AP Macro Unit 3

5.0(2)

5.0(2)

Card Sorting

1/45

Earn XP

Description and Tags

Study Analytics

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

46 Terms

1

New cards

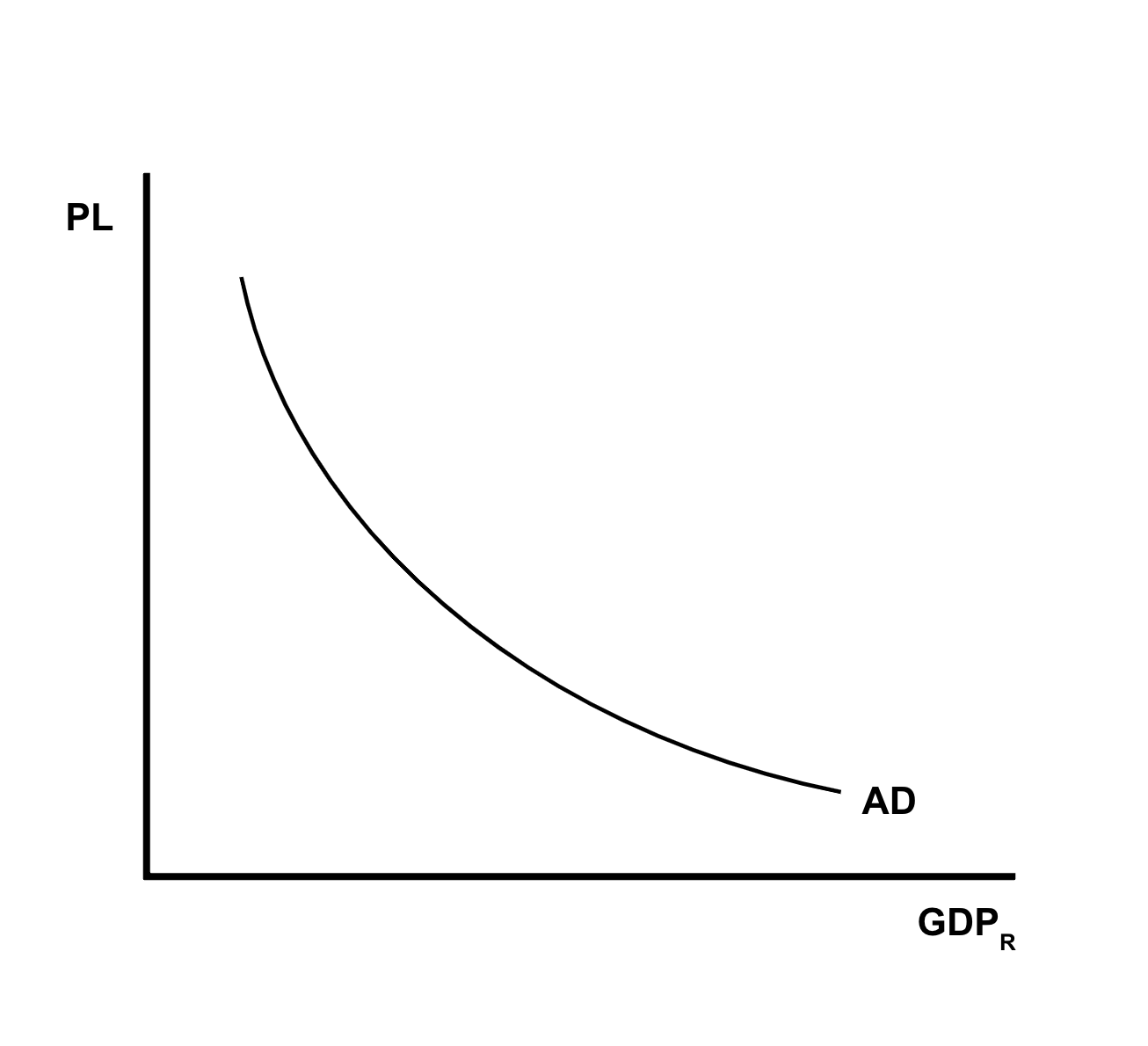

Aggregate Demand

all the goods and services (real GDP) that buyers are willing and able to purchase at different price levels

