A1: Audit Reports

1/60

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

61 Terms

A1-M1: Which standards provide the most authoritative U.S. Auditing guidance for nonissuers and issuers, and who issues those standards?

Nonissuers: Statement on Auditing Standards (SAS), issued by the AICPA Auditing Standards Board

Issuers: Auditing Standards (AS), issued by the PCAOB

A1-M2: State the primary purpose of an audit.

To provide financial statement users with an opinion on whether the financial statements are fairly presented, in all material respects, in accordance with the applicable financial reporting framework.

A1-M2: What are the five general GAAS requirements related to the conduct of an audit?

S - Professional Skepticism

E - Ethical Requirements

J - Professional Judgment

E - Sufficient and Appropriate Audit Evidence

C - Compliance with GAAS

A1-M2: Identify three inherent limitations of an audit.

The nature of financial reporting

The nature of audit procedures

Timeliness of financial reporting and the balance between benefit and cost

A1-M3: When should an auditor’s opinion be modified?

When the auditor determines that the financial statements as a whole are materially misstated (GAAP issue)

When the auditor is unable to obtain sufficient appropriate audit evidence to conclude that the financial statements as a whole are free from material misstatement (GAAS issue)

A1-M4: List in order the primary sections of an unmodified audit opinion (nonissuer).

Title

Addressee

Auditor’s Opinion

Basis for Opinion

Responsibilities of Management for the Financial Statements

Auditor’s Responsibilities for the Audit of the Financial Statements

Signature of the Auditor, Auditor’s Address, and Date of the Auditor’s Report

When applicable, the auditor’s report may include additional sections depending on the circumstances of the audit. Examples include Going Concern, Key Audit Matters, Other Information, and Other Reporting Responsibilities.

A1-M4: What should be included in the opinion paragraph of the unmodified audit opinion (nonissuer)?

The entity under audit

The title of each financial statement and reference to the notes

The dates or periods covered by the financial statements

A statement that the financial statements have been audited

A statement that the financial statements present fairly, in all material respects, in accordance with the applicable financial framework

The applicable financial reporting framework and its origin

A1-M4: What should be included in the management’s responsibility paragraph of the unmodified audit opinion (nonissuer)?

An explanation that management is responsible for the preparation and fair presentation of the financial statements

A statement that this responsibility includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error

When required, the evaluation of whether there are conditions or events that raise substantial doubt about the entity’s ability to continue as a going concern

A1-M4: Where in the standard unmodified opinion (nonissuer) does the auditor refer to (1) the applicable financial reporting framework (i.e., GAAP or IFRS) and (2) generally accepted auditing standards?

The applicable financial reporting framework is referred to in the management’s responsibility and opinion sections.

GAAS is referenced to in the basis for opinion and auditor’s responsibility sections.

What is the definition of a key audit matter (KAM)?

Key audit matters are those matters that were of most significance in the audit of the financial statements of the current period and are selected from the matters communicated to those charged with governance.

Key audit matters relate to the audits of NONISSUERS ONLY and entities have the option of whether or not to engage the auditor to communicate such matters in the auditor’s report.

A1-M4: When an auditor is engaged to communicate key audit matters in the auditor’s report, what information should be included?

The auditor’s report should include a separate section with the heading “Key Audit Matters” and the following information should be included:

A description of each matter

A description of why it was of most significance to the audit

How the matter was addressed in the audit of the financial statements

A1-M4: In what circumstances would an auditor be prohibited from communicating key audit matters in the auditor’s report?

When the auditor expresses an adverse opinion or disclaims an opinion on the financial statements, unless such reporting is required by law or regulation

A1-M4: Can an auditor that has been engaged to communicate key audit matters in the auditor’s report conclude that there are no key audit matters to communicate?

Yes, an auditor may determine, based on the facts and circumstances of the audit, that there are no key audit matters to communicate. In this circumstance, a statement to this effect should be added to the “Key Audit Matters” section of the auditor’s report.

