1.1-1.2: Introduction to Economics

1/19

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

20 Terms

Economics

The study of how society allocates scarce resources among unlimited wants and needs.

Microeconomics

How producers and consumers interact in individual markets.

Macroeconomics

Factors that affect the economy.

Cost-benefit analysis

Choose the option that gives the most utility by weighing up the pros and cons of each outcome.

Opportunity cost

The next best thing sacrificed as a result of a choice.

Trade-off

Anything given up as a result of a choice.

Free goods vs economic goods

Abundant

Scarce and competition for it exists

Incentive

Something that motivates an individual to act in a certain way.

Basic economic problem

What could be produced and how much?

How should thing be produced?

For whom should things be produced?

Rationing systems

Planned (command economy)

Government makes decisions

Resources owned “collectively”

DISAD: Lack of liberty and choice, and poor efficiency.

Free market economy

Resources and production are owned privately

Use of prices to ration g+s

DISAD: high income inequality, over provision of demerit goods, and poor use of resources

Mixed market economy

Some measure of government intervention

Four Factors of Production

Land: Provided by nature (property and resources found under the land)

Labor: All human resources

Capital: Anything made by humans

Entrepreneurship: Management that organizes the factors of production

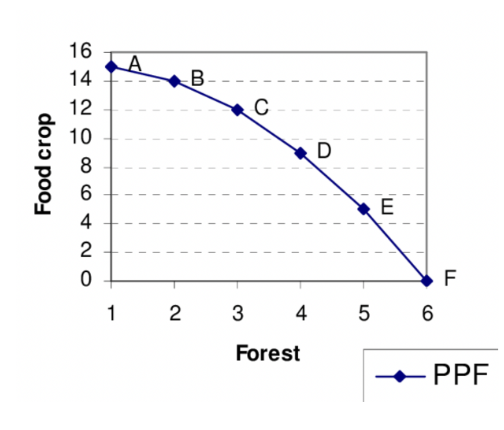

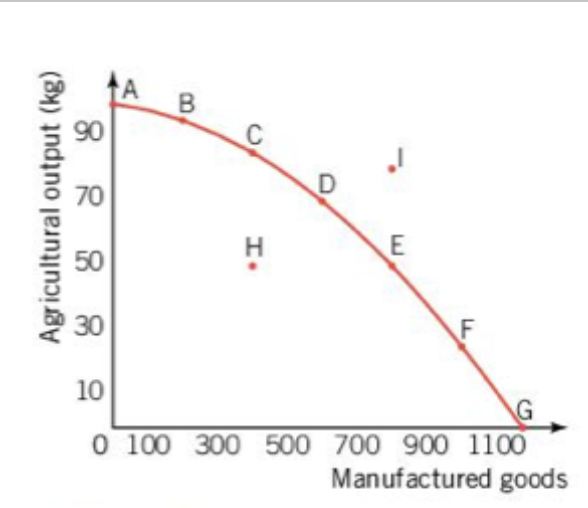

Production Possibilities Curve

Graph that shows the tradeoff between the production of different items.

Maximum combinations of two types of output that can occur if all resources are being used efficiently and technology is fixed.

Inverse relationship between two types of good (why curve is downward sloping)

The Law of Increasing Opportunity Cost:

increasing quantities of one good can only be achieved by sacrificing ever-increasing quantities of another good

PPC Curve - Points (increasing opportunity cost)

A to G:

potential output

productive efficiency exists wherein the economy is using its resources to the maximum potential

I:

not possible, exceeds the productive capability of available resources and technology

H

resources are not fully utilized

actual economic growth is shown through a movement of H towards the PPC (utilize more resources)

