Business Tax (Trading Profits, Income Tax)

1/13

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

14 Terms

Calculating trading profits

trading profit/loss =

Chargeable receipts − deductible expenses − capital allowances

sequence:

[company only] 1. full expensing (can be bought to lease out)

2. AIA (1M)

3. 40% FYA

4. 18% WDA on existing pool

_

-FYA - new stuff, can be bought to lease out. excess goes to pool subsequent year

![<p>trading profit/loss =<br><strong>Chargeable receipts − deductible expenses − capital allowances</strong><br><br><u>sequence:</u><br>[company only] <strong><em>1. full expensing </em></strong><em>(can be bought to lease out)</em><br>2. <strong>AIA </strong>(1M)<br>3. <strong>40% FYA</strong> <br>4. <strong>18% WDA </strong>on existing pool<br>_<br>-FYA - <em>new stuff, can be bought to lease out. excess goes to pool subsequent year</em></p>](https://assets.knowt.com/user-attachments/ad36a793-23e3-4b1e-9498-fe6047d3e036.jpg)

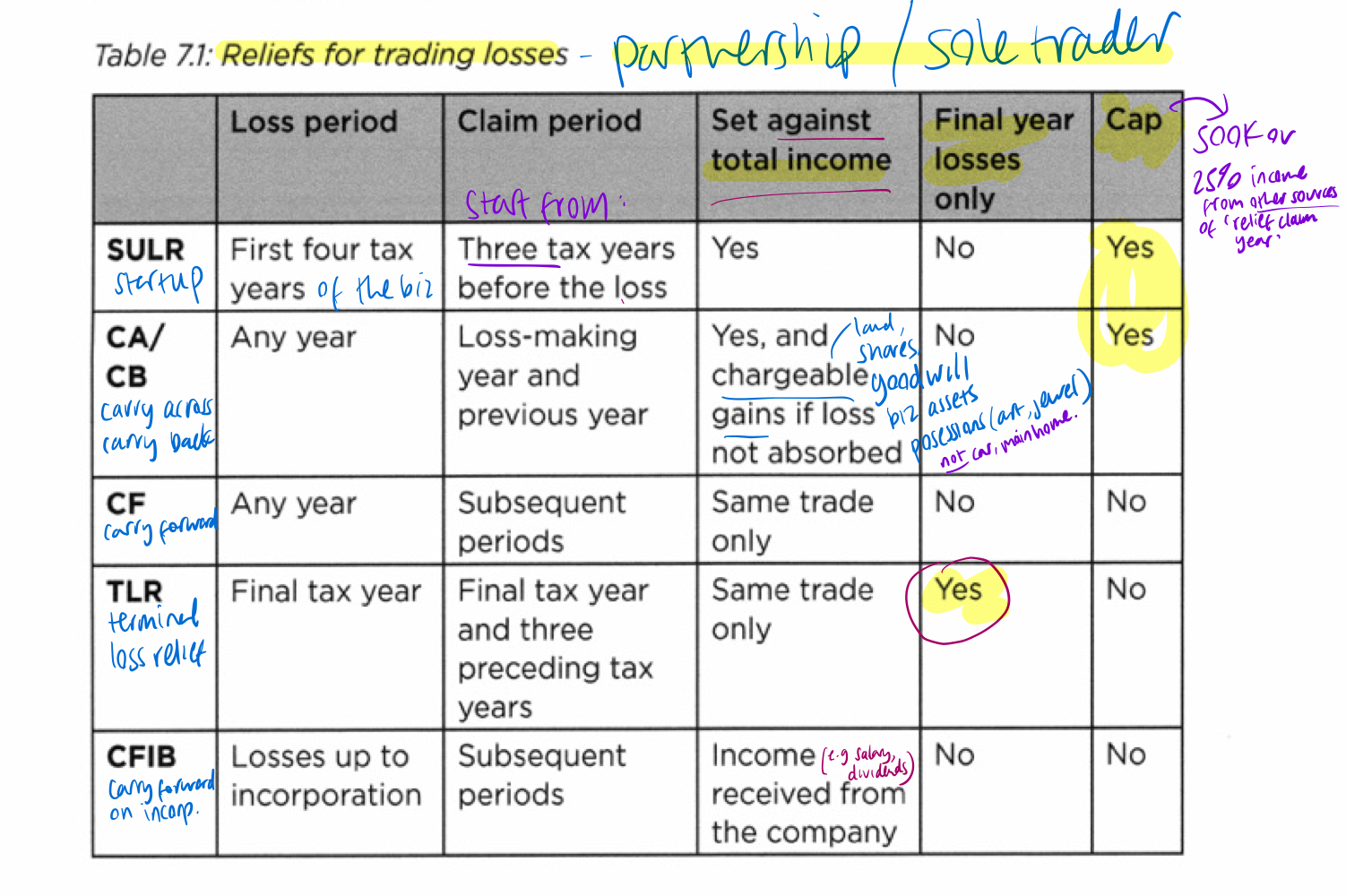

Trading losses — unincorporated businesses overview

TABLE: reliefs for trading losses

_

Additional points:

• Cap applies only to SULR + CA/CB: greater of:

→£50,000 or

→25% of taxpayer's income from other sources in the relief claim year.

• These reliefs apply to sole traders + individual partners.

• For partnerships, each partner chooses relief separately for their own share of the loss.

• Reliefs are not automatic → taxpayer must claim.

• Same loss cannot be relieved twice.

• If one relief only uses part of the loss, another relief can be used for the balance.

• "Claim period" in the table means the tax years/income the loss can be set against — not the filing deadline.

_

Exam shortcut:

• start-up loss → SULR

• any-year loss against current/previous income → CA/CB

• business continues → CF

• business ends → TLR

• business incorporates → CFIB

Trading losses — general principles

A sole trader or individual partner may get tax relief for trading losses.

Effect:

• relief reduces taxable income, gains, or future trading profits

• this can reduce tax payable or produce a tax repayment

_

Key points:

• reliefs are not automatic → taxpayer must claim

• if more than one relief is available, taxpayer can choose the most useful one

• same loss cannot be relieved twice

• if one relief only absorbs part of the loss, another relief may be used for the remaining loss

Partnership point:

• each partner claims relief separately for their own share of partnership loss

