A level Economics - Micro

1/151

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

152 Terms

Ceteris paribus definition?

All other influencing factors are held constant

Four factors of production?

Land, labour, capital, enterprise

What is land?

Natural physical inputs which are used up in production

What is labour?

The exertion (physical and mental) of workers

What are capital and consumer goods?

capital good - Used to make other goods, are not used up in production

consumer good - goods bought by individuals for personal consumption

What is an entrepreneur?

Takes risks and organises factors of production

What is a positive statement?

objective statements that can be tested and evaluated based on empirical evidence

can be proven to be true or false

What is a normative statement?

subjective statements that include opinions and personal beliefs

cannot be tested by empirical evidence

What is resource scarcity and the economic problem?

when demand for a resource is greater than the available supply

having unlimited wants and finite resources

What are the causes of resource scarcity?

demand-induced, supply-induced, structural scarcity, no effective substitutes

What is demand-induced resource scarcity?

high market demand for a scarce resource

can be due to fast growing populations, rising prosperity, advances in technologies and economies of scale

What is supply-induced resource scarcity?

supply of a resource is running out over time as extraction rates increase

What is structural scarcity?

due to mismanagement of the resource which leads to long term degradation of the resource

What is allocative efficiency?

resources have been allocated in the most efficient manner

demand = supply

social surplus is maximised

working at the social optimum

What is a non-renewable resource?

finite in supply, no mechanisms exist at present to replenish them

eg fossil fuels

What is a renewable resource?

replaceable over time

eg solar energy, oxygen

What is opportunity cost?

the benefit lost from the next best alternative

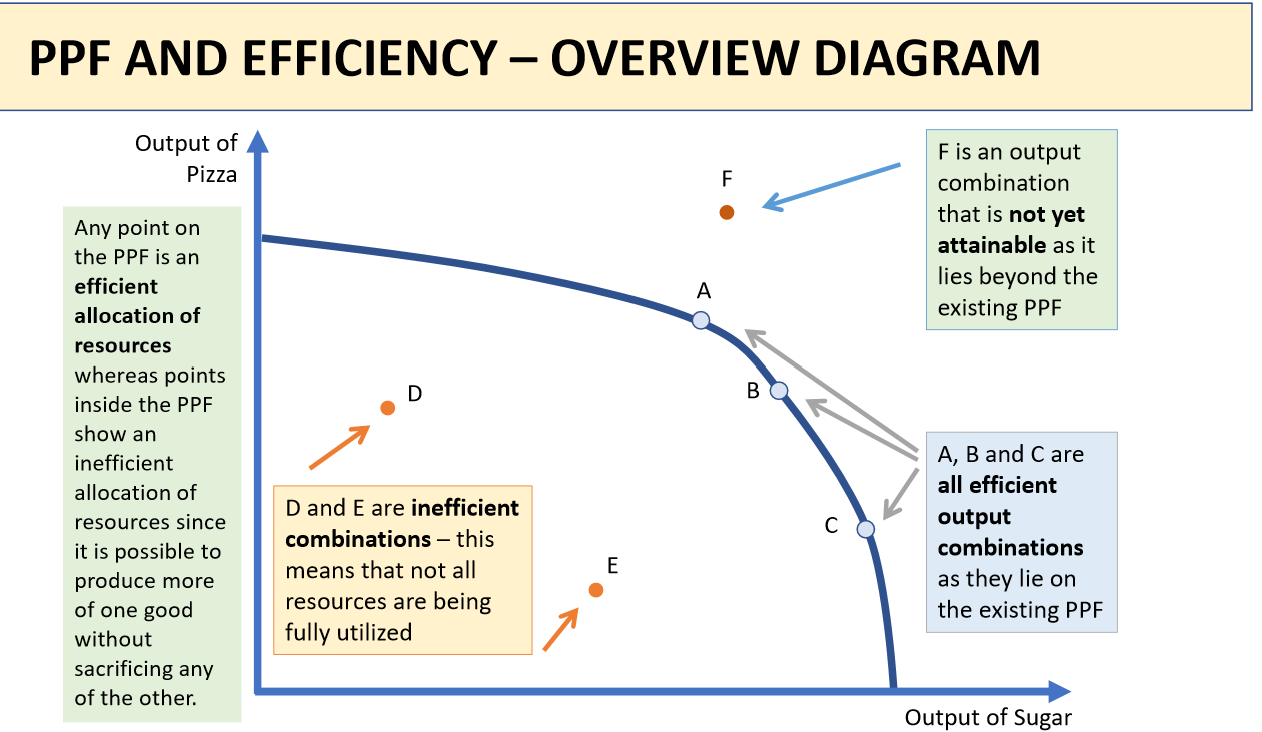

What is a PPF?

