Micro (ECON1001)

1/37

Earn XP

Description and Tags

Flashcards covering key economic concepts related to production, costs, market demand, and opportunity costs.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

38 Terms

Scarcity

The condition of having limited resources to meet unlimited wants.

Opportunity Cost

The value of the next best forgone alternative when making a choice.

Ceteris Paribus

A Latin phrase meaning 'all other things being equal'; used to isolate the impact of one factor.

Marginal Analysis

Examination of the additional benefits and costs of a decision.

PPF (Production Possibility Frontier)

A graph showing the maximum output combinations of two goods that can be produced with available resources.

Absolute Advantage

When a party can produce more of a good or service than another party using the same resources.

Comparative Advantage

When a party can produce a good or service at a lower opportunity cost than another party.

Marginal Benefit

The additional benefit received from consuming one more unit of a good or service.

Diminishing Marginal Benefit

The decrease in additional satisfaction gained from consuming additional units of a good.

Market Demand Curve

A curve derived from summing the individual demand curves at each price level.

Fixed Costs

Costs that do not vary with the level of output.

Variable Costs

Costs that vary with the quantity of output produced.

Marginal Cost

The increase in total cost that arises from producing one additional unit.

Long Run Average Cost (LRAC)

The average cost per unit of output when all inputs are variable.

Economies of Scale

Cost advantages that a firm experiences as it increases output.

Diminishing Marginal Product

A reduction in the additional output gained from increasing an input.

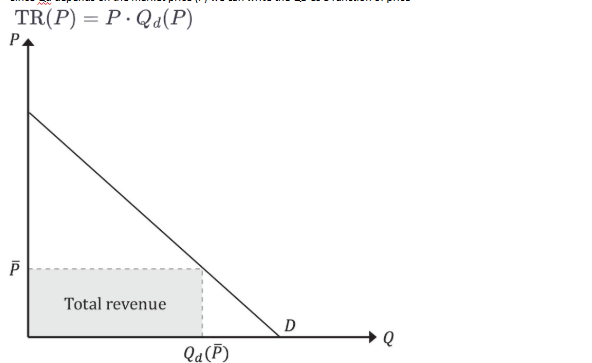

Total Revenue (TR)

The total income generated from selling goods or services, calculated as price times quantity.

Economic Profit

Profit calculated as total revenue minus total costs.

What is the difference between correlation and causation?

Correlation indicates a relationship between two variables, while causation implies that one variable directly affects or causes a change in another.

(W4) Consumer surplus

The difference between what consumers are willing to pay for a good or service versus what they actually pay.

Producer surplus

The difference between the amount producers are willing to accept for a good or service versus the actual price they receive.

Value of Time Savings

The monetary estimate of the benefits derived from reduced travel time, calculated per person per hour.