A1-M4: List in order the primary sections of an unqualified audit opinion (issuer).

Title

Addressee

Opinion section

Basis for Opinion section

Critical audit matters

Signature, tenure, location

Report date

A1-M4: What should be included in the opinion section of the unqualified audit opinion (issuer)?

The first section of the auditor’s report must include the section heading “Opinion on the Financial Statements” and the following:

The name of the company whose financial statements have been audited

A statement identifying each financial statement and any related schedule that has been audited

Dates or periods covered by each financial statement and related schedule

A statement indicating that the financial statements were audited

An opinion that the financial statements present fairly, in all material respects, the financial position of the company as of the balance sheet date and the results of its operations and its cash flows for the period ended in conformity with the applicable financial reporting framework

A1-M4: What should be included in the first paragraph under the Basis for Opinion section in the unqualified audit opinion (issuer)?

The second section of the auditor’s report must include the section heading “Basis for Opinion” and the following:

A statement that the financial statements are the responsibility of the company’s management

A statement that the auditor’s responsibility is to express an opinion on the financial statements based on the audit

A statement that the auditor is a public accounting firm registered with the PCAOB (United States) and is required to be independent with respect to the company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the SEC and the PCAOB

A1-M4: What should be included in the second paragraph under the Basis for Opinion section in the unqualified audit opinion (issuer)?

The second paragraph under the Basis for Opinion section contains the following:

A statement that the audit was conducted in accordance with the standards of the PCAOB

A statement that the PCABO standards require that the auditor plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud

A statement that the audit included:

Performing procedures to assess the risks of material misstatement

Examining, on a test basis, evidence regarding the amounts and disclosures

Evaluating the accounting principles used and significant estimates made by management and

Evaluating the overall presentation of the financial statements and

A statement that the auditor believes that the audit provinces a reasonable basis for the auditor’s opinion

A1-M4: Where in the standard unqualified opinion (issuer) does the auditor refer to (1) the applicable financial reporting framework (i.e., GAAP) and (2) the standards of the PCAOB?

The applicable financial reporting framework is referred to in the opinion paragraph.

The standards of the PCAOB are referred to in the second paragraph under the Basis for Opinion section.

A1-M4: The auditor’s report should not be dated earlier than the date on which the auditor has obtained sufficient appropriate audit evidence. This should include evidence that what three things have occurred?

Evidence that:

Audit documentation has been reviewed

Financial statements have been prepared and

Management has taken responsibility for the financial statements

A1-M4: In most audits of issuers, how many critical audit matters (CAMs) will an auditor normally identify?

It is expected that, in most audits, the auditor would identify at least one CAM.

A1-M4: What is the definition of a critical audit matter (CAM)?

A critical audit matter is defined as a matter that was communicated or required to be communicated to the audit committee and that:

relates to the accounts or disclosures that are material to the financial statements and

involved especially challenging, subjective, or complex auditor judgment

Note: Audit reports for issuers must include any CAMs or state that the auditor determined there were no CAMs

A1-M4: In determining critical audit matters (CAMs), what factors should the auditor consider?

The auditor should consider the auditor’s assessment of the risks of material misstatement, areas of significant judgment or estimation by management, nature and timing of unusual transactions, the degree of subjectivity in applying audit procedures, and the extent of specialized skill or knowledge regarding a matter.

A1-M4: For each CAM identified, what should the audit report of an issuer include?

I - Identification of the CAM

P - Description of the Principal considerations that led the author to determine the matter was a CAM

A - Description of how the CAM was Addressed in the audit

D - Reference to the relevant financial statement accounts or Disclosures

A1-M4: What should the auditor of an issuer do if the auditor determines there are no CAMs?

When the auditor determines that there are no CAMs, the audit report should state:

“We determined that there are no critical audit matters.”

A1-M5: When would an auditor use professional judgment to determine whether to issue a qualified opinion or an adverse opinion?

