Cost accounting

1/134

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

135 Terms

What is cost accounting?

supports the management of a company by providing information necessary for managing the entire company or individual departments

What are the four main accounting objectives?

control (steer)

planning

monitoring

documentation

What are the three systems in corporate accounting?

financial accounting (balance-sheet, cash-flow)

capital budgeting

management accounting (incl. cost accounting)

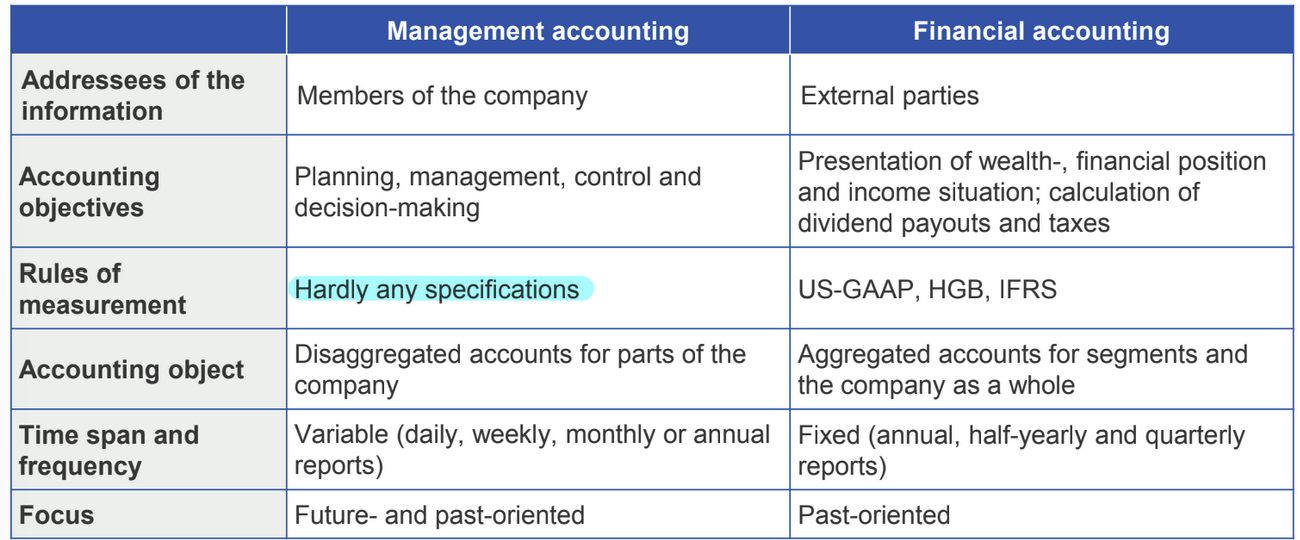

What are the differences between management and financial accounting?

What is the difference between cost accounting and capital budgeting?

cost accounting

up to one year

operational decisions

time value of money neglected

capital budgeting

long-term effects of decisions

time value of money important - interests

What are costs?

valuated consumption of resources

What are revenues?

valuated production of goods

What are the three key elements related to costs and revenues?

objective orientation (cost: only if expense aligns with intent)

valuation (no explicit price tag)

consumption of resources/production of goods

exchange of money for products/using them to make something else

What are artificial indirect costs?

costs that could be traced, but would be hard to, thus treated as indirect (e.x. electricity)

What is economies of scale?

with increasing quantity, average costs decrease as fixed costs are distributed over more products

How are fixed costs calculated?

What are inventoriable costs?

costs assigned to a particular product unit

What are period costs?

costs that cannot be capitalized (cannot be considered in balance sheet; e.x. research)

What are opportunity costs?

Contributions to a company’s profit that is foregone by choosing a decision

alternative over the next-best alternative

What are sunk costs?

Costs that were caused in the past and can no longer be changed by current decisions

What are levelized product costs?

how expensive a product is over its entire life cycle (e.x. electricity - wind vs. solar)

