M&D Module 6c -- LCM & Error Corrections

1/16

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

17 Terms

write down inventory

When unsold inventory falls below cost, companies must ______ ______ _____to reduce the asset and periodic net income

LCNRV

With a FIFO/Avg Cost CF Assumption, what measurement approach do you use?

LCM

With a LIFO CF Assumption, what measurement approach do you use?

est. selling price - est. selling costs

How do you calculate NRV?

LCNRV can be applied to

T

(T/F) For LCNRV, if NRV is < cost, you need an adjusting entry to reduce inventory from cost to the lower NRV

T

(T/F) If cost is lower than NRV, you don’t need an adjusting entry

NRV (ceiling); NRV - NPM (floor)

For LCM, the market is the current replacement cost, except that: market can’t be > than ____ (____) and market can’t be < ___ - _____ (___)

COGS

What do you debit if the write-down is common?

loss on inventory

What do you debit if the write-down is uncommon?

False

(T/F) Accounting principles DO NOT need to be applied consistently from period to period to allow comparability

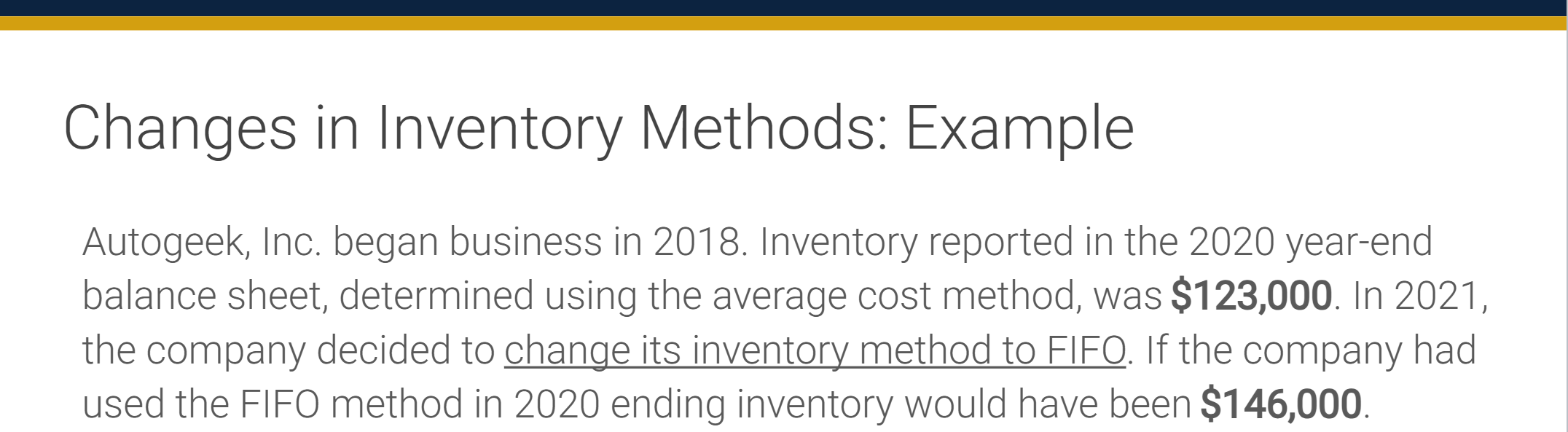

prior year

If you voluntarily change inventory method (e.g. Average Cost to FIFO), you must adjust ____ _____ (comparative) financial statements to reflect the change

Dr. Inventory 23,000, Cr. RE 23,000

What should your journal entry be?

True

(T/F) When a company changes to the LIFO inventory method from any other method, it is likely impossible to calculate the income effect on prior years

T

(T/F) A company changing to LIFO usually does not report the change retrospectively; instead LIFO method is used from that point on

reversed; appropriate entry

If an error is discovered in the same accounting period, the original erroneous entry should be ___ . And the __ ___ should be recorded

retrospectively; prior period adjustment

If error discovered in subsequent accounting period:

Previous year financial statement should be______ restated

Incorrect account balances are corrected by journal entry

Correction of retained earnings is reported as a _____ _____ _____ to the beginning balance in the statement of shareholders’ equity

Disclosure note describing the nature and impact of error