When audit evidence indicates that there is material misstatement of the financial statements,

A qualified opinion is issued when the auditor concludes that misstatements, individually or in the aggregate, are material but not pervasive to the financial statements

An adverse opinion is issued when the auditor concludes that misstatements, individually or in the aggregate, are both material and pervasive to the financial statements

A1-M5: Describe the circumstances in which a material misstatement of the financial statements may arise

Misstatements may arise in relation to:

The appropriateness of accounting policies

The application of accounting policies

The appropriateness of the financial statement presentation

The appropriateness or adequacy of disclosures in the financial statements

A1-M5: If an opinion is qualified due to material misstatement of financial statements on an issuer audit report, where does the paragraph explaining the qualification appear?

A paragraph should be placed immediately following the opinion paragraph. There is no heading for this paragraph. The paragraph should include:

All of the substantive reasons that led the auditor to conclude that there has been a departure from GAAP

Disclosure of the principal effects of the subject matter of the qualification on financial position, results of operations, and cash flows, if practicable

If the effects are not reasonably determinable, the report should so state

If such disclosures are made in a note to the financial statements, the explanatory paragraph(s) may be shortened by referring to it

Compared to a standard unqualified opinion of an issuer, determine the paragraphs that are modified in an audit report when the following opinions are issued due to financial statement issues (Misstatement):

Qualified

Adverse

Qualified: Opinion Section* = Except for, Additional Paragraph = Yes, Basis for Opinion Section* = Standard

Adverse: Opinion Section* = Do not present fairly, Additional Paragraph = Yes, Basis for Opinion Section* = Standard

*Note: The section headings (“Opinion on the Financial Statements” and “Basis for Opinion”) are the same as the standard unqualified report when a qualified or adverse opinion is issued

A1-M5: Is an auditor required to report on critical audit matters (CAMs) when issuing an adverse opinion?

No, the auditor is not required to report CAMs when an adverse opinion is expressed

A1-M6: When would an auditor use professional judgment to determine whether to issue a qualified opinion or a disclaimer of opinion?

When there is a limitation of the scope of the audit.

A qualified opinion is issued when an auditor is unable to obtain sufficient appropriate audit evidence on which to base an opinion and the auditor determines that the possible effects could be material but not pervasive

A disclaimer of opinion is expressed when the auditor is unable to obtain sufficient appropriate audit evidence on which to base an opinion and the auditor determines that the possible effects could be both material and pervasive

A1-M6: Identify some examples of scope limitations

Restrictions on the auditor’s ability to perform auditing procedures may be caused by:

Time constraints

Inability to observe inventory

Inability to confirm receivables

Inability to obtain audited financial statements of a consolidate investee

Restrictions of the use of auditing procedures

Inadequacy of accounting records

Refusal of the client’s attorney to respond to inquiry

Refusal of management to provide a representation letter

A1-M6: What situations may result in a disclaimer of opinion in an audit report?

Pervasive inability to obtain sufficient appropriate audit evidence

Lack of independence (always results in disclaimer)

Going concern uncertainty [Note: If adequate disclosure of going concern exists, the auditor may choose between either an unqualified opinion with a separate report section (nonissuer) or explanatory paragraph (issuer), or a disclaimer of opinion.]

A1-M6: If an opinion is modified on a nonissuer audit report, where does the explanation of the modification appear?

The paragraph explaining the modification would appear after the opinion paragraph. The “basis for modification” paragraph should use the appropriate heading. Appropriate headings include:

Basis for Qualified Opinion

Basis for Adverse Opinion

Basis for Disclaimer of Opinion

A1-M6: Is an auditor required to report on critical audit matters (CAMs) when issuing a disclaimer of opinion?

No, the auditor is not required to report on CAMs when issuing a disclaimer of opinion

A1-M7: What is the purpose of an emphasis-of-matter paragraph (nonissuer)?