• different partners may choose different reliefs depending on their personal income/tax position

_

Exam approach:

Ask what happened to the business:

• new business?

• continuing business?

• final year / ceasing trade?

• incorporated into company?

Start-up loss relief / early trade losses relief

Use where trading loss arises in the first 4 tax years of a new trade.

Effect:

• loss can be set against total income of the 3 tax years before the loss

• set against earliest year first

• useful where taxpayer had taxable income before starting the business, e.g. previous salary, previous business, rental income

Example:

Business starts in 2019/20 and makes first-year loss.

SULR can look back to:

• 2016/17

• 2017/18

• 2018/19

Use 2016/17 first, then move forward.

Other points:

• cap applies

• claim deadline = first anniversary of 31 January following end of loss-making tax year

Exam point:

Start-up + loss in first 4 tax years + previous taxable income = think SULR.

Carry-across / carry-back relief

Use where trading loss arises in any year.

Effect:

• loss can be set against total income of the loss-making tax year → carry-across

• loss can be set against total income of the previous tax year → carry-back

Taxpayer can choose order:

• loss year first, then previous year; or

• previous year first, then loss year

Chargeable gains point:

• if carry-across does not absorb the full loss, balance can be set against chargeable gains in the same tax year

Practical downside:

• loss is set against total income

• this may reduce income to zero and waste the personal allowance

Other points:

• cap applies

• claim deadline = first anniversary of 31 January following end of loss-making tax year

Exam point:

Any-year loss + current/previous total income = think CA/CB.

Carry-forward relief

Use where trading loss arises in any year and the same trade continues.

Effect:

• loss is carried forward

• loss is set against future profits of the same trade only

• earlier future years used first

• loss can be carried forward indefinitely until absorbed

Other points:

• no cap applies

• taxpayer must notify HMRC no more than 4 years after end of loss-making tax year

Practical effect:

• good where business is expected to become profitable later

• less useful if the trade never makes future profits

Example:

• Year 1 sole trader loss = £30,000

• Year 2 same trade profit = £50,000

• £50,000 − £30,000 = £20,000 taxable trading profit

Exam point:

Business continues + future same-trade profits = CF.

