ECON 2020 EXAM 3

1/9

Earn XP

Description and Tags

Study guide

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

10 Terms

What is a Monopoly?

A monopoly is a market that produces a good or service for which NO close substitutes exists in which there is ONE supplier that is protected from competition by a barrier preventing the entry of new firms.

If a good has a close substitute, then

the firm effectively faces competition form the PRODUCERS of the SUBSTITUTE.

A constraint that protects a firm from potential competitor’s is called ________. What are the three different types?

barrier to entry; natural, ownership, legal

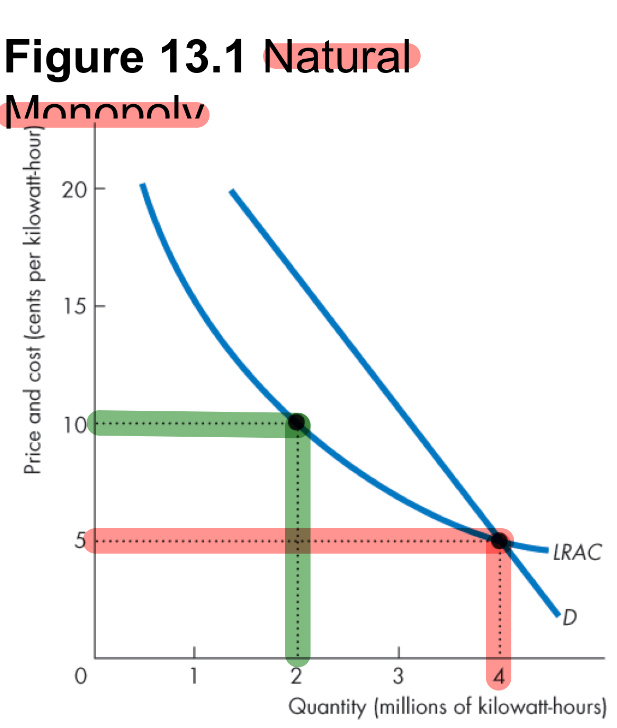

What is a natural monopoly?

is a market in which economics of scale enable one firm to supply the entire market at the lowest possible cost.

A LARGER production scale …

LOWERS average cost and is therefore inefficient to spread production over multiple firms. (may occur when there is a LARGER fix cost compared to marginal cost like in power production).

When does ownership barrier to entry occur?

If ONE firm owns a significant portion of a key resource.

Legal barriers to entry creates a __________.

Legal monopoly

What is a legal monopoly?

Is a market in which COMPETITION and ENTRY is restricted by the granting of a public franchise (like U.S. postal service), a government license, or a patent/ copyright.

For a monopoly firm to determine the quantity it sells, it must choose the appropriate price. What are the TWO types of monopoly price-setting strategies?

a single-price monopoly is a firm that must sell each unit of its output for the same price to all its customers.

price discrimination is the practice of selling different units of a good or service for different prices. (many firms price discriminate, but not all are monopolies)

what is total revenue?; what is marginal revenue?

(TR) is the price (P) multiplied by the quantity sold (Q).

Marginal revenue (MR) is the change in total revenue that results form a one-point