a production possibility frontier graphically demonstrates how much an economy can produce when all factors of production are fully and efficiently employed

Explain the shape of the PPF curve?

arc that is concave to the origin

this is because the opportunity cost of expanding X measured in terms of lost units of Y is increasing

Why would a PPF be linear?

the marginal opportunity cost of switching resources between consumer and capital goods is constant - perfect factor substitutability of resources

When will a PPF shift outwards?

represents economic growth - allows the economy to produce more of both goods or to improve its production capabilities

due to: increase in natural resources, technological advancements, human capital development, or investment in capital

What do the points on, inside and outside the PPF mean?

any point on PPF = efficient allocation of resources

any point inside PPF = inefficient allocation of resources since it is possible to produce more of one good without sacrificing any of the other

any point outside the PPF = not yet attainable/sustainable with current resources

What is a value judgement?

evaluative processes based on an individual’s standards or priorities

What is specialisation?

The concentration of production on a limited range of goods or tasks, allowing for increased efficiency.

What is division of labour?

The splitting of the production process into different tasks, with each worker specializing in one task to increase productivity.

What are the advantages and disadvantages of division of labour?

Advantages: increased efficiency, economies of scale

Disadvantages: reduced job satisfaction, lower motivation, increased workplace absenteeism

What is the difference between production and productivity?

production - a measure of the value of the output of goods and services (eg GDP)

productivity - a measure of the efficiency of factors of production measured by output per person employed

What are the factors affecting productivity?

competition, technology, specialisation, training, demand

What is economies of scale?

the cost advantage experienced by a firm when it increases its level of output

What are the main functions of money?

medium of exchange (widely accepted), store of value (can save it), unit of account (standard value), standard of deferred payment (can owe it)

What is a free market economy?

economic decisions are primarily made by private individuals and firms

Advantages and disadvantages of a free market economy?

advantages: choice, profit motive, dynamic, risk is well rewarded, competition, efficiency

disadvantages: market failure, monopolies, potential loss of quality/ price, missing markets, inequality, sustainability

What did Friedrich Hayek believe?

pro free market

strong belief in the role and importance of the individual in an economy

he was highly critical of centralised planning, arguing that no government or authority could understand and control an economy effectively, leading to mistakes and inefficiencies

What did Adam Smith believe?

pro free market

came up with concept of the invisible hand - pricing mechanism that assume the markets would always return to equilibrium and allocate resources efficiently on their own

came up with the ideas of division of labour and competition

What is a command economy?

all economic decisions are made by the government or central authority

Advantages and disadvantages of a command economy?

advantages: less inequality, provision of public goods and services

disadvantages: lack of competition (reduces efficiency), no profit motive, narrow range of choice, inefficient resource allocation

What did Karl Marx believe?

pro command economy

he believed that in a free market, drive for profit would lead to exploitation of workers

he believed command economies would lead to equality and a classless society based on collective ownership and distribution according to need

What is a mixed economy?

both the private sector and the government play significant roles in economic decision making

most modern economies have mixed economic systems

What did John Maynard Keynes believe?

he debated with Hayek in the 1930s

he supported significant government intervention in the economy to stimulate growth whereas Hayek did not

What is a market?

places where buyers and sellers can meet to sell and purchase goods and services

What is demand?

the quantity of a good or service that consumers are able and willing to buy at a given price

What is the law of demand?

as price increases demand decreases

Why does the demand curve slope down?

substitution effect, income effect and diminishing marginal utility

What is the substitution effect?

substitutes are replacements for another product

a fall in the price of goods and services will lead to higher demand as some switch from other similar goods due to price

