Econ 201 Final

1/69

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

70 Terms

Production Function

The maximum amount of output that a firm can produce with a given quantity of inputs and for a given state of technology

Law of Diminishing Returns

If we vary 1 of the inputs, keeping all other inputs as well as the technological level constant, then, at least after some point, successive additional units of the variable input will add less and less to the Total output

Short Run

A period of time in which only the variable inputs, such as labor and materials, could be adjusted

Can distinguish between fixed and variable costs

Long Run

A period of time in which all inputs, including fixed factors, such as capital, could be adjusted

All costs are variable

Assuming that firms produce efficiently

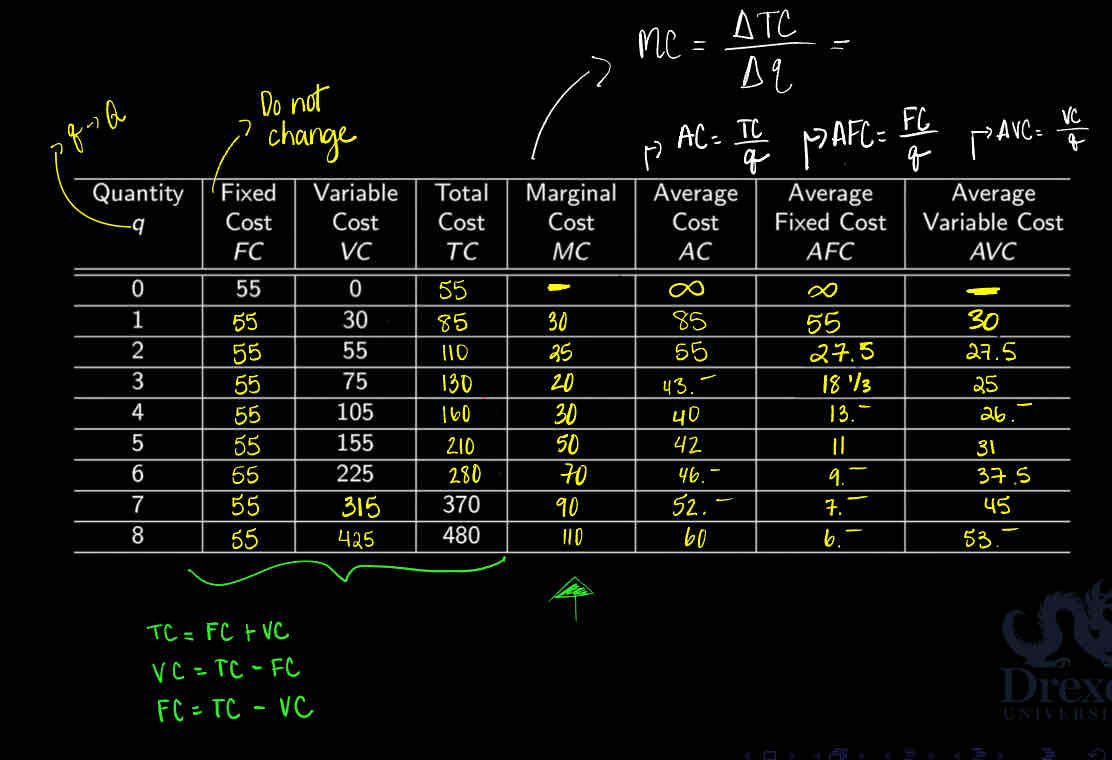

Total Cost [TC]

Represent the total amount of $ spent, in all the inputs required for a business firm in order to produce a given level of output

Assuming that firms produce efficiently

Fixed Costs [FC]

Costs that the firm has to pay even if it doe snot produce anything

Do not depend on the level of output produced

Assuming that firms produce efficiently

Variable Costs [VC]

Costs that vary and are directly related to output

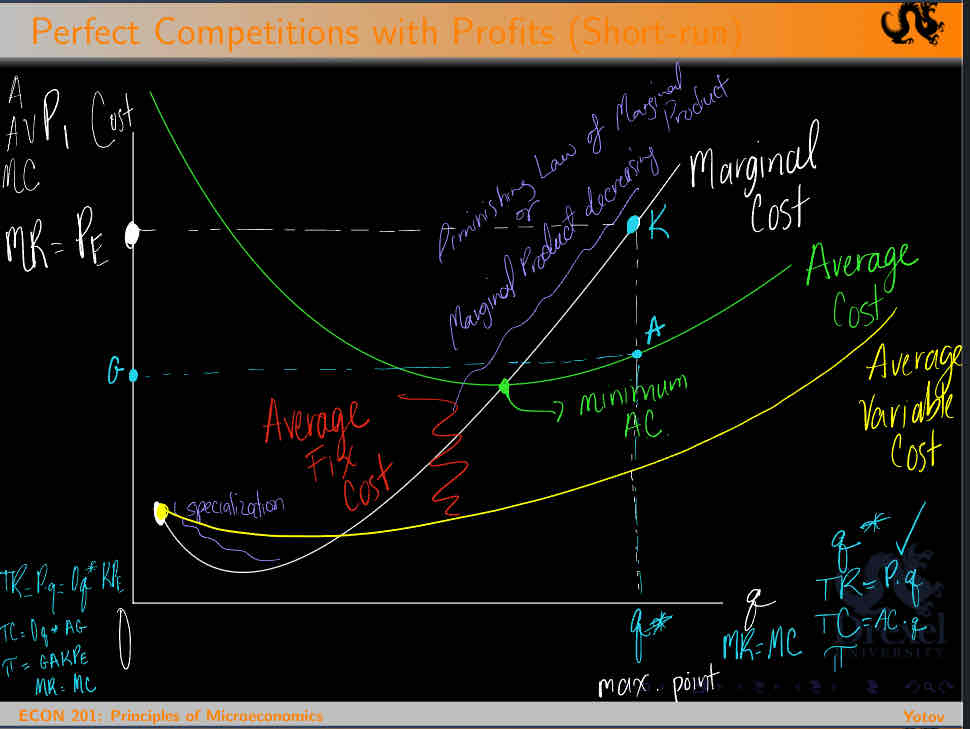

Marginal Cost — MC

Economists definition

The additional expenditure that a firm has to incur in order to produce 1 more unit of output