2

New cards

Aggregate Demand Curve

→ the demand by consumers, businesses, government, and foreign countries

→ downward slope

→ x-axis: real domestic output, y-axis: price level

→ downward slope

→ x-axis: real domestic output, y-axis: price level

3

New cards

Wealth Effect

→ higher price levels reduce the purchasing power of money; this decreases the quantity of expenditures

→ lower price levels increase the purchasing power and increase expenditures

→ Real Balance Effect

→ lower price levels increase the purchasing power and increase expenditures

→ Real Balance Effect

4

New cards

Interest Rate Effect

→ when the price level increases, lenders need to charge higher interest rates to get a REAL return on their loans

→ higher interest rates discourage consumer spending and business investment

→ higher interest rates discourage consumer spending and business investment

5

New cards

Foreign Trade Effect

→ when U.S. price level rises, foreign buyers purchase fewer U.S. goods and Americans buy more foreign goods

→ exports fall and imports rise causing real GDP demanded to fall

→ exports fall and imports rise causing real GDP demanded to fall

6

New cards

Shifters of Aggregate Demand

( 1 ) Change in Consumer Spending

( 2 ) Change in Investment Spending

( 3 ) Change in Government Spending

( 4 ) Change in Net Exports (X - M)

( 2 ) Change in Investment Spending

( 3 ) Change in Government Spending

( 4 ) Change in Net Exports (X - M)

7

New cards

Change in Consumer Spending

→ increase in disposable income

→ consumer expectations

→ household indebtedness

→ taxes

→ consumer expectations

→ household indebtedness

→ taxes

8

New cards

Change in Investment Spending

→ real interest rates (price of borrowing money)

→ future business expectations

→ business taxes

→ future business expectations

→ business taxes

9

New cards

Change in Government Spending

→ government expenditures

10

New cards

Change in Net Exports

→ exchange rates

→ national income compared to abroad

→ national income compared to abroad

11

New cards

Marginal Propensity to Consume (MPC)

how much people consume rather than save when there is a change in disposable income (always expressed as a decimal)

MPC = Change in Consumption / Change in Disposable Income

MPC = Change in Consumption / Change in Disposable Income

12

New cards

Marginal Propensity to Save (MPS)

how much people save rather than consume when there is a change in disposable income (always expressed as a decimal)

MPS = Change in Save / Change in Disposable Income

MPS = Change in Save / Change in Disposable Income

13

New cards

Calculating the MPS

1 / MPS or 1 / 1 -- MPC

14

New cards

Total Change in GDP

Total Change in GDP = Multiplier * Initial Change in Spending

15

New cards

Calculating the Tax Multiplier

MPC / MPS

The Tax Multiplier is always one less than the Spending Multiplier

The Tax Multiplier is always one less than the Spending Multiplier

16

New cards

MPS = 1 -- MPC

people can either save or consume

17

New cards

Total Change in GDP (w/Tax Multiplier)