What is the income effect?

when the price of a product falls, consumers have more real purchasing power allowing them to purchase more of the product, leading to an increase in the quantity demanded

What is diminishing marginal utility?

as people consume more of a particular product, the additional satisfaction they derive from each additional unit decreases, meaning they are willing to pay less for each successive unit

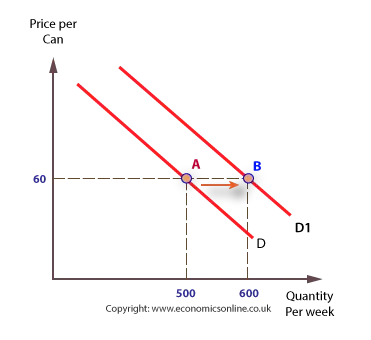

What is a shift in the demand curve?

inward shift - less is demanded at each given price

outward shift - more is demanded at each given price

What are the factors that affect demand?

changes in:

price, weather, life style, tastes and preferences, seasonality, population, price of substitutes and complementary goods, advertisement, interest rates

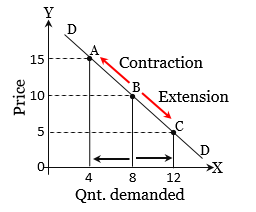

What causes movement along a demand curve?

changes in the market price of the product itself

higher price leads to contraction of demand

lower price leads to expansion of demand

What are complementary goods?

goods that are joint in demand - if you buy one you are likely to buy the other

What is supply?

the amount firms are willing and able to produce at a given price

What is the law of supply?

as price increases firms will be willing to supply more

Why does the supply curve slope up?

firms are profit motivated

cost to produce each additional unit increases

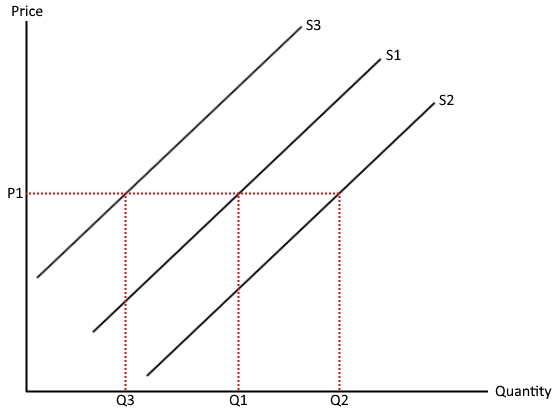

What is a shift in the supply curve?

inward shift - less is supplied at each given price

outward shift - more is supplied at each given price

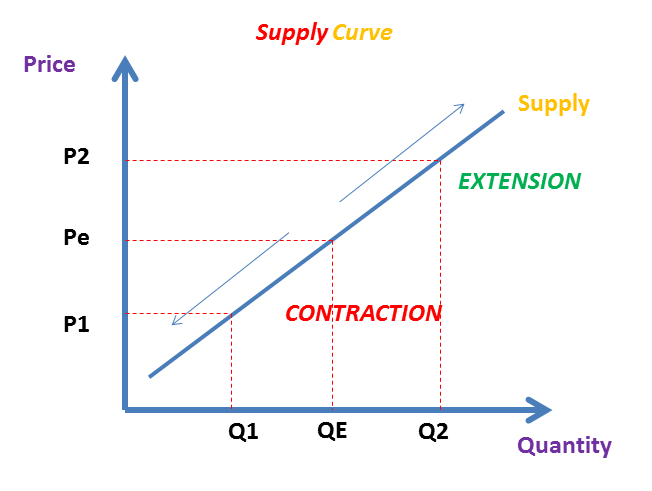

What causes a movement along a supply curve?

changes in the market price of the product itself

higher price leads to expansion of supply

lower price leads to contraction of supply

What are the reasons for a shift in supply?

PINTSWC

Productivity, indirect taxes, number of firms, technology, subsidies, weather, cost of production

Demand and supply key diagram?

What is a subsidy?