Average Cost — AC

The ratio between the Total Cost and the quantity produced

AC= TC/Q

Average Fixed Cost — AFC

The ratio between fixed costs and quantity of output produced

AFC = FC/Q

Average Variable Cost

The ratio between variable costs and quantity of output produced

AVC = VC/Q

Perfect Competition

A market setting involving large number of profit maximizing firms that sell a homogeneous product

Cannot individually affect the market price

Free entry and exit are assumed

Perfectly Competitive Firm

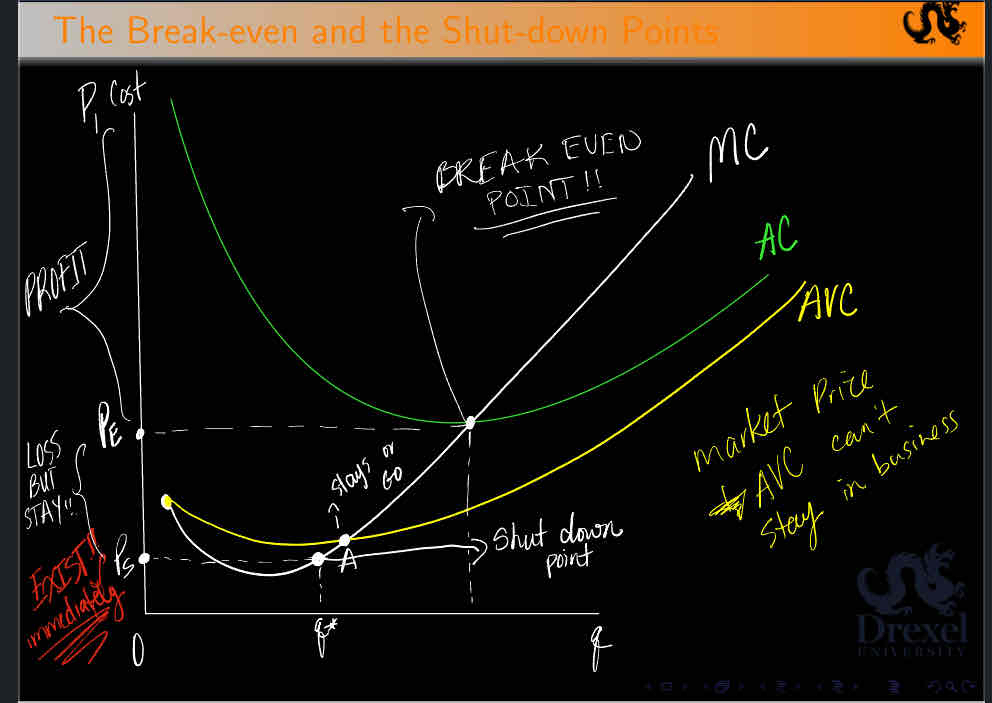

Will maximize its profit when it produce at the level where Marginal Cost = Market Price

MC = P = MR

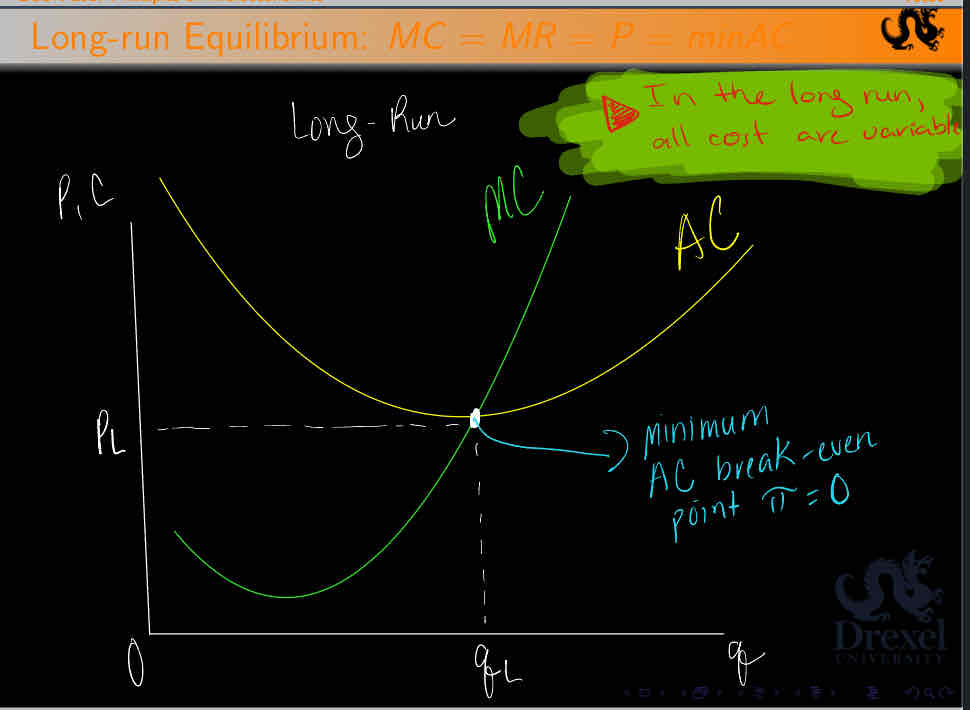

Perfect Competition in the long run

The economic profit realized by each of the large number of identical firms operating in a perfectly competitive market setting w/ free entry and exit will be zero.

