Investment Banking Interview Prep: WSP RedBook (Accounting)

1/115

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

116 Terms

What is the primary purpose of U.S. GAAP?

U.S. GAAP serves as a set of guidelines that ensures financials are prepared fairly on a consistent basis for investors and lenders. GAAP is issued by the Financial Accounting Standards Board (FASB) which is issued under the SEC.

What are the primary sections of a 10K?

The primary sections of the 10K include:

- the business overview which shows items like strategy, risks, and divisions

- management discussion and analysis which gives commentary and summarizes the companies fiscal year results

- the financial statements (3 core: IS, BS, CFS & 2 others: statement of comprehensive income, shareholders equity)

- footnotes which gives disclosures on the financial statement about specific details

What is the difference between the 10K and 10Q?

The 10K is an annual report which includes an in-depth look at management commentary, financial statement, and business overview. The 10Q is a quarterly report which tends to be more vague but include many of the sections on the 10K. 10Ks must be audited by an external auditor but 10Qs are only reviewed by CPAs and unaudited. 10Ks can be filled out 60-90 days post period, while 10Qs are can be filled out 40-45 days post period.

Walk me through the 3 financial statements.

- The income statement shows a companies profitability over a given period. The beginning line is revenue and upon deductions such as COGS the ending line is net income.

- The balance sheet is a snapshot of a companies assets and funding (liabilities & equity) at a specific point in time.

- The cash flow statement under the direct approach starts with net income which will be adjusted for non-cash items such as D&A and changes in working capital to arrive at the net change in cash, which represents the actual cash inflow/outflow in a given period.

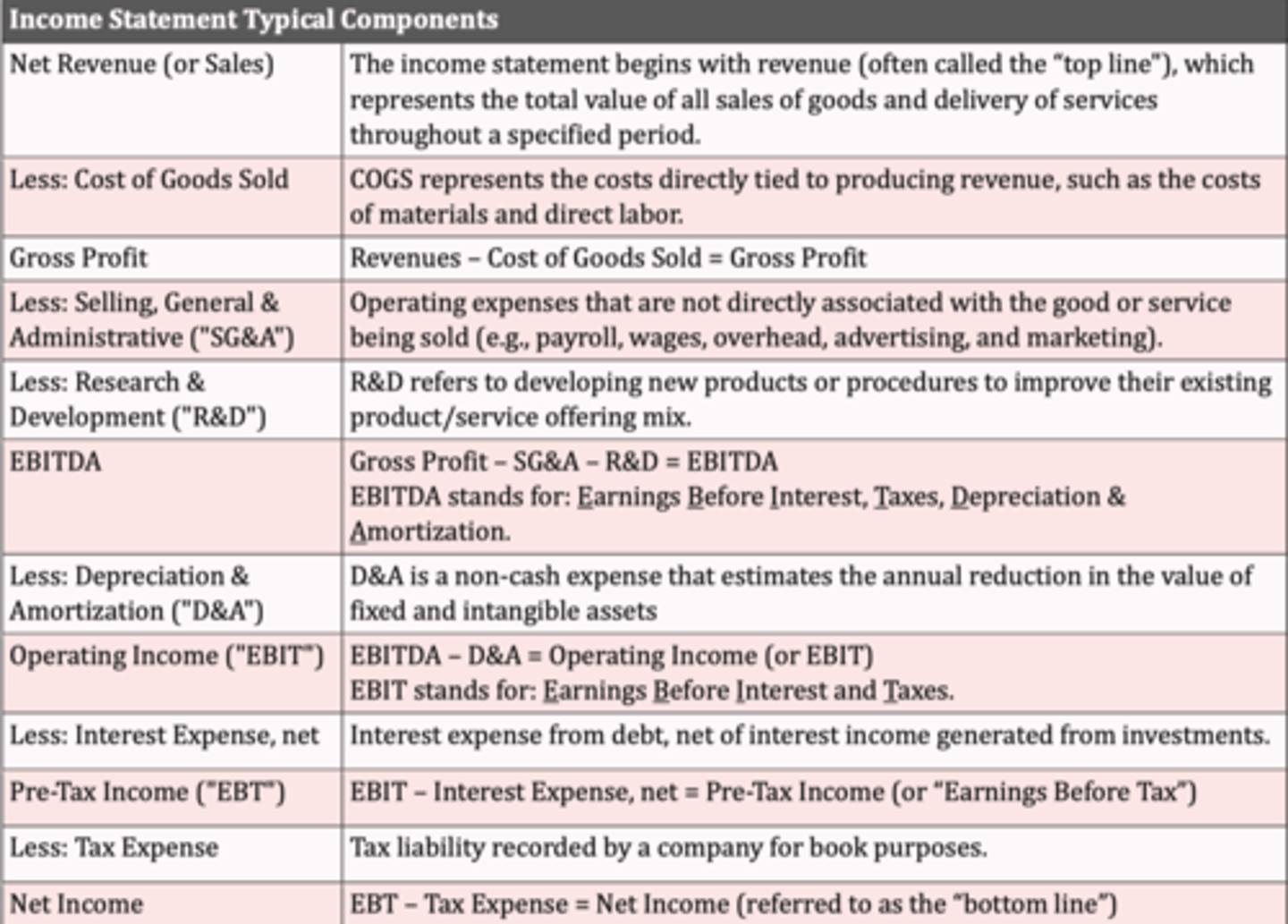

Walk me through the income statement.

The income statement shows a companies accrual based profitability over a given period and facilitates the analysis of historical growth/performance. A traditional income statement starts with revenue then subtracts COGS and gets to gross profit, then subtracts SG&A and R&D which gives EBITDA, then subtracts D&A to get EBIT (Operating Income) then subtracts interest expense to get EBT (Pre-Tax Income) then subtracts Taxes to get Net Income

Walk me through the balance sheet.

The balance sheet shows a companies assets, liabilities, and equity sections at a point in time. Assets = liabilities + equity. The assets for a company must be funded somehow so assets will always equal this.

Assets: assets are organized in order of liquidity with current assets as the first listed. This refers to assets that can be converted to cash within a year. Examples are: cash, marketable securities, AR, Prepaid expenses, inventories. Long term assets come next which include: PP&E, intangible assets, goodwill.

Liabilities: liabilities are listed in order of when they're due. Current liabilities include: AP, Accrued expenses, short term debt. Long term debt includes: deferred revenue and long-term debt.

Shareholders Equity: consists of common stock, additional paid-in capital, treasury stock, and retained earnings.

Could you give further context on what assets, liabilities, and equity each represent?

Assets: resources with economic value that can bring positive monetary benefit in the future. For example PP&E is used to generate cash flows in the future and AR are payments due from customers which both represent inflows of cash.

Liabilities: unsettled obligations to another party in the future and represent external sources of capital from third-parties which help fund company assets. Liabilities represent future cash outflows.

Equity: capital invested in the business and represents internal sources of capital that help fund assets, this could come from self-funding or institutional investors. accumulated net profits over time will be shown as retained earnings.