average prices should be higher than levelized costs

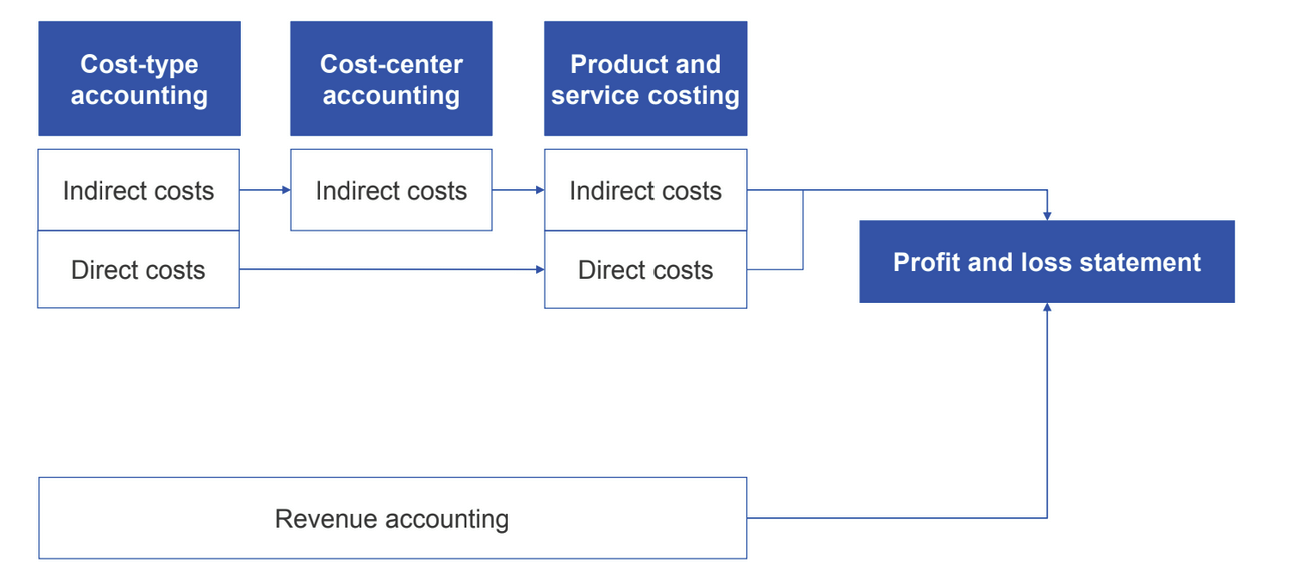

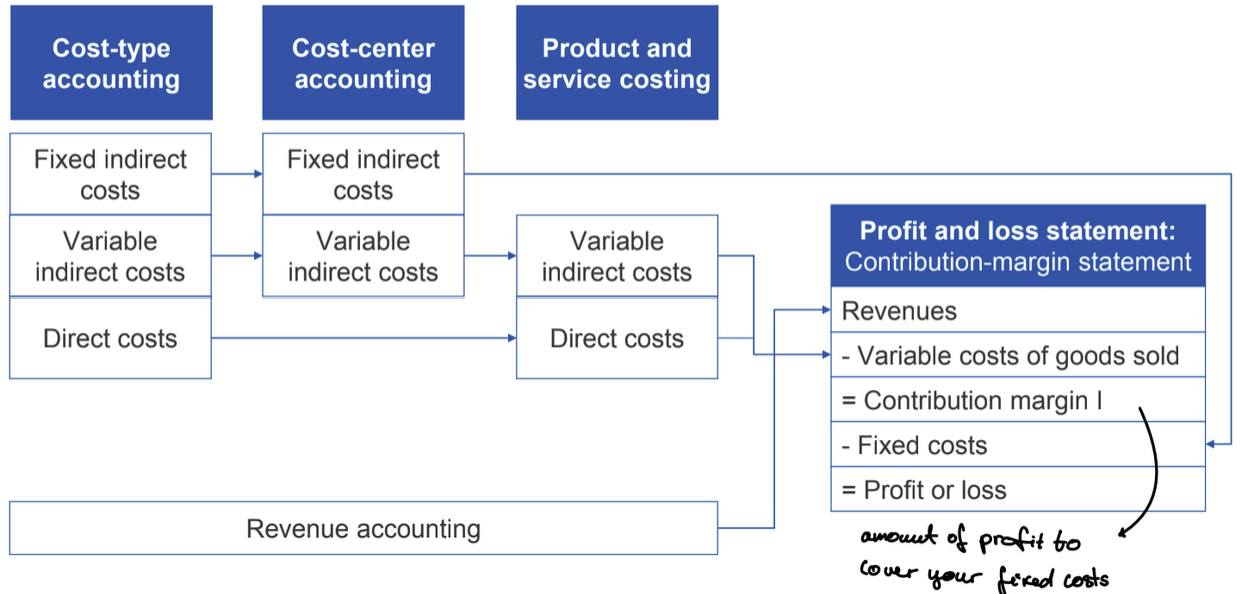

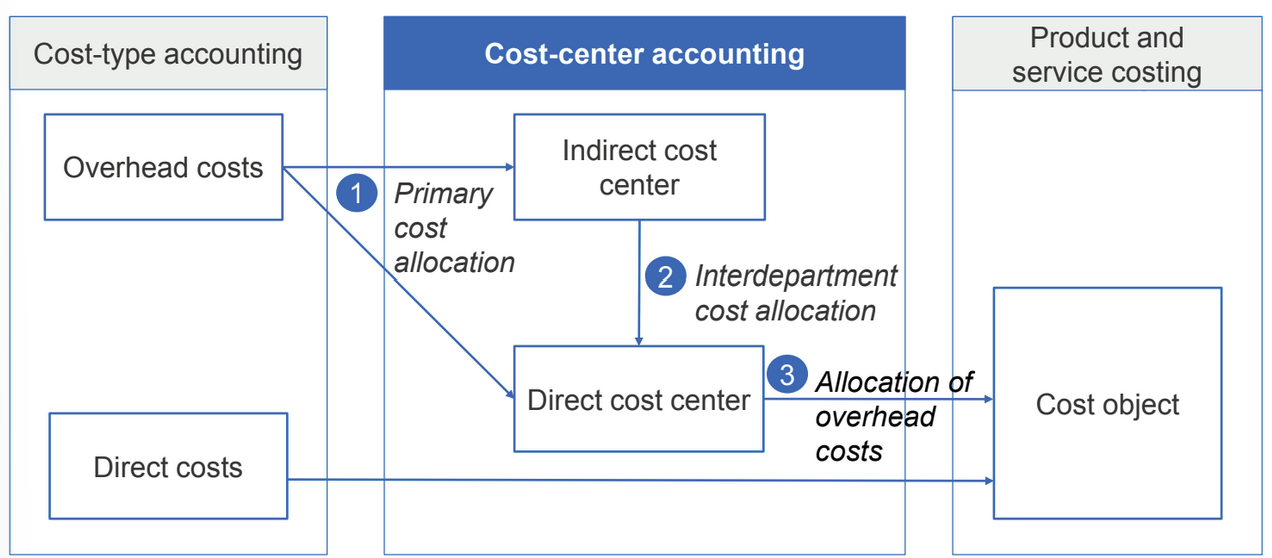

What does cost-type accounting show?

which costs have been incurred

e.x. labor, material, depreciation

What does cost-center accounting show?

where have costs been incurred

e.x. cost centers

What does product and service costing show?

for which products have the costs been incurred

How are costs calculated in absorption costing?

Product units are valued at full costs

How are costs calculated in variable costing?

product units are valued at variable cost

do not include e.x. R&D, just what directly went into producing the product → shows what you have to sell the product at at minimum

How are costs funnelled into the P&L statement in absorption costing?

How are costs funnelled into the P&L statement in variable costing?

How can cost types be classified?

nature of the input goods: material costs, personnel (labor) costs, machine costs (depreciation, interest), costs for external services

attributability of costs: direct, indirect

dependence on output variation: variable, fixed

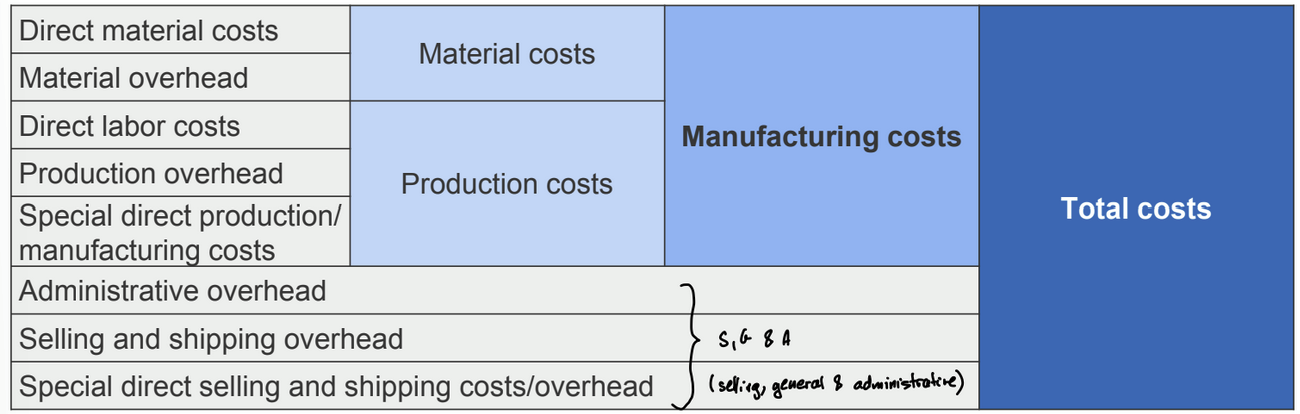

position in value chain: R&D costs, procurement costs, manufacturing costs, selling and shipping costs, administrative costs

origin of the input goods: primary, secondary

What are the 3 most important cost types?

material, personnel, machine

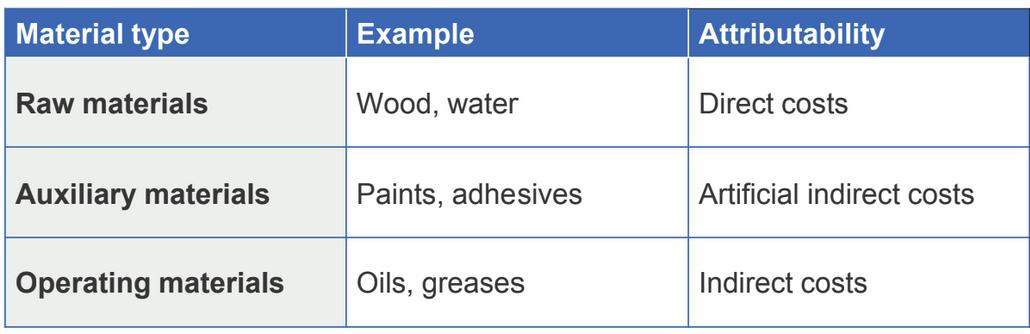

What are the 3 material types based on which manufacturing costs are categorized? How are they attributed?

How are material costs calculated?

= quantity ∙ price

What are the 3 methods to record material consumption?

inventory method

carry-on method

retroactive accounting method

What are the 4 methods for valuing material consumption?