A grant given to firms which lowers the cost of production

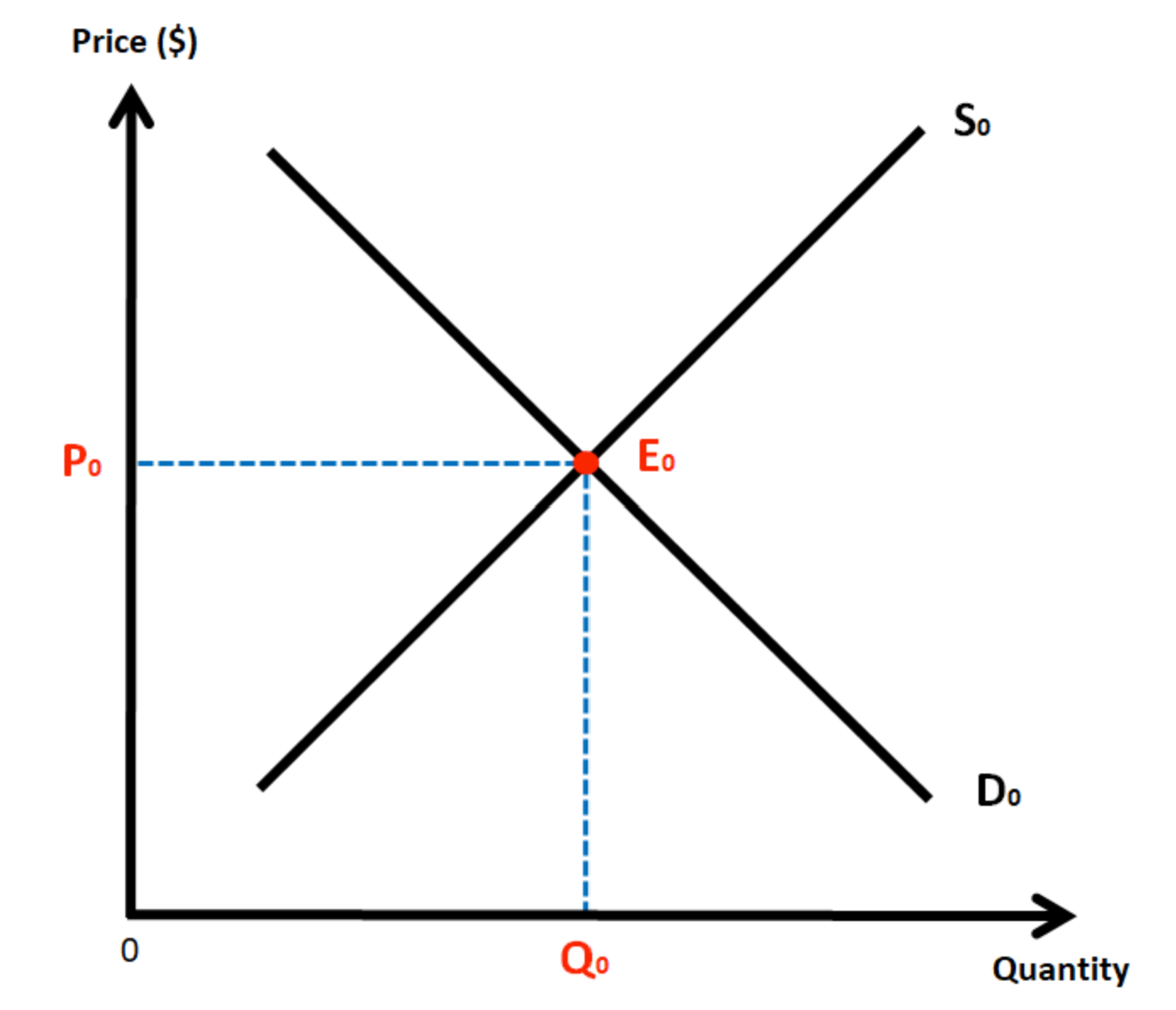

What is market equilibrium and the equilibrium point?

when supply and demand are equal leading to stability in prices and quantities exchanged

the point at which the supply and demand curve intersect is the equilibrium point

What is excess demand and excess supply?

excess supply - when supply is greater than demand

excess demand - when demand is greater than supply

How does the price mechanism work when there is a shift in demand?