Walk me through the cash flow statement.

The cash flow statement can be organized in two methods, indirect or direct. The more common approach is indirect which is broken into 3 sections: Cash from operation, Cash from Investing, and Cash from financing. Together the sum of the three sections will be the net change in cash for the period. This will then be added to the beginning of period cash balance to arrive at ending cash balance.

Cash from operations: starts with net income and adds back non-cash expenses such as D&A and Stock-Based Compensation, then makes adjustments for changes in working capital

Cash from investing: Cash from investing section accounts for capital expenditures, followed by any business acquisitions or divestitures.

Cash from financing: shows the net impact of raising capital from issuances of equity or debt, net of cash used for share repurchases, and repayments of debt. Cash outflows from the payout of dividends will be reflected here as well.

How are the three financial statements connected?

IS<->CFS: CFS is connected to IS through net income, as net income is the starting line on CFS.

CFS<->BS: Linked because CFS tracks the BS changes in working capital (current assets and liabilities). The impact from capital expenditures (PP&E), debt or equity issuances, and share buybacks (treasury stock) are also reflected on the balance sheet. Also cash balance at bottom of CFS flows onto balance sheet.

IS<->BS: Connected through retained earnings (RE). Net income - Dividends issued during the period will be added to the prior periods RE balance to calculate new RE. Interest expense on the IS is also calculated off the beginning and ending debt balances on the BS, and PP&E on the BS is reduced by D&A on the IS.

If you have a balance sheet and must choose between the income statement or cash flow statement, which would you pick?

If given the beginning and ending period balance sheets, I would choose the income statement since I could reconcile the cash flow statement using the balance sheet's year-over-year changes along with the IS.

Which is more important, the income statement or cash flow statement?

Both are necessary for in-depth analysis, but CFS is arguably more important because it reconciles net income, the accrual-based bottom line on the IS to what is actually occuring to cash. This means the actual movement of cash during the period is reflected on the CFS, thus the CFS brings attention to liquidity-related issues and investments and financing activities that don't show up on the accrual-based IS.

If you had to pick between either the income statement or cash flow statement to analyze a company, which would you pick?

In most cases the CFS would be chosen because it shows a companies true liquidity and is not prone to the discretion that is used in the accrual-based IS. Whether an investor or lender, a companies ability to generate sufficient FCF to reinvest in operations and pay debt is most important.

One factor that could switch the answer is the companies profitability. For an unprofitable company, the IS can be used to value based on a revenue multiple. The cash flow statement becomes less useful for valuation purposes if the company's net income, cash from operations, and FCF are all negative.

Why is the income statement insufficient to assess the liquidity of a company?

The IS can be misleading in portrayal of a companies health from a liquidity and solvency standpoint. For example a company could have positive net income but struggle to retrieve payments from customers via credit and it wouldn't show up on the IS. Accrual based accounting allows for wiggle room which can skew depiction of a companies operational performance. The solution to the shortcomings is the CFS which reconciles net income based on real cash flows to understand the true impact from operations, investing, and financing activities over a period.

What are some discretionary management decisions that could inflate earnings?

- Using excess useful life assumptions for new capital expenditures to reduce the annual depreciation

- Switching from LIFO to FIFO if inventory costs are expected to increase, resulting in higher net income

- Refusing to write-down impaired assets to avoid the impairment loss, which would reduce net income

- Changing policies for costs to be capitalized rather than expensed (e.g., capitalized software costs)

- Repurchasing shares to decrease its share count and artificially increase earnings per share ("EPS")

- Deferral of capex or R&D to the next period to show more profitability and cash flow in the current period

- More aggressive revenue recognition policies in which the obligations of the buyer become less stringent

Tell me about the revenue recognition and matching principle used in accrual accounting.

Revenue Recognition Principle: Revenue is recorded in the same period the good or service was delivered, whether or not cash was collected.

Matching Principle: The expenses associated with the production/delivery of a good or service must be recorded in the same period as when the revenue was earned.

How does accrual accounting differ from cash-basis accounting?

Accrual Accounting: Revenue recognition is based on when it's earned and the expenses associated with that revenue are incurred in the same period.

Cash-Bases Accounting: Cash is recorded when it is collected by the company and expenses are recorded when the company spends the cash. Example: inventory is bought and delivered in a prior period and then collected in a later period results in different period recognition for costs and revenue.

What is the difference between cost of goods sold and operating expenses?

COGS: direct costs associated with the production of the goods sold or the delivery of services to generate revenue. Examples include direct material and labour costs.

Operating Expenses: Expenses such as SG&A and R&D are not directly associated with the production of goods or services offered. Often called indirect costs, examples include rent, payroll, wages, commissions, advertising and marketing expenses.

When do you capitalize vs. expense items under accrual accounting?

The factor that determines whether an item gets capitalized as an asset or expensed in the period incurred is its useful life.

Capitalized: Expenditures on fixed and intangible assets expected to benefit the firm for more than one year need to be capitalized and expensed over time. For example, PP&E such as a building can provide benefits for 15+ years and is therefore depreciated over its useful life.

Expensed: In contrast, when the benefits received are short-term, the related expenses should be incurred in the same period. For example, inventory cycles out fairly quickly within a year and employee wages should be expensed when the employee's services were provided.

If depreciated is a non-cash expense, how does it affect income?

While depreciation is treated as non-cash and an add-back on the cash flow statement, the expense is tax-deductible and reduces the tax burden. The actual cash outflow for the initial purchase of PP&E has already occurred, so the annual depreciation is the non-cash allocation of the initial outlay at purchase.

Do companies prefer straight-line or accelerated depreciation?

GAAP reporting companies prefer straight-line because lower depreciation will be recorded in the earlier years of the asset's useful life than under accelerated depreciation. Companies show higher net income and EPS in the initial years this way. Eventually accelerated depreciation will show less depreciation but many companies are worried about near-term earnings. If a company is consistently acquiring new assets, the "flip" won't occur until the company significantly scales back capital expenditures.

What is the relationship between depreciation and the salvage value assumption?

Most companies assume a salvage value of 0 by the end of an assets life. If the salvage value is 0, the depreciation expense each year will be higher and the tax benefits from depreciation will be fully maximized. D = (Cost-Salvage)/Useful Life

Do companies depreciate land?

While classified as a long-term asset on the balance sheet, land is assumed to have an indefinite useful life under accrual accounting, and therefore depreciation is prohibited.

How would a $10 increase in depreciation flow through the financial statements?

Depreciation will be embedded on the COGS or operating expenses line of the income statement.

IS: when depreciation goes up by $10, taxable income (EBIT) goes down by $10 and net income is decreased by $7 if a 30% tax rate is assumed.

CFS: $10 will be added back in operating cash flow as it is non-cash expense. Net change on ending balance cash is +$3 as net income goes down by 7.