Total Change in GDP = Tax Multiplier * Initial Change in Taxes

18

New cards

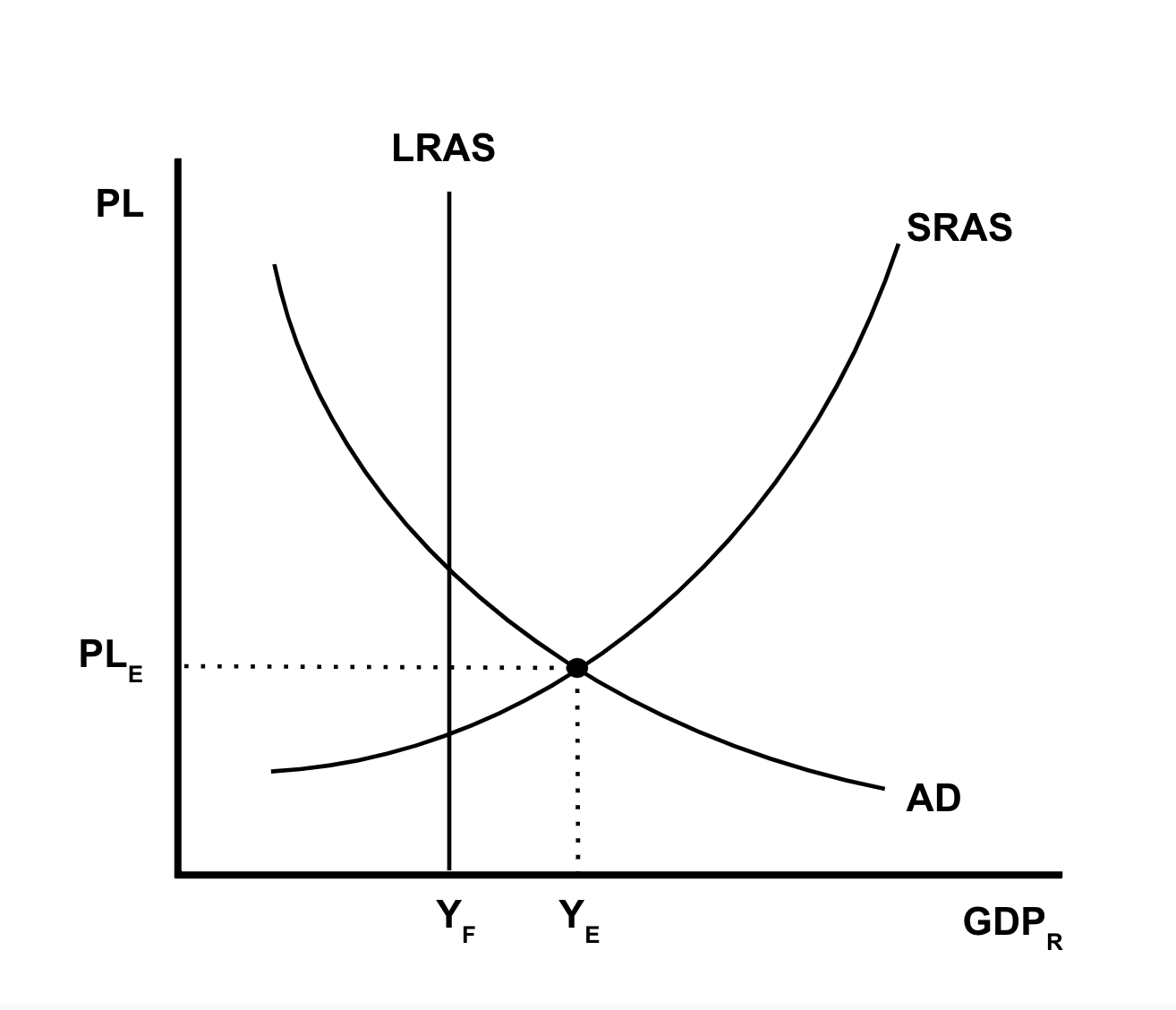

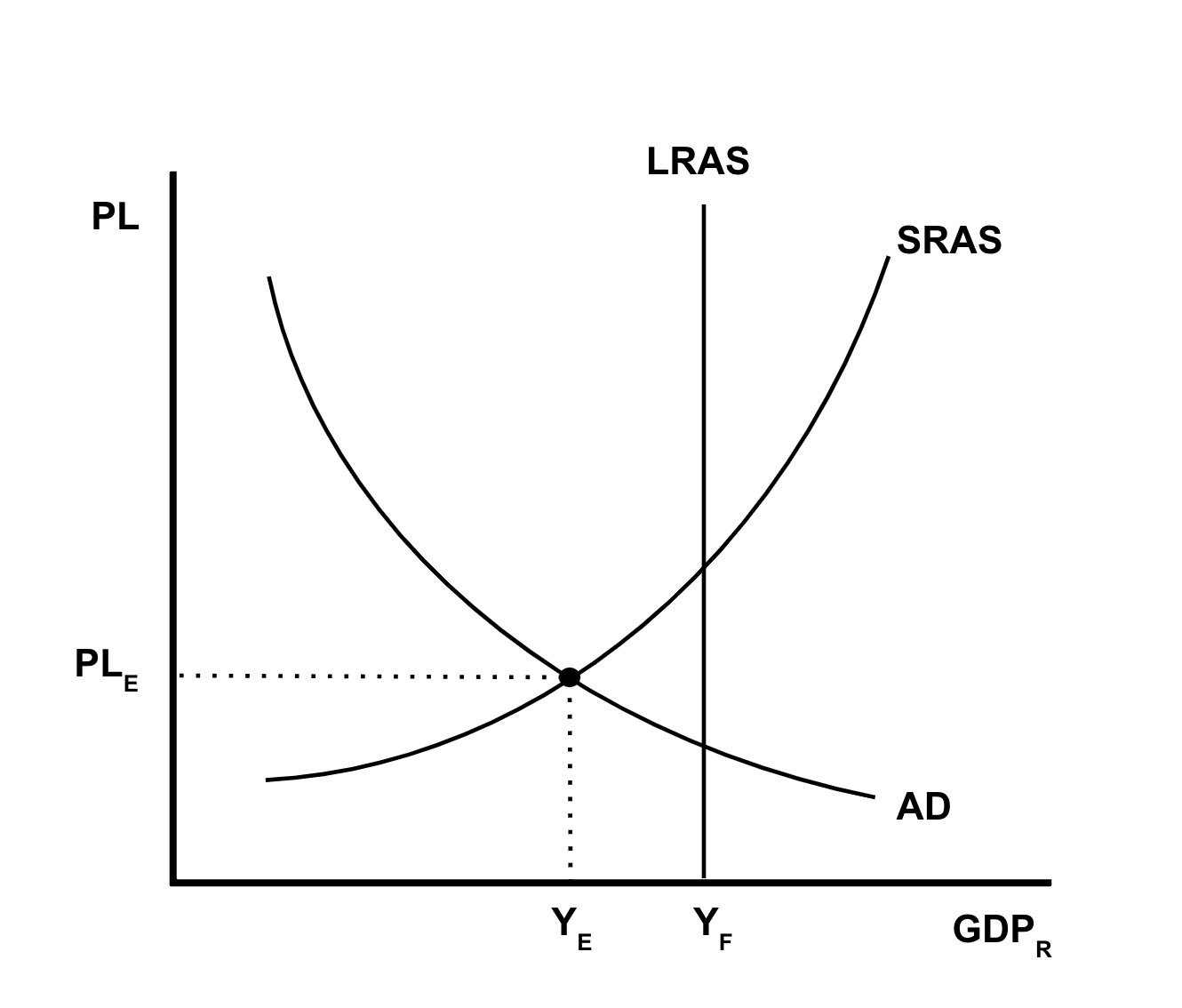

Aggregate Supply

the amount of goods and services (Real GDP) that firms will produce in an economy at different price levels, the supply for everything by all firms

19

New cards

Short-run Aggregate Supply (SRAS)

wages and resource prices are sticky and WILL NOT change as price levels change

20

New cards

Long-run Aggregate Supply (LRAS)

wages and resource prices are flexible and WILL change as price levels change

21

New cards

Shifters of Short-run Aggregate Supply

( 1 ) Change in Resource Prices

( 2 ) Change in Actions of the Government (NOT Government Spending)

( 3 ) Change in Productivity

( 2 ) Change in Actions of the Government (NOT Government Spending)

( 3 ) Change in Productivity

22

New cards

Shifter of SRAS: Change in Resource Prices

→ price of domestic and imported resources

→ supply shocks

→ inflationary expectations

→ supply shocks

→ inflationary expectations

23

New cards

Supply Shock

an unexpected event that suddenly changes the supply of a commodity resulting in an unforeseen change in price

→ negative supply shock: low supply, high price

→ positive supply shock: increased supply, low price

→ negative supply shock: low supply, high price

→ positive supply shock: increased supply, low price

24

New cards

Shifter of SRAS: Change in Actions of the Government

→ taxes on producers

→ subsidies for domestic producers

→ government regulations

→ subsidies for domestic producers

→ government regulations

25

New cards

Shifter of SRAS: Change in Productivity

→ technology

26

New cards

Shifters of Long-run Aggregate Supply

( 1 ) Change in Resource Quantity or Quality

( 2 ) Change in Technology

( 3 ) Change in Population

(SAME SHIFTERS AS THE PPC!!!!)

( 2 ) Change in Technology

( 3 ) Change in Population

(SAME SHIFTERS AS THE PPC!!!!)