FIFO

LIFO

ex-post average prices

uses the average purchase price for all the consumed material at the end of an accounting period

moving average prices

uses the average price after each material consumption based on the total inventory at that time

How is consumption calculated under the inventory method?

= beginning inventory + acquisitions – ending inventory

What are the benefits and disadvantages of the inventory method?

very accurate but complex

requires stock taking

reasons for consumption cannot be identified (e.x. regular consumption, theft, shrinkage)

cannot identify for which cost center or cost object the materials were consumed

How is consumption calculated under the carry-on method?

Directly recorded (consumption slip) → when they occur

What are the benefits and disadvantages of the carry-on method?

differences from other methods: measurement errors, stealing

can directly trace what the material consumption was used for

stock taking still necessary → account for unplanned usage

How is consumption calculated under the retroactive accounting method?

Calculated based on the bills of materials for each product

What are the benefits and disadvantages of the retroactive accounting method?

unplanned consumption cannot be recorded → stocktaking still necessary

bills of material must be kept up-to-date

How are auxiliary wages allocated?

wages of employees like warehouse or transportation workers

not directly involved in production

treated as indirect cost

allocated to the cost objects through cost centers and overhead rates

What are the 5 types of personnel costs?

salaries

time wages

piece-rate wages

premium wages

fringe benefits

e.x. corporate car, social security contributions

convert to standardized values & allocate them to wages as percentage

What are the 5 types of machine costs?

depreciation

interest costs

leasing/rental payments

acquisition-related costs (e.x. transportation, training)

maintenance costs

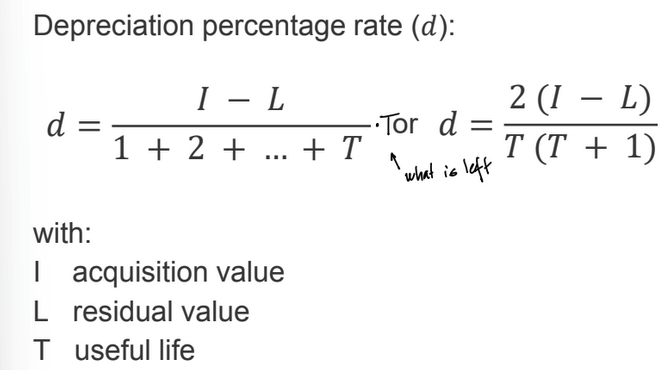

What are the 4 depreciation methods?

time dependent

straight-line depreciation

declining balance depreciation

arithmetic-degressive depreciation

output dependent

units of production depreciation

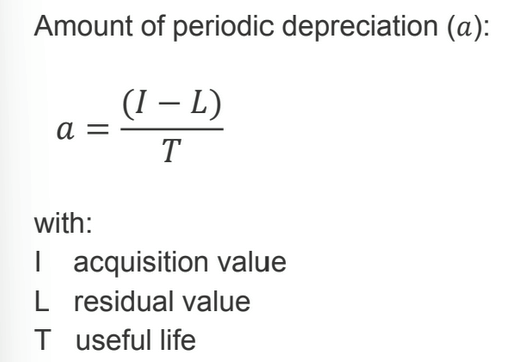

How is straight-line depreciation calculated?

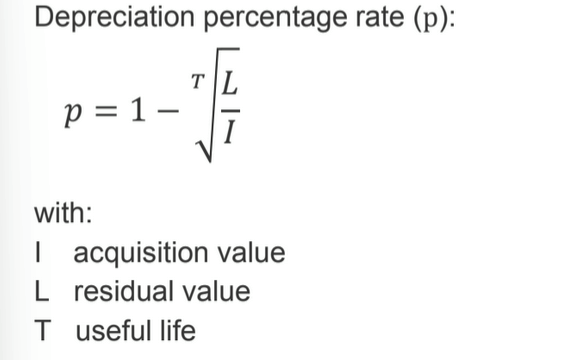

How is declining balance depreciation calculated?

depreciation amounts decrease gradually over time

How is arithmetic-degressive depreciation calculated?

depreciation amounts decrease each year by a constant value

useful for companies to decrease earnings heavily in the beginning → lower taxes

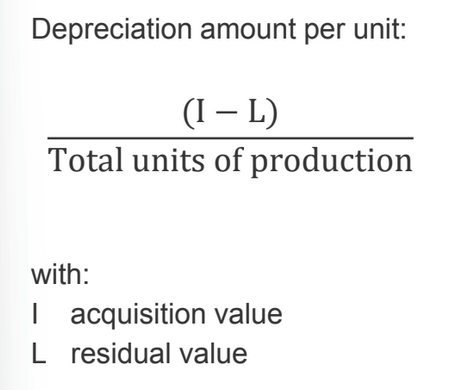

How is units of production depreciation calculated?

based on the utilization of the asset

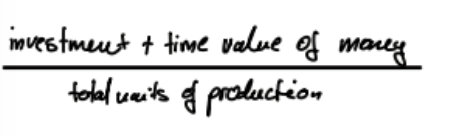

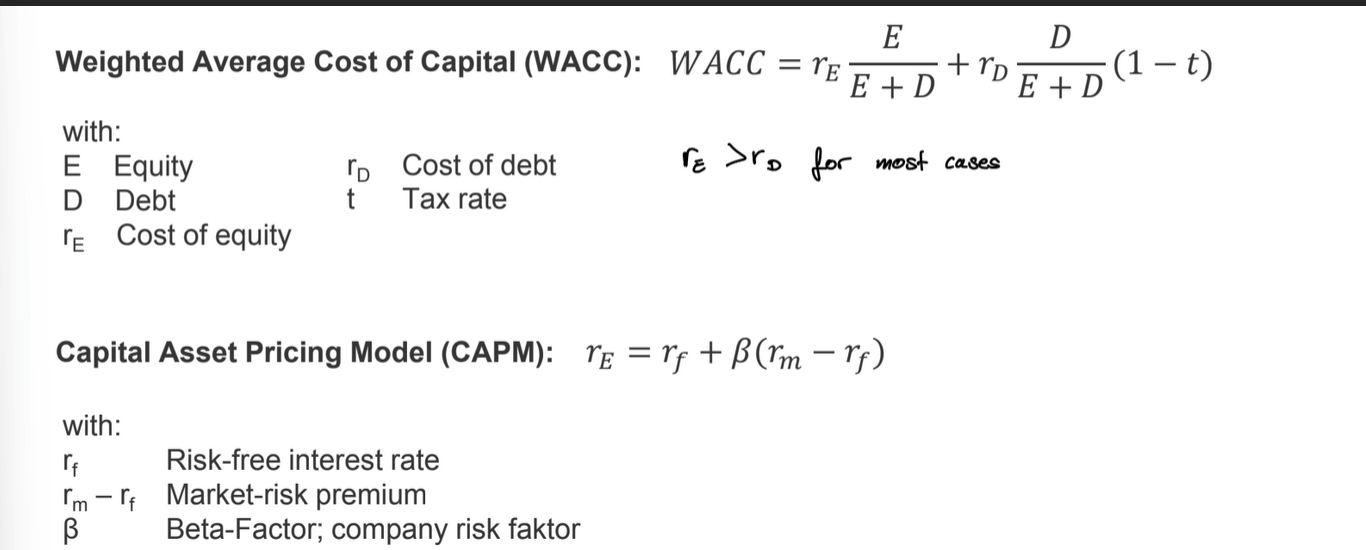

How are interest costs calculated, and what are the four steps of determining interest costs

capital required for operations ∙ interest rate

Determine the assets necessary for operations

check the operational necessity for each position on the active side

important: machinery, inventory, cash & cash equivalents

Value the assets necessary for operations

decision: valuation based on replacement cost/acquisition & production cost

estimate average values of assets over the accounting year (previous & current year’s balance sheets)