Terminal loss relief

Use where trading loss arises in final tax year / final year of trade.

Effect:

• loss can be set against profits of the same trade only

Claim period:

• final tax year

• 3 preceding tax years

Order:

• set against later years first

Other points:

• no cap applies

• claim deadline = no more than 4 years after end of loss-making tax year

Practical effect:

• business is ending, so normal carry-forward relief will not help

• TLR lets taxpayer look backwards and reclaim tax paid on earlier same-trade profits

Example:

Business stops in 2024/25 and makes terminal loss.

Use against same-trade profits in:

• 2024/25 first

• then 2023/24

• then 2022/23

• then 2021/22

Exam point:

Final year loss + business ceasing = TLR.

Carry-forward relief on incorporation of business

Use where an unincorporated business is transferred into a company.

Applies to:

• trading losses up to incorporation that have not been relieved

Conditions:

• business must be transferred wholly or mainly in return for shares; shares must be 80%+ of the consideration

Effect:

• loss can be carried forward

• loss can be set against income taxpayer receives from the company, e.g. → salary → director's fees → dividends

Other points:

• no cap applies

• claim deadline = no more than 4 years after end of loss-making tax year

Practical effect:

• after incorporation, taxpayer personally no longer earns sole trader profits from that business

• the company earns the trade profits instead

• CFIB lets old personal trading losses reduce the taxpayer's future personal income from the company

Exam point:

Old unincorporated loss + business becomes company + 80%+ shares = CFIB.

Trading loss reliefs — cap + claim deadlines

Cap applies only to:

• SULR

• CA/CB

Cap = greater of:

• £50,000; or

• 25% of taxpayer's income from other sources in the tax year for which relief is claimed

No cap applies to:

• CF

• TLR

• CFIB

_

Claim / notification deadlines:

SULR + CA/CB:

• claim by first anniversary of 31 January following end of loss-making tax year

Example:

• loss in 2019/20

• tax year ends 5 April 2020

• following 31 January = 31 January 2021

• first anniversary = 31 January 2022

• deadline = 31 January 2022

CF:

• notify HMRC no more than 4 years after end of loss-making tax year

TLR + CFIB:

• claim no more than 4 years after end of loss-making tax year

Exam point:

• cap = how much relief can be used

• deadline = when relief must be claimed/notified

VAT

20%

VAT registration threshold = £90,000 in any 12-month period.

VAT = "charged on any supply of goods or services made in the United Kingdom, where it is a taxable supply made by a taxable person in the course or furtherance of any business carried on by him".

VAT calculation:

• output tax − input tax = VAT payable to HMRC

• output tax = VAT business charges customers

• input tax = VAT business pays on its own purchases, e.g. raw materials

• if input tax exceeds output tax → business may get rebate

_

VAT registration:

• anyone making taxable supplies of more than £90,000 in any 12-month period must register and charge VAT

• below threshold → voluntary registration possible if making taxable supplies

• cannot register if business only makes exempt supplies

• exception / crossover = zero-rated business does not effectively charge VAT to customer, but can still recover input VAT

• examples of zero-rated businesses: bookshop, supermarket selling non-catering food

_

Exempt supplies:

• examples: health, education, insurance, residential land

• no VAT charged

• cannot register if only exempt supplies

• cannot recover input tax if only exempt supplies

_

Zero-rated supplies:

• examples: non-catering food, books, water

• VAT charged at 0%

• still a taxable supply

• business can register for VAT

• business can recover input tax

_

VAT invoices:

• VAT-registered business making taxable supply to taxable person must issue VAT invoice

• invoice should include VAT number, value of supply, and rate of VAT

_

Returns/payment:

• VAT return usually submitted quarterly

• VAT paid within 1 month from end of quarter

• full VAT records must be kept

_

• business supply of goods/services in UK → check VAT

• taxable supply + taxable person + VAT registration = charge VAT

• output tax − input tax = amount due to HMRC

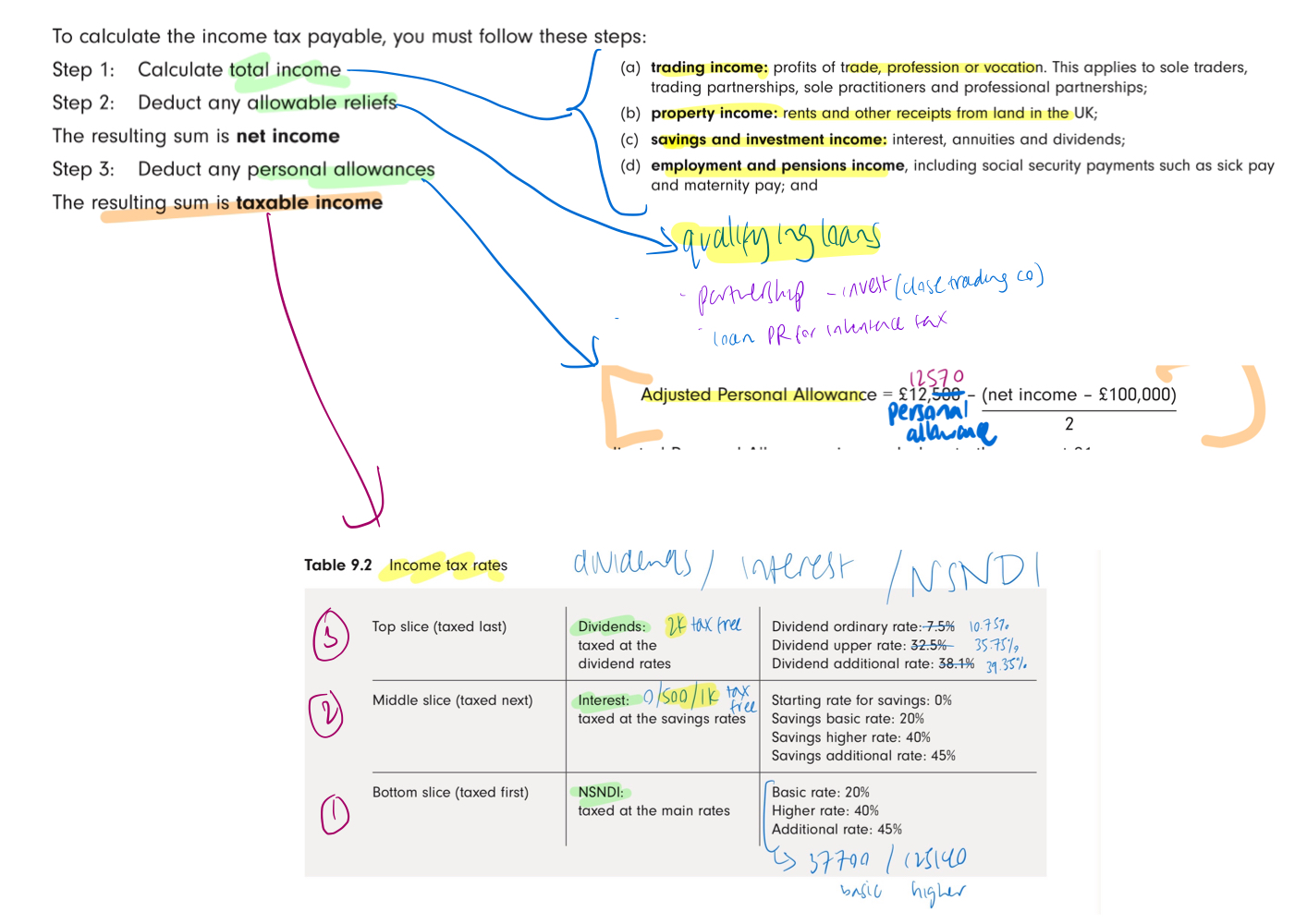

*INCOME TAX - calculation (individual)

see diagram

_

Income tax bands as of 2026/27:

• personal allowance = £12,570

• basic rate band = first £37,700 of taxable income

• higher rate band = taxable income above £37,700 - £125,140

• additional rate = taxable income above £125,140

_

Income tax calculation structure:

• Step 1: calculate total income

↳ aggregate gross income from each source.

• Step 2: deduct allowable reliefs

↳ result = net income.

• Step 3: deduct personal allowance

↳ result = taxable income.

