Equations APCB

1/139

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

140 Terms

Balance Sheet Identity (2.1)

\text{Assets} = \text{Liabilities} + \text{Stockholders' Equity}

Market Value of Equity (2.2)

\text{Market Value of Equity} = \text{Shares Outstanding} \times \text{Market Price per Share}

Market-to-Book Ratio (2.3)

\text{Market-to-Book Ratio} = \dfrac{\text{Market Value of Equity}}{\text{Book Value of Equity}}

Enterprise Value (2.4)

\text{EV} = \text{Market Value of Equity} + \text{Debt} - \text{Cash}

Earnings Per Share / EPS (2.5)

\text{EPS} = \dfrac{\text{Net Income}}{\text{Shares Outstanding}}

Retained Earnings (2.6)

\text{Retained Earnings} = \text{Net Income} - \text{Dividends}

Change in Stockholders' Equity (2.7)

\Delta\text{Stockholders' Equity} = \text{Net Income} - \text{Dividends} + \text{Sales of Stock} - \text{Repurchases of Stock} l

Gross Margin (2.8)

\text{Gross Margin} = \dfrac{\text{Gross Profit}}{\text{Sales}}

Operating Margin (2.9)

\text{Operating Margin} = \dfrac{\text{Operating Income}}{\text{Sales}}

Net Profit Margin (2.10)

\text{Net Profit Margin} = \dfrac{\text{Net Income}}{\text{Sales}}

Accounts Receivable Days (2.11)

\text{AR Days} = \dfrac{\text{Accounts Receivable}}{\text{Average Daily Sales}}

Accounts Payable Days (2.12)

\text{AP Days} = \dfrac{\text{Accounts Payable}}{\text{Average Daily Cost of Sales}}

Inventory Turnover (2.13)

\text{Inventory Turnover} = \dfrac{\text{Annual Cost of Sales}}{\text{Inventory}}

EBITDA (2.14)

\text{EBITDA} = \text{EBIT} + \text{Depreciation} + \text{Amortization}

Debt-Equity Ratio (2.15)

\text{Debt-Equity Ratio} = \dfrac{\text{Total Debt}}{\text{Total Equity}}

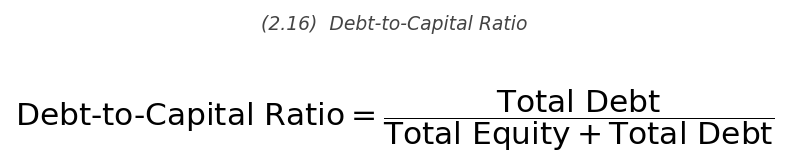

Debt-to-Capital Ratio (2.16)

\text{Debt-to-Capital} = \dfrac{\text{Total Debt}}{\text{Total Equity} + \text{Total Debt}}

Net Debt (2.17)

\text{Net Debt} = \text{Total Debt} - \text{Cash \& Short-Term Investments}

Enterprise Value-to-EBITDA Leverage Ratio (2.18)

\text{Leverage Ratio} = \dfrac{\text{Enterprise Value}}{\text{Net Debt}}

Price-Earnings (P/E) Ratio (2.19)

\text{P/E} = \dfrac{\text{Share Price}}{\text{EPS}} = \dfrac{\text{Market Capitalization}}{\text{Net Income}}

Return on Equity / ROE (2.20)

\text{ROE} = \dfrac{\text{Net Income}}{\text{Book Value of Equity}}

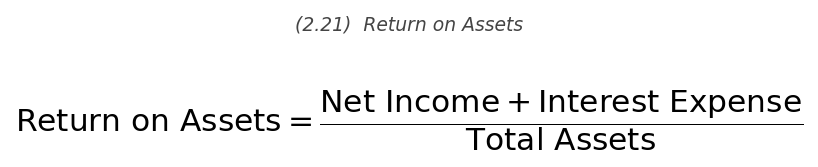

Return on Assets / ROA (2.21)

\text{ROA} = \dfrac{\text{Net Income} + \text{Interest Expense}}{\text{Total Assets}}

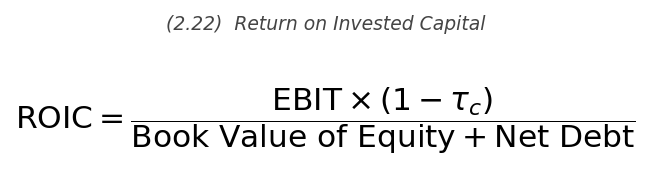

Return on Invested Capital / ROIC (2.22)