The purpose of an emphasis-of-matter paragraph is to reference a matter that is appropriately presented in the financial statements, but is of such importance that it is fundamental to the user’s understanding of the financial statements.

A1-M7: Under what circumstances would an emphasis-of-matter paragraph be required in an auditor’s report (nonissuer)?

An emphasis-of-matter paragraph should be used in the auditor’s report when:

A change in reporting entity results in financial statements that, in effect, are those of a different reporting entity

There is a need to describe a justified change in accounting principle that has a material effect on the entity’s financial statements

Facts are subsequently discovered that lead to a change in the auditor’s opinion (note: an other-matter paragraph may also be appropriate)

The financial statements are prepared in accordance with an applicable special purpose framework, other than regulatory basis financial statements intended for general use

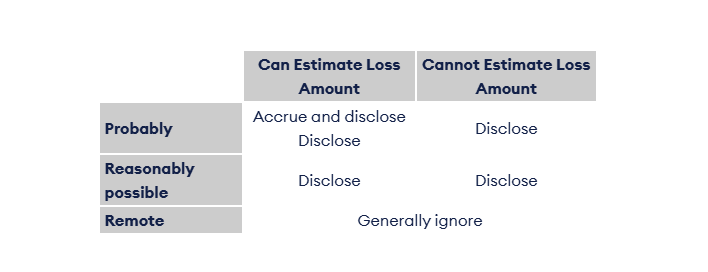

A1-M7: According to U.S. GAAP, when are contingencies (such as pending litigation) required to be:

Accrued and disclosed?

Disclosed only?

A1-M7: What are the reporting requirements for an other-matter paragraph (nonissuer)?

When an other-matter paragraph is included in the auditor’s report, the auditor should use the heading “Other Matter” or other appropriate heading

A1-M7: What are the reporting requirements for an explanatory paragraph (issuer)?

Reporting requirements for an explanatory paragraph include:

The explanatory paragraph generally should include an appropriate heading

The paragraph should describe the matter being emphasized and the location of relevant disclosures about the matter in the financial statements

The explanatory paragraph will generally follow the opinion paragraph when added to an unqualified report

A1-M8: If, during the current examination of comparative financial statements, the auditor discovers evidence that affects the prior statements and the opinion that was expressed, what action should be taken? *Only DORCS change their mind!

The auditor should update the opinion in the current year’s report. If the opinion differs from the previous opinion, the reason(s) should be disclosed in a separate emphasis-of-matter or other-matter paragraph following the opinion paragraph (nonissuers) or explanatory paragraph (issuers).

The paragraph should disclose the:

D - Date of the auditor’s previous report

O - Opinion type previously issued

R - Reason for prior opinion

C - Changes that have occurred

S - Statement that the “opinion….is different”

A1-M8: The predecessor auditor should take what steps before reissuing an audit report on prior period financial statements?

Read the statements for the current period

Compare the previous audited statements with the current period statements

Obtain a letter of representation from the successor auditor

Obtain a letter of representation from management at or near the date of reissuance

If unrevised, use the original report date; if revised, dual date the report

A1-M8: What statements should be included in the auditor’s report in an other-matter paragraph (nonissuer) or explanatory paragraph (issuer) when comparative financial statements are presented and the prior auditor’s report is not reissued?

The other-matter paragraph (nonissuer) or explanatory paragraph (isser) should include the following

A statement that the financial statements of the prior period were audited by the predecessor auditor

The type of opinion expressed by the predecessor auditor. If the opinion was modified, include the reason for the modification

The nature of any emphasis-of-matter, other-matter, or explanatory paragraph included in the predecessor’s report

The date of the predecessor auditor’s report

A1-M8: What is the effect on the audit report when the current period financial statements are audited and presented in comparative format when the prior period was reviewed or compiled?

