Quiz 2 - Introduction to Microeconomics

1/14

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

15 Terms

Is anything actually free?

no, as goods go beyond their monetary value

Demand curve relates quantity demanded to all costs

ex. waiting in line

law of demand

quantity purchased varies inversely with price

cost-benefit principle

states that you should only do something if the benefits outweigh the costs

tom has a $200 budget, he has to chose between two goods, $4 beef and $2 apples

Qb = 50 - ½ x Qa

reservation price

a limit on the price of a good or service

rational human preference

states that people’s preferences is semi-consistent and people prefer paying less

wants & demands

Want is something people desire to have, that they may, or may not, be able to obtain.

Demand is the quantity of a good or service that consumers are willing and able to buy at a given price in a given period

utility

the total satisfaction a consumer derives from consuming any particular product

marginal utility

the amount of satisfaction a consumer derives by additional consumption of the same product

the law of diminishing marginal utility

states that for any good or service, the marginal utility of that good or service decreases as the quantity of a good increases

when you buy less, marginal utilities decrease

when you buy more, marginal utilities increase

so how does tom find the best bundle?

rational spending rule: MuA/PA = MuB/PB

this value should be equal

as MuA increases, MuB decreases. So the quantity of beef must decrease for an optimal bundle

no cash on the table principle

sellers should always strive to maximize their profit by not leaving any potential value on the table during negotiation

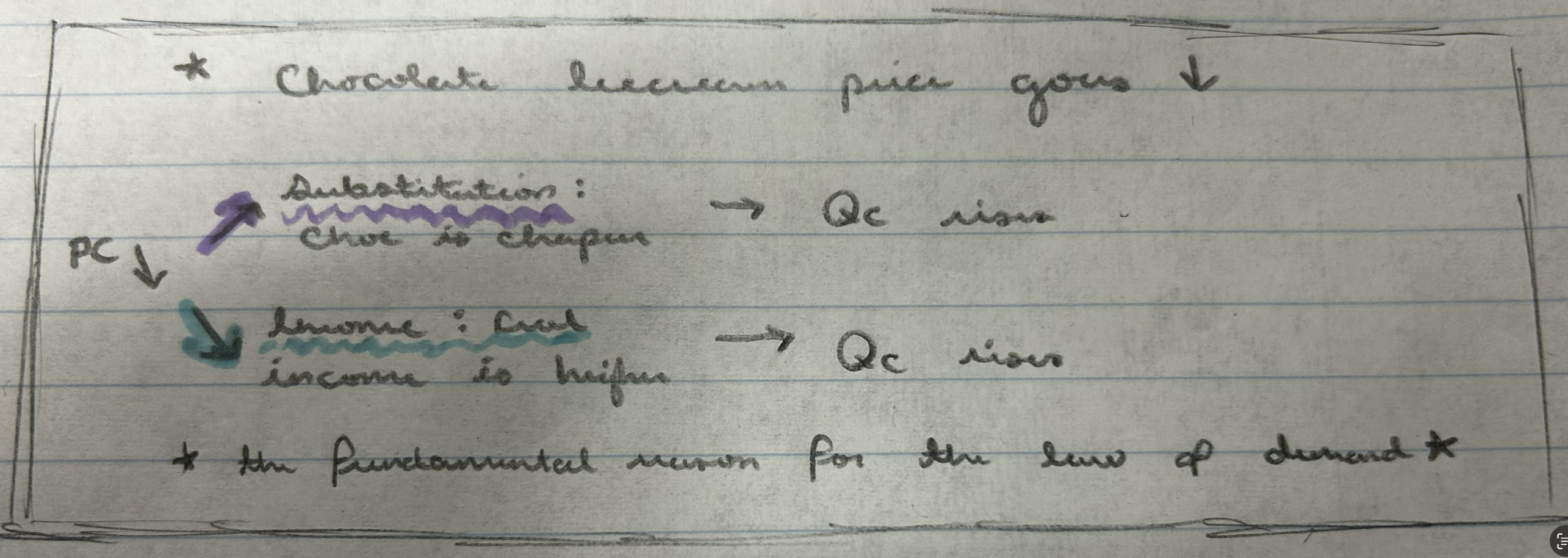

substitution effect

describes how consumers shift their demand towards cheaper alternatives when the price of a good increase or a substitute is cheaper

income effect

the change in consumer demand for goods and services resulting from a change in real income or a substitute is cheaper

nominal and real price

nominal- the price of goods in terms of dollars

real- the nominal price of a good relative to the average dollar price of other goods