Topic 11: Standard costing and variance analysis

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

29 Terms

standard costing

enables derivations from budget to be calculated and analysed

typically applied in cost centres

standard costs

predetermined costs that should be incurred under efficient operating conditions

CPU

standard v budget

standard = CPU while budget = total

how dow standard costing systems work?

input required to produce a unit of output can be specified

fast food restaurants

banks - loan applications

must be a repetitive activity to set standard

can have a verity of products as long as they are similar operations

Product standard costs

found by combining the standard costs from the operations necessary to make the product

price standard

the amount that should be paid for each unit of input

quantity standard

the amount of input that should be used per unit of output

who acts on the variance of standard costing

•The accountant identifies variances, and the responsible managers investigate the reasons for the variance.

This should result in appropriate remedial action being taken, or perhaps the standard should be changed

what are the two approaches of cost standards

historical records

widely used

doesnt focus on finding best combination of resources

engineering studies

detailed study of each operation with careful specs of material, labour, and equipment

direct material standards

derived from input quality necessary

establish the most suitable materials for the operation

optimal quality should be used, taking into account unavoidable wastage/loss

material quantity standards

recorded on a bill of materials

shows required quantity of materials for reach operation to complete product

Standard material product cost

multiplying standard quantities by appropriate standard prices

standard prices

obtained from purchasing department

must select suppliers who can provide P & Q

direct labour standards

standard labour time

eliminate unnecessary elements and determine most efficient method

smite # of hours to complete

unavoidable delays are included - machine breakdown and routine patience

standard labour cost

contractual wage rates

why standard costing?

decision making purposes

provides prediction of future costs

preferrable to estimates based on adjusted past costs which may incorporate inefficiencies

challenging target

motivates individuals

Research evidence suggests that the existence of a defined quantitative goal motivates higher levels of performance.

setting budgets

evaluating managerial performance

control device

hihglihts non conforming activities that need corrective action

profit measurement and inventory valuation purposes

variance

the difference between standard and actual cost

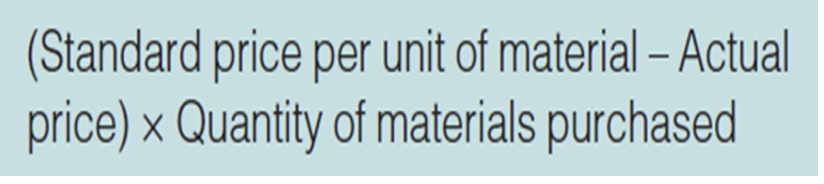

material price variance

adverse

failure to get best source of supply

change in market conditions

favourable

inferior quality goods,

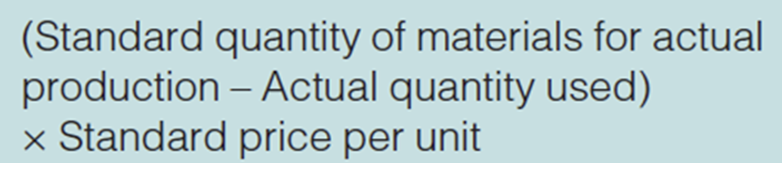

material usage variance

Did we use more or less materials than the standard?

controllable by manager

carless handling

purchase of inferior quality

pilferage

changes in quality control

changes in methods of productions

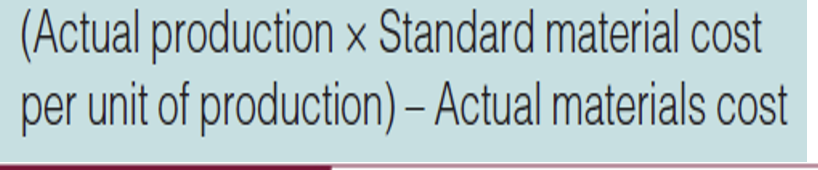

total material variance

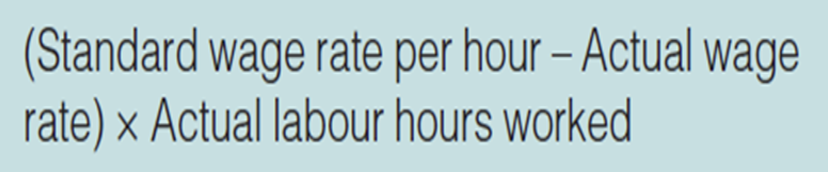

wage rate variance

Did we use more or less materials than the standard?

least subject to control by management

changes in wage rate standards

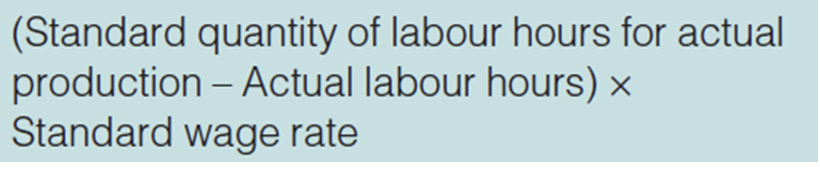

labour efficiency variance

Were our employees more or less efficient than the standard?

controllable by manager

inferior quality materials

failure to maintain machinery

introduction of new equipment/tools/processes

total labour variance

variable overhead expenditure variance

•Did we pay more or less for our variable overheads than the standard?

variable overhead efficiency variance

•The difference between actual and budgeted hours worked, applied to the standard variable overhead rate per hour.

total variable overhead variance

changes due to prices of individual items changing

can be affected by efficiency

not very informative

need comparison of actual expenditure against each line time

fixed overhead

Did we pay more or less for our fixed overheads compared to the budget?

budgeted - actual overheads

sales margin price variance

Did we sell our products for more or less than the standard?

sales margin volume variance

Did we sell our products for more or less than the standard?

total sales margin variance

•It may not be very meaningful to analyse the total sales margin variance into price and volume components, since changes in selling prices are likely to affect sales volume.

•A favourable price variance will tend to be associated with an adverse volume variance, and vice versa.

•A further problem: the sales variances may arise from external factors not controllable by management. E.g. changes in selling prices may be a reaction to changes in selling prices of competitors.

•Alternatively, a reduction in both selling price and sales volume may be the result of an economic recession.

•For control and performance appraisal it may be preferable to compare actual market share with target market share for each product.

•