ch.10 - budgeting

1/32

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

33 Terms

types of budgets

Long range planning

Set long term goals

Strategies to achieve those goals

Plans to implement the strategies

Strategic budget

Goals used to develop a long range plan

Anticipate market trends

Master budget

AKA pro forma financial statement

Set up budgets that summarizes the goals of all of the subunits in the company

Consists of two classes

Operating

smaller Budgets used to prepare the budgeted income statement

need rev. and cash collections to make

Financial

capital expenditure budget

Cash budget

Budgeted balance sheet

Continuous or rolling budget

Updating the budget every month

pros of budgets

Requires all levels of management to plan ahead and form goals on a continuous basis

There are objectives to evaluate performance at each level of responsibility

Creates a warning system for potential problems

Communication and coordination is easier within the organization because you all have similar goals

Management has greater awareness of overall operations and the impact of the external environment

Motivates personnel

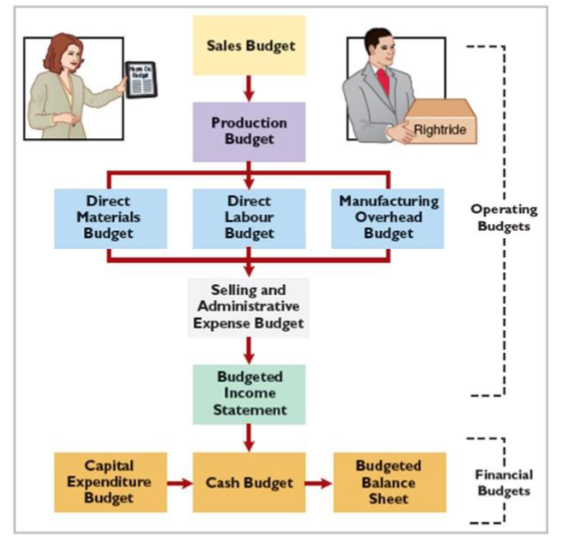

master budget components

Sales budget

Other budgets stem from this one

Production budget

You should know how much you are able to sell before you decide on how much to produce

DM purchases budget

DL budget

MOH budget

Ending FG inventory budget

Selling and administrative budget

Cash budget

Wages and salaries to personnel

Budgeted i/s

Budgeted balance sheet

sales forecasting

Aka the cornerstone of all budgeting

Cuz every budget is based on what is forecasted

Usually determined by marketing

Find the sales for that industry and then what the company's share of those sales would be

A prediction of sales(A forecast) under a set of conditions

Realistic

Optimistic

Pessimistic

As you get closer to the time period, you pick a forecast and implement it for the sales budget

sales forecasting error

Q:

Suppose actual total revenue $480,000, not the $405,000 shown in this budget.

Suppose also that prices were stable. Costs would differ significantly from budgeted amounts in which of these budgets: direct materials budget, overhead budget, selling and administrative expense budget.?

A: In the situation where the actual revenue is higher than the budgeted revenue significantly, that means that the wrong sales forecast was used which affects every budget.

In this case, the price is the same but revenue has gone up which means that sales units has increased which will make for higher variable costs for the period

Factors to consider when sales forecasting

Economic conditions

Boom or bust

Past performance

Industry trends

Do market research

Plans for advertising and promotions

Will the budget for this increase or decrease?

What was our previous market share

The effect of changes in prices

Technological developments

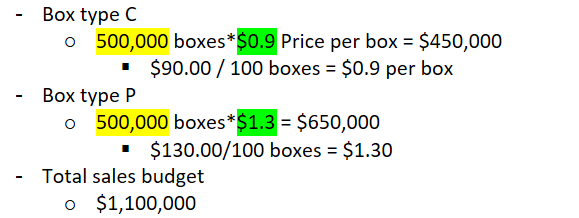

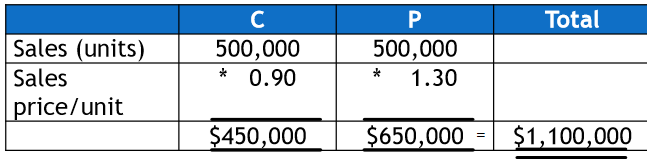

sales budget

For each product:

expected Sales Volume* expected sales price per unit

budgeted rev used in I/S and cash budget

budgeted unit sales used in production budget

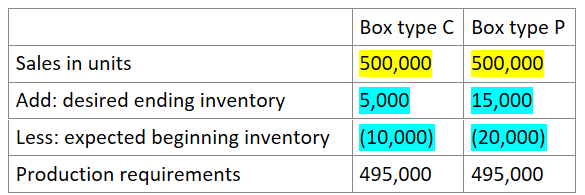

production budget

Want to find out the total units that need to be produced

Total units to be produced = total units to be sold

Inventories have to do with finished goods

leads to DM budget, DL budget, and MOH budget

Budget:

expected Sales in units

Add: desired ending inventory

(Less: expected beginning inventory)

= Production requirements

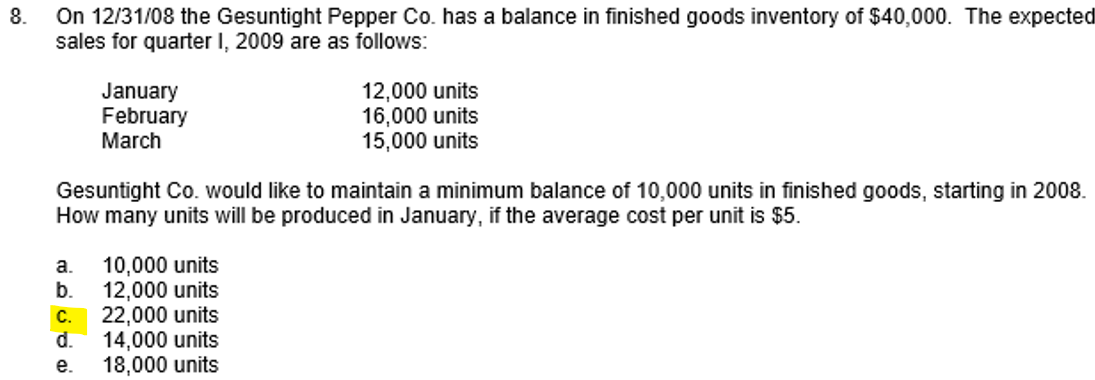

production requirements ex.

expected beginning inventory

ending balance of the period before/avg cost per unit

40,000 units/$5 = 8,000 units

For Jan.:

expected sales in units + desired ending inv. - expected beginning inv.

desired ending inv. = “maintain a minimum balance of … in fg”

12,000+10,000-8,000 = 14,000

dm budget

DM that needs to be purchased in the period = DM required for production

However purchased will be in dollars, requirements for production will be in units

Budget:

Production requirements

Comes from the production budget

* DM required per unit

= DM required for production

This will give you units

Add: desired ending inventory

(Less: expected beginning inventory)

= DM to be purchased

DM to be purchased (in units)* price per unit

This will give you dollars

DL budget

Budget:

Production requirements

Comes from the production budget

* DL required per unit

= DL required for production

This will give you units

* DL rate per hour

= DL budget

This will give you dollars

mfg cost per unit budgeting

from DM and DL budget

Budget:

DM cost per unit

+ DL cost per unit

+MOH

Using the predetermined MOH rate

from the DL hours required for production or DM required for production

hours or units for ex.

also use from the DL required per unit or DM required per unit

hours or units for ex.