increase in demand:

demand shifts right

excess demand

signals to producers (eg empty shelves)

producers increase price and increase supply

new market equilibrium is reached

decrease in demand:

demand shifts left

excess supply

signals to producers (eg too much stock)

producers decrease price and contract supply

new market equilibrium is reached

How does the price mechanism work when there is a shift in supply?

increase in supply:

supply shifts right

excess supply

price falls

incentive for consumers to increase demand

new market equilibrium is reached

decrease in supply:

supply shifts left

excess demand

price rises

incentive for consumers to reduce demand

new market equilibrium is reached

What is elasticity?

the responsiveness of one variable to changes in another

What is PED and formula?

price elasticity of demand measures responsiveness of demand to a change in the price of the good itself

PED = % change in QD / % change in P

Values for PED meaning?

0 - perfectly inelastic (d doesnt change when p changes)

0-1 - inelastic

1- unitary

>1- elastic (d responds more than proportionately to a change in p)

infinite - perfectly elastic

What are the factors that determine PED?

inelastic demand:

low percentage of income

necessity

few substitutes

short time frame

broad definition

difficult to switch between subs

habitual consumption (addiction)

peak demand

brand loyalty

opposites for elastic demand

How to draw a graph to represent PED?

inelastic demand - steep curve

elastic demand - shallow curve

perfectly inelastic - straight line vertically

perfectly elastic - straight line horizontally

What is the relationship between total revenue and PED?

change in revenue is greater for elastic goods than inelastic goods when the price changes

What is XED and the formula?

cross price elasticity of demand measures the responsiveness of demand for good X following a change in the price of good Y

XED = % change in QD of good X / % change in price of good Y

What does the XED value represent?

positive value - goods are substitutes

negative value - goods are complementary

value of 0 - goods are not related

the higher the absolute value the stronger the relationship between the 2 goods (strong/weak substitutes/complements)

What is YED and what is the formula?

income elasticity of demand measures the relationship between in change in quantity demanded for a good and a change in consumers’ real income

YED = % change in QD for X / % change in real income

YED values meaning?

positive - normal goods

negative - inferior goods

0-1 - necessities

1+ - luxury goods

What is an inferior good?

demand varies inversely to the economic cycle (demand rises in a recession)

e.g own-label beans

What is a normal good?

a good that experiences an increase in demand due to an increase in a consumer's income

e.g clothing

What is price elasticity of supply (PES) and equation?

measures the responsiveness of quantity supplied following a change in price

PES = %change is QS / % change in P

PES values

coefficient is always positive

0-1 = inelastic supply

1+ = elastic supply

What factors determine supply elasticity?

ease of factor substitution

availability of spare production capacity

stock levels

time frame

artificial limits eg quotas

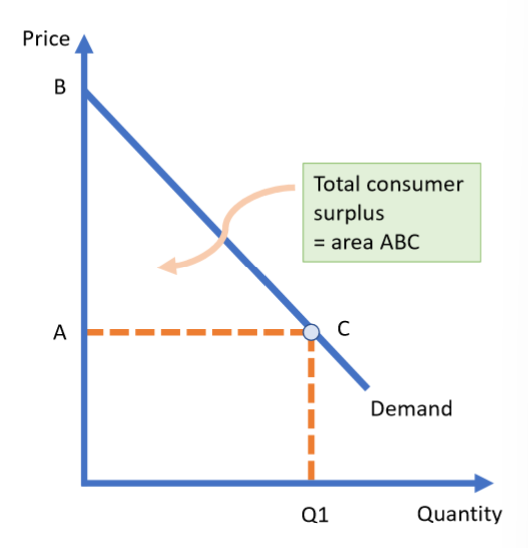

What is consumer surplus?

the difference between what consumers are willing and able to pay for a good or service (demand curve) and the total amount they do pay (price per unit x quantity)

How is consumer surplus shown on a graph?