BS: PP&E will decrease by $10 from depreciation, while cash will be up by $3 on the asset side. On the L&E side, a $7 reduction in net income flows through retained earnings. The balance sheet remains in balance as both sides went down by $7.

A company acquired a machine for $5 million and has since generated $3 million in accumulated depreciation. Today, the PP&E has a fair market value of $20 million. Under GAAP, what is the value of that PP&E on the balance sheet?

$2 million, except for certain liquid financial assets that can be written up to reflect there FMV, companies must carry the value of assets at their net historical cost.

Under IFRS, the revaluation of PP&E to fair value is permitted. Even though permitted, it's not widely used and thus not even well known in the US.

What is the difference between growth and maintenance capex?

Growth Capex: The discretionary spending of a business to facilitate new growth plans, acquire more customers, and expand geographically. Throughout periods of economic expansion, growth capex tends to increase across most industries (and the reverse during an economic contraction).

Maintenance Capex: The required expenditures for the business to continue operating in its current state (e.g., repair broken equipment).

Which types of intangible assets are amortized?

Amortization is based on the same accounting concept as depreciation, except it applies to intangible assets rather than fixed tangible assets such as PP&E. Intangible assets include customer lists, copyrights, trademarks, and patents, which all have a finite life and are thus amortized over their useful life.

What is goodwill and how is it created?

Goodwill represents an intangible asset that captures the excess of the purchase price over the fair market value of an acquired business's net assets.

Suppose an acquirer buys a company for a $500 million purchase price with a fair market value of $450 million. In this hypothetical scenario, goodwill of $50 million would be recognized on the acquirer's balance sheet.

Can companies amortize goodwill?

Under GAAP, public companies are prohibited from amortizing goodwill as it's assumed to have an indefinite life, similar to land. Instead, goodwill must be tested annually for impairment.

However, privately held companies may elect to amortize goodwill and under some circumstances, goodwill can be amortized over 15 years for tax reporting purposes.

What is the "going concern" assumption used in accrual accounting?

In accrual accounting, companies are assumed to continue operating into the foreseeable future and remain in existence indefinitely. The assumption has broad valuation implications, given the expectation of continued cash flow generation from the assets belonging to a company, as opposed to being liquidated.

Explain the reasoning behind the principle of conservatism in accrual accounting.

The principle of conservatism stats that accountants shall use caution when preparing financial statements by using downward measurement bias. This means that it is generally better to understate assets and vice-versa with liabilities and equity. This leads to less risk of faulty accounting/company inflation that could mislead investors.

Why are most assets recorded at their historical cost under accrual accounting?

The historical cost principle states that an asset's value on the balance sheet must reflect the initial purchase price, not the current market value. This guideline represents the most consistent measurement method since there's no need for constant revaluations and markups, thereby reducing market volatility.

What role did fair-value accounting have in the subprime mortgage crisis?

In the worst-case scenario, sudden drops in asset values could cause a domino effect in the market. An example was the subprime mortgage crisis, in which the meltdown's catalyst is considered to be FAS-157. This mark-to-market accounting rule mandated financial institutions to update their pricing of illiquid securities. Soon after, write-downs in financial derivatives, most notably credit default swaps ("CDS") and mortgage-backed securities ("MBS"), ensued from commercial banks, and it was all downhill from there.

Why are the values of a company's intangible assets not reflected on its balance sheet?

Intangible assets are much more subjective than other assets, and accrual accounting states only verifiable, unbiased data may be used in the financial filings. For this reason, internally developed intangible assets such as branding, trademarks, and intellectual property will have no value recorded on the balance sheet because they cannot be accurately quantified and recorded. Companies are not permitted to assign values to these intangible assets unless the value is readily observable in the market via acquisition. Since there's a confirmable purchase price, a portion of the excess amount paid can be allocated towards the rights of owning the intangible assets and recorded on the closing balance sheet.

If the share price of a company increases by 10%, what is the balance sheet impact?

There would no change on the balance sheet as shareholders' equity reflects the book value of equity. Equity value, also known as the "market capitalization," represents the value of a company's equity based on supply and demand in the open market. In contrast, the book value of equity is the initial historical amount shown on the balance sheet for accounting purposes. This represents the company's residual value belonging to equity shareholders once all of its assets are liquidated and liabilities are paid off.

Book Value of Equity=Total Assets -Total Liabilities

The equity value recorded on the books will be significantly understated from the market value in most cases.

Do accounts receivable get captured on the income statement?

There is no accounts receivable line item on the income statement, but it gets captured, if only partially, indirectly in revenue. Under accrual accounting, revenue is recognized during the period it was earned, whether or not cash was received.

The two other financial statements would be more useful to understand what is happening to the accounts receivable balance since the cash flow statement will reconcile revenue to cash revenue, while the absolute balance of accounts receivable can be observed on the balance sheet.

Why are increases in accounts receivable a cash reduction on the cash flow statement?

Since the cash flow statement begins with net income and net income captures all of a company's revenue (not

just cash revenue), an increase in accounts receivable means that more customers paid on credit during the

period.

Thus, a downward adjustment must be made to net income to arrive at the ending cash balance. Although the revenue has been earned under accrual accounting standards, the customers have yet to make the due cash payments and this amount will be sitting as receivables on the balance sheet.

What is deferred revenue?

Deferred revenue (or "unearned" revenue) is a liability that represents cash payments collected from customers for products or services not yet provided. Some examples are gift cards, service agreements, or implied rights to future software upgrades associated with a product sold. In all the examples listed, the cash payment was received upfront and the benefit to the customer will be delivered on a later date.

Why is deferred revenue classified as a liability while accounts receivable is an asset?

Deferred Revenue: For deferred revenue, the company received payments upfront and has unfulfilled obligations to the customers that paid in advance, hence its classification as a liability.

Accounts Receivable: A/R is an asset because the company has already delivered the goods/services and all that remains is the collection of payments from the customers that paid on credit.

Why are increases in accounts payable shown as an increase in cash flow?

An increase in accounts payable would mean the company has been delaying payments to its suppliers or vendors, and the cash is currently still in the company's possession. The due payments will eventually be made, but the cash belongs to the company for the time being and is not restricted from being used. Thus, an increase in accounts payable is reflected as an inflow of cash on the cash flow statement.

Which section of the cash flow statement captures interest expense?

The cash flow statement doesn't directly capture interest expense. However, interest expense is recognized on the income statement and then gets indirectly captured in the cash from operations section since net income is the starting line item on the cash flow statement.

What happens to the three financial statements if a company initiates a dividend?

IS: When a company initiates a dividend, there'll be no changes to the income statement. However, a line below net income will state the dividend per share ("DPS") to show the amount paid.

CFS: On the cash flow statement, the cash from financing section will decrease by the dividend payout amount and lower the ending cash balance at the bottom.

BS: The cash balance will decline by the dividend amount on the balance sheet, and the offsetting entry will be a decrease in retained earnings since dividends come directly out of retained earnings.

Do inventories get captured on the income statement?