If the prior period financial statements were reviewed or compiled, an other-matter paragraph (nonissuer) or explanatory paragraph (issuer) is added that includes

A description of the service performed in the prior period

The date of the prior period report

A description of any material modifications in the report

A statement that the service was less in scope than an audit and does not provide a basis for expressing an opinion on the financial statements (review)

A statement that no opinion or other form of assurance is expressed on the financial statements (compilation)

A1-M8: Define a component auditor

A component auditor is an auditor who performs work on the financial information of a component that will be used as audit evidence for the group audit of a nonissuer. The component auditor may be part of the group engagement partner’s firm, a network firm, or another firm

A1-M8: Should a group auditor refer to the work of a component auditor in the auditor’s report of a nonissuer?

For audits of group financial statements of nonissuers, the auditor should use his or her understanding of each component auditor to determine whether to make reference to the individual component auditor in the auditor’s report. If the group engagement partner decides to assume responsibility for the work of a component auditor, then no reference to the component auditor should be made in the auditor’s report.

A1-M8: What are the responsibilities of a group engagement partner (team) when it assumes responsibility for the work of a component auditor in the audit of a nonissuer?

No reference to the component auditor is made in the auditor’s report.

If the component is a significant component due to its individual financial significance, it should be audited by the group engagement team or the component auditor.

When a component is deemed significant because of significant risks of material misstatement to the group of financial statements, the group engagement team or component auditor should perform additional audit procedures pertaining to the potential risks identified.

Components that are not considered significant only required that analytical procedures be performed by the group engagement team.

A1-M8: Identify the two requirements that are necessary to reference a component auditor in the auditor’s report of a nonissuer

Reference to the component auditor in the auditor’s report of a nonissuer can be made if the following requirements are met:

The component auditor has performed an audit in accordance with GAAS

The component auditor’s report is not restricted use

A1-M9: Define the two types of subsequent events

A recognized subsequent event relates to a condition that existed on or before the balance sheet date. Recognized subsequent events require financial statement adjustment

A nonrecognized subsequent event occurs after the balance sheet date. Nonrecognized subsequent events generally do not require financial statement adjustment, but may require footnote disclosure

A1-M9: What procedures should the auditor perform during the subsequent period?

Between the date of the financial statements and the date of the auditor’s report (subsequent period), the auditor should:

P - review Post balance sheet transactions

R - obtain a Representation letter from management describing events that occurred during the subsequent period requiring adjustment to the financial statements

I - Inquire with management or those charged with governance whether subsequent events occurred that could impact financial statements. Also inquire with the client’s legal counsel concerning litigation, claims, and assessments

M - review Minutes of board and committee meetings

E - Examine current interim financial statements and compare to financial statements under audit

A1-M9: After the date of the auditor’s report, what actions should an auditor take regarding subsequent events?

None. Although the auditor is responsible for investigating subsequent events until the date of the auditor’s report, the auditor has no active responsibility to make inquiries or perform auditing procedures after that date.

An exception to this rule is when an auditor’s report is included in an exempt offering document (and the auditor is involved in the offering) or registration statement. In such a case, the auditor should extend subsequent event procedures.

A1-M9: After issuance of the report, what actions should an auditor take upon discovering information that materially affects the report?

DETEERMINE whether there are persons relying or likely to rely on the financial statements

ADVISE the client to immediately disclose the new information to persons currently replying or likely to rely on the financial statements. This disclosure may take the form of REVISED financial statements, DISCLOSURES and revisions to any imminent financial statements, or NOTIFICATION that the financial statements and report should not be relied upon

ADVISE the client to discuss the new disclosures or revisions with the SEC, stock exchanges, and appropriate regulatory agencies

ENSURE that appropriate steps have been taken by the client

A1-M9: When and why is dual dating used?

Dual dating is used when subsequent events requiring financial statement adjustment or disclosure come to the auditor’s attention after the original date of the audit report. Dual dating extends the auditor’s responsibility only for the particular subsequent event. The original date of the report is retained for the rest of the financial statements.

A1-M10: What is the auditor’s responsibility with respect to information that is presented in a document containing the audited financial statements?