\text{ROIC} = \dfrac{\text{EBIT} \times (1 - \tau_c)}{\text{Book Value of Equity} + \text{Net Debt}}

DuPont Identity (2.23)

ROE = Profit Margin x Asset Turnover x Equity multiplier

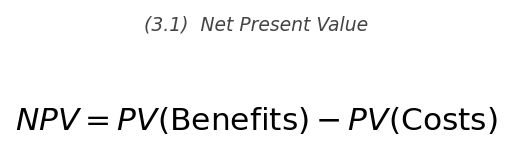

Net Present Value (3.1)

\text{NPV} = PV(\text{Benefits}) - PV(\text{Costs})

NPV as PV of Cash Flows (3.2)

\text{NPV} = PV(\text{All project cash flows})

No-Arbitrage Price of a Security (3.3)

\text{Price}(\text{Security}) = PV(\text{All cash flows paid by the security})

Return Calculation (3.4)

r = \dfrac{FV - \text{Price}}{\text{Price}} = \dfrac{FV}{\text{Price}} - 1

Value Additivity (3.5)

\text{Price}(C) = \text{Price}(A+B) = \text{Price}(A) + \text{Price}(B)

Future Value of a Cash Flow (4.1)

FV_n = C \times (1+r)^n

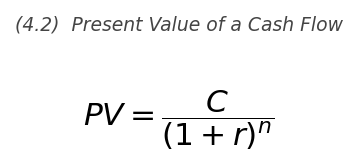

Present Value of a Cash Flow (4.2)

PV = \dfrac{C}{(1+r)^n}

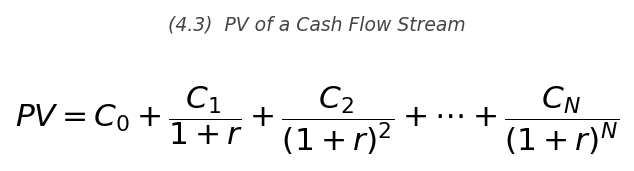

Present Value of a Cash Flow Stream (4.3)

PV = C_0 + \dfrac{C_1}{1+r} + \dfrac{C_2}{(1+r)^2} + \cdots + \dfrac{C_N}{(1+r)^N}

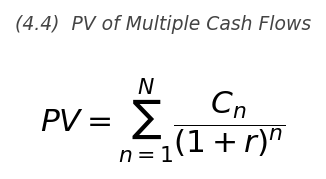

Present Value of Multiple Cash Flows (4.4)

PV = \displaystyle\sum_{n=1}^{N} \dfrac{C_n}{(1+r)^n}

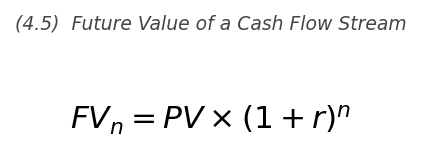

Future Value of a Cash Flow Stream (4.5)

FV_n = PV \times (1+r)^n

Net Present Value — Alternative Form (4.6)

\text{NPV} = PV(\text{benefits}) - PV(\text{costs})

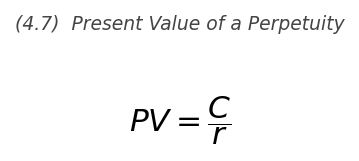

Present Value of a Perpetuity (4.7)

PV = \dfrac{C}{r}

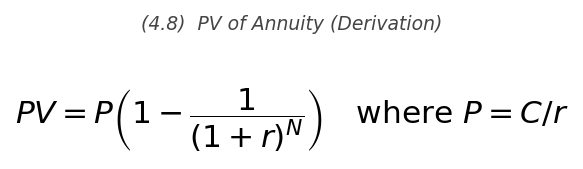

Present Value of an Annuity (4.9)

PV = C \times \dfrac{1}{r}\left(1 - \dfrac{1}{(1+r)^N}\right)

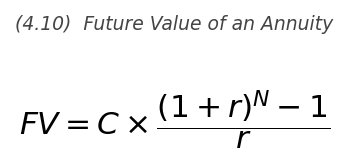

Future Value of an Annuity (4.10)

FV = C \times \dfrac{(1+r)^N - 1}{r}

Present Value of a Growing Perpetuity (4.11)