There is no inventory line item on the income statement, but it gets indirectly captured, if only partially, in cost of goods sold (or operating expenses). For a specific period, regardless of whether the associated inventory was purchased during the same period, COGS may reflect a portion of the inventory used up.

The two other financial statements would be more useful for assessing inventory as the cash flow statement shows the year-over-year changes in inventory, while the balance sheet shows the beginning and end-of-period inventory balances.

How should an increase in inventory get handled on the cash flow statement?

An increase in inventory reflects a use of cash and should thus be reflected as an outflow on the cash from operations section of the cash flow statement. The inventory balance increasing from the prior period implies the amount of inventory purchased exceeded the amount expensed on the income statement.

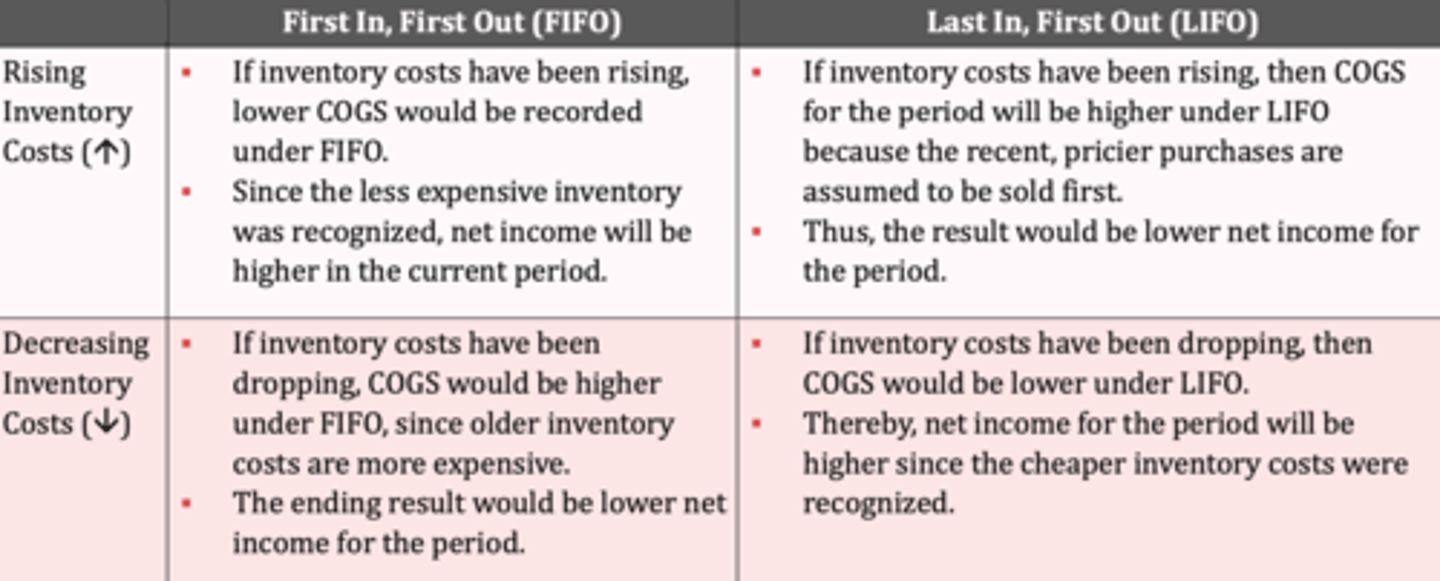

What is the difference between LIFO and FIFO, and what are the implications on net income?

FIFO and LIFO are two inventory accounting methods to estimate the value of inventory sold in a period.

First In, First Out ("FIFO"): Under FIFO accounting, the goods that were purchased earlier would be the first ones to be recognized and expensed on the income statement.

Last In, First Out ("LIFO"): Alternatively, LIFO assumes that the most recently purchased inventories are recorded as the first ones to be sold first.

The impact on net income would depend on how inventory costs have changed over time:

What is the average cost method of inventory accounting?

Besides FIFO and LIFO, the average cost method is the third most widely used inventory accounting method. Under this method, the assigned inventory costs are based on a weighted average, in which the total costs of production in a period are summed up and divided by the total number of items produced.

Each product cost is treated equally and inventory costs are spread out evenly, disregarding the date of purchase or production. Thus, this method is viewed as a simplistic compromise between the two other methods, but would be improper to use if the products sold are each unique with significant variance in the cost to manufacture and the sale price (i.e., more applicable for high-volume, identical batches of inventory).

How do you calculate retained earnings for the current period?

Retained earnings represent the total cumulative amount of net income held onto by a company since inception after accounting for any dividends paid out to its common and preferred shareholders. Current Period Retained

Earnings=Prior Retained Earnings+Net Income -Dividends

What does the retention ratio represent and how is it related to the dividend payout ratio?

The retention ratio represents the proportion of net income retained by the company, net of any dividends paid out to shareholders. The inverse of the retention ratio is the dividend payout ratio, which measures the proportion of net income paid out as dividends to investors.

Retention Ratio=(Net Income−Dividends)/Net Income

Dividend Payout Ratio=Dividends Paid/Net Income

What are the two ways to calculate earnings per share (EPS)?

Basic EPS: Determines a company's earnings on a per-share basis, but allocable to only the basic shares outstanding (otherwise known as "common shares").

Basic EPS= (Net Income−Dividends on Preferred Stock)/Basic Weighted Average Shares Outstanding

Diluted EPS: Compares a company's earnings relative to its shares outstanding on a per-share basis but considers the impact of potentially dilutive securities such as options, warrants, and convertible securities. If an option is "in-the-money," the option holder can become a common shareholder at their choosing. Thus, diluted EPS is a more accurate depiction of ownership value per share.

Diluted EPS=(Net Income−Dividends on Preferred Stock)/Diluted Weighted Average Shares Outstanding

Where can you find the financial reports of public companies?

In the US, public companies are required to report periodic filings with the SEC, including an annual report (10-K) and three quarterly (10-Q) reports each year. These reports are available for free through SEC EDGAR.

In other countries, reporting requirements will vary, but most countries will require at least an annual report, while some will require an interim filing (i.e., a report in the middle of the company's fiscal year). Only a few countries make company filings easily accessible through a central database, forcing analysts to rely on expensive financial data providers or dig through company websites manually to collect data.

The closest database to EDGAR in breadth and ease of use is Canada's SEDAR database.

What is a proxy statement?

The proxy statement, formally known as "Form 14A," is required to be filed before a shareholder meeting to solicit shareholder votes. The document must disclose all relevant details regarding the matter for shareholders to make an informed decision.

In addition, the board of directors' compensation and other notable announcements such as changes to the company's articles of incorporation are included.

What is an 8-K and when is it required to be filed?

An 8-K is a required filing with the SEC when a company undergoes a materially significant event and must disclose the details. Often called the "current report," 8-Ks are usually filed within four days of the event. The information contained within the report should be of high importance and pertinent to shareholders.

