Looks like no one added any tags here yet for you.

asymmetric information

exists in any transaction where one party has less information than the other

examples of asymmetric information

subprime mortgages granted by a lender to a poorer property buyer.

a lender does not know how likely a borrower is to repay their loan

car insurance

a car insurance company cannot tell the risks associated with each single driver

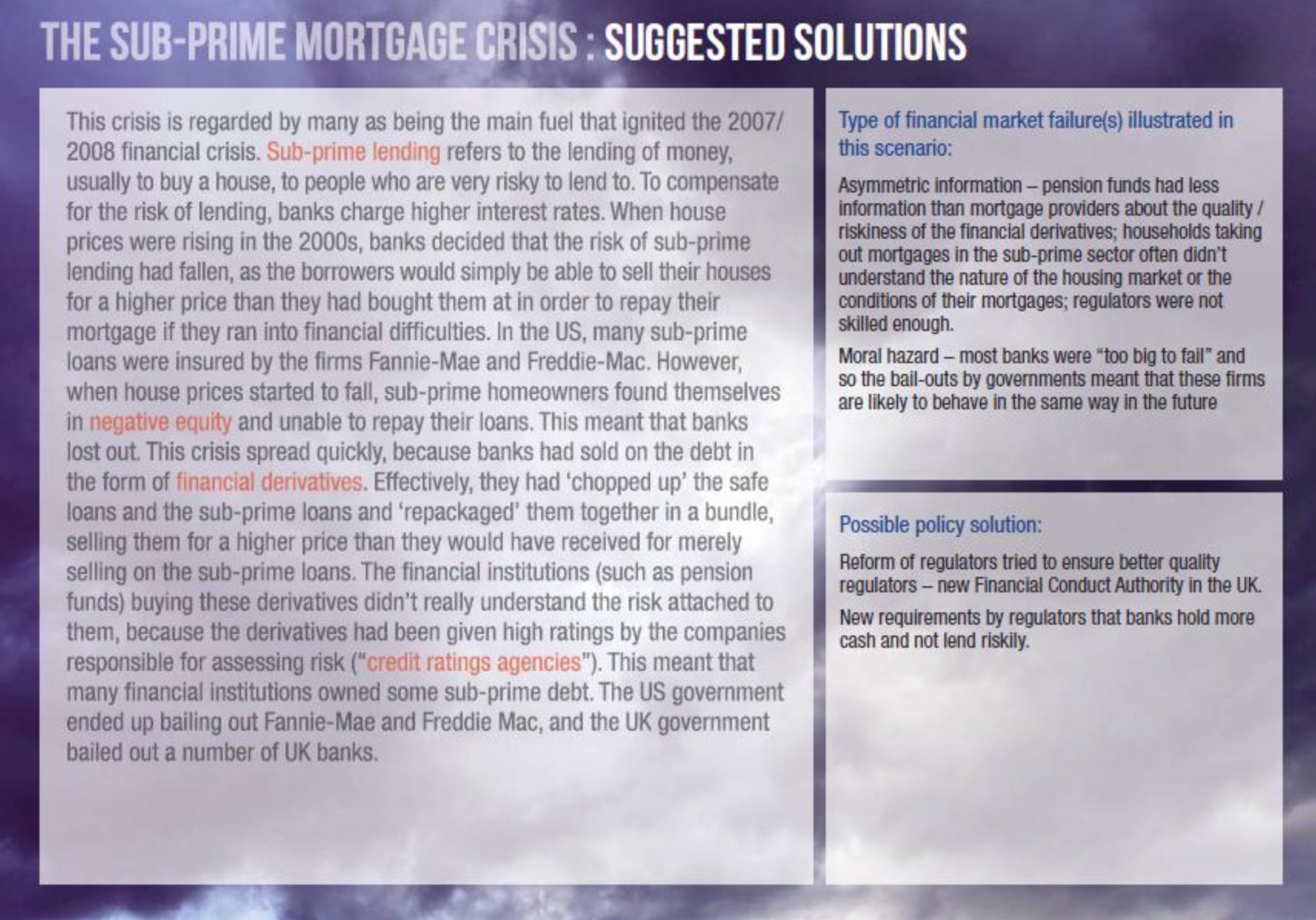

financial institutions who purchased packages of mortgages called Collateralised Debt Obligations, CDOs (which caused the 2008 financial crisis)

institutions unaware of the true level of risk since some of the CDO was composed of pools of subprime mortgages lent to poorer people – who may struggle to repay

regulators in the financial sector vs the banks they regulate

regulators have insufficient information compared with the bankers about the true level of risk associated with different financial product

explain why banks were able to exploit asymmetric information to sell PPI

banks were aware that PPI products were highly profitable.