PV = \dfrac{C}{r - g}

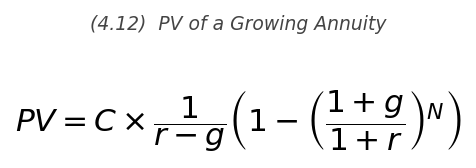

Present Value of a Growing Annuity (4.12)

PV = C \times \dfrac{1}{r-g}\left(1 - \left(\dfrac{1+g}{1+r}\right)^N\right)

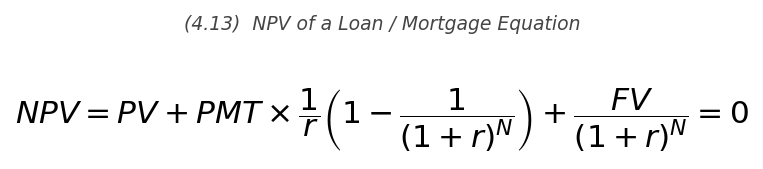

Loan or Annuity Payment (4.14)

C = \dfrac{P \cdot r}{1 - \dfrac{1}{(1+r)^N}}

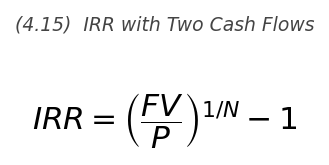

IRR with Two Cash Flows (4.15)

\text{IRR} = \left(\dfrac{FV}{P}\right)^{1/N} - 1

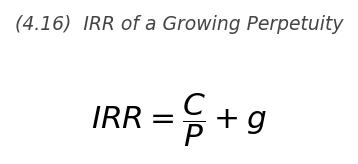

IRR of a Growing Perpetuity (4.16)

\text{IRR} = \dfrac{C}{P} + g

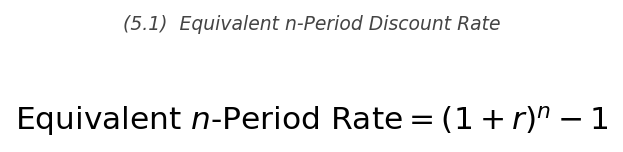

Equivalent n-Period Discount Rate (5.1)

\text{Equivalent } n\text{-Period Rate} = (1+r)^n - 1

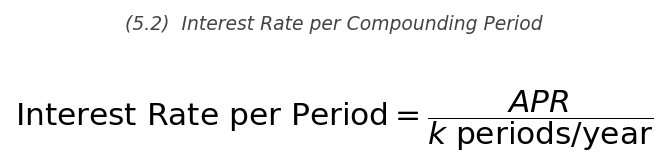

Interest Rate per Compounding Period (5.2)

\text{Rate per Period} = \dfrac{\text{APR}}{k}

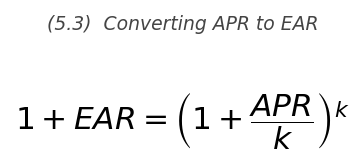

Converting APR to EAR (5.3)

1 + \text{EAR} = \left(1 + \dfrac{\text{APR}}{k}\right)^k

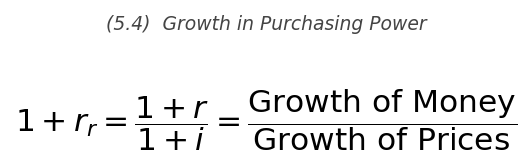

Growth in Purchasing Power (5.4)

1 + r_r = \dfrac{1 + r}{1 + i}

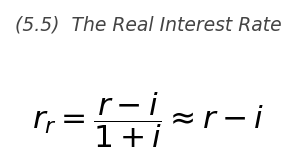

The Real Interest Rate (5.5)

r_r \approx \dfrac{r - i}{1 + i} \approx r - i

PV with Varying Discount Rates (5.6)

PV = \dfrac{C_n}{(1+r_n)^n}

PV of Cash Flow Stream with Term Structure (5.7)

PV = \dfrac{C_1}{1+r_1} + \dfrac{C_2}{(1+r_2)^2} + \cdots + \dfrac{C_N}{(1+r_N)^N}

After-Tax Interest Rate (5.8)

r_{\text{after-tax}} = r(1 - \tau)

Coupon Payment (6.1)

\text{CPN} = \dfrac{\text{Coupon Rate} \times \text{Face Value}}{k}

Price of a Zero-Coupon Bond (6.2)