The market price will be equal to both the marginal cost and the long - run-minimum-average-cost

MR = P = MC = min AC

Imperfect Competition

Prevails in an industry where individual sellers have some control over the price of their output

Monopoly

Exists when a single firm is the sole producer of a product for which there are no close substitutes

Entry in the industry is blocked

Monopolistic Competition

market structure

A market structure in which a relatively large number of sellers offer similar but not identical products

Entry is easy

Large # of small firms

Differentiated products —> ability to affect price

Entry and exit are easy

Oligopoly

Exists where a few large firms producing a homogeneous or differentiated product dominate a market

These producers are interdependent in their profit-maximizing decisions

Hard to enter their industry

Cartel

A group of producers that creates a formula written agreement specifying how much each member will produce and charge

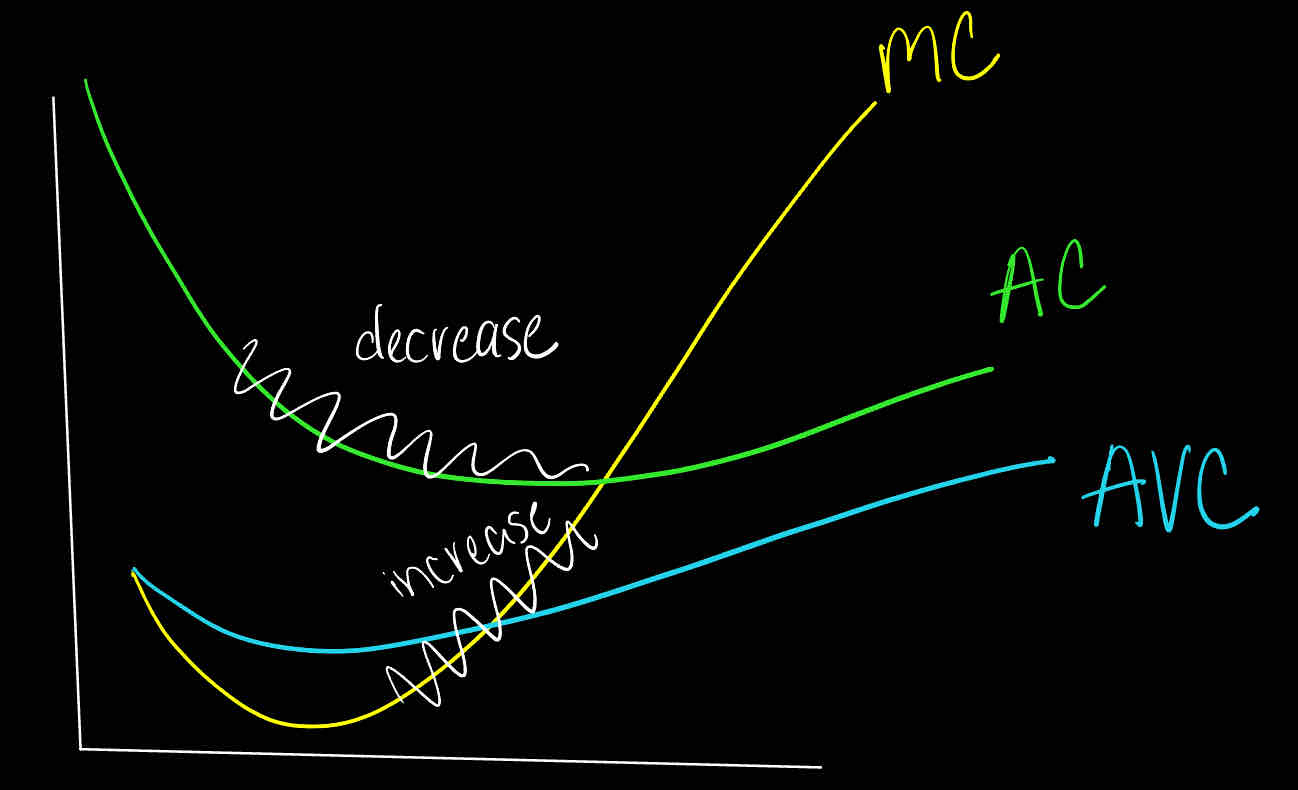

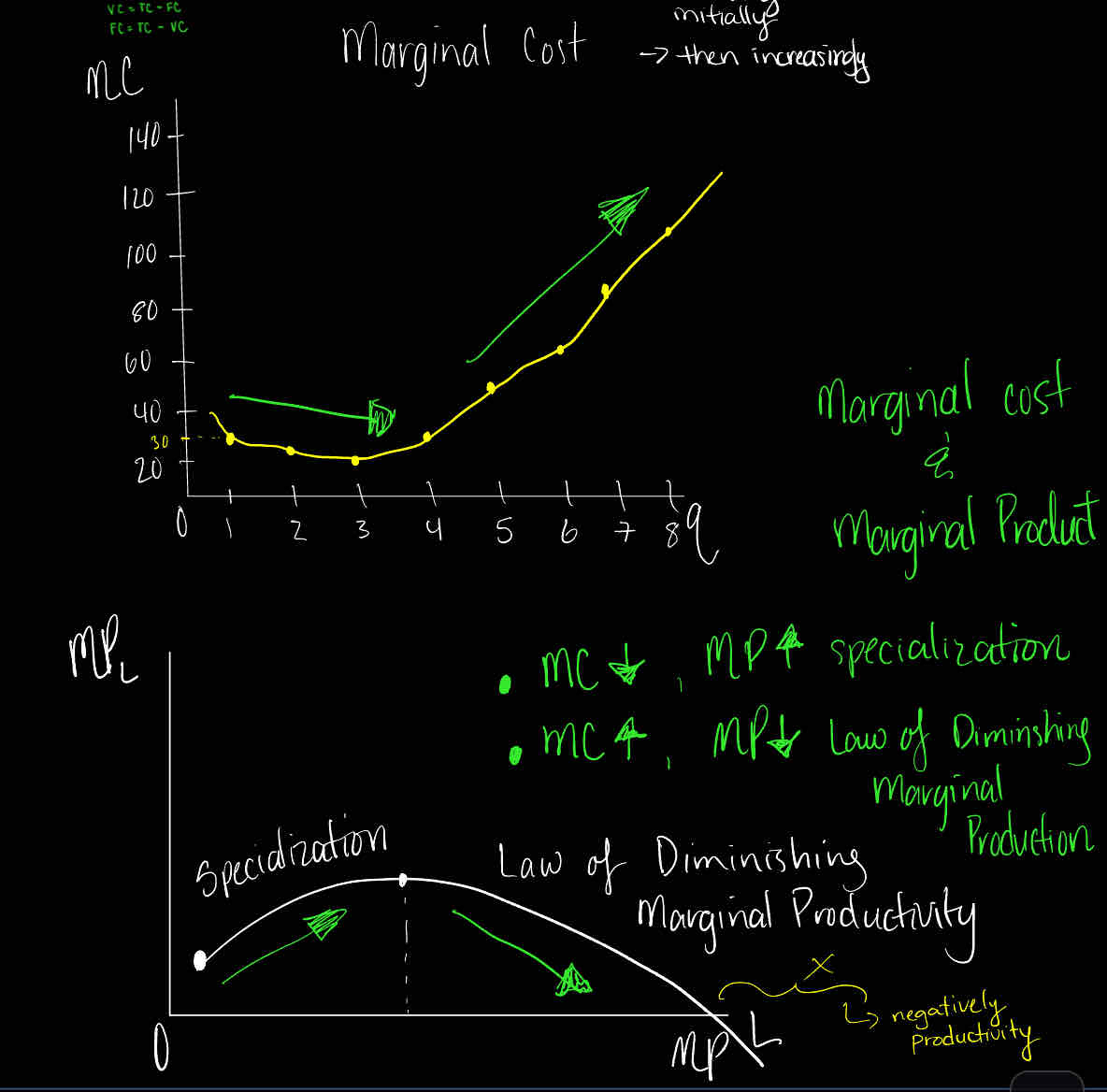

Marginal Cost decreases at the early stages of production because Marginal Product is increasing

True

False

True

When production reaches a certain point, Marginal Cost will start increasing because of the Law of Diminishing Returns

True

False

True

Marginal Cost increases at the early stages of production because of Specialization.

True

False

False

MC decrease first then increase

When output approaches zero, Average Cost approaches infinity because of fixed costs

True

False

True

Increasing marginal cost implies increasing average cost

True

False

False

increasing MC means that AC can still have the possibility to be in the decreasing stage

Marginal Cost below Average Cost implies decreasing Average Cost

True

False

True

The supply curve for the perfectly competitive firm is the segment of its Marginal Curve that is above the shut down point

True

False

True

Perfect competitive firms will make zero profits in the long run because of free/easy entry and exit in the perfectly competitive industry

True

False

True

If perfectly competitive firms make profits in the short run, then new firms will enter this industry, and there will be zero economic profits in the long run

True

False

True