Events that would trigger this filing would include previously unannounced plans for a new acquisition, disposal of assets, bankruptcy, a tender offer, the resignation of a senior-level manager or member of the board of directors, or disclosure that the company is under SEC investigation for alleged wrongdoing.

Why has understanding the differences between US GAAP and IFRS financial reporting become increasingly important?

Understanding the differences between US GAAP and IFRS has become more important because:

Continuation of Globalization: Globalization is the gradual convergence of economies in different countries. The widespread adoption of IFRS has placed pressure on the US to adopt IFRS to have a single set of accounting standards and rules used worldwide, but it seems unlikely in the near-term.

Geographic Diversification of Investments: In recent years, investment firms have been broadening their investments' geographic scope to consider more opportunities overseas. Nowadays, institutional investors are more open to making investments in emerging markets due to the prevalence of opportunities and as a strategy to re-risk their overall portfolio.

Cross-Border M&A Activity: Cross-border mergers and acquisitions ("M&A") have emerged as a strategy for multinational companies to enter new markets, extend their reach to new potential customers, and diversify their revenue sources.

What do the phrases "above the line" and "below the line" mean?

The expression "the line" is in reference to operating income, which represents the point that divides normal, ongoing business operations from non-operational line items.

"Above the Line": If a profitability metric is "above the line," it reflects a company's operational performance before non-operational items such as interest and taxes. Financing-related activities are an example of such non-operational items, as decisions on how to fund a company are discretionary (debt vs. equity). For example, a metric such as earnings before interest, taxes, depreciation and amortization ("EBITDA") is considered "above the line." Hence, its widespread usage for comparative purposes since operational performance is portrayed while being independent of capital structure and taxes.

"Below the Line": In contrast, profitability metrics "below the line" have adjusted operating income for non-operating income and expenses, which are items classified as discretionary and unrelated to the core operations of a business. An example would be net income, since interest expense, non-operating income/(expenses), and taxes have all been accounted for in its ending value.

Is EBITDA a good proxy for operating cash flow?

While EBITDA does add back D&A, typically the largest non-cash expense, it doesn't capture the full cash impact of capital expenditures ("capex") or working capital changes during the period.

EBITDA also doesn't adjust for stock-based compensation, although an increasingly used "adjusted EBITDA" metric does add-back SBC. These non-cash and any non-recurring adjustments must be properly accounted for to assess a company's past operational performance and to accurately forecast its future cash flows.

What are some examples of non-recurring items?

Non-recurring items include legal settlements (gain or loss), restructuring expenses, inventory write-downs, or asset impairments. Often called "scrubbing" the financials, the act of adjusting for these non-recurring items is meant to normalize the cash flows and depict a company's true operating performance.

When adjusting for non-recurring expenses, are litigation expenses always added back?

Not necessarily, as whether an expense is non-recurring depends on the industry. In many cases, it's a discretionary decision on whether an expense is a part of the normal operations of a company. For example, expenses related to litigation might not be added back for a research and development (R&D) oriented pharmaceutical company, given the prevalence of lawsuits in the industry.

What is the difference between organic and inorganic revenue growth?

Organic Growth: A company experiencing organic growth is expanding to new markets, enhancing its sales & marketing strategies, improving its product/service mix, or introducing new products. The focus is on continuously making operational improvements and bringing in revenue (e.g., set prices more appropriately post-market research, target right end markets).

Inorganic Growth: Once the opportunities for organic growth have been maximized, a company may turn to inorganic growth, which refers to growth driven by M&A. Inorganic growth is often considered faster and more convenient than organic growth. Post-acquisition, a company can benefit from synergies, such as having new customers to sell to, bundling complementary products, and diversification in revenue.

How does the relationship between depreciation and capex shift as companies mature?

The more a company has spent on capex in recent years, the more depreciation the company incurs in the near-term future. Therefore, when looking at high-growth companies spending heavily on growth capex, their ratio between capex and annual depreciation will far exceed 1.

For mature businesses experiencing stagnating or declining growth, this ratio converges near 1, as the only capex is related to routine maintenance capex (e.g., replace equipment, refurbish store layouts).

What is working capital?

The working capital metric measures a company's liquidity and ability to pay off its current obligations using its current assets. In general, the more current assets a company has relative to its current liabilities, the lower its liquidity risk. Current liabilities represent payments that a company needs to make within the year (e.g., accounts payable, accrued expenses), whereas current assets are resources that can be turned into cash within the year (e.g., accounts receivable, inventory).

Working Capital=Current Assets−Current Liabilities

Why are cash and debt excluded in the calculation of net working capital (NWC)?

In practice, cash and other short-term investments (e.g., treasury bills, marketable securities, commercial paper) and any interest-bearing debt (e.g., loans, revolver, bonds) are excluded when calculating working capital because they're non-operational and don't directly generate revenue.

Net Working Capital (NWC)=Operating Current Assets−Operating Current Liabilities

Cash & cash equivalents are closer to investing activities since the company can earn a slight return (~0.25% to 1.5%) through interest income, whereas debt is classified as financing. Neither is operations-related, and both are thereby excluded in the calculation of NWC.

Is negative working capital a bad signal about a company's health?

Working capital can be positive or negative, further context is needed.

Positive Example: Being efficient at collecting revenue, quick inventory turnover, and delaying payments to suppliers while efficiently investing excess cash into high-yield investments.

Negative Example: Signifies liquidity issues. High AP due soon, with low inventory balance that desperately needs replenishing and low AR. The company would need to gather external financing to pay off liabilities.

What does change in net working capital tell you about a company's cash flows?

The change in net working capital is important because it gives you a sense of how much a company's cash flows will deviate from its accrual-based net income.

Change in Net Working Capital=NWC Prior Period −NWC Current Period

If a company's NWC has increased year-over-year, its operating assets have grown and/or its operating liabilities have shrunk from the prior year. Since an increase in an operating asset is a cash outflow, it should be intuitive why an increase in NWC means less cash flow for a company (and vice versa).

What is the cash conversion cycle?

The cash conversion cycle ("CCC") measures the number of days it takes a company to convert its inventory into cash from sales. Therefore, a lower cash conversion cycle is preferred as it implies the company generates and collects cash in a shorter duration. As a general rule, companies with lower CCCs operate efficiently, hold more negotiating power over suppliers, and have quicker sales collection cycles. Cash Conversion Cycle=DIO+DSO -DPO

How would you forecast capex and D&A when creating a financial model?

In the simplest approach, D&A can be projected as either a percentage of revenue or capital expenditures, while capex is forecasted as a percentage of revenue. Re-investments such as capex directly correlate with revenue growth, thus historical trends, management guidance, and industry norms should be closely followed.

Alternatively, a depreciation waterfall schedule can be put together, which would require more data from the company to track the PP&E currently in-use and the remaining useful life of each. In addition, management plans for future capex spending and the approximate useful life assumptions for each purchase will be necessary. As a result, depreciation from old and new capex will be separately shown.

