ap microeconomics unit 2

1/38

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

39 Terms

What are the 5 shifters of demand

Demand shifters

Taste and preferences

Market size

Price of Related Goods Substitutes + Complements

Changes in Income

Expectations

What are complementary goods?

A pair of goods where one is often needed to enjoy another; like cookies and milk.

If x and y are complements, an increase in the price of x will cause the demand for y to

decrease

If x and y are complements, a decrease in the price of x will cause the demand for y to

increase

The law of demand, ceteris paribus (Latin for "all other things being equal"),

as the price of a good or service increases, the quantity demanded will decrease, and vice versa, assuming all other factors that could influence demand remain constant

What is the law of supply

Ceteris Paribus Producers sell more at high prices and less at low prices.

What are substitute goods?

A pair of goods where one can be used in place of the other; like ice cream and frozen yogurt

If x and y are substitutes, an increase in the price of x will cause the demand for y to

increase

If x and y are substitutes, a decrease in the price of x will cause the demand for y to

decrease

What are normal goods in regards to changes in income?

These are goods that people buy more of when they have larger incomes; like shoes.

If consumers’ incomes increase, demand for normal goods will

increase

What are inferior goods?

These are goods that people buy less of when they have more income; like generic brands.

If consumers’ incomes increase, demand for inferior goods will

decrease

Income effect

As prices fall, your income has more purchasing power so you can afford to buy a larger quantity.

Substitution effect

As prices fall, substitute goods look less attractive so consumers buy a larger quantity.

What are the 6 non-price determinants of supply?