If perfectly competitive firms make profits in the short run, then new firms will enter this industry, and there will be positive economic profits in the long run

True

False

False

The marginal revenue for a perfectly competitive firm is always equal to the market price

True

False

True

MR = P = MC

In order to maximize profits, a perfectly competitive form should produce where its marginal cost is equal to its marginal revenue

True

False

True

Which of the following is NOT a distinct feature of monopolistic competition:

Downward-slopping demand ⭐️

Differentiated products

No substitutes

Easy entry & exit

Many firms

No substitutes

Zero economic profit for a firm in the long-run indicates that firm could be:

Monopoly

Perfectly competitive

Small

Large

All of the above

All of the above

You know that for a monopolist MR=$7 and MC=$14 when the output produced by the firm is 12. Which of the following is true if the firm is a profit-maximizer?

The firm is making the right production decision

The firm should produce less than 12

The firm should produce more than 12

There is no sufficient information to decide whether to produce more or less

The firm should leave the industry since MR<MC

The firm should produce less than 12

If prices fall in a perfectly competitive industry, then the firms in that industry will in the short run:

Produce more and increase in number

Reduce production or shut down

Keep output at the same level but make losses

Produce more and decrease in number

Both A and B

Reduce production or shut down

Which of the following statements is incorrect?

AC bellow MC implies rising AC

My below AC implies falling AC

MC rising implies AC rising

AC falling implies MC below AC

AFC is always falling with output

MC rising implies AC rising

True or False

A monopolist will produce when the price of her product is equal to her marginal cost

P = MR = MC

False

True or False

A perfectly competitive will produce when the price of her product is equal to her marginal cost

True

True or False

Marginal Cost decrease at the early stages of production because of Specialization

True

True or False

Free entry into a monopolistic ally competitive industry shifts each firm’s downward sloping demand curve far enough to eliminate all profits in the long run

