Theme 1

1/45

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

46 Terms

An economic model

A simplified version of reality that helps you observe, understand and make predictions about economic behaviour

Ceteris paribus

All of things remain equal

Positive statement

Statements about economics which can be proven true or false. supported or refuted by evidence. fact which can be proven or disproven. For example, “the service sector will grow by 30% in the next five years.”

Normative statement

Statements which cannot be supported or refuted conclusively. opinions about how economics and markets should work. Contains a value judgment i.e. subjective. for example, ‘the government should increase the state pension.’

Positive economics

A scientific or objective study

Normative economics

is value judgements and policy recommendations

Scarcity

A situation that arises when people have unlimited wants in the face of limited resources

Free goods

Goods such as the earths atmosphere that are not normally regarded as being scarce

Economic goods

Goods that are scarce

Opportunity cost

The value of the next best alternatives forgone

Marginal analysis

An approach to economic decision making based on considering the additional (marginal) benefits and cost of a change in behaviour

the three key groups of decision makers in economic analysis

Consumers

Government

Producers

Factors of production

resources used in the production process; inputs into production, particularly including:

Land

Enterprise

Labour

Capital

rewards for the 4 factor inputs

land - rental income to owners of land

Enterprise - profits

Labour - wages and salaries from employment

Capital - interest from savings + dividends from shares

Renewable resources

natural resources that can be replenished, such as forests that can be replanted, or solar energy that does not get used up

Non-renewable resources

natural resources that once used cannot be replenished, such as coal or oil

Production possibility frostier (PPF)

a curve showing the maximum combinations of goods or services that can be produced in a given period

Trade-off

a situation in which the choice of one alternative requires the sacrifice of another

Capital goods

goods used as part of the production process, such as machinery or factory buildings (like an investment)

Consumer goods

goods produced for present use (consumption)

Gross Domestic Product

The measure of the total output of an economy

Market demand is the sum of ________

All individual demands in the market

What are some things that influence supply

production cost

technology of production

Taxes and subsidies

Price of related goods

firms’ expectations about future prices

the number of firms operating in the market

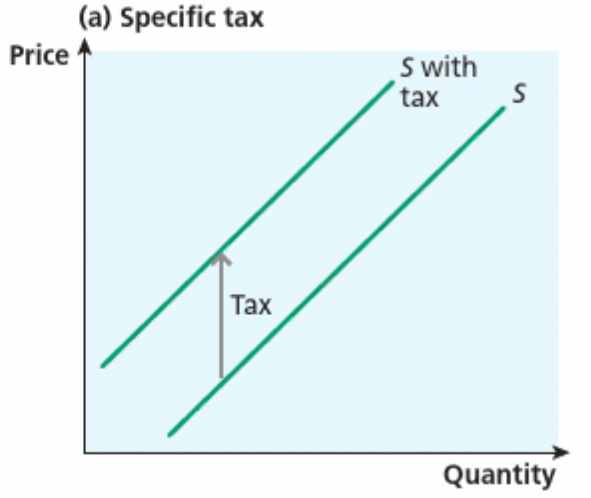

Which way will the supply curve shift when taxes are add

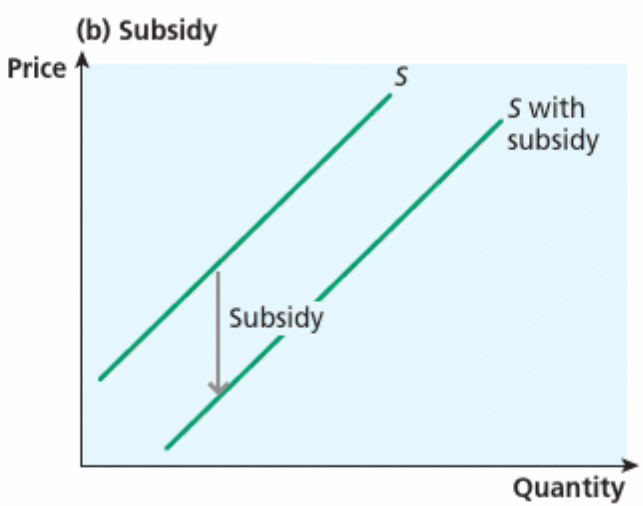

Which way will the supply curve shift when the government pays firms a subsidy

Right

What will companies do if they think prices will go up

Save some to sell later

What will happen to the supply curve if more firms join the market

Shift right

What’s cartel

an agreement between firms in a market on price and output with the intention of maximising their joint profits

What’s excess supply

a situation in which the quantity that firms are willing and able to supply exceeds the quantity that consumers wish to demand at the going price

Excess demand

a situation in which the quantity that consumers wish to demand at the going price exceeds the quantity that firms are willing and able to supply

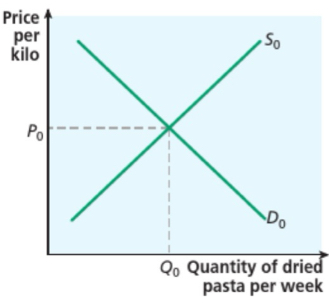

Market equilibrium

a situation that occurs in a market when the price is such that the quantity demanded by consumers is exactly balanced by the quantity supplied by firms

What can affect market equilibrium

A change in consumer preferences

A change in the price of a substitute

An improvement in the ‘good’s technology

An increase in labour costs

What’s the difference between a free market and a centrally planned economy

In a free market, market forces are allowed to allocate resources but in a centrally planned economy the state plans and directs resources. (In between these is the mixed economy)

Consumer surplus

the value that consumers gain from consuming a good or service over and above the price paid

Marginal social benefit (MSB)

the additional benefit that society gains from consuming an extra unit of a good

What’s indirect tax

a form of taxation where the tax is collected by an intermediary, such as a manufacturer or retailer, and then passed onto the consumer through the price of a good or service

Direct tax

A tax you pay directly to the government

Subsidy

A sum of money granted by the state or a public body to help a firm keep their prices low

Marginal utility

When you have more and more of a product the satisfaction you get from having one more unit diminishes.

Disposable income

Measures an individuals or households purchasing power after accounting for inflation and taxes, reflecting the actual amount of goods and services that can be bought

Normal good

An item that demand increases when consumer income rises and decreases when income falls Ceteris paribus

Inferior good

A good whose demand decreases as consumer income increases and vice versa

Joint demand

When demand for two or more goods is interdependent and they are consumed together

Competitive demand

When two goods are substitute for each other

Derived demand

Demand for a factor of production that is derived from the demand for the final product

Revenue

total income a business generates from selling its core products or service