1. Prices of resources or inputs

2. Government tools (taxes decrease supply, subsidies increase supply, & regulations generally decrease supply).

3. Competition (number of sellers)

4. Technology

. Prices of other goods

6. Producer Expectations

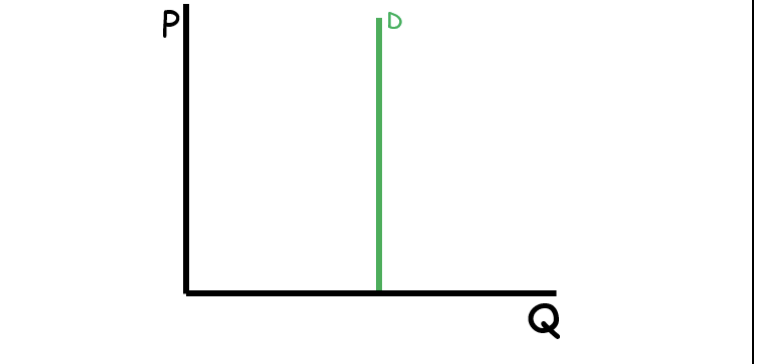

Perfectly Inelastic

0

Relatively Inelastic

<1

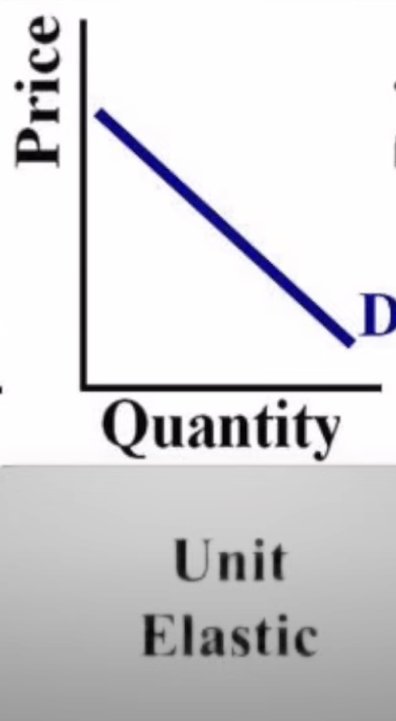

Unit Elastic

1

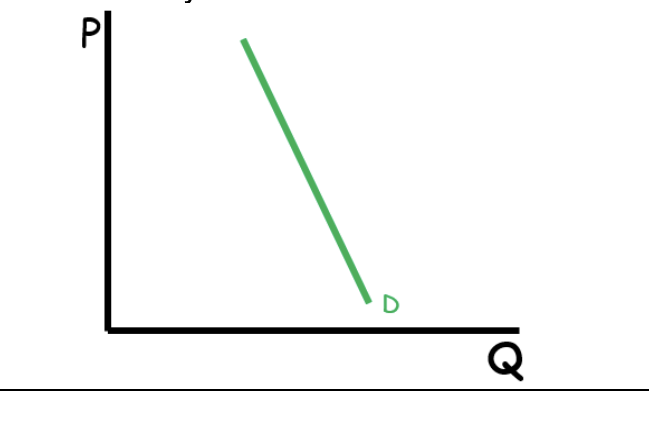

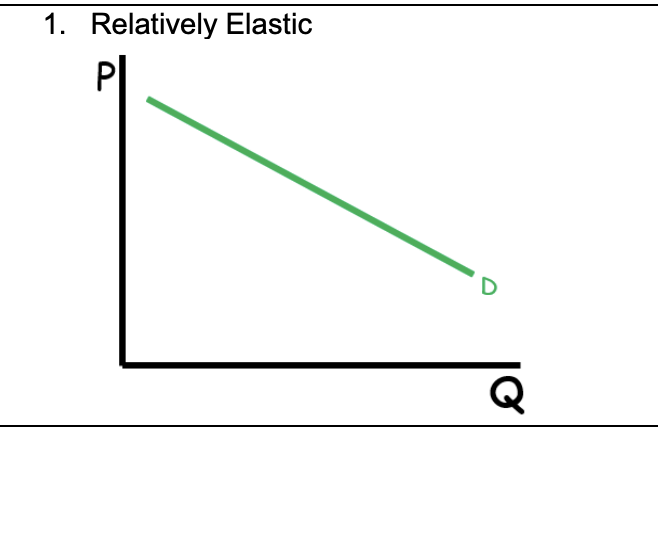

Relatively Elastic

>1

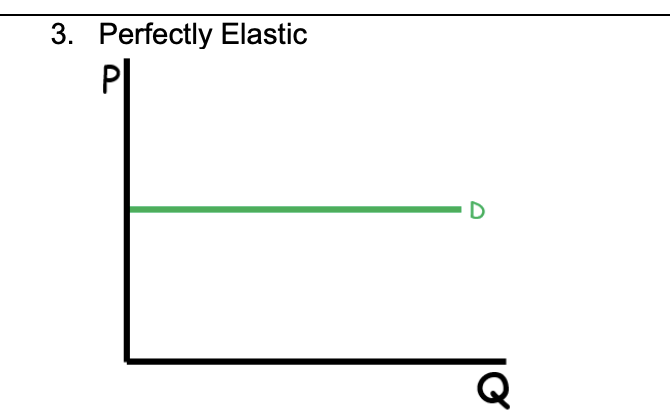

Perfectly Elastic

∞

Formula for Total Revenue

TR= Price * Quantity

If price decreases and TR increases, the demand curve is

Elastic

If price decreases and TR doesn’t change, the demand curve is

Unit Elastic

If price decreases and TR decreases, the demand curve is

Inelastic

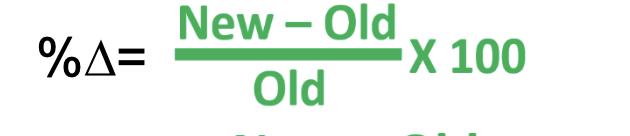

formula for elasticity percentage change

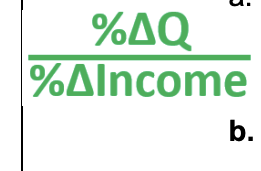

Income Elasticity Formula

negative coefficient means its inferior good

Price Elasticity Formula

%Quantity/%Price

Cross Price Elasticity

CP= %change in quantity of x/ %change price of y

positive coefficient= goods are substitutes

negative coefficient= goods are complements

Consumer surplus

The difference between what consumers are willing to pay for a product (the demand curve) and the price they actually pay.

Producer surplus

The difference between what producers are willing to accept for a product (the supply curve or marginal cost) and the price received.

Economic surplus

Consumer surplus, producer surplus, and any tax revenue added together.

Deadweight loss

AKA efficiency loss, is a reduction of economic surplus.

Allocative efficiency

When economic surplus is maximized. Marginal social benefit equals marginal social cost. (In a competitive market without externalities allocative efficiency is at equilibrium. A firm is allocatively efficient when P=MC)

An increase in the price of good X causes buyers to want to buy more of good Y. Which of the following explains the resulting change in the market?

A. The demand curve for good X will shift to the right because the goods are substitutes in consumption.

B. The demand curve for good Y will shift to the right because the goods are substitutes in consumption.

C. The demand curve for good X will shift to the left because the goods are complements in consumption.

D. The demand curve for good Y will shift to the left because the goods are complements in consumption.

E. There will be a downward movement along the demand curve for good X because the goods are complements in consumption.

Which of the following correctly describes the income effect associated with the law of demand?

If the price of a normal good decreases, the purchasing power of a consumer’s income increases and therefore consumers will be willing and able to purchase more of the good.

Which of the following will occur as a result of a decrease in the prices of the inputs used to produce a good?

The quantity supplied would increase at each possible price for the good.

Assume that the market for a good is characterized by a downward-sloping demand curve and an upward-sloping supply curve. Suppose that there is an improvement in technology for producing the good. Which of the following would occur?

The total economic surplus in the market would increase.