Determine the capital required for operations

deduct non-interest-bearing-liabilities from the operating assets

valuation based on average values

e.x. provisions, accounts payable, revenues received in advance

Determine the interest rate

WACC or CAPM model

What are the 4 basic requirements for cost centers?

homogeneity of cost drivers (dependence on same variable)

matching of cost centers & the assignment of responsibilities

completeness & clarity

cost-benefit criterion (benefit > cost; usually above 100 employees)

What are 2 criteria that need to be considered about defining cost centers?

depending on the business function of departments (ideal: 8-10)

depending on how costs are allocated

indirect: far from products (e.x. energy, building, maintenance)

direct: close to products (e.x. material, manufacturing, administration, sales & distribution)

Germany: many small cost centers - detailed management → bring down costs

US: bigger cost centers - cost departments → less detailed departments

According to the Federation of German Industries, what are the main tasks allocated to the 6 main cost centers?

material-handling cost centers: procurement of raw, auxiliary & operating materials

manufacturing cost centers: carry out activities directly on the company’s products

R&D centers: R&D, design & construction of prototypes

administrative cost centers: corporate management, HR management, finance, accounting

sales cost centers: finished goods storage, sales, order processing, shipping

general cost centers: services required by most other cost centers; property, energy, social services

What are the three steps of cost-center accounting?

What are the two types of primary costs?

cost center direct costs: costs that can be directly traced to one cost center (e.g. the salary of the head of the material warehouse)

cost center indirect costs: costs for which it is not possible to trace them directly to a unique cost center (e.g. salary of the employee responsible for material storage and production preparation)

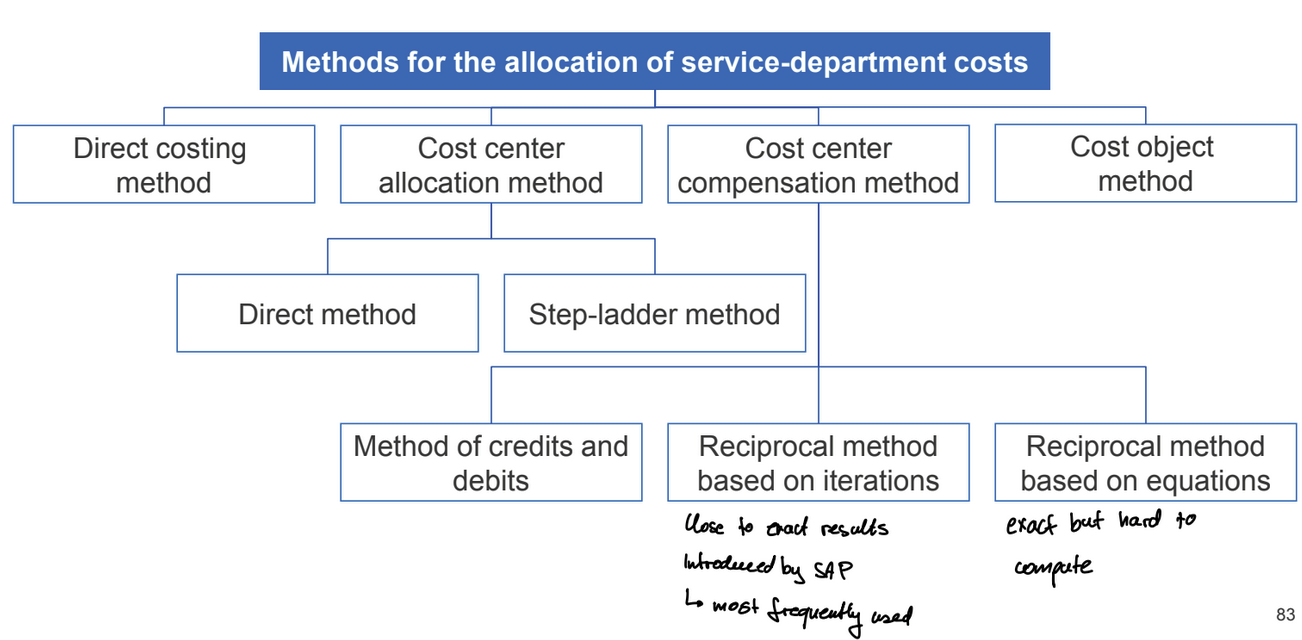

What are the possible methods for the allocation of service-department costs?

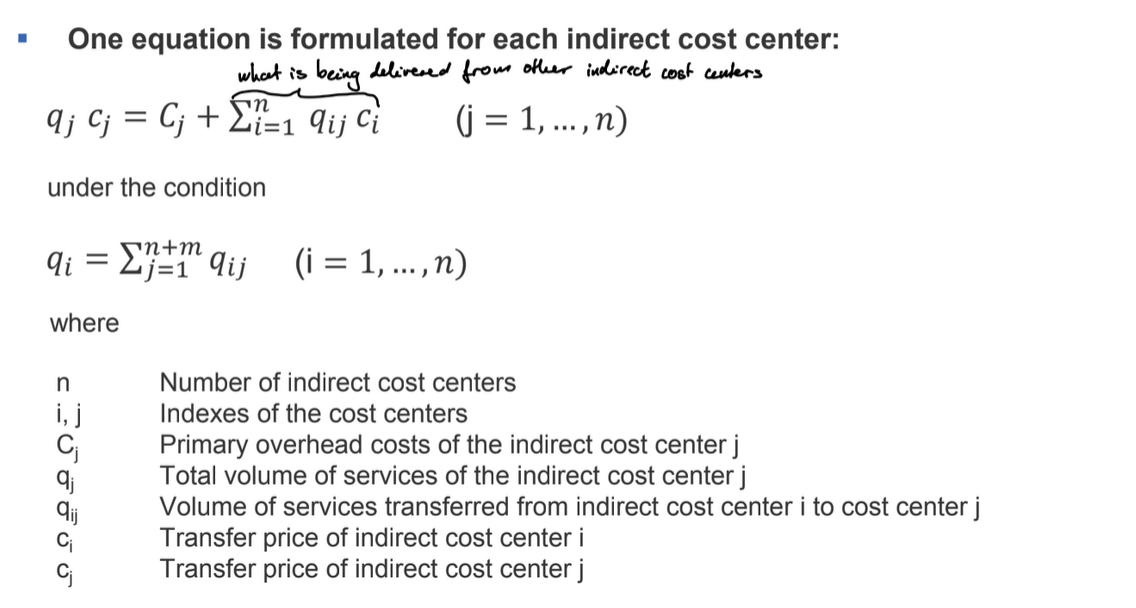

How are costs allocated using the reciprocal method based on equations?

determine transfer prices by solving a system of equations

exact method

need to record all internal exchanges of services

transfer prices (or total costs) must be recalculated periodically

e.x. total x c1 = primary overhead + energy x c1 + property x c2 + maintenance x c3

How are costs allocated using the reciprocal method based on iterations?

repeated allocation of the costs for internal services in several steps

approximation, accuracy increases with number of iteration

all internal exchanges of services need to be recorded

determination of transfer process for allocation of service exchanges not necessary

termination of the procedure as soon as the costs on each indirect cost center fall below 2 cents

transfer price = Sum of all cost incurred by an indirect cost center at all iteration levels divided by the output to other cost centers

primary overhead + what is carried over from other cost centers/total - what is used for own cost center

How are costs allocated using the method of credits and debits?

assume that transfer prices for internal services already exist

approximation, accuracy depending on the transfer prices used

all internal exchange of services need to be recorded

transfer prices are predefined → can only determine transfer prices accurately at the end of the year (as it involves primary costs)

How are costs allocated using the step-ladder method?

unlike the reciprocal method, it is only in one direction → reduce iterations

considers services between indirect cost centers, but only in one direction

internal exchange of services recorded in one direction only

transfer prices must be recalculated periodically; the amount of transfer prices varies according to the sequence of the settled indirect cost centers

(primary overhead + what comes from previous cost center)/(total-used for own)

How are costs allocated using the direct method?

no consideration of exchanges of services between indirect cost centers

exact if no exchanges between indirect cost centers exist, otherwise approximate

internal exchanges only recorded at direct cost centers

transfer prices must be recalculated periodically; relation of primary costs and activity output to direct cost centers

primary overhead/(total-what is used across all indirect cost centers)

What are the purposes of product and service costing?

planning: production program, procurement decisions, sales/list prices

control: cost control, performance review

documentation: inventory valuation

How are manufacturing costs calculated?