At a given market price a firm should sell up until…

P = MC

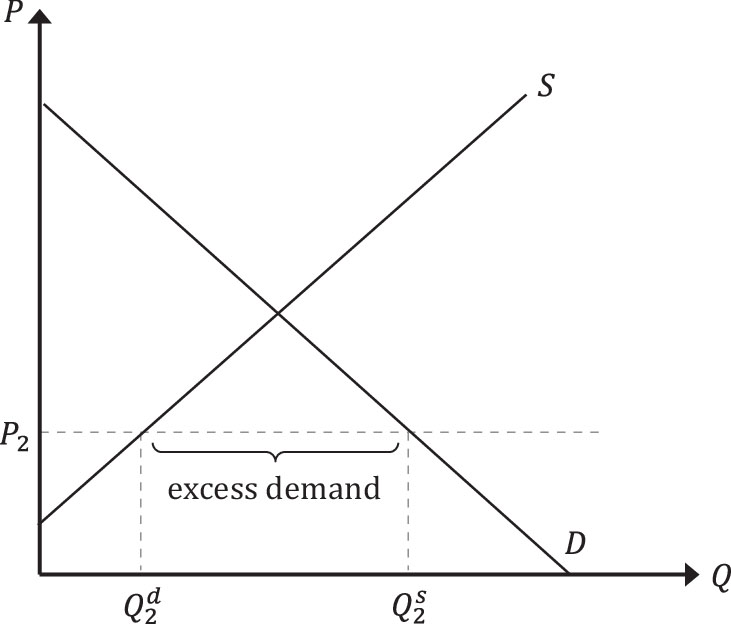

(W5) Explain this figure

At P2 there is not enough QS to fulfil QD

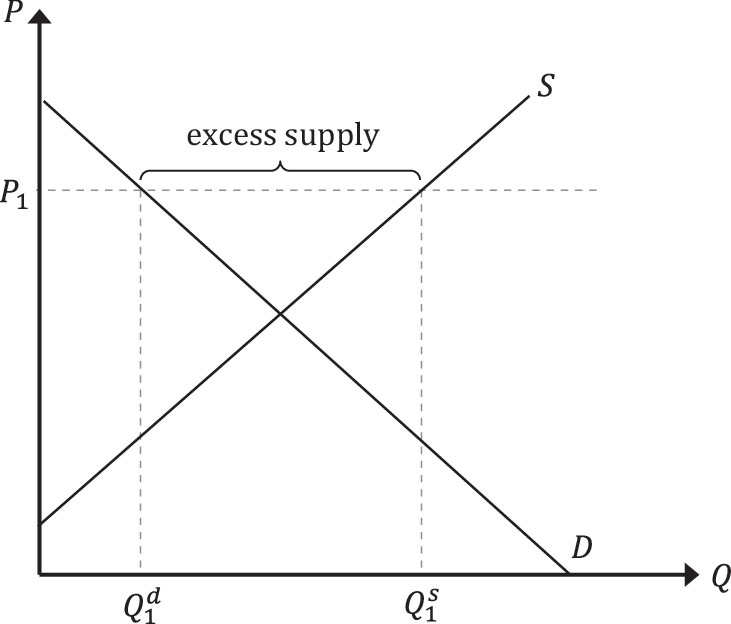

Explain this figure

At price P1 the QD does not meet QS, resulting in excess supply

What is comparative static analysis?

How the market equilibrium is affected by the change or event

What is a welfare analysis?

how consumers and firms benefit within markets

What is pareto efficiency?

When it is not possible to make someone better off without making someone else worse off

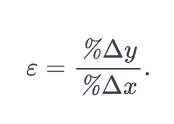

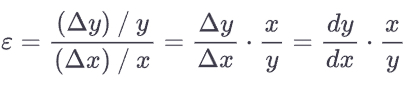

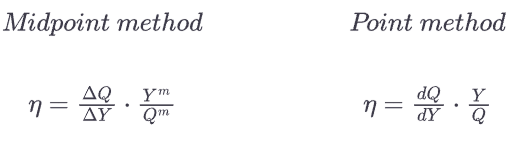

What is the basic elasticity formula (not point or arc method)

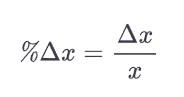

How do you find the proportional change (%) of a variable

How do you find elasticity at a single point

With the point method

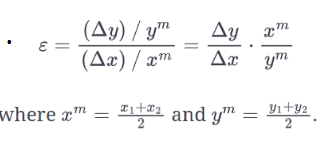

How to find elasticity moving from one point to another

Midpoint (arc) method

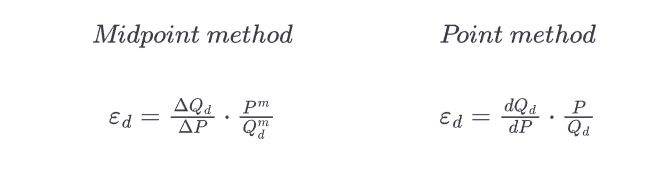

How to find elasticity of demand in both the midpoint and point method?

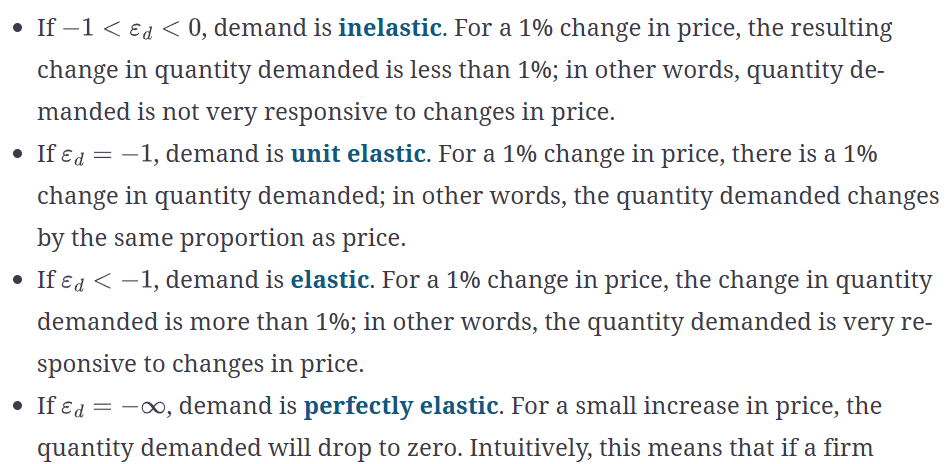

At what point is demand inelastic, elastic, unit elastic and perfectly elastic

How would we find how a total revenue in the market will change as price changes?

How do you find the cross price elasticity (how sensitive the QD of good A is to changes in price of good B) in both point and midpoint method?

How do you find income elasticity (how sensitive the QD of a good is (Q) to changes in income (Y)) in both the point and midpoint method?

Characterise all types of goods

If n < 0, demand for a good decreases when income rises, this is an inferior good

If n = 0, demand for the good does not change when income rises, this is an neutral good

If 0 < n < 1, when income rises by 1% demand for the good increases by less than 1%, this is a normal good

If n > 1, when income rises by 1%, demand for the good increase by more than 1%, this isi a luxury good