Economics C.2 - The Economics Concepts of Scarcity and Choice B

1/33

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

34 Terms

What is economics?

the study of how finite resources are allocated to satisfy wants and needs

What is scarcity?

the fundamental economic problem of having seemingly unlimited human wants and needs in a world of limited resources

What does the term ‘scarce resource’ refer to?

the limited supply of factors of production and the unlimited demand for them

What is the opportunity cost?

the best alternative forgone when a choice is made

Who do choices that involve an opportunity cost apply to?

governments, firms, and individuals alike

What is an incentive?

something that motivates an individual or firm to behave in a certain way

What is a regulation?

a law, rule or order that must be followed. A violation of the regulation results in a punishment

Why do governments prefer to use incentives to influence consumer and producer behaviour?

enforcing punishments for breaches of regulations results in a drain on scarce resources

What is the separation of labour/division of labour?

the separation of a work process into a number of tasks, with each task carried out by a separate worker or group of workers

Which economist is associated with the concept of specialisation of labour?

Adam Smith

What example does Adam Smith give for labour specialisation?

a pin factory

What are the 3 main advantages of labour specialisation?

efficiency, productivity, and lowered training costs

What are the 3 main disadvantages of labour specialisation?

decreased worker morale, little chance of career progression, and a narrow range of skills

What is the Law of Demand?

the inverse(negative) relationship between price and quantity demanded

What is the Law of Supply?

the positive relationship between price and quantity supplied

What is a market?

a place where buyers and sellers come together, and where the interaction of supply and demand occurs to determine a price

What is a cost-benefit analysis?

an evaluation of all the costs and benefits of various options in order to make the most optimal decision

What are financial costs relating to a cost-benefit analysis?

the monetary expenditures and sacrifices required to implement a decision

What are extrenal costs relating to a cost-benefit analysis?

indirect, unintended expenses or negative impacts imposed on third parties who are not directly involved in the transaction or project

What are external benefits relating to a cost-benefit analysis?

the indirect positive effects of a project, policy or business decision on third parties who are not directly involved in the transaction

What are future projected costs and benefits relating to a cost-benefit analysis?

the estimated expenses and expected returns of a proposed project, decision, or investment over a specific future timeframe

What is a net cost relating to a cost-benefit analysis?

the costs outweigh the benefits, therefore generally the project does not proceed

What is a net benefit relating to a cost-benefit analysis?

the benefits outweigh the costs, therefore generally the project is more likely to proceed

What is microeconomics?

studies the behaviour and decisions of individuals and firms

What is macroeconomics?

studies the behaviour and decisions of governments and countries, it looks at the economy as a whole