For projecting amortization, useful life assumptions would also be required, which can often be found in a separate footnote in a company's financial reports.

How would you forecast PP&E and intangible assets?

When forecasting PP&E, the end of period balance will be calculated using the roll-forward schedule shown below. Note, capex will input as a negative, meaning the PP&E balance should increase. Other factors that could affect the end-of-period PP&E balance are asset sales and write-downs.

PP&E Roll-Forward:

EOP PP&E=BOP PP&E+Capex−Depreciation

To forecast intangible assets, management guidance becomes necessary as unlike capex, there's usually no clear historical pattern that can be followed as these purchases tend to be inconsistent. In most cases, it's best to rely on management if available, but in the absence of guidance, it's recommended to assume no purchases.

Intangible Assets Roll-Forward:

EOP Intangibles=BOP Intangibles+Intangibles Purchases -Amortization

What is the difference between the current ratio and the quick ratio?

Both ratios are used to assess a company's short term liquidity situation.

Current Ratio: Greater then 1 implies that a company can meet its short-term obligations and is financially healthy.

Current Ratio=Current Assets/Current Liabilities

Quick Ratio: Also known as the acid-test ratio, is the same as the current ratio but uses stricter guidelines on what a liquid asset is.

Quick Ratio=(Cash & Cash Equivalents+AR+Short Term Investments)/Current Liabilities

Give some examples of when the current ratio might be misleading?

* The cash balance used includes the minimum cash amount required for working capital needs - meaning operations could not continue if cash were to dip below this level.

* Similarly, the cash balance may contain restricted cash, which is not freely available for use by the business and is instead held for a specific purpose.

* Short-term investments that cannot be liquidated in the markets easily could have been included (i.e., low liquidity, cannot sell without a substantial discount).

* Accounts receivable could include "bad A/R", but management refuses to recognize it as such.

Is it bad if a company has negative retained earnings?

Not necessarily. Retained earnings can turn negative if the company has generated more accounting losses than profits. For example, this is often the case for startups and early-stage companies investing heavily to support future growth (e.g., high capex, sales & marketing expenses, R&D spend).

Another component of retained earnings is the payout of dividends and share repurchases, contributing to lower or even negative retained earnings. In these scenarios, the negative retained earnings mean the company has returned more capital to shareholders than taken in.

How can a profitable firm go bankrupt?

To be profitable, a company must generate more revenue than expenses; however, if a company is ineffective at collecting cash, the company can suffer from liquidity issues due to timing mis-match of inflow and outflow.

Profitable companies with working capital issues can usually secure financing but if it's unavailable, they'll go bankrupt.

Alternatively, a profitable company that took on far too much debt in its capital structure and could not service the interest payments may also default on its debt obligations.

What does return on assets (ROA) and return on equity (ROE) each measure?

Return on assets ("ROA") and return on equity ("ROE") are measures of profitability that show how effective a company's management team is at utilizing the resources it has on-hand (assets or equity).

Return on Assets: ROA measures asset utilization and how efficiently a company's assets are used to generate earnings. A high ROA relative to a peer group indicates assets are being used near full capacity, whereas a low ROA means management may not be deriving the full potential benefit from its assets.

Return on Assets

(ROA)=Net Income/(Average of Beginning and Ending Total Assets)

Return on Equity: The ROE ratio gives insight into how efficiently a management team has been using the capital shareholders have contributed. A higher ROE means management is efficient at using the money raised from equity financing (and vice versa).

Return on Equity

(ROE)=Net Income/(Average of Beginning and Ending Book Value of Equity)

What is the relationship between return on assets (ROA) and return on equity (ROE)?

The relationship between ROA and ROE is tied to the use of leverage. In the absence of debt in the capital structure, the two metrics would be equal. But if the company were to add debt to its capital structure, its ROE would rise above its ROA due to increased cash, as total assets would rise while equity decreases.

If a company has a ROA of 10% and a 50/50 debt-to-equity ratio, what is its ROE?

Imagine a company with $100 in total assets. A 10% return on assets (ROA) would imply $10 in net income. Since the debt-to-equity mix is 50/50, the return on equity (ROE) is $10/$50 = 20%.

When using metrics such as ROA and ROE, why do we use averages for the denominator?

The numerator, usually net income, comes from the income statement. The denominator, either assets or equity, comes from the balance sheet. The income statement covers a specific period, whereas the balance sheet is a snapshot at one particular point in time. Thus, the average between the beginning and ending balance of the denominator is used to adjust for this mismatch in timing.

What are some shortcomings of the ROA and ROE metrics for comparison purposes?

A company's ROA and ROE ratios are benchmarked against competitors in the same industry to assess management efficiency and track historical trends. However, the ROA and ROE ratios are most useful when compared to a peer group of companies with similar growth rates, margin profiles, and risks. This approach would be best suited for established companies operating in mature, low-growth industries with many comparable companies to accurately track the management team's profitability and efficiency.

What is the return on invested capital (ROIC) metric used to measure?

The return on invested capital ("ROIC") metric is used to assess how efficient a management team is at capital allocation. A company that generates an ROIC over its cost of capital (WACC) suggests the management team has been allocating capital efficiently (i.e., investing in profitable projects or investments) and if sustained over the long-run, this indicates a competitive advantage. ROIC represents one of the most fundamental assessments of a company: "How much in returns is the company earning for each dollar invested?" Return on Invested Capital (ROIC)=NOPAT/Invested Capital

What does the asset turnover ratio measure?

The asset turnover ratio is a metric used to understand how efficiently a company uses its assets to generate sales. The asset turnover ratio answers the question, "How many dollars in revenue does the company generate per dollar of assets?" The higher the ratio, the better, as this suggests the company is generating more revenue per dollar of an asset owned. But it has shortfalls in being distorted by capital expenditures and asset sales. Asset Turnover

Ratio=Revenue/(Average of Beginning and Ending Total Assets)

What does inventory turnover measure and how does it differ from days inventory held (DIH)?

The inventory turnover ratio is how often a company has sold and replaced its inventory balance throughout a specified period (i.e., the number of times inventory was "turned over").

Inventory Turnover=Cost of Goods Sold/(Average of Beginning and Ending Inventory)

In contrast, DIH is the average number of days it takes for a company to turn its inventory into revenue.

What does accounts receivables turnover measure?

Accounts receivable turnover is a metric used to measure the number of times per year that a company can collect its average accounts receivable from customers. The higher the turnover ratio, the better as it indicates the company is efficient at collecting its due payments from customers that paid on credit.

Receivables Turnover =Revenue/(Average of Beginning and Ending Accounts Receivables)

What does accounts payables turnover measure and is a higher or lower number preferable?

Accounts payable turnover measures how quickly a company pays its vendors. Generally, longer credit terms provide a company with more flexibility as it means the company has more cash-on-hand. A higher A/P turnover means the company pays off its A/P balance quickly, meaning the cash outflows occur faster.