P = \dfrac{FV}{(1 + YTM_n)^n}

Yield to Maturity of an n-Year Zero-Coupon Bond (6.3)

YTM_n = \left(\dfrac{FV}{P}\right)^{1/n} - 1

Risk-Free Interest Rate with Maturity n (6.4)

r_n = YTM_n

Yield to Maturity of a Coupon Bond (6.5)

P = \text{CPN} \times \dfrac{1}{y}\left(1 - \dfrac{1}{(1+y)^N}\right) + \dfrac{FV}{(1+y)^N}

Price of a Coupon Bond (6.6)

P = \dfrac{\text{CPN}}{1+YTM_1} + \dfrac{\text{CPN}}{(1+YTM_2)^2} + \cdots + \dfrac{\text{CPN}+FV}{(1+YTM_n)^n}

NPV of a Project (7.1)

\text{NPV} = -\text{Initial Investment} + \dfrac{FCF_1}{1+r} + \dfrac{FCF_2}{(1+r)^2} + \cdots

Profitability Index (7.2)

\text{PI} = \dfrac{\text{NPV}}{\text{Initial Investment}}

Income Tax on a Project (8.1)

\text{Income Tax} = \text{EBIT} \times \tau_c

Unlevered Net Income (8.2)

\text{Unlevered Net Income} = \text{EBIT} \times (1-\tau_c) = (\text{Rev} - \text{Costs} - \text{Dep}) \times (1-\tau_c)

Net Working Capital (8.3)

\text{NWC} = \text{Current Assets} - \text{Current Liabilities}

Change in Net Working Capital (8.4)

\Delta NWC_t = NWC_t - NWC_{t-1}

Free Cash Flow — Expanded Form (8.5)

FCF = (\text{Rev} - \text{Costs} - \text{Dep})(1-\tau_c) + \text{Dep} - \text{CapEx} - \Delta NWC

Free Cash Flow — Condensed Form (8.6)

FCF = (\text{Rev} - \text{Costs})(1-\tau_c) - \text{CapEx} - \Delta NWC + \tau_c \times \text{Dep}

PV of a Single Free Cash Flow (8.7)

PV(FCF_t) = \dfrac{FCF_t}{(1+r)^t}

Gain on Sale of Asset (8.8)

\text{Gain on Sale} = \text{Sale Price} - \text{Book Value}

Book Value of Asset (8.9)

\text{Book Value} = \text{Purchase Price} - \text{Accumulated Depreciation}

After-Tax Cash Flow from Asset Sale (8.10)

\text{After-Tax CF} = \text{Sale Price} - \tau_c \times \text{Gain on Sale}

One-Period Stock Price (9.1)

P_0 = \dfrac{Div_1 + P_1}{1 + r_E}

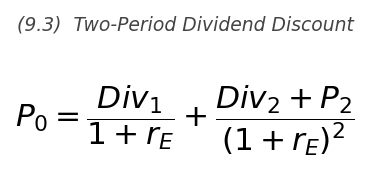

Two-Period Dividend Discount (9.3)

P_0 = \dfrac{Div_1}{1+r_E} + \dfrac{Div_2 + P_2}{(1+r_E)^2}

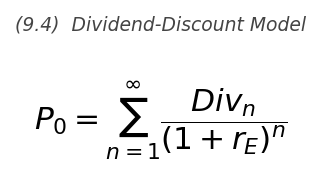

Dividend-Discount Model — General (9.4/9.5)

P_0 = \displaystyle\sum_{n=1}^{\infty} \dfrac{Div_n}{(1+r_E)^n}

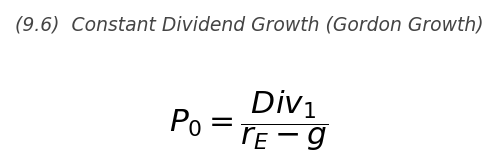

Constant Dividend Growth / Gordon Growth Model (9.6)

P_0 = \dfrac{Div_1}{r_E - g}

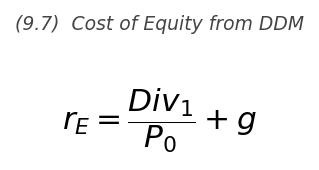

Cost of Equity from Dividend-Discount Model (9.7)

r_E = \dfrac{Div_1}{P_0} + g

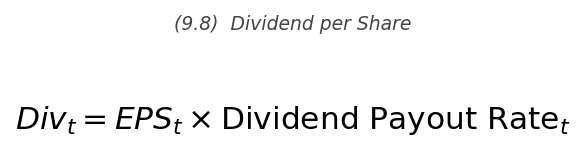

Dividend per Share (9.8)