= material costs + production costs

How is total cost calculated?

= manufacturing costs + research and development costs + administrative costs + selling and shipping costs

What are the 4 characteristics based on which cost objects are classified?

production stage: final or intermediate products

purpose: products to be sold or products to be used by the company

production-related connection: non-connected products or joint & byproducts (e.x. hydrogen production)

type of goods: tangible or intangible goods

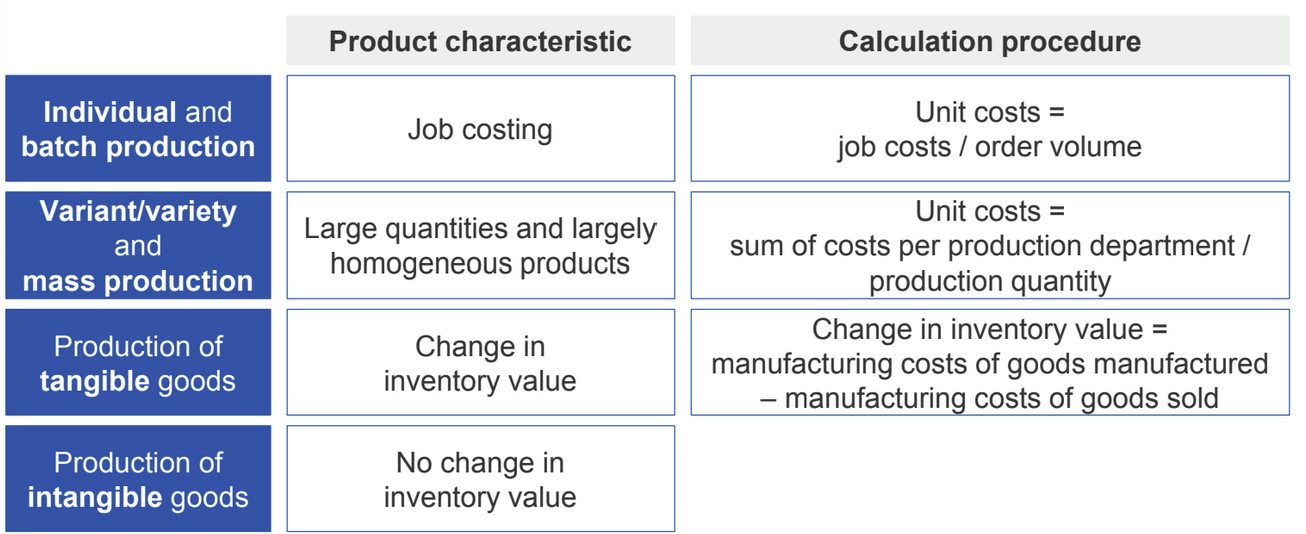

What are the 4 types of production methods and what costing methods are used for that?

job costings & machine hour costing

individual production (e.x. custom clothing, large scale plant)

batch production (e.x. business cards, wine, cars)

process costing & equivalence number method

variant/variety production (e.x. magazines, chemicals, beer)

mass production (e.x. electricity, cement, pencil)

How are different program types and costing methods related?

How is job costing broken-down in industrial companies?

Why is machine-hour costing particularly difficult to allocate?

increasing automation of processes → total labor costs & production times are not suitable for cost allocation

alternative allocation bases

machine times

lead times

processing times

most precise approach for costing

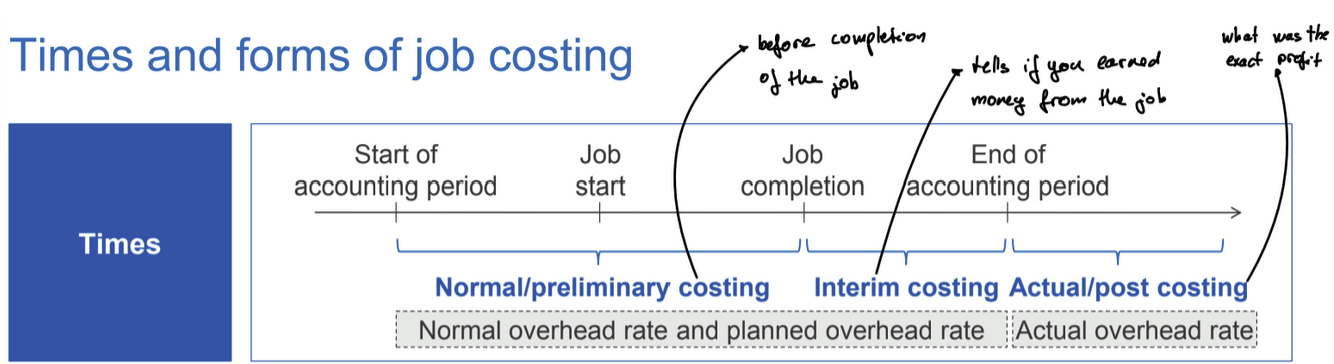

What is the timeline for job costing?

normal/preliminary costing

until job completion

production program, negotiation or price policy planning

normal & planned overhead rate

interim costing

promptly after job completion

cost & profit control

actual/post costing

after the end of the accounting period

inventory valuation, costs, and profit control

actual overhead rate

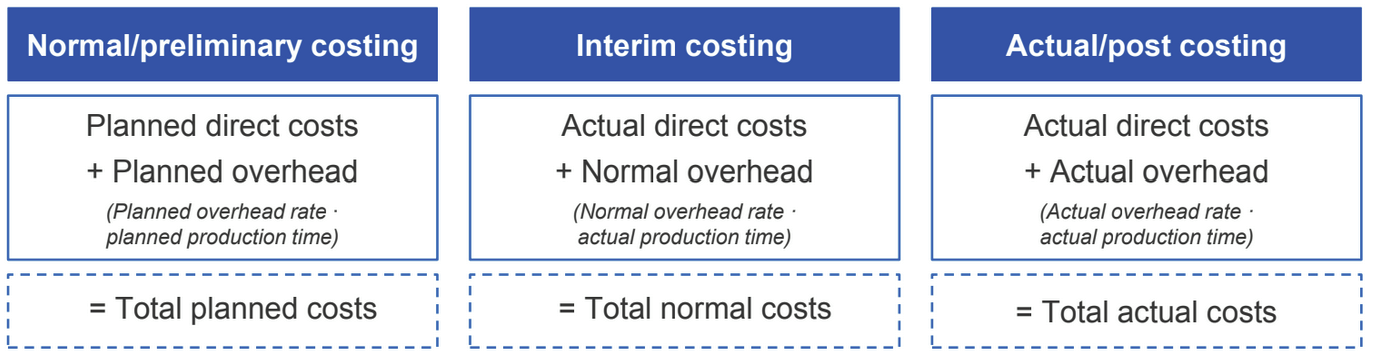

How is normal overhead rate calculated?

