Economic ISL Year10

1/60

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

61 Terms

Want

A want is a desire however not an essential for survival

Need

A need is an essential for survival

Economic choice

A decision to purchase certain goods instead of another

List of preference

A list used to state the urgency and importance of resources

Basic Economic Problem

There are unlimited wants and needs however the number of resources are scarce/limited

Economics

Economics is the study of using limited resources to satisfy unlimited needs and wants

Free Goods

Free goods are goods with no price, plenty and have no opportunity cost

Economic Goods

Economic goods are goods that have a value, scarce, require an economic choice and have an opportunity cost

Factors Of Production(FOPs)

Land, Labour, Capital, Enterprise

LAND

All natural resources found on, above and below the earth’s surface used in production

Land Mobility

Occupationally mobile and not geographically mobile

LABOUR

Mental and physical efforts put in by workers or labourers

Labour Mobility

Occupationally mobile and highly geographically mobile

CAPITAL

All man-made resources available in an economy

Capital mobility

Occupationally mobile and geographically mobile

Enterprise

The ability to take risks and run a business

Reward for Land

Rent

Reward for Labour

Wage

Reward for Capital

Interest

Reward for Enterprise

Profit

Opportunity cost

Opportunity cost is the nest best alternative forgone/option

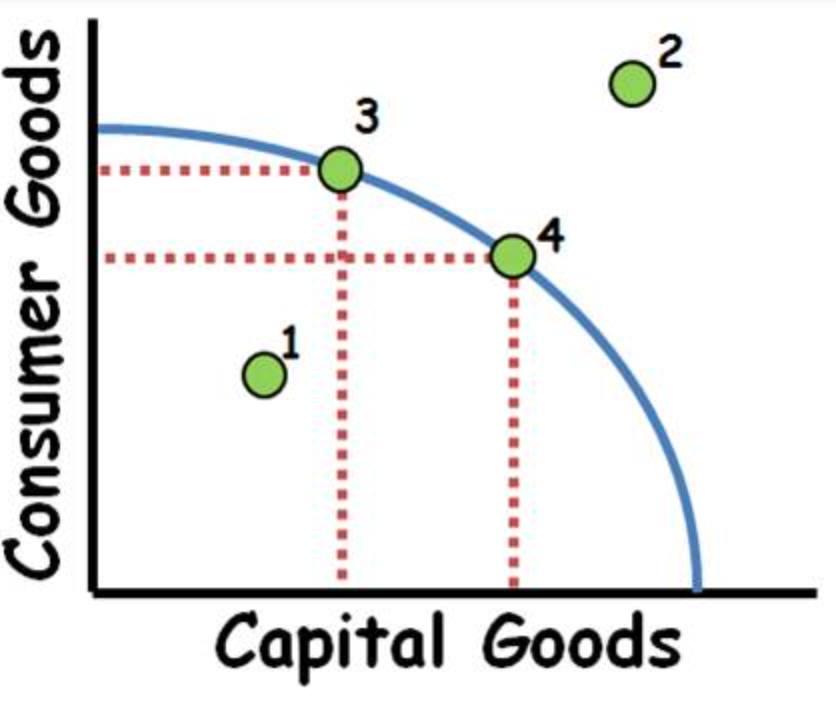

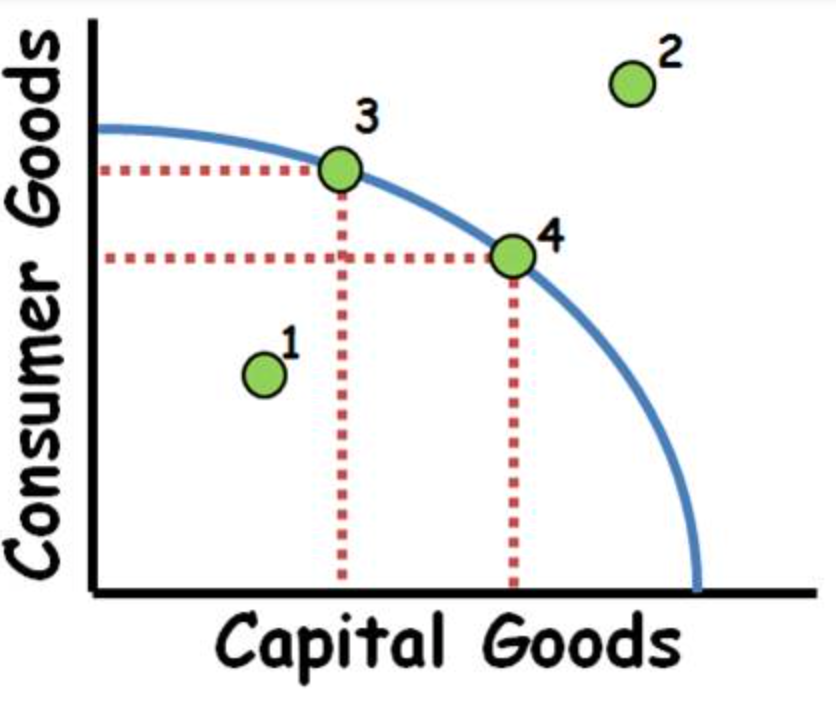

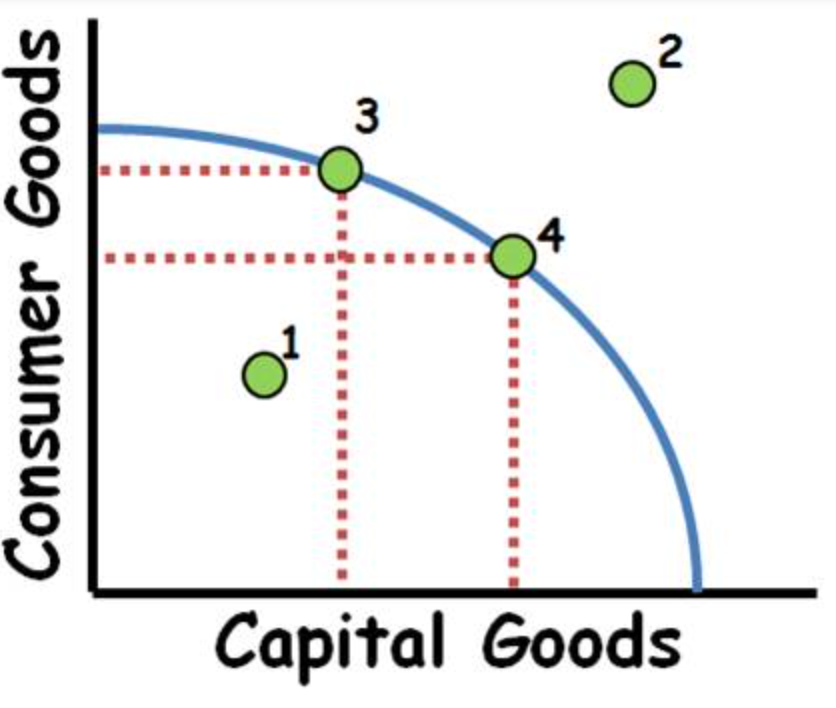

Define PPC

PPC is used to show the maximum combination of two goods that can be produces at a particular time using available resources

Expand PPC

Production Possibility Curve

Point 1

Under efficient use of resources

Point 4

Efficient use of resources

Point 2

Unattainable point

Microeconomics

The study of individual markets, microeconomic decision makers are the producers and consumers

Macroeconomics

The study of an entire economy, macroeconomic decision makers are the government

Economy

An area where people and firms produce, trade and consume goods

Market

An arrangement that enables buyers and sellers to exchange goods and services

Demand

Demand is the quantity of goods and services consumers are willing able to buy at a given price

Demand Curve

The demand curve is a graphical representation of the relationship between quantity demanded and the price

Law Of Demand

The higher the price the lower the quantity demanded and the lower the price the higher the quantity demanded

Non-Price determiners of Demand

Population, Price of other related goods, Income, Government, Fashions, Advertisement, Future price expectations

Non-Price determiners of supply

Cost of production, Government, Price of other related goods, Technological advancement, Quantity and Quality of factors of production