this was because they were highly priced but it was difficult for customers to make claims on the insurance policy.

customers, on the other hand, were for the most part unaware that the insurance could be bought at a fraction of the price from other providers.

they were also unaware that the insurance often did not cover them, for example, because they were self-employed.

some customers were falsely told that they would not be able to take out a loan without PPI.

others were not even told they were buying PPI when they took out a credit card or loan.

banks therefore knew they were selling a product in a highly pressured way which did not suit the financial needs of many of their clients.

customers on the other hand had little understanding of the product they were being pressurised to buy → banks had far more information than customers → asymmetric information in the market.

explain why banks would want to sell their customers a product like PPI when they also wanted to be attractive to customers and sell them other financial products

neo-classical economic theory suggests that firms aim to maximise profits.

for a monopolist, this will be at the expense of its customers.

managerial theories suggest that directors, managers and workers will aim to maximise their returns from employment whilst being constrained by the need to profit satisfice.

PPI was such a highly profitable product both for banks and the employees who were incentivised to sell PPI, that selling other less profitable financial products was not as important an objective.

moreover, because there was asymmetric information in the market, customers were for the most part unaware that banks were exploiting them.

therefore they continued to trust banks and buy other products from them, many of which would have been at best only partially suited to their needs or more highly priced than the best products on the market

negative externality

exists when a market transaction has a negative consequence for a 3rd party

microeconomic external costs of a bank’s failure.

e.g. bankruptcies for businesses if a bank’s customers lose their deposits and can no longer pay bills to other businesses

macroeconomic external costs of the 2008 financial crisis

fall in GDP, rising unemployment and falling incomes across the world economy, particularly in Europe and the US.

cost to taxpayers of bank bailout

moral hazard

an individual or organisation takes much more risks than they should do

this is often because they know that they are either covered by insurance, or that the government will protect them from any damage incurred as a result of those risks

moral hazard: examples from the financial markets

in the 2008 financial crisis, when employees sold subprime mortgages to those who would not be unable to pay them back → huge bonuses but no negative impact on the employee if loan was not repaid

financial institutions may take excessive risk because they know the central bank is the lender of last resort and so will not allow them to fail because of the impact it would have on the economy

speculation and market bubbles

almost all trading in financial markets is speculative → creation of market bubbles, where the price of an asset rises massively and then falls.

how do bubbles arise and burst?

investors see the price of an asset is rising and so buy it.

prices become very high and investors think price will fall, so they sell their assets and panic sets in, causing mass selling → herding behaviour

how may pre-2008 housing bubble arise?

financial market has also caused market bubbles in the housing market by lending too much in mortgages and increasing demand and prices of houses.

when this bubble burst, there was a fall in demand for houses and house prices fell

lower house prices → can create negative equity as some highly indebted households owe more on their mortgage than the new lower value of the house they have bought.

this in itself can cause households to default → a negative wealth effect, reducing AD, and banks are left with loans that will not be repaid in full

speculation and market bubbles: late 1990s dot.com stock bubble

tech stocks became popular and investors were buying any stock which had a tech-sounding name

demand → prices rising massively above the underlying valuations of these companies; in fact many were loss making

when people realised this, the selling began and the bubble burst

what is market rigging?

group of individuals or institutions collude to fix prices or exchange information that will lead to gains for themselves at the expense of others

examples of market rigging

insider trading

an individual or institution has knowledge about something that will happen in the future that others do not know and so can buy or sell shares to make a profit.

collusion

when there is a small number of firms in a market, they may choose to work together to increase their joint profits and exploit consumers.