area underneath the demand curve and above the market price

Changes in consumer surplus

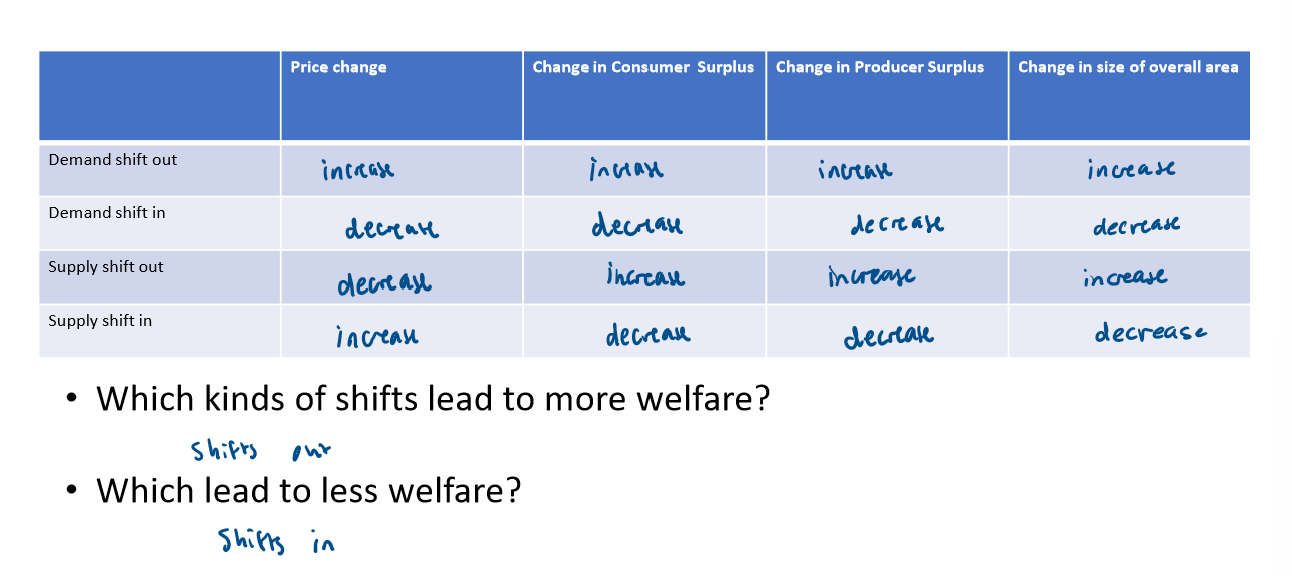

when supply shifts in consumer surplus decreases (area is smaller)

when demand shifts out consumer surplus increases (area is bigger)

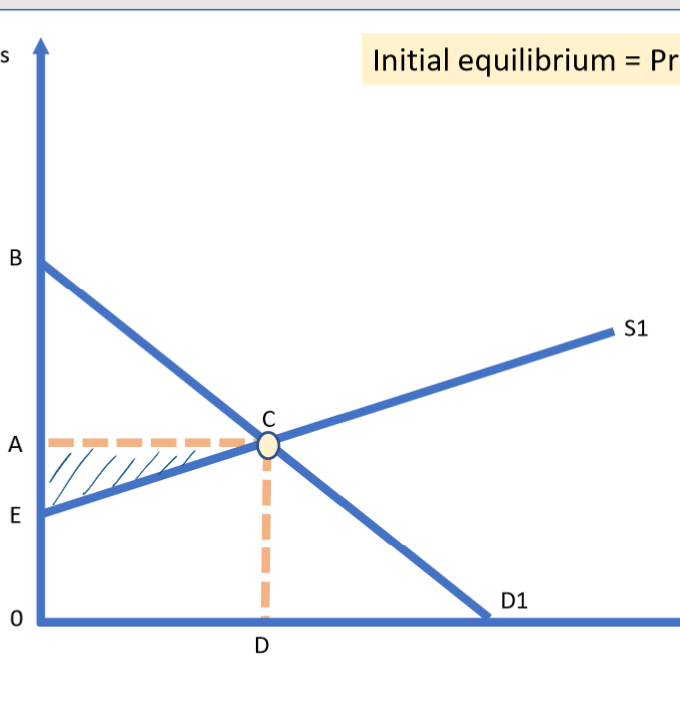

What is producer surplus?

the difference between the price producers are willing and able to supply at and the price they receive in the market

How is producer surplus shown on a graph?

the area above the supply curve and below the market price

What is social surplus?

consumer surplus + producer surplus

How do shifts impact overall surplus?