• Step 4: tax each source separately

↳ NSNDI first, savings income next, dividends last.

• Step 5: add the tax due and deduct tax already paid/deducted at source.

_

Income categories:

• NSNDI = non-savings, non-dividend income

↳ employment income, trading income, property income, pensions.

• savings income

↳ interest.

• dividend income

↳ dividends from shares.

_

NSNDI rates:

• basic rate = 20%

• higher rate = 40%

• additional rate = 45%

_

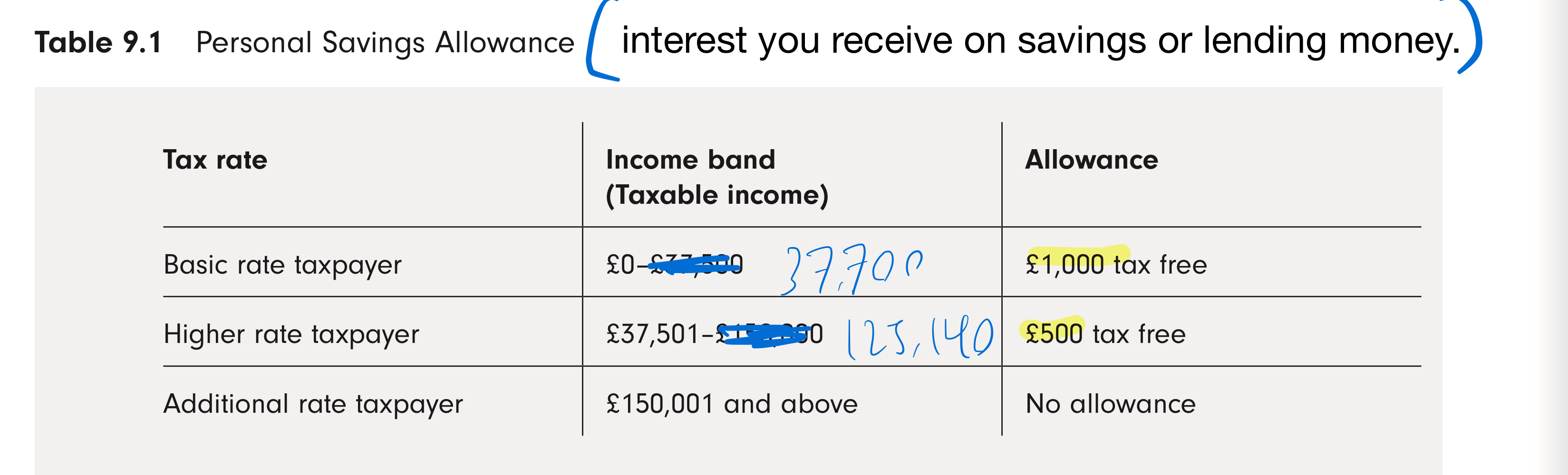

Savings income rates:

• starting rate for savings = 0% on £0/500/1000*

• savings basic rate = 20%

• savings higher rate = 40%

• savings additional rate = 45%

• *personal savings allowance:

↳ basic rate taxpayer = £1,000 at 0%

↳ higher rate taxpayer = £500 at 0%

↳ additional rate taxpayer = £0

_

Dividend income rates as of 2026/27:

• dividend allowance = £500 at 0%

• ordinary/basic dividend rate = 10.75%

• upper/higher dividend rate = 35.75%

• additional dividend rate = 39.35%

_

NB PSA and dividend allowance are nil-rate bands, not deductions.

They are taxed at 0%, but still count towards the cumulative income bands.

income tax:

adjusted personal allowance - formula ?

other allowances ?

Personal allowance is reduced when net income exceeds £100,000. FORMULA

marriage - 1250 transferable

blind 1250

gross trading property income - first 1k tax free

PSA personal savings allowance (interest on savings/lending) - 0/500/1000 tax free depending on income bracket

dividend allowance - first 2k tax free

personal savings allowance thresholds (first X tax free)

0/500/1000

income tax rates

NSNDI, interest, dividends

NSNDI = 20 / 40 / 45

interest = 0 starting rate, then 20 / 40 / 45

dividends = 10.75 / 35.75 / 39.35