What are the three types of costing methods?

they do not affect the general structure of job costing

When is single-stage process costing used?

single-product production (e.x. electricity, forestry, water)

When is multi-stage process costing used?

manufacturing process meets different quality standards

stock changes to varying degrees

products’ degrees of completion differ

What are the two special features that can happen at the end of an accounting period?

different levels of completion of intermediate products possible

cost of unfinished products flows into next period

material and production costs may change over time

What are the requirements for the products produced to use the equivalence number method?

related products

produced on similar equipment

using similar raw materials

mainly in batch production

e.x. breweries - types of beer, screws

What are the three methods based on which costs of joint products and byproducts can be calculated?

main-product method

breakdown into main and byproducts

profits of byproducts deduced form total cost before decoupling point → cost neutralization

process cost - (market value-direct cost of byproducts) = process cost of main product

distribution method based on production volumes

allocation of costs before decoupling point according to produced quantities or weight

determination of profit for all products

distribution method based on market values

allocation of costs before decoupling point according to market values

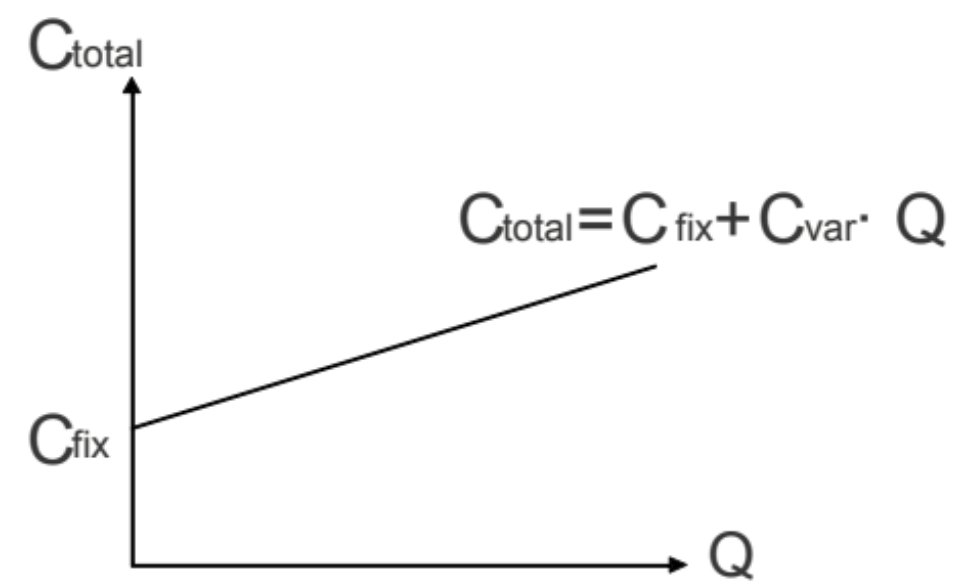

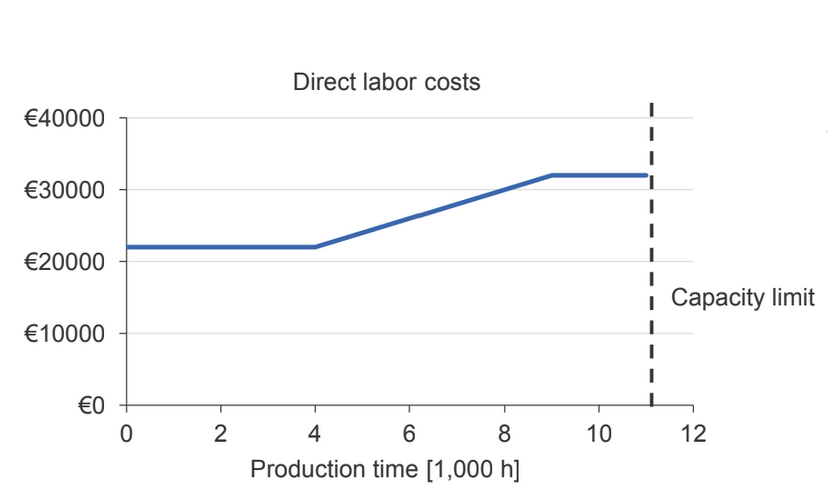

How are proportional, convex and concave costs related to each other?

proportional costs: increase in the same proportion as the level of activity

convex costs: increase in higher proportion compared to the increase in activity (e.x. overtime, training for LLM, plane tickets)

concave costs: increase in lower proportion compared to the increase in activity

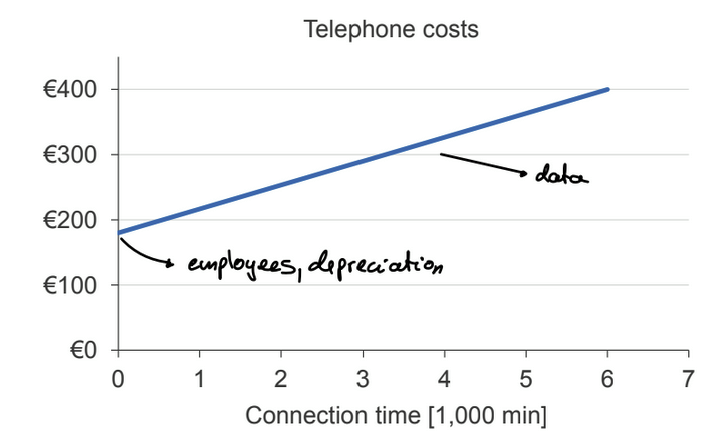

What are semi-proportional costs?

consist of a fixed and a proportional component

e.x. buy a machine, then pay for the electricity; phone plan

What are examples of costs with limits?

legal fees, electricity with cutoff, bonuses of managers

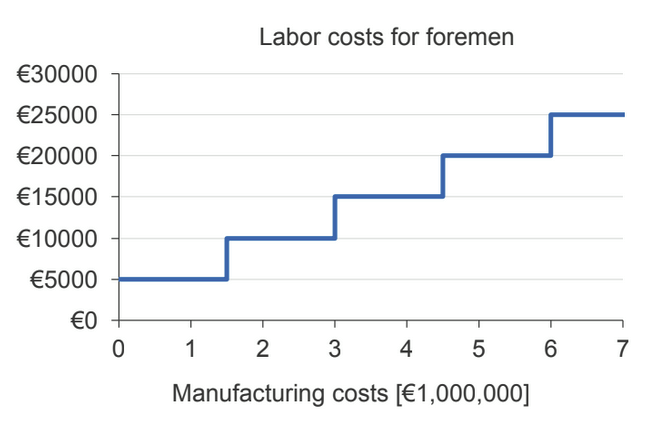

What are step fixed costs?

they increase by leaps and pounds

e.x. needing another machine; some process with capacity limits

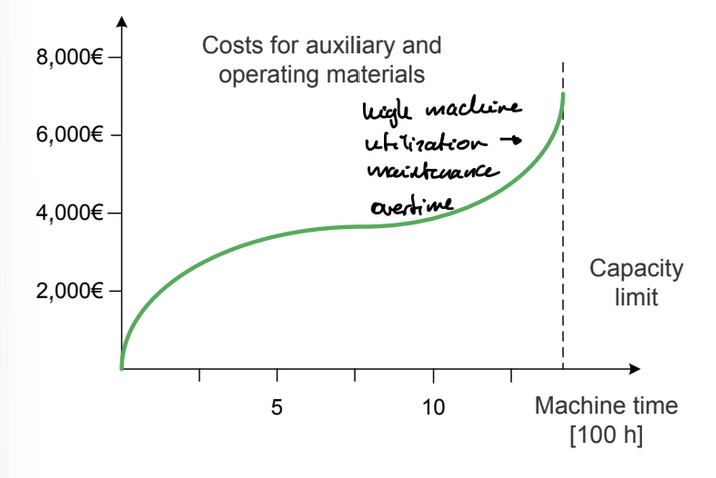

What are S-shaped costs?