The auditor should discuss with management and obtain written acknowledgement regarding which documents compose the annual report. The auditor should read the other information to determine that it is consistent with the audited financial statements and that there are no material inconsistencies or material misstatements of fact. The auditor should reference the other information in the auditor’s report by including a separate section with the heading “Other Information” or another appropriate heading.

A1-M10: What are the two objectives of engagements to report on supplementary information?

To evaluate the presentation of the supplementary information in relation to the financial statements as a whole.

To report on whether the supplementary information is fairly stated, in all material respects, in relation to the financial statements as a whole.

A1-M10: What procedures would an auditor perform related to supplementary information that accompanies the financial statements and is required by a designated accounting standards setter, such as the FASB?

Apply limited procedures, which includes:

An inquiry regarding the methods used to prepare the supplementary information, including whether preparation is in accordance with prescribed guidance, changes from prior years and reasoning, and significant assumptions used.

Determining whether the supplementary information is consistent with management’s responses, audited financial statements, and other knowledge.

Obtaining written management representations regarding the required supplemental information.

The auditor may (but is not required to) issue an opinion on the information.

A1-M11: Give examples of special purpose frameworks

Cash basis

Tax basis

Regulatory basis

Contractual basis

Any other basis of accounting that uses a definite set of logical, reasonable criteria that is applied to all material items appearing in the financial statements.

A1-M11: Which of the following elements should be included in the auditor’s report when financial statements are prepared on the cash or tax basis?

Description of purpose for which special purpose financial statements are prepared

Emphasis-of-matter paragraph alerting readers about the preparation in accordance with a special purpose framework

Other-matter paragraph restricting the use of the auditor's report

An emphasis-of-matter paragraph alerting readers about the preparation in accordance with a special purpose framework should be included in the auditor’s report for financial statements prepared on the cash or tax basis.

A1-M11: Which of the following elements should be included in the auditor’s report when financial statements are prepared on the regulatory basis (not for general use) and contractual basis?

Description of purpose for which special purpose financial statements are prepared

Emphasis-of-matter paragraph alerting readers about the preparation in accordance with a special purpose framework

Other-matter paragraph restricting the use of the auditor's report

An auditor’s report for financial statements prepared on the regulatory basis (not for general use) or contractual basis should include:

Description of purpose for which special purpose financial statements are prepared

Emphasis-of-matter paragraph alerting readers about the preparation in accordance with a special purpose framework

Other-matter paragraph restricting the use of the auditor’s report

A1-M11: Which of the following elements should be included in the auditor’s report when financial statements are prepared on the regulatory basis (for general use)?

Description of purpose for which special purpose financial statements are prepared

Emphasis-of-matter paragraph alerting readers about the preparation in accordance with a special purpose framework

Other-matter paragraph restricting the use of the auditor's report

An auditor’s report for financial statements prepared on the regulatory basis for general use include the description of purpose for which special purpose financial statements are prepared.

A1-M11: What should be included in an emphasis-of-matter paragraph included in a special purpose framework (other than regulatory basis financial statements intended for general use)?

An emphasis-of-matter paragraph should:

Indicate that the financial statements are prepared in accordance with the applicable special purpose framework

Refer to the note to the financial statements that describes that framework

State that the special purpose framework is a basis of accounting other than GAAP

State that the financial statements may not be suitable for any purpose other than the stated purpose (when the purpose is required to be described)

A1-M11: List several elements of a report on special purpose financial statements

An addressee and a title stating the auditor is independent

An opinion that describes the special purpose financial statements have been audited, expresses an opinion, and references the special purpose framework used

Date of report, issuance city and state, and audit firm’s signature

When required:

An emphasis-of-matter paragraph

An other-matter paragraph for preparing the financial statements

Description of the purpose for preparing the financial statements

Description of management’s responsibility for the preparation of the financial statements and use of the applicable financial reporting framework