Div_t = EPS_t \times \text{Dividend Payout Rate}

Change in Earnings from New Investment (9.9)

\Delta\text{Earnings} = \text{New Investment} \times \text{Return on New Investment}

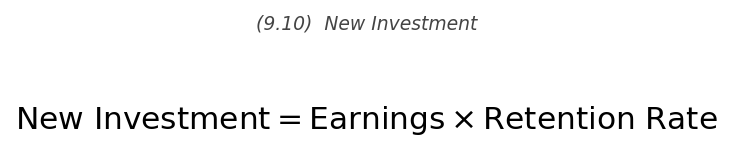

New Investment (9.10)

\text{New Investment} = \text{Earnings} \times \text{Retention Rate}

Earnings Growth Rate (9.11/9.12)

g = \text{Retention Rate} \times \text{Return on New Investment}

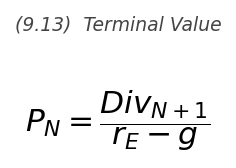

Terminal Value — Constant Growth (9.13)

P_N = \dfrac{Div_{N+1}}{r_E - g}

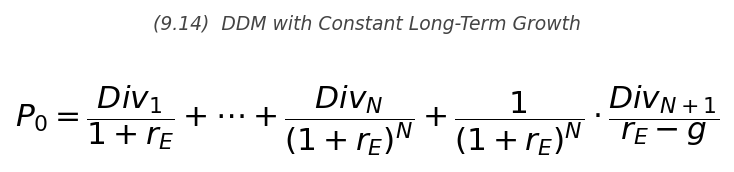

DDM with Constant Long-Term Growth (9.14)

P_0 = \dfrac{Div_1}{1+r_E} + \cdots + \dfrac{Div_N}{(1+r_E)^N} + \dfrac{1}{(1+r_E)^N} \cdot \dfrac{Div_{N+1}}{r_E - g}

Dividend-Discount Model — Compact (9.15)

P_0 = PV(\text{Future Dividends per Share})

Total Payout Model (9.16)

P_0 = \dfrac{PV(\text{Future Total Dividends and Repurchases})}{\text{Shares Outstanding}}

Enterprise Value — Restated (9.17)

\text{EV} = \text{Market Value of Equity} + \text{Debt} - \text{Cash}

Free Cash Flow for DCF Model (9.18)

FCF = \text{EBIT}(1-\tau_c) + \text{Dep} - \text{CapEx} - \Delta NWC

Net Investment (9.19)

\text{Net Investment} = \text{CapEx} - \text{Depreciation}

Free Cash Flow — Net Investment Form (9.20)

FCF = \text{EBIT}(1-\tau_c) - \text{Net Investment} - \Delta NWC

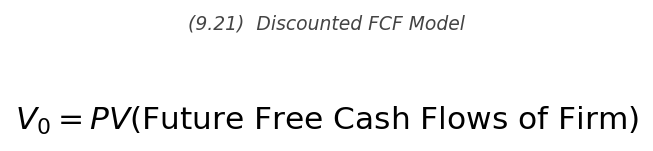

Discounted Free Cash Flow Model (9.21)

V_0 = PV(\text{Future Free Cash Flows of Firm})

Stock Price from Enterprise Value (9.22)

P_0 = \dfrac{V_0 + \text{Cash}_0 - \text{Debt}_0}{\text{Shares Outstanding}}

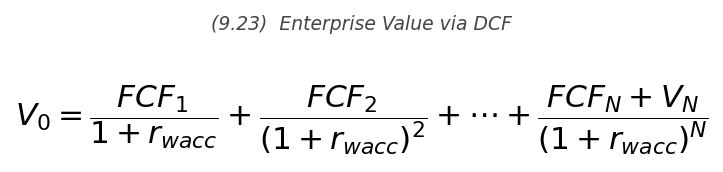

Enterprise Value via DCF (9.23)

V_0 = \dfrac{FCF_1}{1+r_{\text{wacc}}} + \dfrac{FCF_2}{(1+r_{\text{wacc}})^2} + \cdots + \dfrac{FCF_N + V_N}{(1+r_{\text{wacc}})^N}