True

True or False

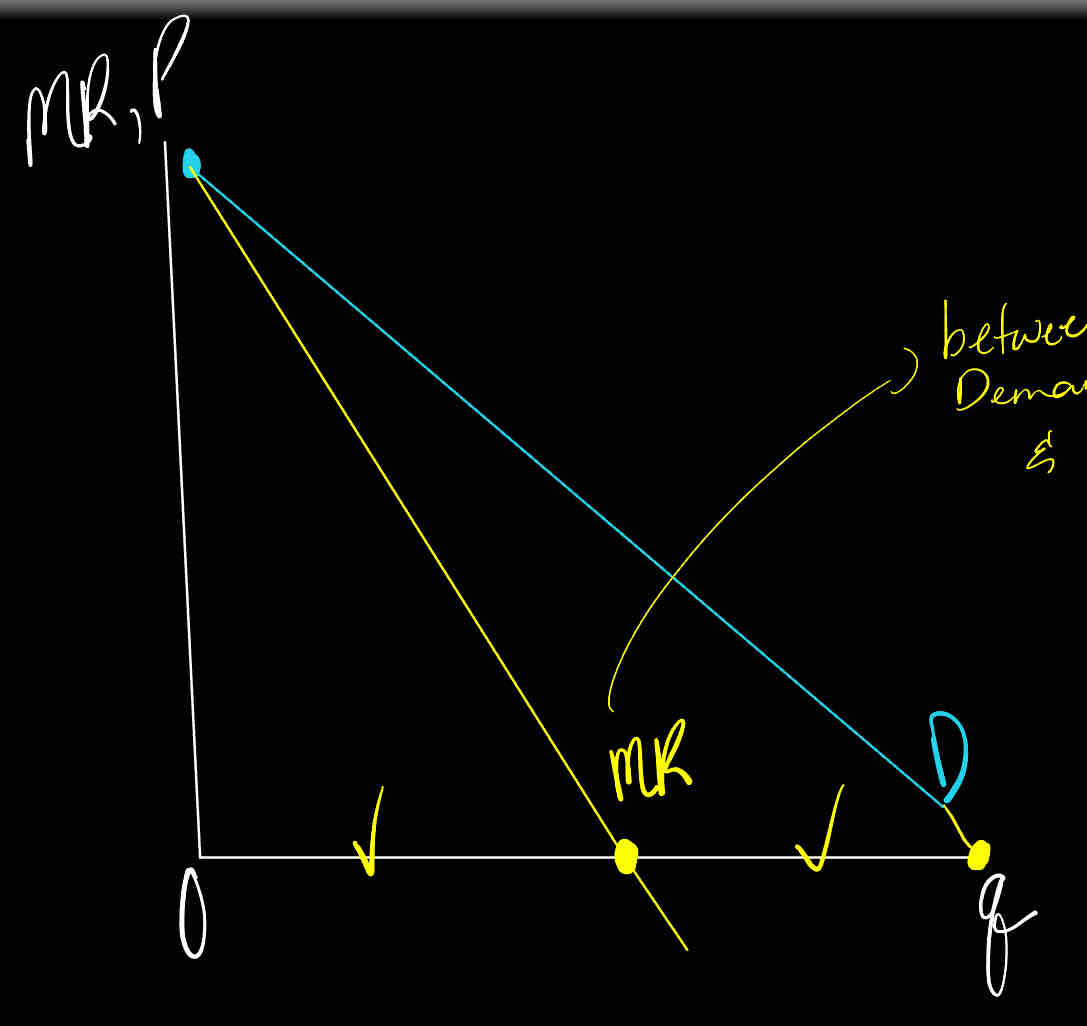

For the first unit sold, and only for the first unit sold, the marginal revenue for an imperfectly competitive firm is equal to its price

True

True or False

The biggest disadvantage of corporation is that they do not alway pay profits to their shareholders

