Lesson 2.9: Pure Competition and Monopolies

1/16

Earn XP

Description and Tags

Flashcards made from a presentation segment created as a lesson on pure competition and monopolies.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

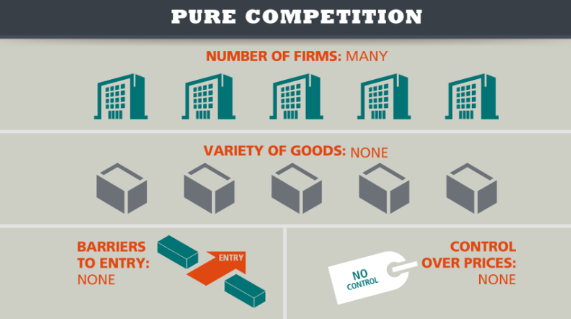

Pure competition

A market structure where:

There is a large number of firms

There is one main, same product

There is little price control in the market

The market is in equilibrium

Imperfect competition

A market structure that fails to meet the conditions of perfect competition

Commodity

A product that is considered the same no matter who sells it

Barrier to entry

Any factor that makes it difficult for a new form to enter a market

Can lead to imperfect competition

Includes start-up costs and technology

Start-up costs

The expenses a new business must pay before it can begin to produce or sell goods

Higher amounts can make it difficult for new firms to enter the market, leading to imperfect competition

Can include complex or expensive technology

Perfect competition

A market where all transactions are efficient as competition keeps prices and production costs low through resource maximization and proper market valuation

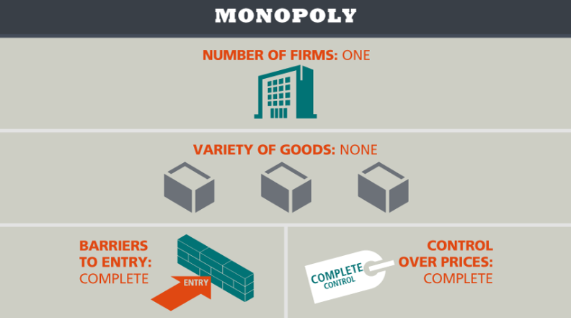

Monopoly

A market in which a single seller dominates

Can be legalized, as is the case for governments allowing drug development companies to accrue more revenue

Has usually one firm, no variety, controlled prices, and high barriers to entry

Natural monopoly

A market that runs most efficiently when one large firm suppplies all output

Adding more firms will drive down the price of both firms’ products, eventually leading both to an inability to pay their initial costs

Seen with residential water companies having only one network connected to each house in an area

Government monopoly

A monopoly created or sanctioned by the government

Patents and franchises are included in this category

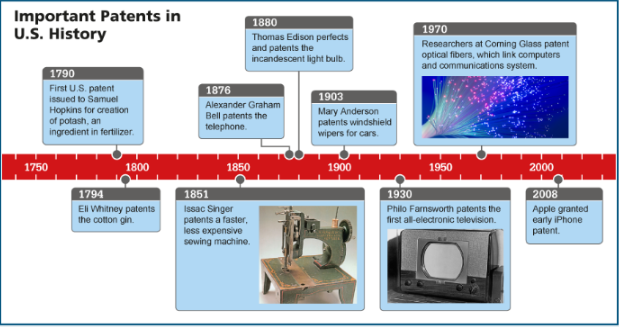

Patent

A license that gives the inventor of a new product the exclusive right to sell it for a specific period of time

Franchise

A contract that gives a single firm the right to sell its goods within an exclusive market

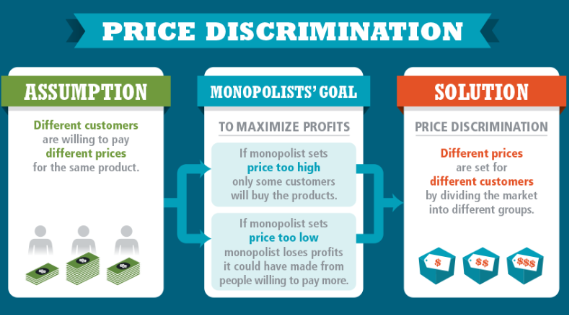

Price discrimination

The division of consumers into groups based on how much they will pay for a good

Market power

The ability of a company to control prices and total market output

Patent

A governmentally-granted exclusive right to sell a new good or service for a particular period of time

License

A permit to operate a business, especially where scarce resources are involved

Monopolist’s Dilemma

Situation where a producer with complete control of a good has to set price and production at equilibrium

More production will lead to lower prices and thus falling revenue

Less production will lead to higher prices and thus lost potential revenue

Price discrimination

Practice where a monopolist may be able to divide consumers into two or more groups and charge a different price to each group for more revenue

Requires significant market power, distinct customer groups, and difficult resellability