= Manufacturing cost per unit

ending FG budget

Desired ending inventory* manufacturing cost per unit

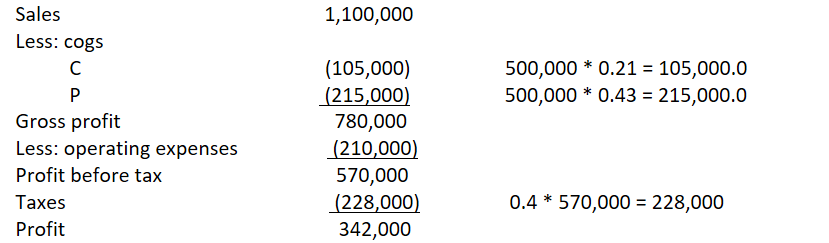

budgeted i/s

Sales

Total $ from sales budget

Less: (COGS)

For each product : sales in units * manufacturing cost per unit

= Gross profit

Less: operating expenses

Like selling and admin

= Profit before tax

Taxes

Tax rate* profit before tax

= Profit

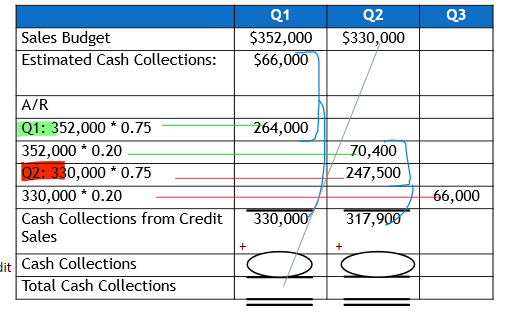

cash collections

| Q1 | Q2 | Q3 |

Sales budget |

|

|

|

Estimated cash collections | From the last quarter of the previous year |

|

|

Accounts receivable Q1 Q2 | Usually given a percentage that will be collected in this quarter | 1-Q1% |

|

Cash collections from credit sales |

|

|

|

Cash collections |

|

|

|

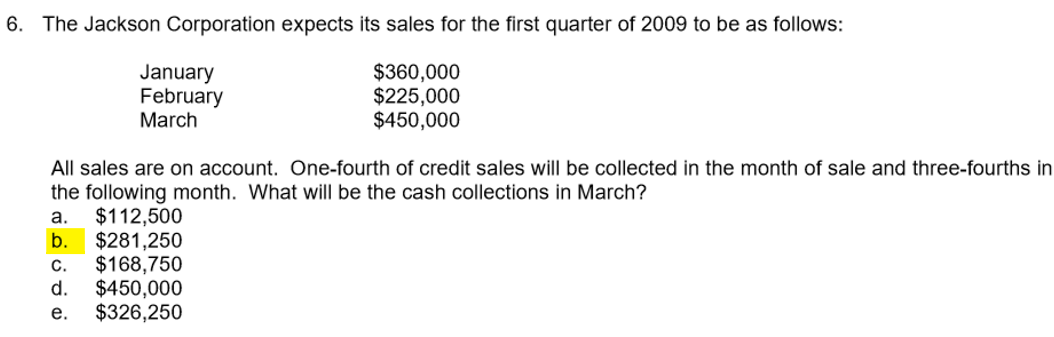

cash collection ex.

the amount that is expensed in feb. but will be collected in march

225,000*(3/4) = 168,750

the amount that is expensed and collected march

450,000*(1/4) = 112,500

total collection for march

168,750+112,500 = 281,250

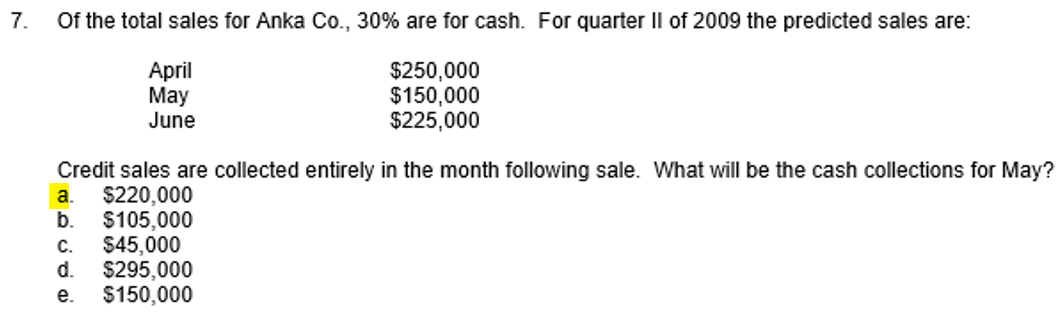

cash collections ex. a % is cash sales and credit sales are collected the next month

physical cash collection for may:

150,000*30% = 45,000

credit sales collected in may = credit sales from april

250,000*(1-30%) = 175,000

total collection for may

45,000+175,000 = 220,000

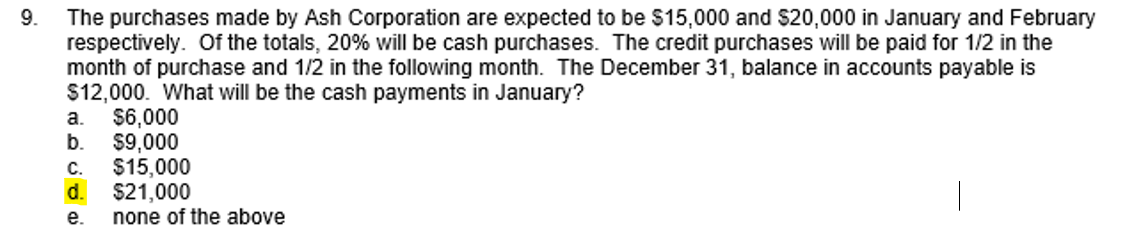

ex. cash collection when there is a previous balance

jan. a/p balance from previous period

$12,000

jan. cash purchase payment

15,000*20% = 3,000

jan. credit purchase payment

credit amount of purchase

15,000-3,000 = 12,000

how much of the credit amount paid in jan.

12,000*(1/2) = 6,000

total jan payment

make sure to include a/p balance from previous period

12,000+3,000+6,000 = 21,000

budgeting admin

Levels:

Budget officer

aka chief budget officer

Specifies how the budget will be compiled

Budget manual

Specifies details on budget information

Who is responsible

When is it required

The form of the information

Budget committee

Appointed committee that advises the budget director

The amount of levels you have depends on the size of the company

Can have none

Multinational companies would need all three

budgeting ethics

Managers are usually rewarded for staying under the budget

but when costs are defined as cash payments for DM, DL, MOH

Managers will increase their payables which would decrease cash payments for the current period

There are ways to manipulate the accounting to reflect being under the budget

business ethics ex.

Q: manager does not participate in the budgeting process. The manager will be paid a bonus equal to ten percent of actual sales revenue in 2008. If the manager responds unethically to the bonus plan, what problem(s) for Healthworks, Inc could arise?

A: If the bonus is connected to the revenue then the likely course the manager will take is being neglectful in terms of costs which is bad for the company

participative budget

Managers and employees are integrated into the budgeting process

Pros

Managers have information and expertise that upper management might not have

Good for morale

Managers are less motivated if they're being told what to do rather than if they are sticking to a plan that they were a part of making

cons

can add too much padding so that easier to meet goals

more time consuming and costly

padding the budget

Setting budgetary goals that are easy to attain

Easily attained goals - realistic goals = budgetary slack

Used to deal with uncertainties

only if there is participative budgeting

ex. of the effects of padding the budget

Q:

sales price of these devices has been very stable over the last three years.If this manager padded his or her budget, what row of numbers in the budget would likely be affected most directly? Are these numbers likely to be above or below the manager's expectations?

A: The most affected row is the sales in units because a padded budget Lowers expectations which would mean less production

zero based budgeting

Developing a budget for each activity as if the company is in its first year of operations

So amounts from the previous period are not carried forward

This happens every few periods

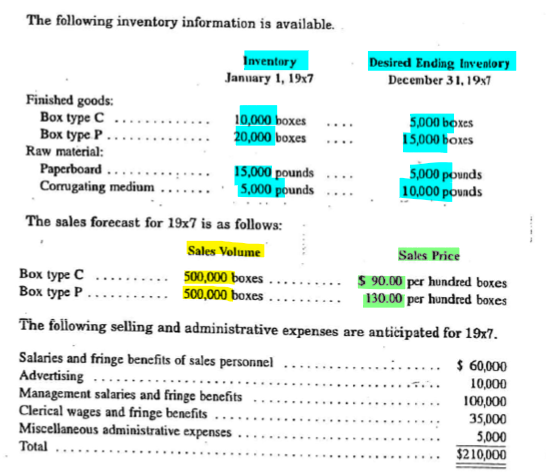

a big ex.