27

New cards

Difference Between SRAS and LRAS

SRAS → in the short run, wages and resource prices are sticky and WILL NOT change when price level changes

LRAS → in the long run, wages and resource prices are flexible and WILL change when price level changes

LRAS → in the long run, wages and resource prices are flexible and WILL change when price level changes

28

New cards

AD/AS Equilibrium: Full Employment

Long Run Equilibrium

the economy is at potential output

the economy is at potential output

29

New cards

AD/AS Equilibrium: Inflationary Gap

ABOVE or BEYOND full employment, positive output gap

30

New cards

AD/AS Equilibrium: Recessionary Gap

BELOW or LESS THAN full employment, negative output gap

31

New cards

Stagflation

stagnant economy + inflation

SRAS decreases, causing high unemployment and high inflation

SRAS decreases, causing high unemployment and high inflation

32

New cards

Disposable Income

the amount of money households have to save or spend after taxes

33

New cards

(Supply) Cost-Push Inflation

(SRAS decrease)

→ tighter production costs increase prices

→ a negative supply shock increases the costs of production and forces producers to increase prices

→ tighter production costs increase prices

→ a negative supply shock increases the costs of production and forces producers to increase prices

34

New cards

(Demand) Demand-Pull Inflation

(AD increase)

→ demand pulls up prices: consumers want goods and services so bad they pull up prices

→ "too many dollars chasing too few goods"

→ demand pulls up prices: consumers want goods and services so bad they pull up prices

→ "too many dollars chasing too few goods"

35

New cards

Role of Consumers in the Economy

→ consumers will spend a certain amount no matter what, regardless of their income (this is usually called autonomous consumption)

→ consumer spending is made up of autonomous spending and disposable income

→ if incomes are less than autonomous spending, then there is dissaving (or negative savings)

→ consumer spending is made up of autonomous spending and disposable income

→ if incomes are less than autonomous spending, then there is dissaving (or negative savings)

36

New cards

How Does the Government Stabilize the Economy?

( 1 ) Fiscal Policy → actions by Congress to stabilize the economy

( 2 ) Monetary Policy → actions by the Federal Reserve Bank to stabilize the economy

( 2 ) Monetary Policy → actions by the Federal Reserve Bank to stabilize the economy

37

New cards

Discretionary Fiscal Policy

Congress creates a new bill that is designed to change AD through government spending or taxation

→ one problem is lag times due to bureaucracy

→ it takes time for Congress to act

→ EX.) in a recession, Congress increases spending

→ one problem is lag times due to bureaucracy

→ it takes time for Congress to act

→ EX.) in a recession, Congress increases spending

38

New cards

Non-Discretionary Fiscal Policy

(AKA: Automatic Stabilizers)

Permanent spending or taxation laws enacted to work counter-cyclically to stabilize the economy

→ when GDP goes down, government spending automatically increases, and taxes automatically fall

→ EX.) Welfare, Unemployment, Income Tax

Permanent spending or taxation laws enacted to work counter-cyclically to stabilize the economy

→ when GDP goes down, government spending automatically increases, and taxes automatically fall

→ EX.) Welfare, Unemployment, Income Tax

39

New cards

Contraction Fiscal Policy (The BRAKE)

Laws that reduce inflation, decrease GDP (close an Inflationary Gap)

→ decrease government spending

→ increase taxes (decrease disposable income)

→ combinations of the two

→ decrease government spending

→ increase taxes (decrease disposable income)

→ combinations of the two

40

New cards

Expansionary Fiscal Policy (The GAS)

Laws that reduce unemployment and increase GDP (close recessionary gap)

→ increase government spending

→ decrease taxes (increasing disposable income)

→ combinations of the two

→ increase government spending

→ decrease taxes (increasing disposable income)

→ combinations of the two

41

New cards

Timing and Fiscal Policy

Fiscal Policy has three time lags:

( 1 ) Recognition Lag → Congress must react to economic indicators before it's too late

( 2 ) Administrative Lag → Congress takes time to pass legislation

( 3 ) Operational Lag → spending/planning takes time to organize and execute (changing taxing is quicker)

( 1 ) Recognition Lag → Congress must react to economic indicators before it's too late

( 2 ) Administrative Lag → Congress takes time to pass legislation

( 3 ) Operational Lag → spending/planning takes time to organize and execute (changing taxing is quicker)

42

New cards

The Multiplier Effect

the idea that an initial change in spending will set off a spending chain that is magnified in the economy; the strength of the multiplier depends on the amount that consumers spend of new income

43

New cards

Autonomous Consumption

the minimum amount of consumer spending when people have no income

44

New cards

LRAS Self-Adjustment: Positive Output Gap

SRAS will shift left due to an increase in expected inflation, which causes wages to increase

45

New cards

LRAS Self-Adjustment: Negative Output Gap

SRAS will shift to the right due to a decrease in wages and resource prices, which causes production costs to fall

46

New cards

Automatic Stabilizers

policies that are already in place in an economy due to previously passed legislation