characterized by a mixture of fixed and proportional costs

e.x. auxiliary & operating materials, covid vaccine production (license, scarce materials), life of a machine

What are sticky costs?

costs that respond asymmetrically to changes in activity

costs decrease to a lesser extent when activity levels decline than they increase when the activity level rises

e.x. selling, general & administrative expenses; cost of goods sold

adjusting capacity down is more challenging then adjusting it up

high committed resources (e.x. airlines, pharma, healthcare)

resistance to downsizing

more likely in financially healthy companies (that cannot bother to make adjustments)

to avoid high adjustment costs (e.x. nurses)

adjustment of prices over costs (e.x. lower selling prices to simulate demand)

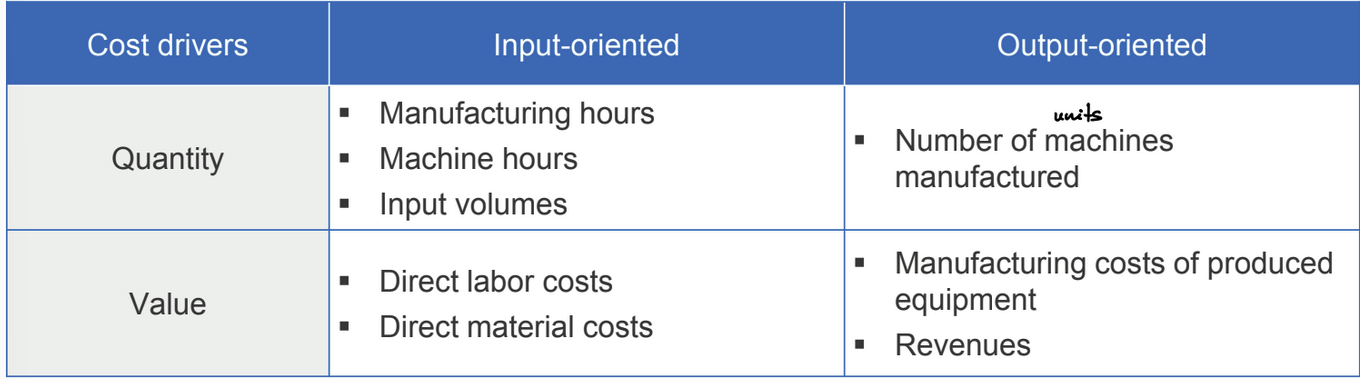

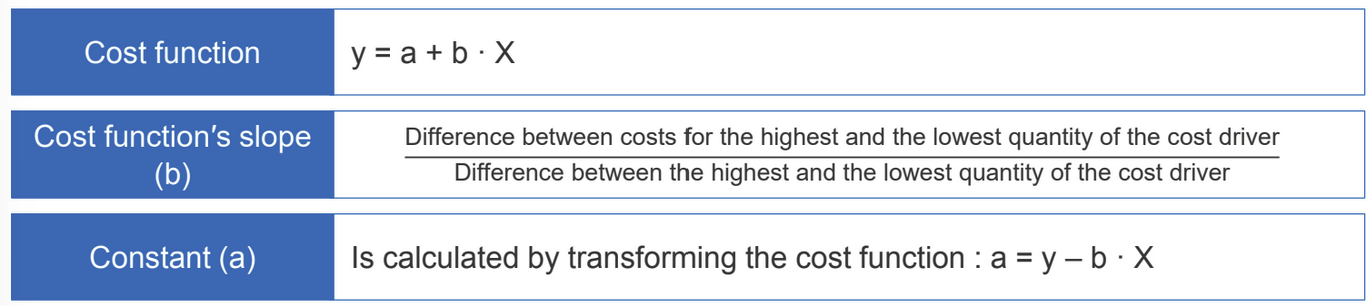

What are cost drivers?

constitute the independent (explanatory) variables of the cost function (e.x. level of activity)

How does the time horizon affect how costs are allocated?

Short-term fixed costs can be variable in the medium to long term and vary with one or more cost drivers

What are learning curves?

average working time decreases with the number of products manufactured (repetition)

concave cost function of wage/salary costs (e.x. direct labor costs per unit decrease with output quantity)

assume manual activities

What are experience curves?

unit costs decrease with the increase in output

concave manufacturing costs function (e.x. consumption of auxiliary and operating materials decreases with the number of repetitions, or the scrap is reduced)

also applies to automated activities

What are the three methods to simplify cost functions?

aggregation (calculate equivalent units for externalities into one variable)

linearization (minimize errors in relevant range; for complex cost curves)

homogenization

What is the purpose of analytical methods & what are the 6 resources for it?

analyze cause-and-effect relationships between outputs and inputs in terms of quantity and time

resources

bills of material

work schedules & functional analysis

time-and-motion studies

empirical values

technical documentation

legal regulations & contractual documents

What are statistical methods, and which are the 3 most common?

use the costs of past periods (historical data) to estimate cost functions & to forecast the costs of a future period

methods

account analysis method

high-low method

univariate/multivariate regression

How are costs estimated using the account analysis method?

costs of each category are classified as fixed, proportional, or mixed

provides a subjective cost function

uses shares of proportional costs (%) / old cost driver + fixed costs

How are costs estimated using the high-low method?

considers only the highest & lowest past observations

provides an objective, estimate cost function

outliers can lead to distorted values

How are costs estimated using linear regression?

uses all available observations to estimate the cost function

provides an objective estimate of the cost function

more precise, but requires more observations with the least deviations (e.x. least-squares method)

linear regression: one dependent & one independent variable (e.x. repair cost & repair hours)

multiple regression: one dependent & several independent variables (e.x. repair costs, repair hours & repair orders)

What is the differentiated approach for overhead cost forecasting, and what are the most common categories?

cost functions are determined & documented separately for each overhead cost category

overhead cost categories

overhead costs of operations

auxiliary material, operating material, and tool costs

maintenance costs

imputed depreciation

imputed interest

taxes & insurance

What is the purpose of cost-center summary sheets?

used to document overhead cost forecasts

assumes that there is only one cost driver for each cost center

What are the 2 ways to calculate the extension of cost-center summary sheets?

differentiated reporting of fixed & variable costs

break down planned budget for fixed & variable costs

step-by-step plans

shows possible costs saved by increasing output volume

beneficial for uncertain environments

What are the tasks of the profit & loss calculation?

linkage of costs & revenues

comparison of costs & revenues to reveal a company’s profit

only possible for private companies that create revenues

determination of the profit per unit

contribution that a product/service makes to a company’s profit

determination of unit costs and prices on a per-unit basis necessary

determination of the net profit for a period

comparison of costs & revenues of an accounting period → net profit (also for individual products)

internal income statements more often produced → decision-making

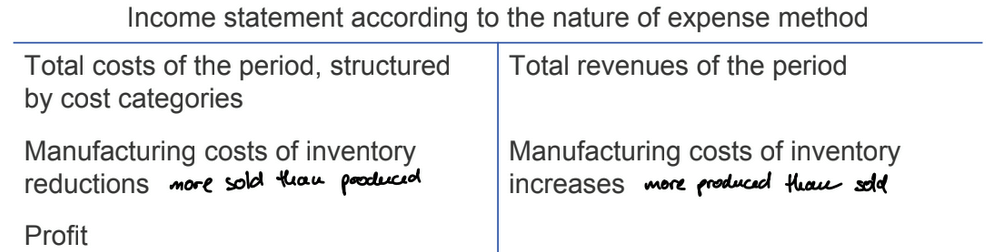

What is the basic problem of preparing an income statement, and what are the 2 methods to calculate the net profit of a period?