Accounts Payable Turnover=Cost of Goods Sold/(Average Beginning and Ending Accounts Payable)

How do you calculate the debt service coverage ratio (DSCR) and what does it measure?

The debt service coverage ratio (DSCR) is a measure of creditworthiness that tests a company's ability to pay its current debt obligations using its current cash flows. As a general rule, a DSCR greater than 1.0 shows the company is generating sufficient cash flows to pay down its debt. But a DSCR below 1.0 could be a cause of concern, as it suggests the company might have insufficient cash flows to handle the debt it currently holds.

There are various methods to calculate the DSCR, but one commonly used example is shown below:

DSCR =(EBITDA−Capex)/(Mandatory Principal Repayment+ Interest Expense)

How do you calculate the fixed charge coverage ratio (FCCR) and what does it mean?

The fixed charge coverage ratio (FCCR) is used to assess if a company's earnings can cover its fixed charges, which can include rent, utilities, and interest expense. The higher the ratio, the better the creditworthiness. Fixed charges can include expenses such as rent or lease payments, and utility bills.

Fixed Charge Coverage Ratio (FCCR)=(EBIT+Lease Charges)/(Lease Charges+Interest Expense)

How would raising capital through share issuances affect earnings per share (EPS)?

The impact on EPS is that the share count increases, which decreases EPS. But there can be an impact on net income, assuming the share issuances generate cash because there would be higher interest income, which increases net income and EPS. However, most companies' returns on excess cash are low, so this doesn't offset the negative dilutive impact on EPS from the increased share count.

Alternatively, share issuances might affect EPS in an acquisition where stock is the form of consideration. The amount of net income the acquired company generates will be added to the acquirer's existing net income, which could have a net positive (accretive) or negative (dilutive) impact on EPS.

How would a share repurchase impact earnings per share (EPS)?

The impact on EPS following a share repurchase is a reduced share count, which increases EPS. However, there would be an impact on net income, assuming the share repurchase was funded using excess cash. The interest income that would have otherwise been generated on that cash is no longer available, causing net income and EPS to decrease.

But the impact would be minor since the returns on excess cash are low, and would not offset the positive impact the repurchase had on EPS from the reduced share count.

What is the difference between the effective and marginal tax rates?

Effective Tax Rate: The effective tax rate represents the percentage of taxable income corporations must pay in taxes. For historical periods, the effective tax rate can be backed out by dividing the taxes paid by the pre-tax income (or earnings before tax).

Effective Tax Rate %=Taxes Paid/Earnings Before Tax

Marginal Tax Rate: The marginal tax rate is the taxation percentage on the last dollar of a company's taxable income. The tax expense depends on the statutory tax rate of the governing jurisdiction and the company's taxable income, as the tax rate adjusts according to the tax bracket in which it falls.

Why is the effective and marginal tax rate often different?

Effective and marginal tax rates differ because the effective tax rate calculation uses pre-tax income from the accrual-based income statement. Since there's a difference between the taxable income on the income statement and taxable income shown on the tax filing, the tax rates will nearly always be different. Thus, the "Tax Provision" line item on the income statement rarely matches the actual cash taxes paid to the IRS.

Could you give specific examples of why the effective and marginal tax rates might differ?

Under GAAP, many companies follow different accounting standards and rules for tax and financial reporting.

- Most companies use straight-line depreciation (i.e., equal allocation of the expenditure over the useful life) for reporting purposes, but the IRS requires accelerated depreciation for tax purposes - meaning, book depreciation is lower than tax depreciation for earlier periods until the DTLs reverse.

- Companies that incurred substantial losses in earlier years could apply tax credits (i.e., NOL carry-forwards) to reduce the amount of taxes due in later periods.

- When debt or accounts receivable is determined to be uncollectible (i.e., "Bad Debt" and "Bad AR"), this can create DTAs and tax differences. The expense can be reflected on the income statement as a write-off but not be deducted in the tax returns.

What are deferred tax liabilities (DTLs)?

Deferred tax liabilities ("DTLs") are created when a company recognizes a tax expense on its GAAP income statement that, because of a temporary timing difference between GAAP and IRS accounting, is not actually paid to the IRS that period but is expected to be paid in the future.

DTLs are often related to depreciation. Companies can use accelerated depreciation methods for tax purposes but elect to use straight-line depreciation for GAAP reporting. This means that for a given depreciable asset, the amount of depreciation recognized in the earlier years for tax purposes will be greater than under GAAP.

Those temporary timing differences are recognized as DTLs. Since these differences are just temporary - under both book and tax reporting, the same cumulative depreciation will be recognized over the life of the asset - at a certain point into the asset's useful life, an inflection point will be reached where the depreciation expense

for tax reporting will become lower than for GAAP.

What are deferred tax assets (DTAs)?

Deferred tax assets ("DTAs") are created when a company recognizes a tax expense on its GAAP income statement that, due to a temporary timing difference between GAAP and IRS accounting rules, is lower than what must be paid to the IRS for that period. These net operating losses ("NOLs") that a company can carry forward against future income create DTAs.

For example, a company that reported a pre-tax loss of $10 million will not get an immediate tax refund. Instead, it'll carry forward these losses and apply them against future profits.

However, under GAAP, the tax benefit will be recognized from a presumed future tax refund immediately on the income statement, and this difference gets captured in DTAs. As the company generates future profits and uses those NOLs to reduce future tax liabilities, the DTAs gradually reverse.

Another reason for DTAs is the differences between book and tax rules for revenue recognition. Broadly, tax rules require recognition based on receiving cash, while GAAP adheres rigidly to accrual concepts.

What impact did the COVID-19 Tax Relief have on NOLs?

Under the Coronavirus Aid, Relief, and Economic Security (CARES) Act, NOLs that arise beginning in 2018 and through 2020 could be carried back for up to a maximum of five years. The rules for claiming tax losses were changed to assist individuals and corporations negatively impacted by the pandemic.

For tax years beginning after 2020, the CARES Act would allow NOLs deduction equal to the sum of:

1. All NOL carryovers from pre-2018 tax years

2. The lesser amount between 1) all NOL carryovers from post-2017 tax years or 2) 80% of remaining taxable income after deducting NOL carryovers from pre-2018 tax years

Previously, NOLs arising in tax years ending after 2017 could not be carried back to earlier tax years and offset taxable income. NOLs arising in tax years post-2017 could only be carried forward to later years. But the key benefit was that the NOLs could be carried forward indefinitely until the loss was fully recovered (yet limited to 80% of the taxable income in a single tax period).

What are the notable takeaways from Joe Biden's proposed tax plans?

- The corporate tax rate will rise from the Trump Era's Tax Cuts and Jobs Act ("TCJA") rate of 21% to 28%; estimated to increase the government's tax revenue from $2 trillion to $3 trillion over the next decade.

- The top tax rate for individuals with a taxable income of $400k+ will rise from 37% to 39.6%.

- A 12.4% payroll tax will be imposed on those earning $400k+ and to be split evenly between employers and employees.