Equilibrium

Occurs when demand is equal to supply

Disequilibrium

Disequilibrium occurs when demand is not equal to supply

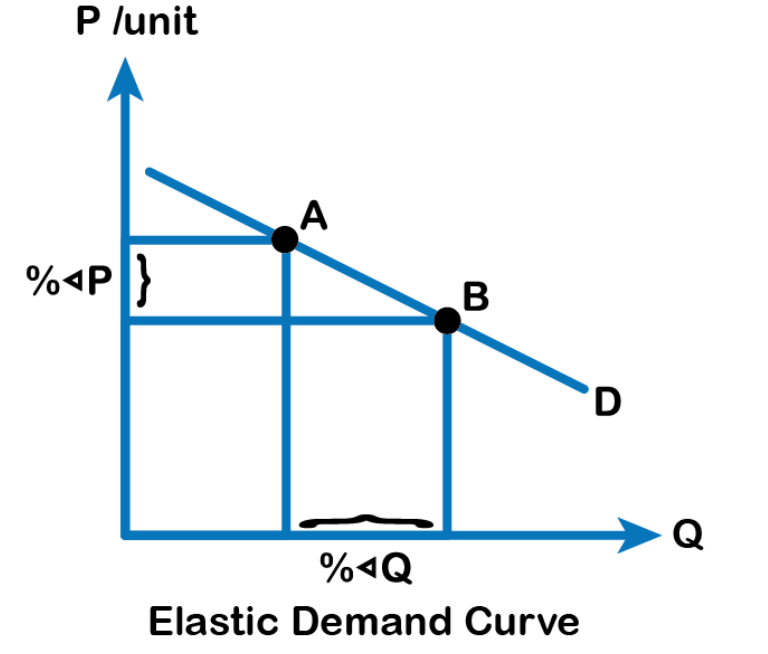

Price Elasticity

Price elasticity is the responsiveness of quantity demanded to the changes in price

Types of Elasticity

Elastic and Inelastic

Elastic demand

Changes in price lead to a more than proportionate change in quantity demanded

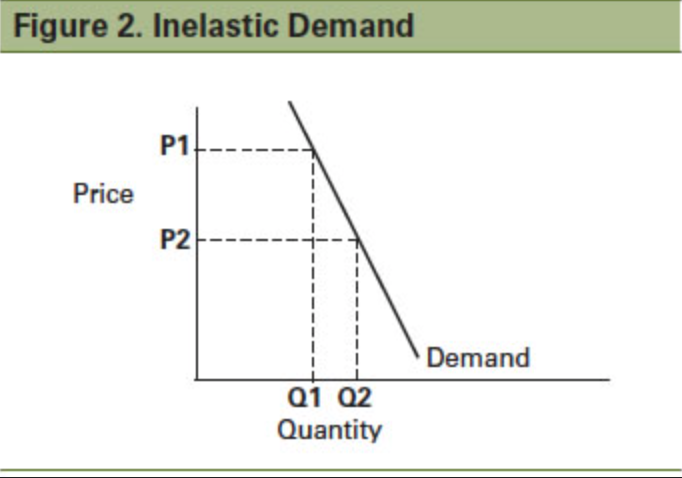

Inelastic demand

A change in price leads to a less than proportionate change in quantity demanded

Perfectly Inelastic

PED is zero

Perfectly Elastic

PED is infinite

Calculaton of PED

Percentage change in quantity/ percentage change in price

Unitary

A change in price leads to an equal change in quantity demanded

Factors determining PED

Degree of necessity, amount of income spent on product, number or closeness of substitutes, Time period

Factors determining PES

Time period, availability of resources

Price Mechanism

Price mechanism occurs as a result of changes in price in order to have equilibrium

Revenue

Revenue is the amount of money made from sales

Revenue Formula

Price x Quantity

Market failure

Market failure occurs when a market does not efficently allocate resources

Pubic Goods

Goods that cannot be produced when left to the forces of demand and supply

Merit Goods

Goods that can be under produces hence under consumed when left to the forces of demand and supply(e.g education, healthcare)

Demerit goods

Goods that can be over produced hence over consumed when left to the forces of demand and supply(e.g cigarettes)

Monopoly

A farm that is the only supplier in the market

External cost

The negative impacts on society due to production or consumption of goods and services

Private goods

Goods that are purchased before consumption

Clearance price

When surplus and shortage are equal

Causes of market failure

Social cost exceeding social benefits, over production of demerit goods, under production of merit goods, Lack of public goods, Immobility of resources, Information failure, Abuse of monopoly powers

Mixed economic system

Public and private sector co-existing together

Public sector

A company owned by the government