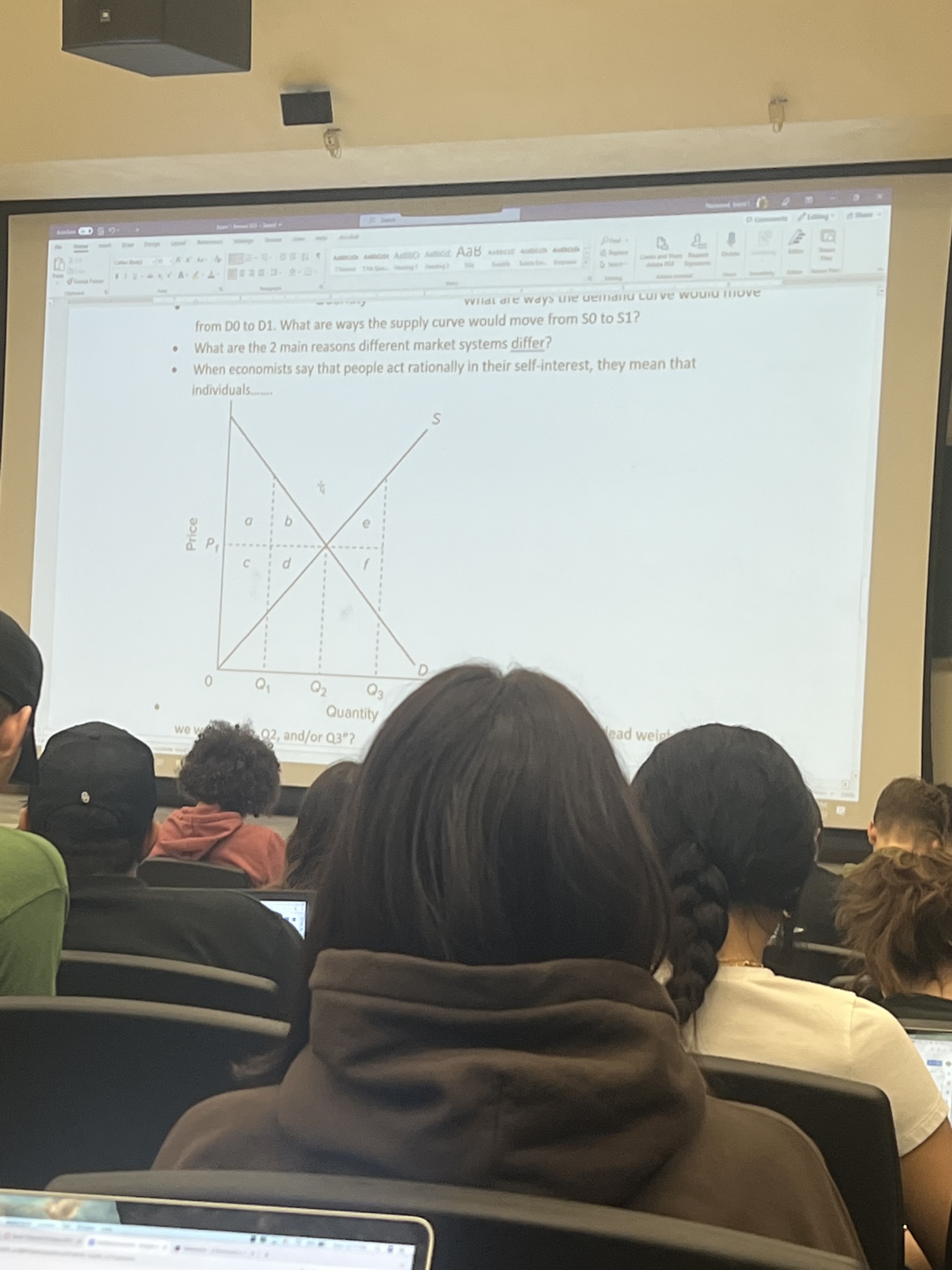

Graph 1

* S0 is original, S1 is shifted

* moving from 0 to 1, is a decrease because it shifted left, input cost go up from s0 to s1 or taxes went up

* two main reasons market systems differ: government involvement and who gets to consume it

* moving from 0 to 1, is a decrease because it shifted left, input cost go up from s0 to s1 or taxes went up

* two main reasons market systems differ: government involvement and who gets to consume it

53

New cards

Graph 2

dead weight: B and D (lost economic activity) Q3 deadweight loss E & F because of overproduction

* Benefit/Cost

* Benefit/Cost

54

New cards

Graph 3

* surplus

* supply/demand

* supply/demand

55

New cards

An increase in demand may be caused by

* A favorable change in consumer tastes

* An increase in the number of buyers

* Rising income if the product is a normal good

* Falling income if the product is an inferior good

* An increase in the price of a substitute good

* A decrease in the price of complementary good

* A new consumer expectation that either prices or income will be higher in the future

* An increase in the number of buyers

* Rising income if the product is a normal good

* Falling income if the product is an inferior good

* An increase in the price of a substitute good

* A decrease in the price of complementary good

* A new consumer expectation that either prices or income will be higher in the future