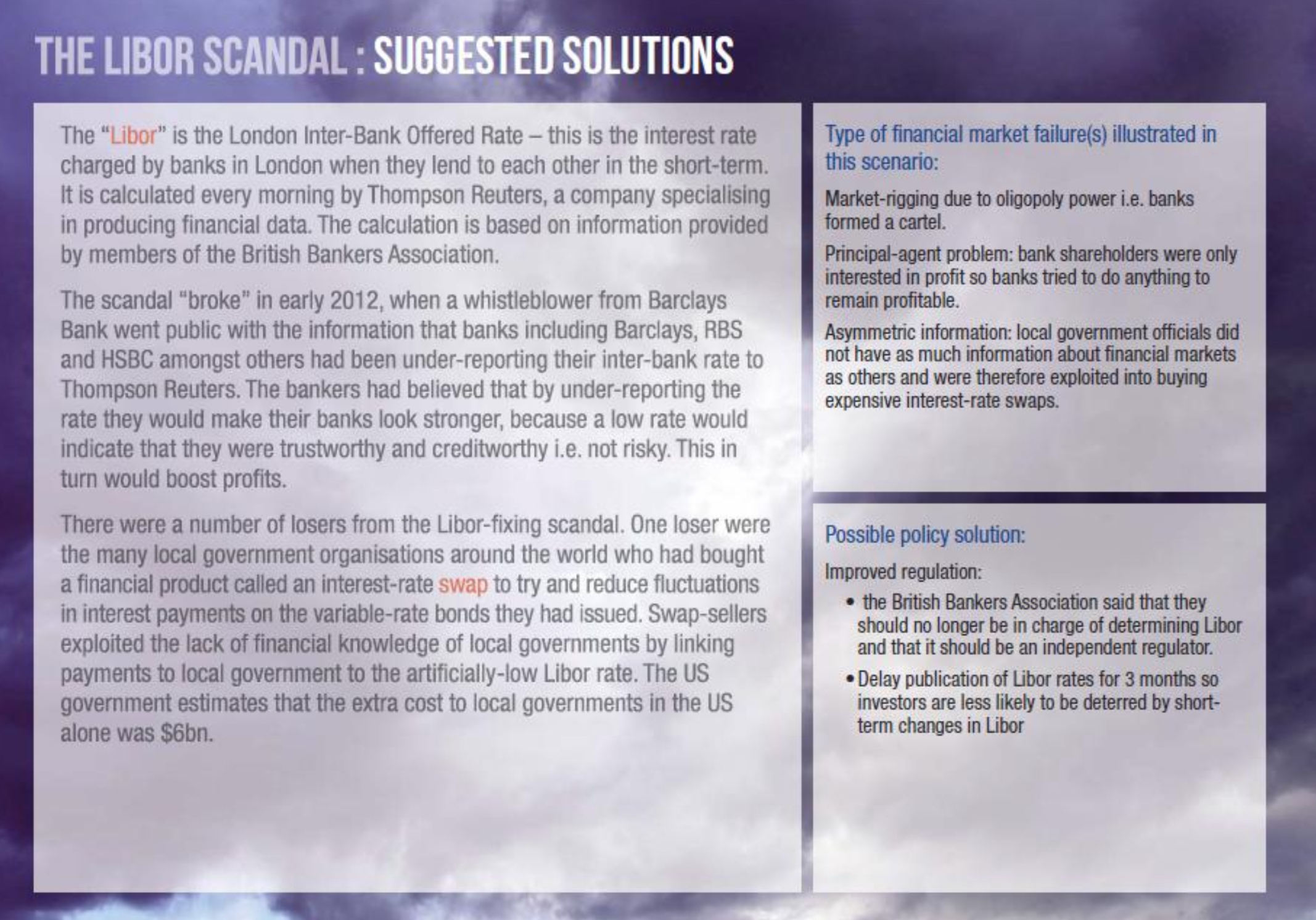

in the Libor scandal of 2008, financial institutions were accused of fixing the London Interbank Lending (offered) Rate (LIBOR), one of the most important rates in the world

explain why individual traders and the financial institutions they work for have an incentive to rig markets.

Financial institutions aim to maximise their profits according to neo-classical theory.

Managerial theories suggest that directors, managers and workers will aim to maximise their

rewards from employment. Financial institutions therefore have an incentive to rig markets

because they can earn higher profits at the expense of their customers or the institutions

with which they deal. So long as the financial or reputational penalties for rigging markets if

they are caught are lower than the profit they earn from rigging markets, the banks will

continue to create cartels.

Individual traders are incentivised by their employers to maximise profits from their trades.