shifts out in both supply and demand curve lead to more welfare and increased overall surplus

How does PED impact consumer surplus?

when demand is inelastic there is a greater consumer surplus as there are some buyers willing to pay a very high price to continue consuming the product

What is the difference between a direct and indirect tax?

direct tax - tax on income

indirect tax - tax on expenditure

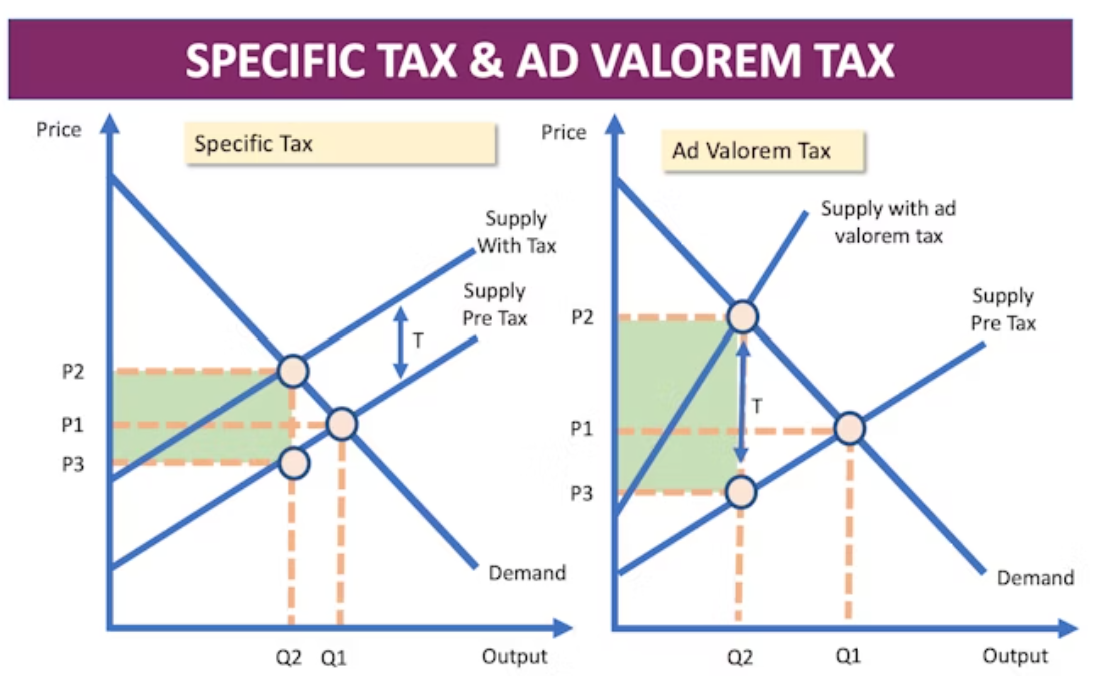

What is tax revenue and how do you calculate it?

revenue received by the government from the tax

tax per unit x quantity

What is producer revenue and how do you calculate it?

income from sales

price x quantity

What is consumer tax burden?

difference between the original market price and the new market price x quantity

What is producer tax burden?

tax revenue - consumer burden

What is the difference between a specific and Ad Valorem tax?

specific - fixed tax per unit regardless of price

ad valorem - tax which is a percentage of the price

Why do we have taxes?

revenue source for government to fund public services etc

reduce income inequality

reduce consumption of demerit goods

help to address market failure

improve a country’s trade balance

What are excise duties?

indirect taxies levied on three major demerit goods: alcohol, tobacco and road fuels

What is a regressive tax?

a tax which takes a higher percentage of someone’s income from those on low incomes

Why would a a government give out subsidies?

encourage consumption of merit goods by increasing supply

to protect domestic industries from threat of foreign competition

maintain or increase revenues of producers

reduce costs of investment which will stimulate long term economic development in a country