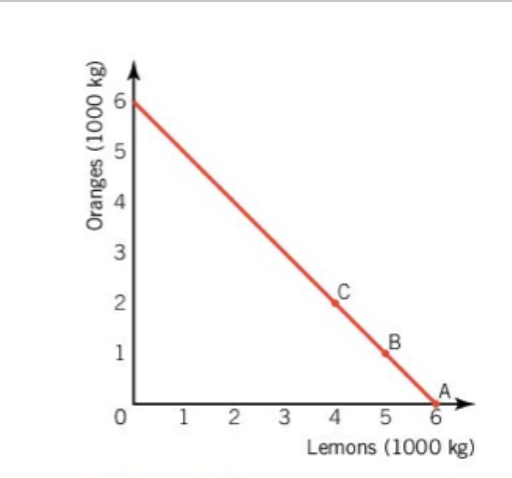

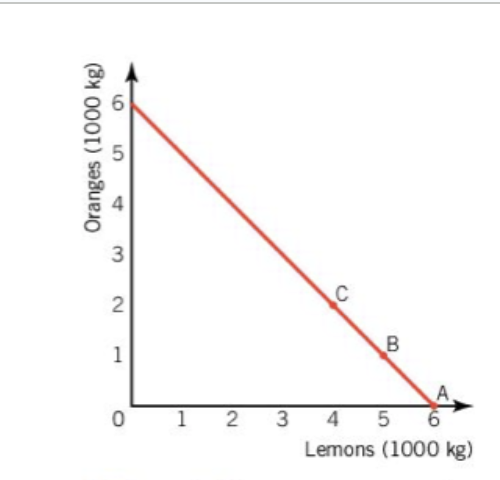

PPC Curve - constant opportunity cost

Production for producing lemons and oranges is largely the same

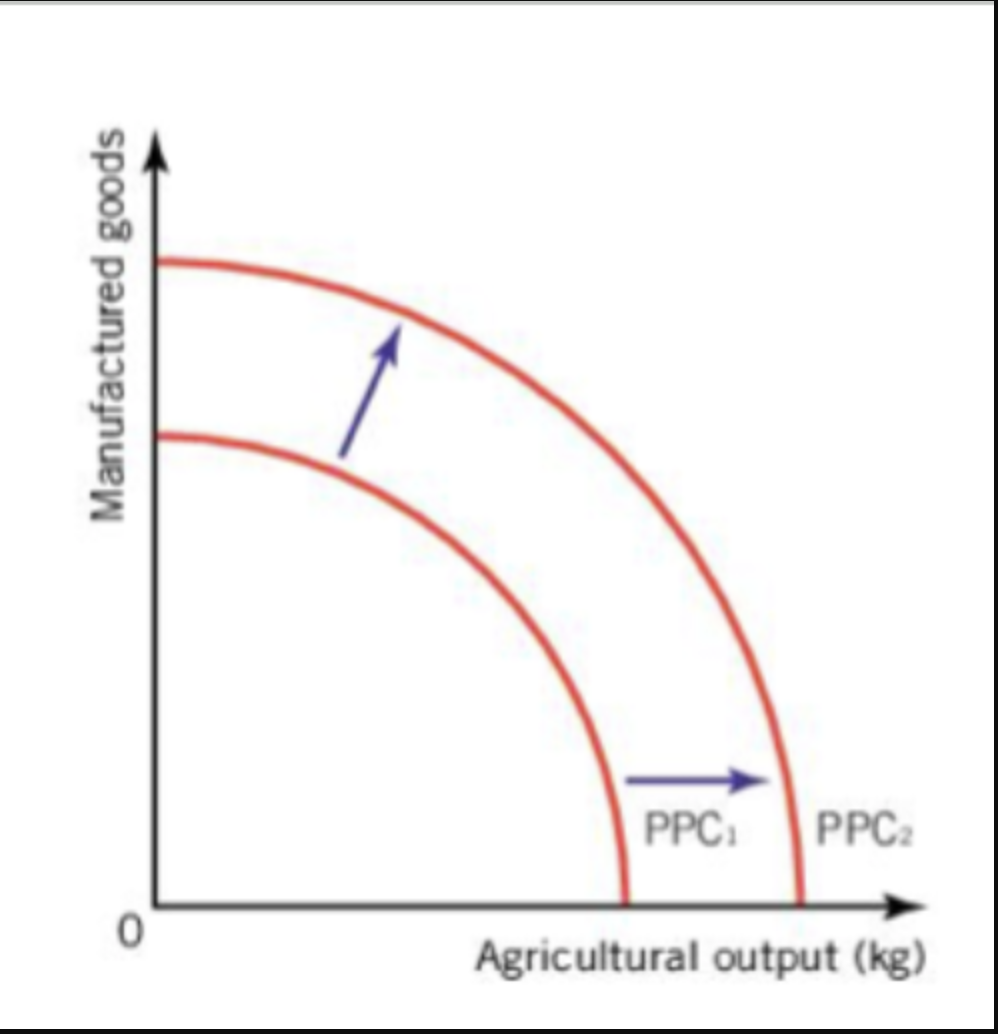

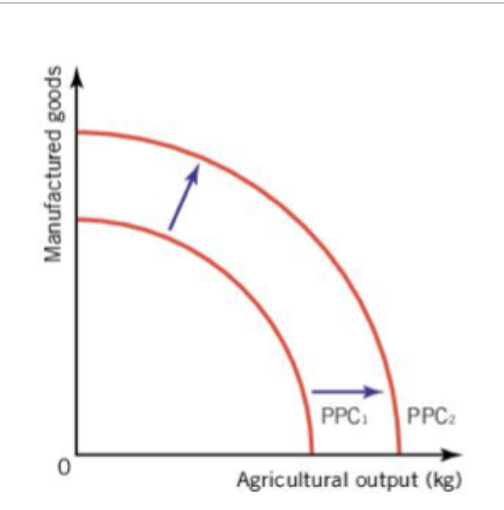

Change in production possibilities

Growth - Increase in the quality and quantity of factors of production

Improved education

Improved production technologies

New forms of energy

Reduce in quality or quantity of factors of production

Wars and natural disasters

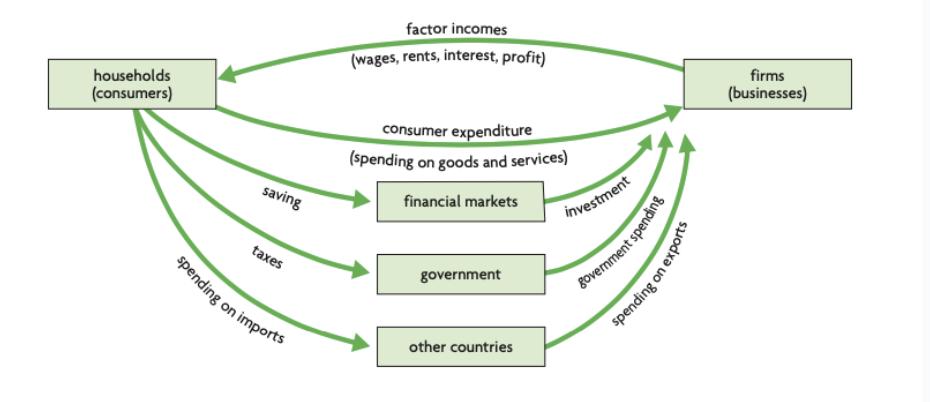

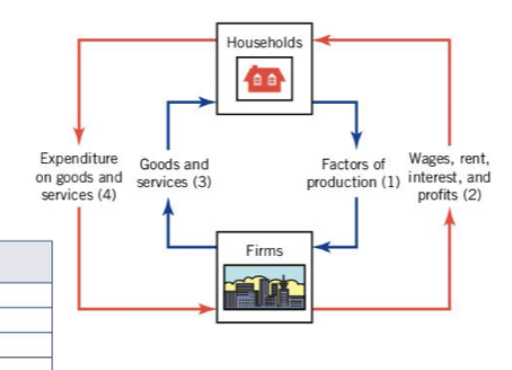

Circular flow of income

Households supply the factors of production and firms provide payments to the factor

Labour → Wages

Land → Rent

Capital → Interest

Entrepreneurship → Profit

Leakages and Injections

Leakages: Some money leave the economy

Governments take money in the form of taxes

Consumers save

Households and businesses spend money on imports

Injections: money enters the economy

Governments spend on public services and infrastructure

Financial sector invests money in firms

Foreign households purchase exports