They will typically be awarded bonuses, the size of which will depend on how much they

have made for their bank or other financial institution. Individual traders therefore have an

incentive to rig markets to their benefit. If caught, they might lose their jobs. However, the

higher the level of bonuses, the more incentive there is to maximise short-term returns. For

example, if a trader could earn £50 000 in his or her next best occupation, but could earn

£1million in salary and bonuses in one year by rigging markets, then one year’s salary and

bonus is the equivalent of 20 years’ salary in their next best job. If they earned £2 million in

salaries and bonuses over two years, they would have earned the equivalent of 40 years’

work in their next best occupation. 40 years is a typical working lifetime for most people.

These large sums explain why individual traders have such an incentive to cheat and collude

LIBOR SCANDAL

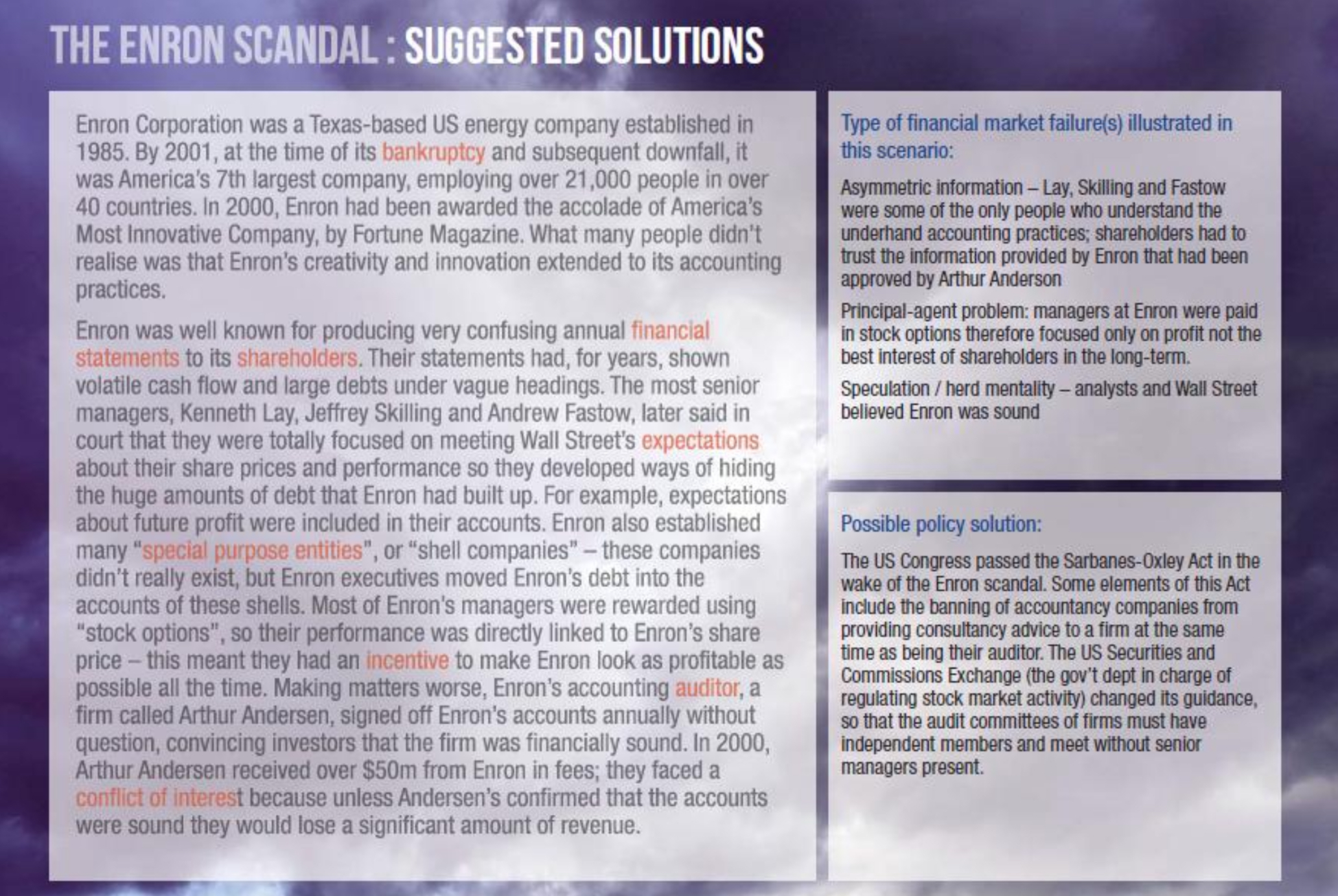

ENRON SCANDAL

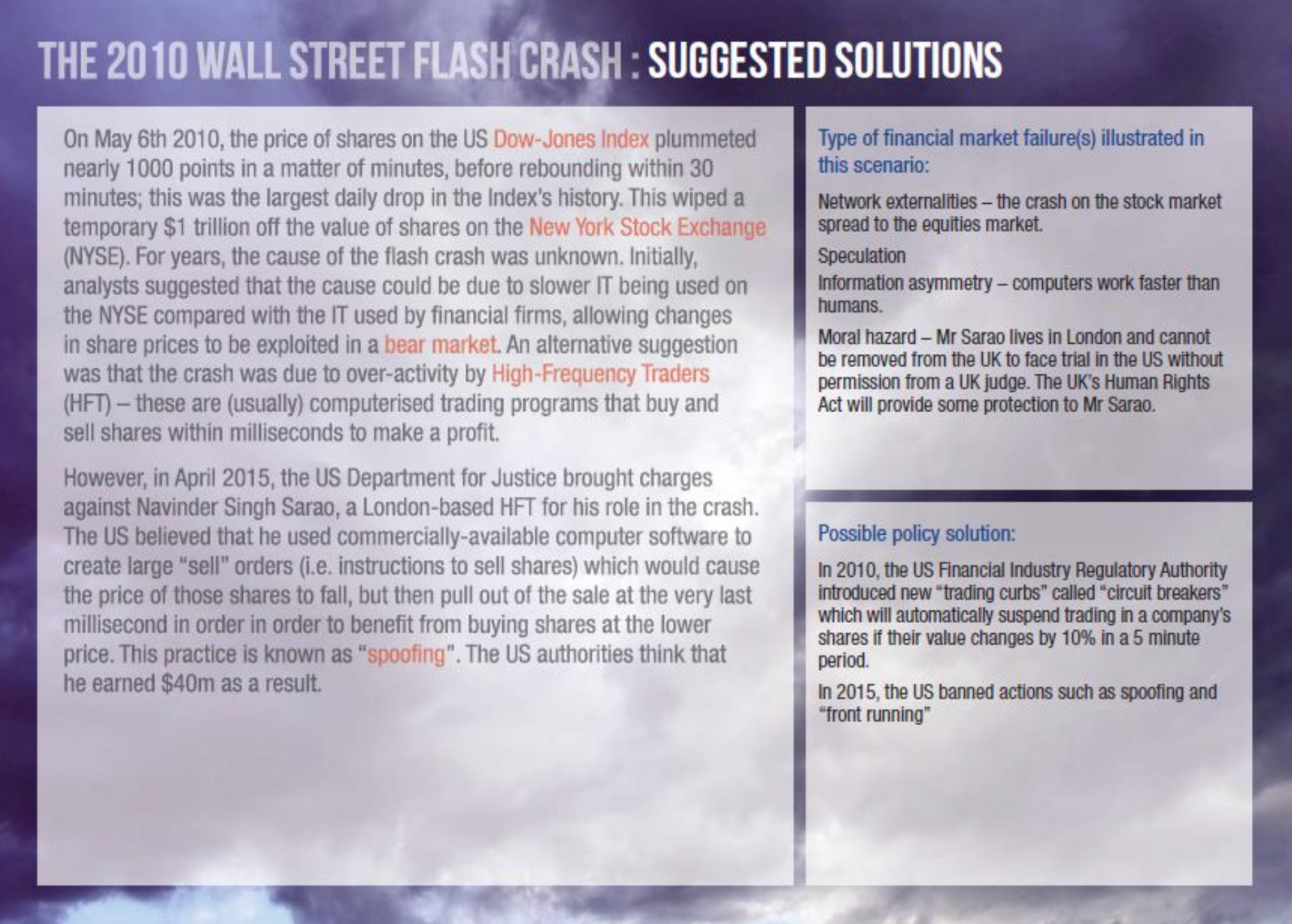

2010 WALL STREET FLASH CRASH

SUB-PRIME MORTGAGES CRISIS