big ex. sales budget

big ex. production budget

|

big ex. dm budget

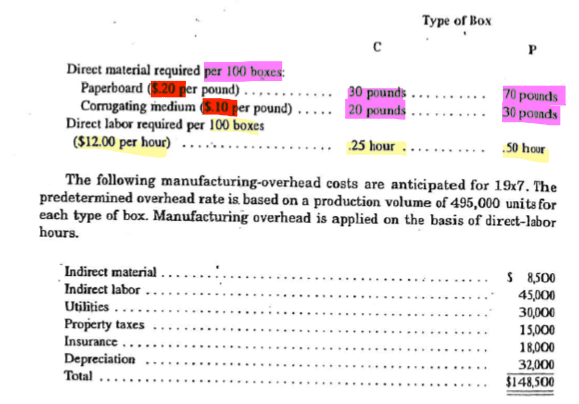

For paper boards

DM required per box

C

70 LBS per 100 boxes = 70 / 100 = 0.7

P

30 LBS per 100 boxes = 30 / 100 = 0.3

| Box type C | Box type P | Total |

Production requirements | 495,000 | 495,000 |

|

DM required per box | *0.3 | * 0.7 |

|

DM required for production | 148,500 lbs | 346,500 lbs | 495,000 lbs |

Add: desired ending inventory |

|

| 5000 |

Less: expected beginning inventory |

|

| (15,000) |

DM to be purchased |

|

| 485,000 * $0.20 = 97,000 |

For corrugating medium

DM required per box

C

20 LBS per 100 boxes = 20 / 100 = 0.2

P

30 LBS per 100 boxes = 30 / 100 = 0.3

| Box type C | Box type P | Total |

Production requirements | 495,000 | 495,000 |

|

DM required per box | * 0.2 | * 0.3 |

|

DM required for production | 495,000 * 0.2 = 99,000 | 495,000 * 0.3 = 148,500.0 | 99,000 + 148,500 = 247,500 |

Add: desired ending inventory |

|

| 10,000 |

Less: expected beginning inventory |

|

| (5000) |

DM to be purchased |

|

| 247,500 + 10,000-5000 = 252500 then 252,500 * 0.1 = 25,250 |

big ex. DL budget

| Box type C | Box type P | Total |

Production requirements | 495,000 | 495,000 |

|

DL required per box | 0.25 / 100 = 0.0025 | 0.5 / 100 = 0.005 |

|

DL hours required for production | 495,000 * 0.0025 = 1,237.5 | 495,000 * 0.005 = 2,475.0 | 1237.5 + 2475 = 3712.5 |

DL rate per hour |

|

| 12 |

DL budget amount |

|

| 3712.5 * 12 = $44550 |

big ex. mfg cost / unit budget

|

| Box type C | Box type P |

DM cost per unit: Paperboards |

| 0.3 * 0.2 = 0.06 0.3 box | 0.7*0.2 = 0.14 0.7 box |

corrugating medium |

| 0.2*0.1 = 0.02 0.2 box | 0.3*0.1 = 0.03 0.3 box |

DL cost per unit |

| 0.0025*12 = 0.03 0.0025 box | 0.005*12 = 0.06 0.005 box |

Pred. MOH rate | 148,500/3712.5 = 40 |

|

|

MOH |

| 0.0025*40 = 0.1 | 0.005*40 = 0.2 |

mfg cost/unit |

| 0.06 + 0.02 + 0.03 + 0.1 = 0.21 | 0.14 + 0.03 + 0.06 + 0.2 = 0.43 |

big ex. ending fg. inv.

C

5000 *0.21 = 1050

P

15,000 * 0.43 = 6,450.0

big ex. budgeted i/s