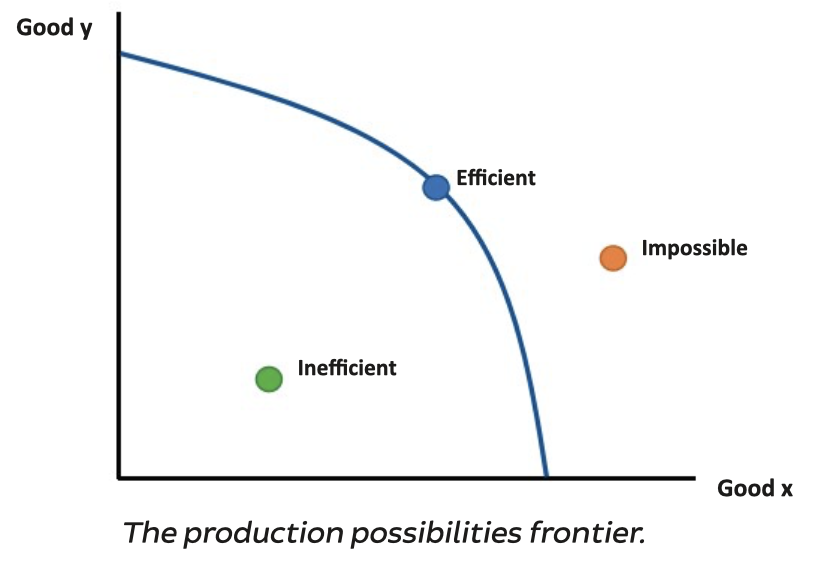

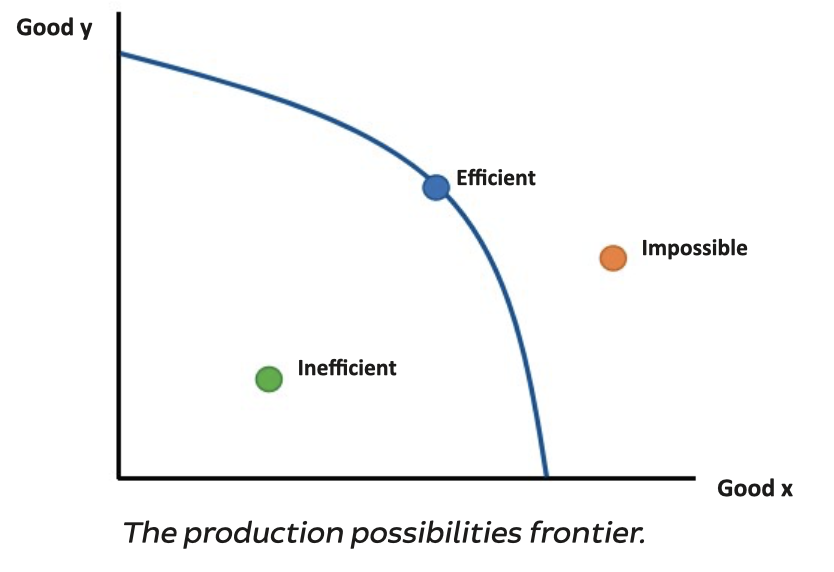

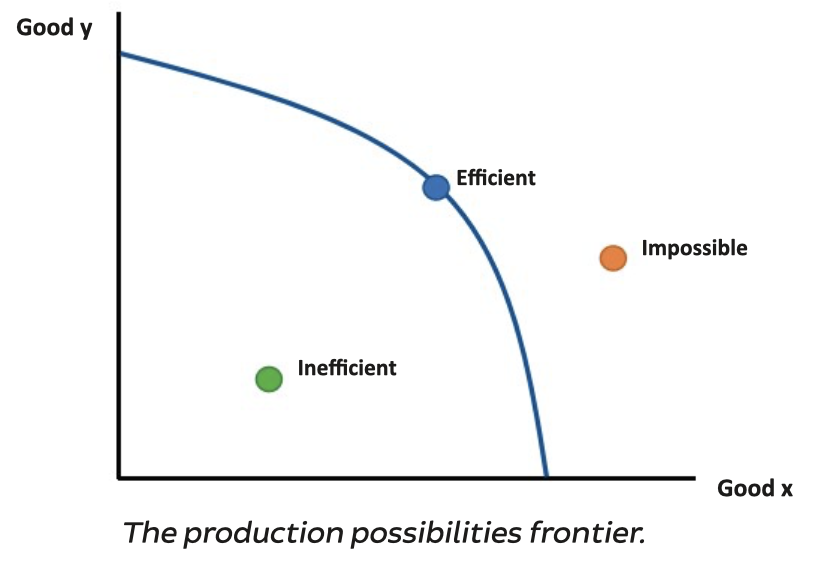

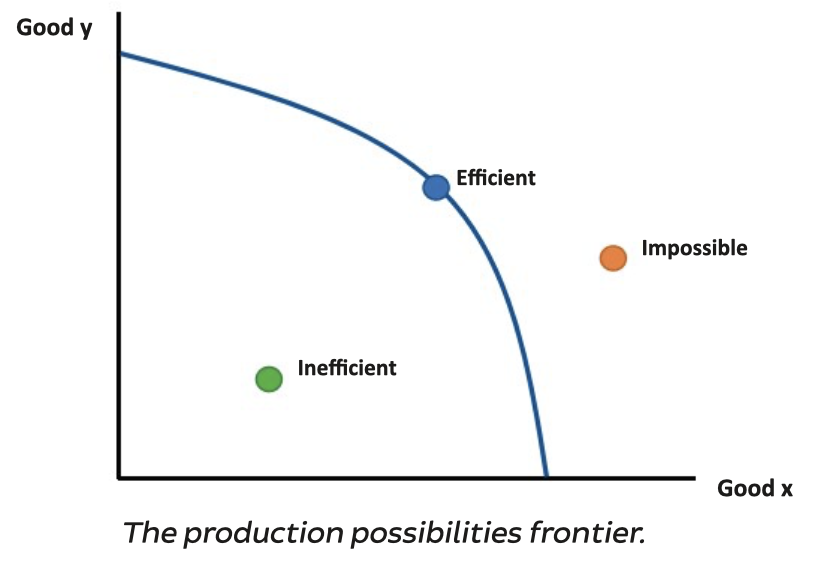

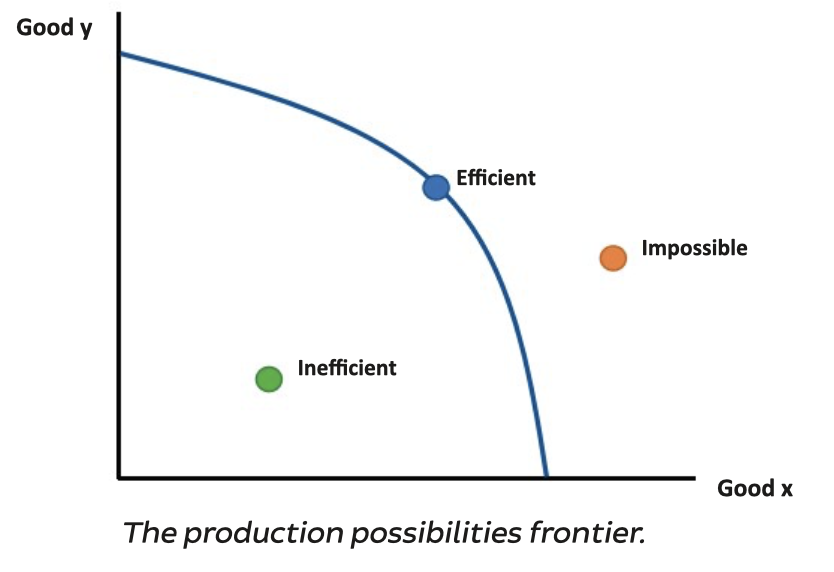

What is this?

production possibilities frontier

What is the production possibility frontier?

an economic model used to show the capacity of the economy or firm to produce goods and services with the scarce resources that are available

What is on the x-axis and thy y-axis of a production possibility frontier?

two goods which can be produced from the same resources

What does the curve on a production possibility frontier represent?

combinations of both goods that could potentially be produced with the scarce resources available assuming these are fully and efficiently used

What does movement along the curve of a production possibility frontier indicate?

that an opportunity cost is incurred

What does a point that is to the left of the curve on a production possibility frontier mean?

it can be produced, however resources are being underutilised and not used efficiently

What does a point that is to the right of the curve on a production possibility frontier mean?

it cannot be produced as the economy or firm does not have the capacity

What causes the curve of a production possibility frontier to shift to the left?

if there is a disruption to the supply of resources

What causes the curve of a production possibility frontier to shift to the right?

if the resource supply increases