False

True or False

The biggest disadvantage of corporations is that they have 3 taxations

True

True or False

If marginal cost is increasing, then average cost must be increasing too

False

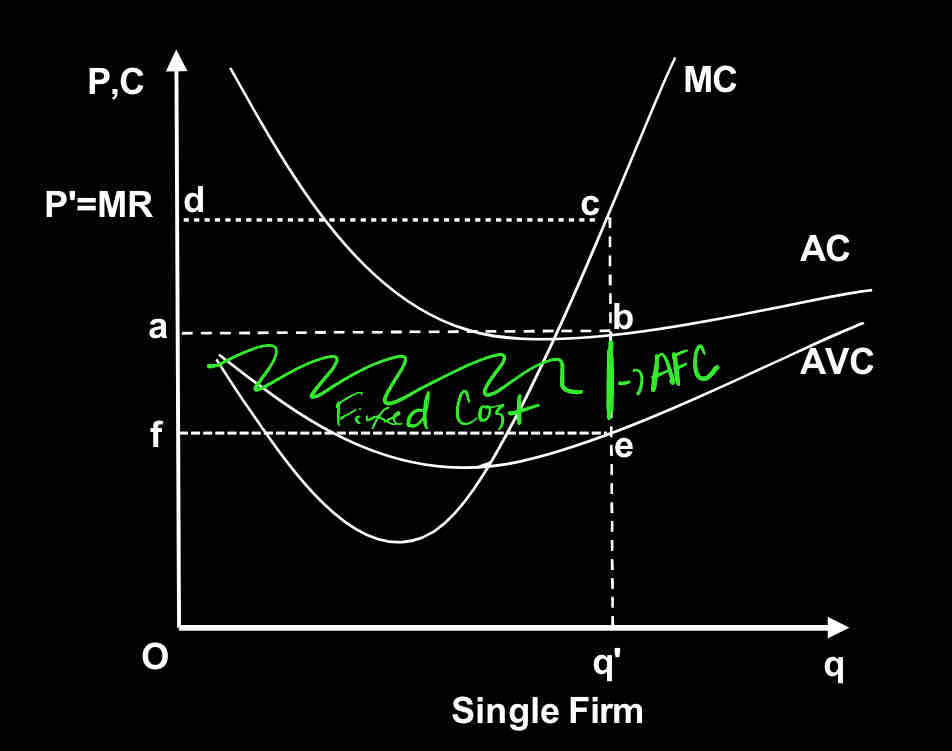

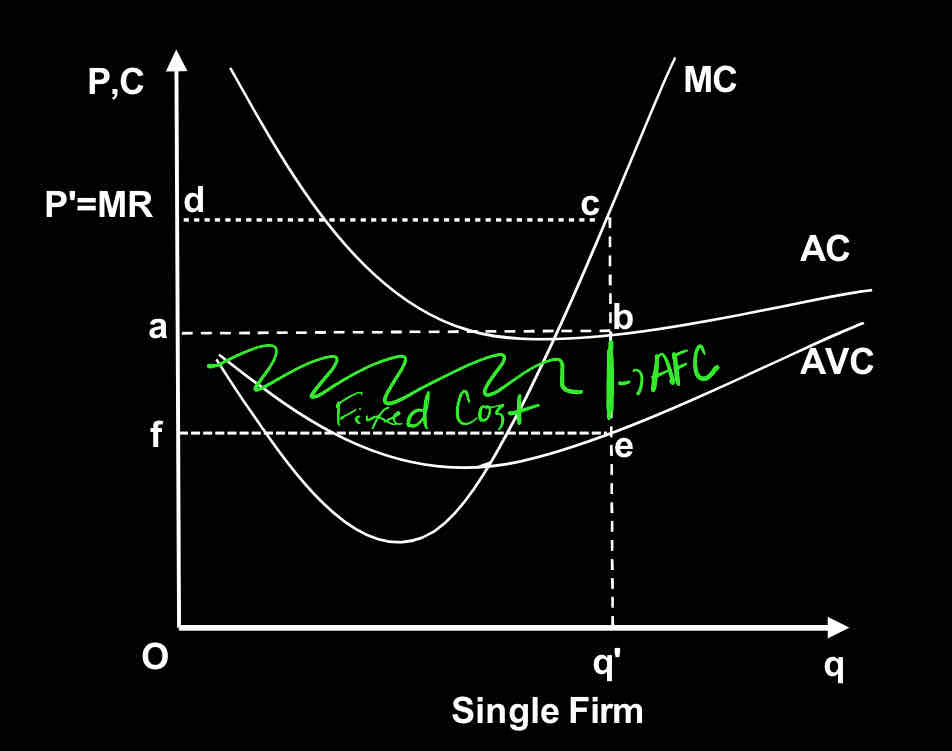

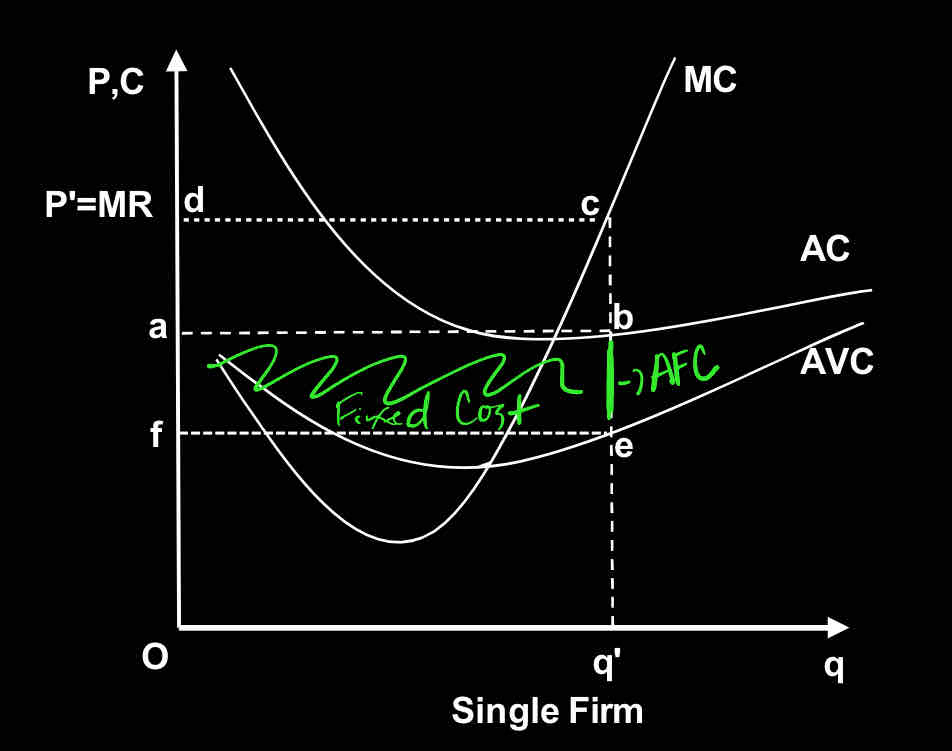

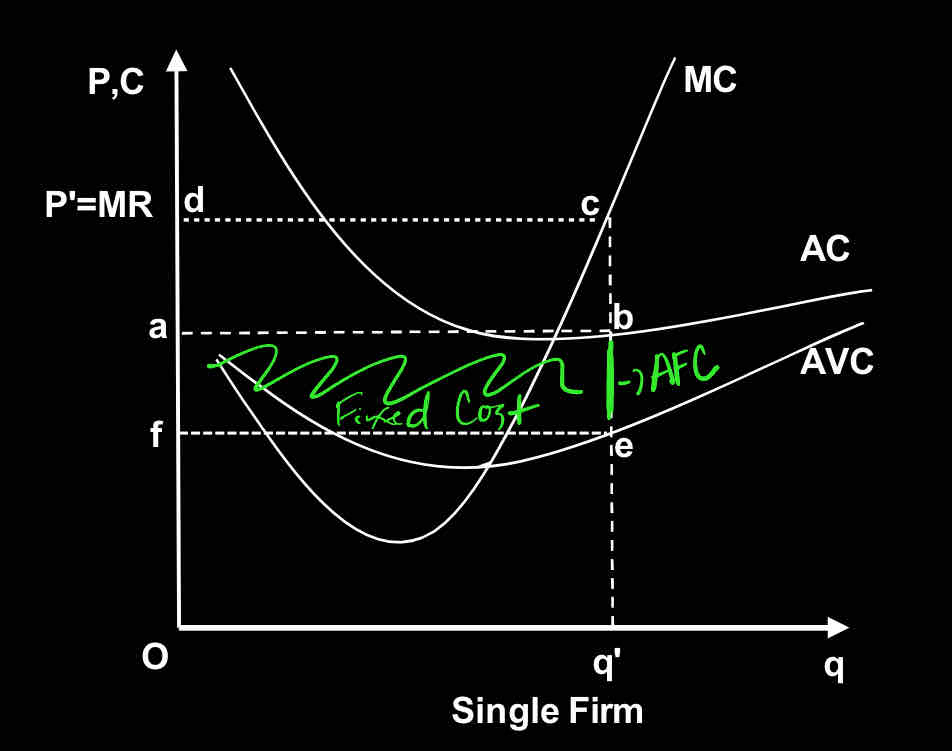

Use the graph:

The figure represents profit-maximization in:

Perfect competition

Monopolistic competition

Oligopoly

Monopoly

Perfect competition

Use the graph:

Total profit / loss (choose one) for the firm is represented by the area:

feba

Oa

Oq’ba

eb

abcd

abcd

Use the graph:

Segment ‘be’ represent

Average cost

Average fixed costs

Average variable costs

Fixed cost

Variable cost

Average fixed costs

Use the graph:

Area ‘feba’ represents:

Average cost

Average fixed costs

Average variable costs

Fixed cost

Variable cost

Fixed cost

Individual proprietorships

small

Many 80-85%

Unlimited liability

Partnerships

small

Not popular = not too many 5-10%

Unlimited liability

Corporations

forms of business organizations chartered as a ‘legal person’ by 1 of the 50 states or abroad and owned by shareholders who have contributed money, time, ideas, or other resources in exchange for stocks

Large

Small number

Limited liability

Advantages

Size

Scale

Innovation

Disadvantages

Triple taxation

Corporate

State

Dividend

Π [pie] represent

Profit

Fixed Costs — FC

Sunk or overhead costs

Costs that the firm has to pay even is it does not produce anything

Do not depend on the level of output

Variable Costs — VC

costs that are vary with and are directly related to output

Such as : materials and enegry

Use the table:

Does fixed cost stay the same?

Yes

Total Cost = _______ + _______

Fixed costs + variable costs

Variable cost = _________ - ________

Total cost - fixed cost

Fixed cost = _______ - _______

Total cost - variable cost

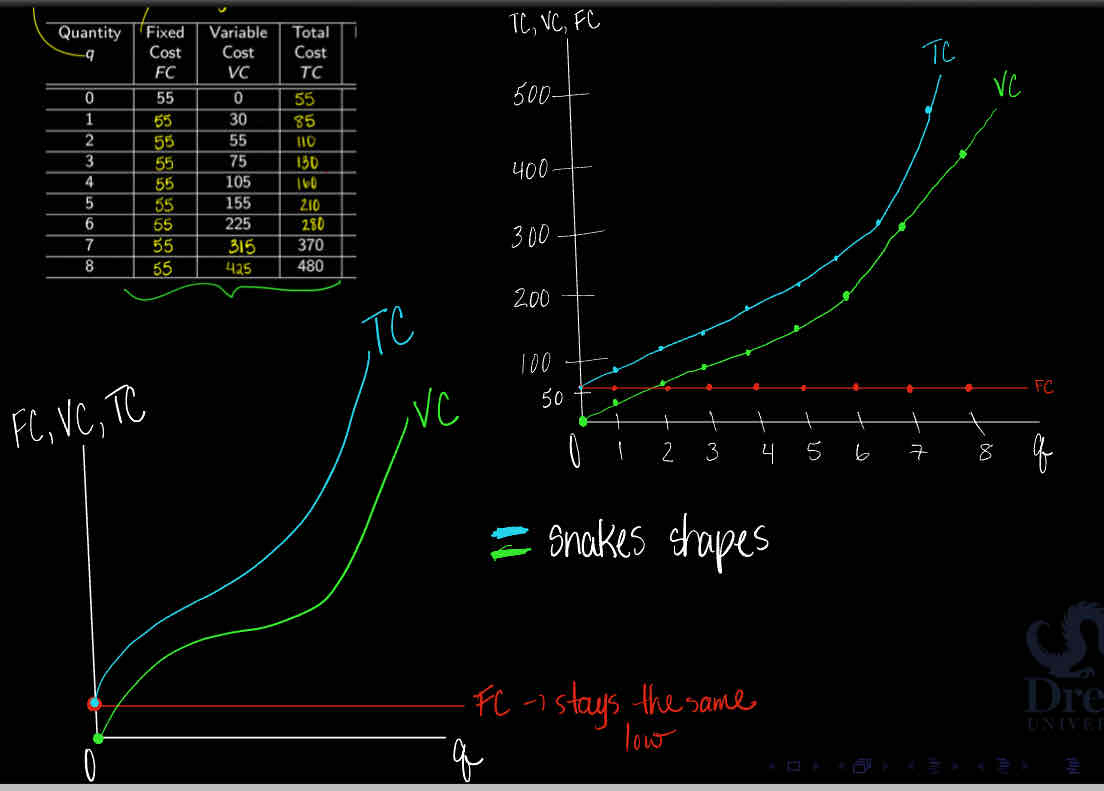

What is the relationship between FC, VC, TC?

Look at the graph

TC and VC are like snake shapes ; will ø intersect due to fixe cost

Fix cost stays the same ; low

What is the relationship between Marginal Cost and Marginal Product?

Look at the graph:

MC down , MP up = specialization

MC up , MP down = Law of Diminishing Marginal Production

Forms of imperfect competition:

Monopolistic competition

Oligopoly

Monopoly

Perfect Competition characteristics

Large number of profit-maximizing producers

Homogeneous product

Each firm is a price taker

Free entry and exit = easy

Perfect Competition with Profits

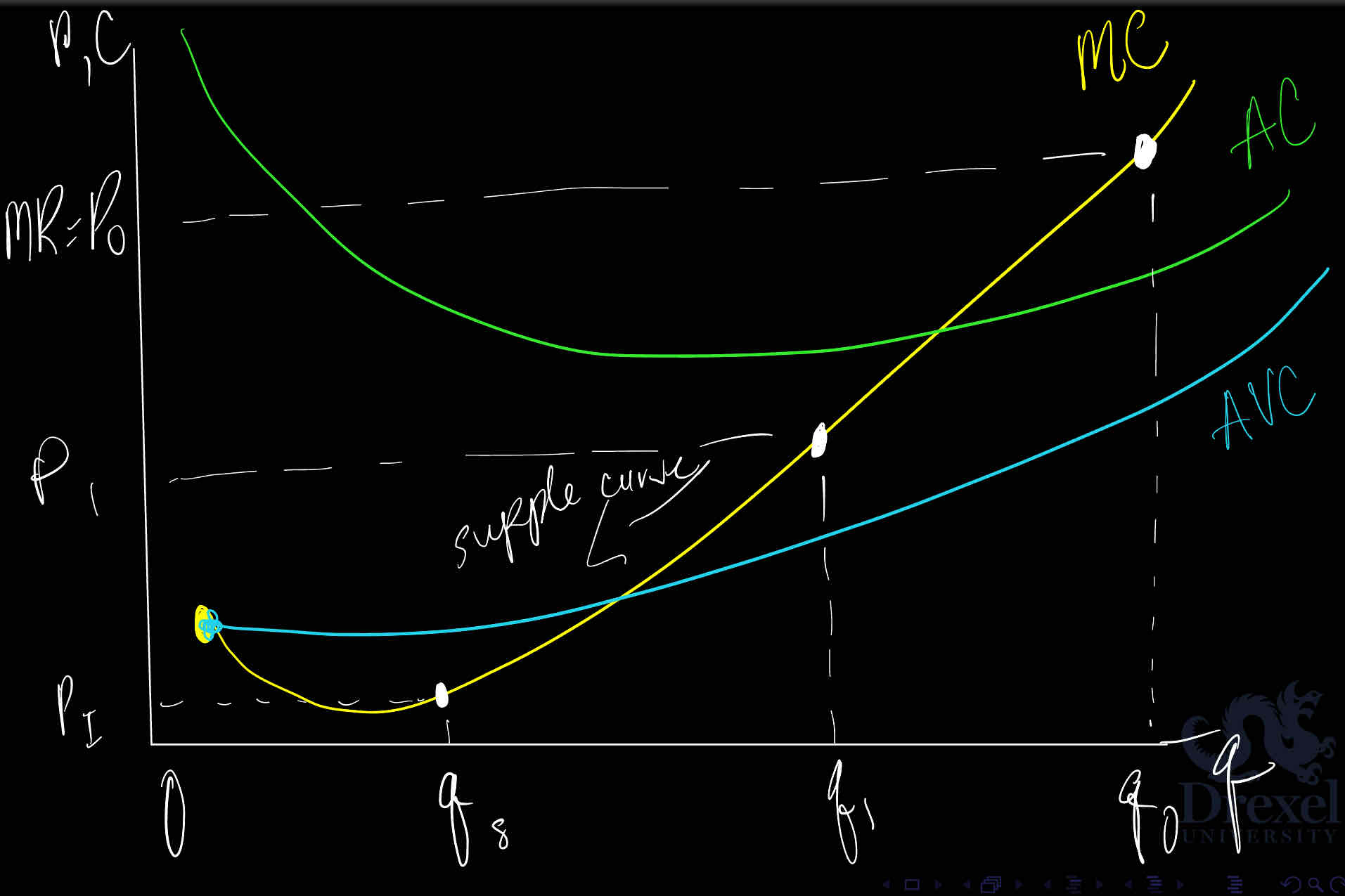

Short run

Look at graph

Perfect Competition Long Run

Look at graph

MC and AC

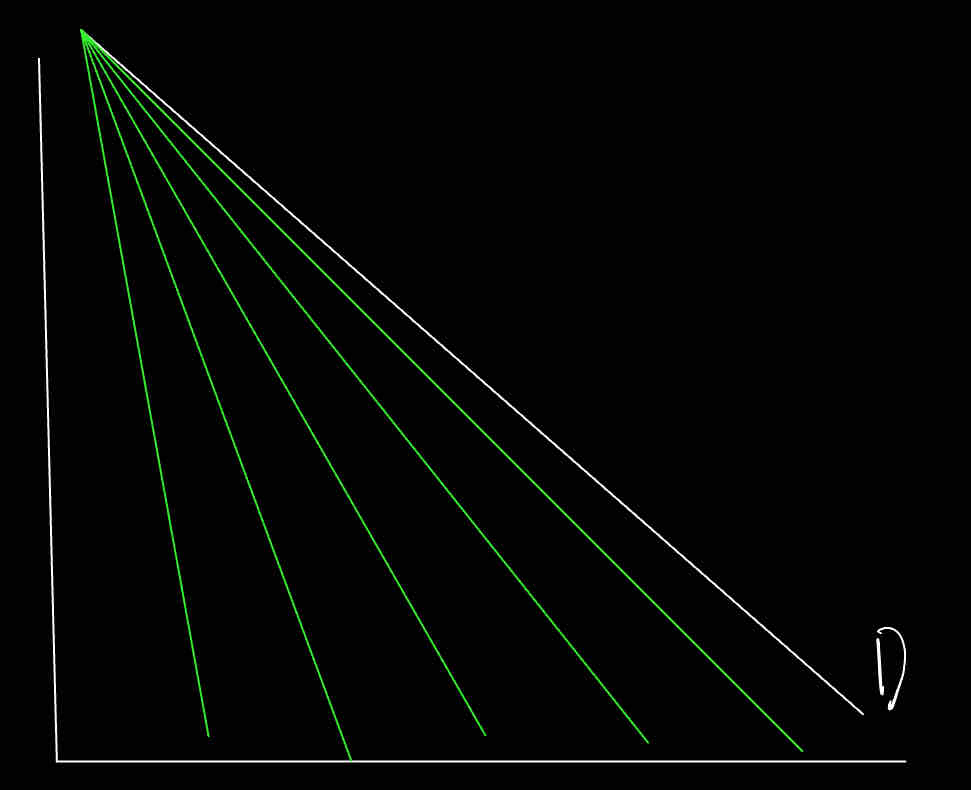

When new firm enters in an imperfect competition the demand for the existing firm(s) decrease and becomes more elastic

True or False

True

Imperf

For imperfect competition,

with profits = demand curve is above the minimum AC

With losses = demand curve is below the minimum AC

Look at the graph

Oligopoly characteristic

Differentiated and Homogeneous products

Internal growths vs. Mergers

Barriers to entry

Price-makers

Relatively stable price

Perfect Competition Break-Even and Shut dow points

Look at the graph