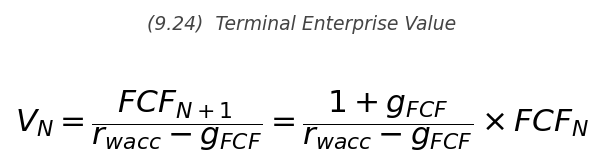

Terminal Enterprise Value — Constant FCF Growth (9.24)

V_N = \dfrac{FCF_{N+1}}{r_{\text{wacc}} - g_{FCF}} = \dfrac{FCF_N(1+g_{FCF})}{r_{\text{wacc}} - g_{FCF}}

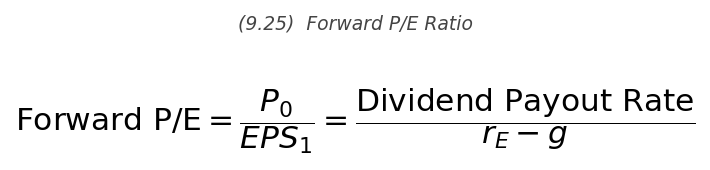

Forward P/E Ratio (9.25)

\text{Forward P/E} = \dfrac{P_0}{EPS_1} = \dfrac{\text{Dividend Payout Rate}}{r_E - g}

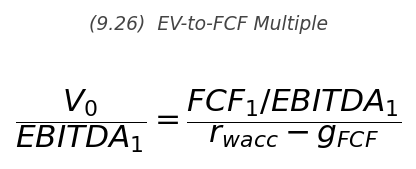

Enterprise Value-to-FCF Multiple (9.26)

\dfrac{V_0}{EBITDA_1} = \dfrac{FCF_1/EBITDA_1}{r_{\text{wacc}} - g_{FCF}}

Expected (Mean) Return (10.1)

E[R] = \displaystyle\sum_R p_R \cdot R

![<p>E[R] = \displaystyle\sum_R p_R \cdot R</p>](https://assets.knowt.com/user-attachments/42c1ff56-4815-44ba-a276-8ea1ccdd8537.png)

Variance of Returns (10.2)

\text{Var}(R) = \displaystyle\sum_R p_R \cdot (R - E[R])^2

![<p>\text{Var}(R) = \displaystyle\sum_R p_R \cdot (R - E[R])^2</p>](https://assets.knowt.com/user-attachments/f68d08cc-2b22-4d0b-8926-cb8768daa77e.png)

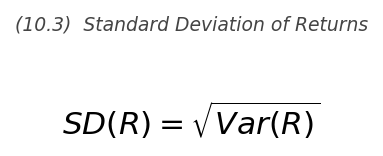

Standard Deviation of Returns (10.3)

SD(R) = \sqrt{\text{Var}(R)}

Annual Return from Quarterly Returns (10.5)

1 + R_{\text{annual}} = (1+R_{Q1})(1+R_{Q2})(1+R_{Q3})(1+R_{Q4})

Average Historical Return (10.6)

\bar{R} = \dfrac{1}{T}\displaystyle\sum_{t=1}^{T} R_t

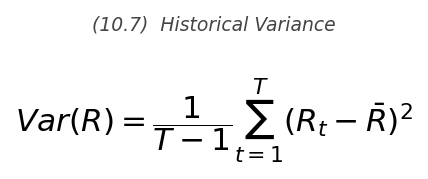

Historical Variance (10.7)

\text{Var}(R) = \dfrac{1}{T-1}\displaystyle\sum_{t=1}^{T}(R_t - \bar{R})^2

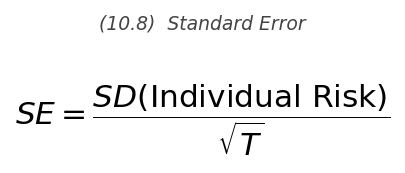

Standard Error of Expected Return Estimate (10.8)

SE = \dfrac{SD(\text{Individual Risk})}{\sqrt{T}}

95% Confidence Interval for Expected Return (10.9)

\bar{R} \pm 2 \times SE

Market Risk Premium (10.10)

\text{Market Risk Premium} = E[R_{\text{Mkt}}] - r_f

![<p>\text{Market Risk Premium} = E[R_{\text{Mkt}}] - r_f</p>](https://assets.knowt.com/user-attachments/97abc520-ec61-4699-a521-9fbadd7c66f3.png)