the quantities produced is different from the quantities sold

produced → manufacturing costs

sold → selling & shipping costs

methods to calculate the net profit of a period

nature of expense method: quantity produced as cost basis

cost-of-sales method: quantity sold as cost basis

How is the net profit calculated with the nature of expense method?

compare total costs (production) with total revenues (sell) of a period

any changes in inventory must be taken into account

mostly used by SMEs in Germany

What are the advantages & disadvantages of the nature of expense method?

advantages

simple calculation structure

easy integration into double-entry bookkeeping

overview of cost type structures

inventory changes can be immediately recognized

classification of cost categories usually already done in financial accounting → necessary information already available

disadvantages

inventory recording needed → time-consuming

unit cost calculation required for manufacturing costs

no indications for profit on product or functional area level

no differentiation of cost structures between functional departments

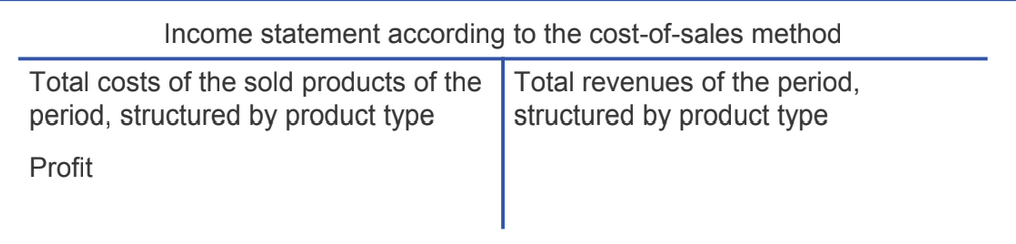

How is the net profit calculated with the cost-of-sales method?

comparison of costs & revenue on a product level, not category level

application of product costing → unit costs

total costs include manufacturing costs, and administrative, selling and shipping costs

more prevalent internationally, especially large companies

What are the advantages & disadvantages of the cost-of-sales method?

advantages

no stocktaking necessary

very fast profit determination

profit analysis on product level possible

disadvantages

difficult to integrate into double-entry bookkeeping

calculation of total cost necessary

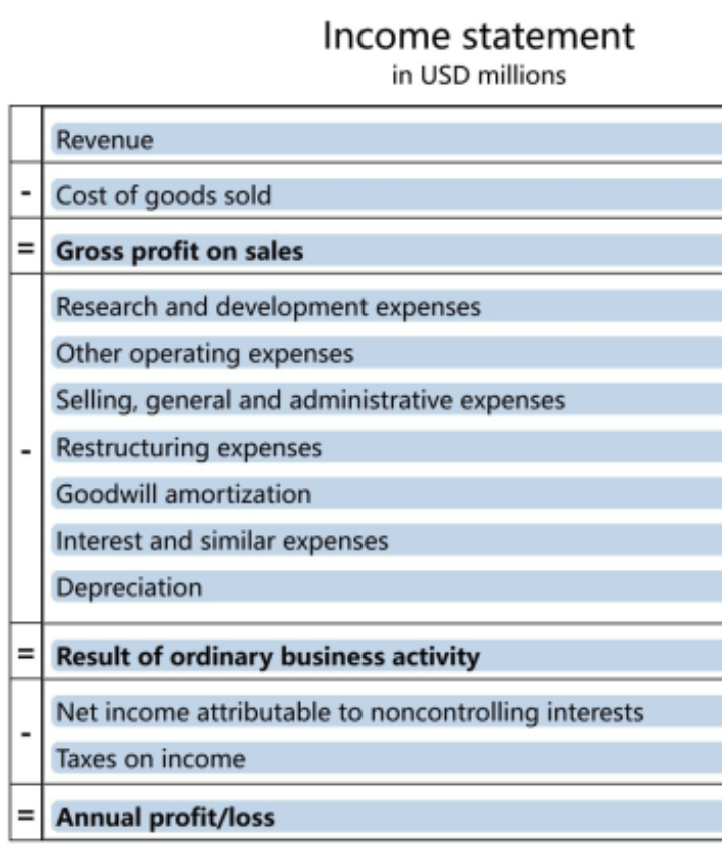

What are the different entries of an income statement?

What is the difference between absorption and variable costing for the income statement?

absorption costing: valuation of product units at full cost

variable costing: valuation of product units at variable cost, fixed costs shown separately

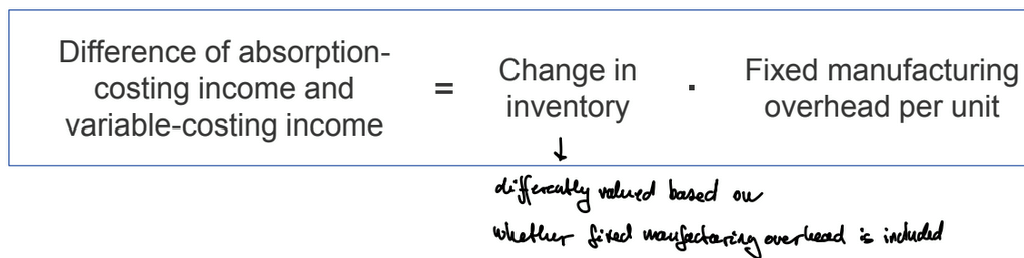

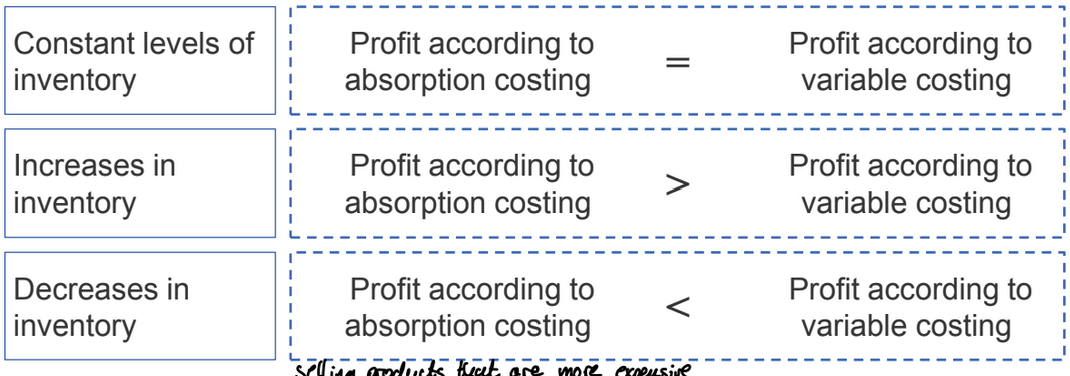

How does the operating income over multiple periods differ between absorption and variable costing

What are possible incentives for building up inventory under absorption costing?

higher production → higher profits without increase in sales

unit-related fix production overhead increases profit for each unit produced & stored

enables managers in making decisions not in the interest of the company

deferral of maintenance & repair → more capacity for production → increase profits short-term

increase of production of products that have a higher proportion of fixed production overhead