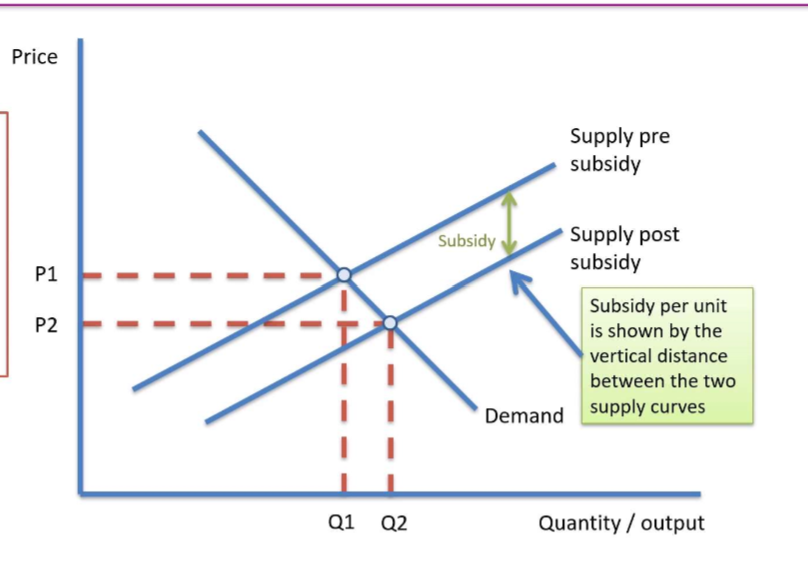

What is the impact of a subsidy and diagram?

supply shifts out

price decreases

output increases

What is consumer and producer subsidy?

consumer subsidy - encourages consumers to purchase more of a particular good or service. affects demand but does not shift supply curve

producer subsidy - lower cost of production for the firm. shifts the supply curve

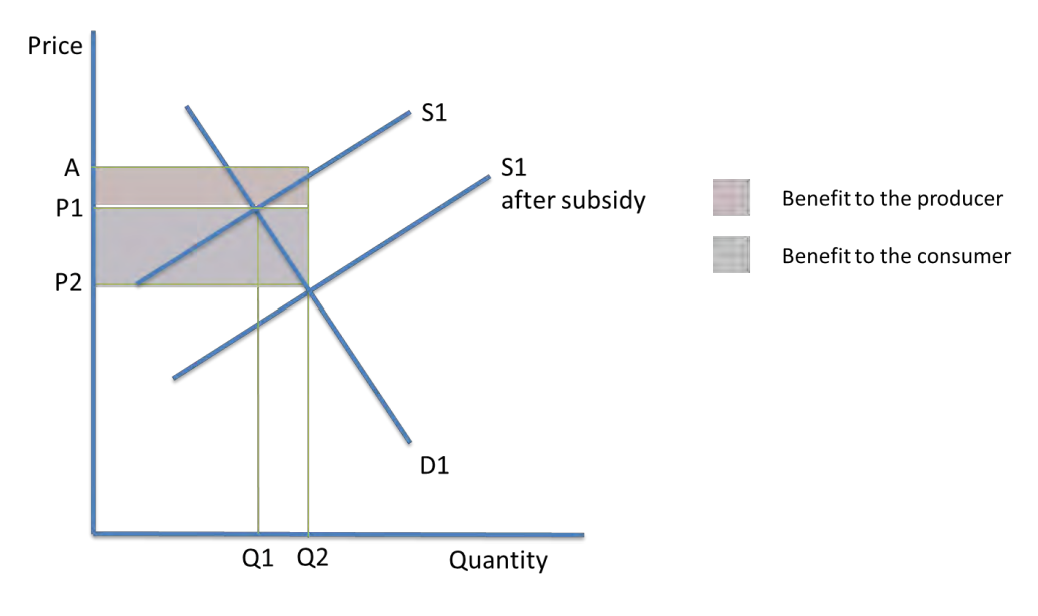

How can subsidy be calculated from a graph?

subsidy per unit: vertical difference between supply curves

consumer subsidy: area - diff between old and new price x output

producer subsidy: area - diff between old price and new equilibrium point x output

total subsidy: area of producer + consumer subsidy

What are three reasons consumers may not behave rationally?

habitual behaviour

weakness at computation

influence of other people’s behaviour

How does the influence of other people’s behaviour affect consumer decisions?

Consumers may follow social norms, influencers, trends, or peer pressure, leading to irrational decision-making and herd behaviour