- Minimum tax on corporations with book profits of $100+ million, which would be structured so that corporations would pay the greater amount between 1) their regular corporate income tax or 2) the 15% minimum tax with net operating loss (NOL) and foreign tax credits allowed.

Does a company truly not incur any costs by paying employees through stock-based compensation rather than cash?

Stock-based compensation is a non-cash expense that reduces a company's taxable income and is added-back on the cash flow statement.

However, SBC incurs an actual cost to the issuer by creating additional shares for existing equity owners. The issuing company, due to the dilutive impact of the new shares, becomes less valuable on a per-share basis to existing shareholders.

Could you define contra-liability, contra-asset, and contra-equity with examples of each?

Contra-Liability: A contra-liability is a liability account that carries a debit balance. While classified as a liability, it functions closer to an asset by providing benefits to the company. An example would be financing fees in M&A. The financing fees are amortized over the debt's maturity, which reduces the annual tax burden and results in tax savings until the end of the term.

Contra-Asset: A contra-asset is an asset that carries a credit balance. An example would be depreciation, as it reduces the fixed asset's carrying balance while providing tax benefits to the company. There is often a line called "Accumulated Depreciation," which is the contra-asset account reflected on the balance sheet.

Contra-Equity: A contra-equity account has a debit balance and reduces the total amount of equity held by a company. An example would be treasury stock, which reduces shareholders' equity. Since treasury stock reduces the total shareholders' equity, treasury stock is shown as a negative on the balance sheet.

What is an allowance for doubtful accounts on the balance sheet?

Under US GAAP, the allowance for doubtful accounts estimates the percentage of uncollectible accounts receivable. This line item is considered a contra-asset because it reduces the accounts receivable balance. The allowance, often called a bad debt reserve, represents management's estimate of the amount of A/R that appears unlikely to be paid by customers. In effect, a more realistic value for A/R that'll actually be turning into cash is shown on the balance sheet, while preventing any sudden decreases in the company's A/R balance.

What is the difference between a write-down and a write-off?

Write-Downs: In a write-down, an adjustment is made to an asset such as inventory or PP&E that has become impaired. The asset's fair market value (FMV) has fallen below its book value; hence, its classification as an impaired asset. Based on the write-down amount deemed appropriate, the value of the asset is decreased to reflect its true value on the balance sheet. Examples of asset write-downs would include damages caused by minor fires, accidents, or sudden value deterioration from lower demand.

Write-Offs: Unlike a write-down in which the asset retains some value, a write-off reduces an asset's value to zero, meaning the asset has been determined to hold no current or future value (and should therefore be removed from the balance sheet). Examples include uncollectible AR, "bad debt," and stolen inventory.

How would a $100 inventory write-down impact the three financial statements?

IS: The $100 write-down charge will be reflected in the cost of goods line item. The expense would decrease EBIT by $100, and net income would decline by $70, assuming a 30% tax rate.

CFS: The starting line item, net income, will be down $70, but the $100 write-down is an add-back since there's no actual cash outflow from the write-down. The net impact to the ending cash will be a $30 increase.

BS: On the asset side, cash is up $30 due to inventory being written down $100. This will be offset by the decrease of $70 in net income that flows through

retained earnings on the equity section. Both sides of the balance sheet will be down by $70 and remain in balance.

How does buying a building impact the three financial statements?

IS: Initially, there'll be no impact on the income statement since the purchase of the building is capitalized.

CFS: The PP&E outflow is reflected in the cash from investing section and reduces the cash balance.

BS: The cash balance will go down by the purchase price of the building, with the offsetting entry to the cash reduction being the increase in PP&E.

Throughout the purchased building's useful life, depreciation is recognized on the income statement, which reduces net income each year, net of the tax expense saved (since depreciation is tax-deductible).

How does selling a building with a book value of $6 million for $10 million impact the three financial statements?

IS: If I sell a building for $10 million with a book value of $6 million, a $4 million gain from the sale would be recognized on the income statement, which will increase my net income by $4 million.

CFS: Since the $4 million gain is non-cash, it'll be subtracted from net income in the cash from operations section. In the investing section, the full cash proceeds of $10 million are captured.

BS: The $6 million book value of the building is removed from assets while cash increases by $10 million, for a net increase of $4 million to assets. On the L&E side, retained earnings will increase by $4 million from the net income increase, so the balance sheet remains balanced.

However, the gain on sale will result in higher taxes, which will be recognized on the income statement. This lowers retained earnings by $1 million and be offset by a $1 million credit to cash on the asset side.

If a company issues $100 million in debt and uses $50 million to purchase new PP&E, walk me through how the three statements are impacted in the initial year of the purchase and at the end of year 1. Assume a 5% annual interest rate on the debt, no principal paydown, straight-line depreciation with a useful life of five years and no residual value, and a 40% tax rate.

Initial Purchase Year (Year 0)

IS: There'll be no changes as neither capex nor issuing debt impact the income statement.

CFS: The $50 million outflow of capex will be reflected in the cash from investing section of the cash flow statement, while the $100 million inflow from the debt issuance will be reflected in the cash from financing section. The ending cash balance will be up by $50 million.

BS: On the assets side, cash will be up by $50 million and PP&E will increase $50 million from the PP&E purchase, making the assets side increase by $100 million in total. On the L&E side, debt will be up $100 million, which will offset the increase in assets and the balance sheet remains in balance.

End of First Year (Year 1)

IS: Since the capex amount was $50 million with a useful life assumption of five years (straight-line to a residual value of zero), the annual depreciation will be $10 million. Next, the interest expense will be equal to the $100 million in debt raised multiplied by the 5% annual interest rate, which comes out to $5 million in annual interest expense. The pre-tax income will be down by $15 million and assuming a 40% tax rate, net income will be down $9 million.

CFS: Net income will be down $9 million, but the non-cash depreciation of $10 million will be added back, making the ending cash balance increase by $1 million.

BS: On the assets side, cash is up by $1 million and PP&E will decrease by $10 million because of the depreciation. Since equity is also down $9 million due to net income, both sides will remain in balance.

For long-term projects, what are the two methods for revenue recognition?

Percentage of Completion Method: In the percentage of completion method, revenue is recognized based on the percentage of work completed during the period. This method is used far more common since it's in a company's best interest to record partial revenue once earned. Two conditions must be met to use this method: the collection of payment must be reasonably assured, and the total project costs with the estimated completion date are required to be provided.

2. Completed Contract Method: The completed contract method recognizes revenue once the entire project has been completed. This method is rarely used in the US, as it would result in a company under-reporting revenue that has been earned under the accrual-based system.

If a company has continuously incurred goodwill impairment charges, what do you take away from seeing this in their financials?

Goodwill on the balance sheet remains unchanged unless it's impaired, meaning the purchaser has determined that the acquired assets are worth less than initially thought. While goodwill impairment can be attributed to unforeseeable circumstances, impairments as a common occurrence may raise concerns regarding the management team's history of overpaying for assets or their inability to integrate new acquisitions.