Microeconomics Exam 1

1/54

Earn XP

Description and Tags

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

55 Terms

Cost-benefit principle

Costs and benefits are the incentives that shape decisions. Pursue only choices with benefits at least as large as cost

Opportunity cost principle

True cost of something is the next best alternative that you have to give up

Marginal principle

Decisions about quantities are best when made incrementally, so break “how many?” questions into smaller marginal decisions

Interdependence principle

Your best choice depends on other factors:

Dependence between individual choices

Dependence on others’ choices

Dependence between markets

Dependence through time

Marginal Cost

Extra cost from one extra unit of a good

Scarcity

Limited resources

Economic Surplus

Total benefits minus total cost

Framing Effect

When a decision is affected by how a choice is described or framed

Opportunity cost

The next best alternative you give up when making a decision

Sunk cost

Cost already incurred that cannot be reversed and should be ignored

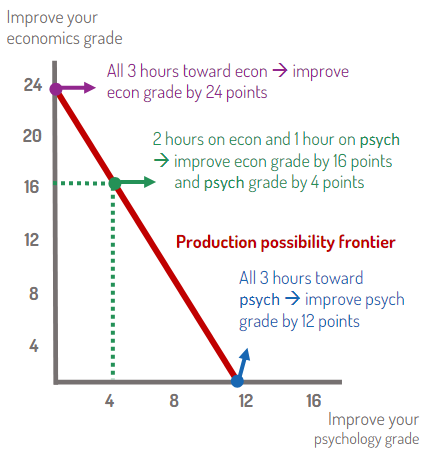

Production Possibility Frontier (PPF)

Shows the different sets of outputs attainable with scarce resources. Used to help visualize the trade-offs of opportunity cost

Willingness to pay

Conversion of non financial costs or benefits into their monetary equivalent

Marginal benefit

Extra benefit from one extra unit of a good

Rational Rule

If something is worth doing then keep doing it until marginal benefit = marginal cost

Economics

The study of choices

Complementary goods

Goods that work well together

Congestion Effect

A good becomes less valuable when other people use it

Decrease in demand

Shift of demand curve to the left

Diminishing marginal benefit

Each additional item yields a smaller marginal benefit than the previous unit

Ceteris Parabus

holding all other things constant

Increase in demand

Shift of demand curve to the right

Individual demand curve

Curve that plots the quantity of an item that an individual plans to purchase at each price

Inferior goods

A good for which a higher income causes a decrease in demand

Law of demand

Tendency for quantity demanded to be higher when the price is lower

Market demand curve

Composed by adding the quantity demanded at each price in multiple individual demand curves, still looks similar.

Movement along demand curve

As price increases, quantity demanded decreases

Network Effect

Good which becomes more useful as other people use it.

Normal good

A good for which a higher income causes an increase in demand

Rational rule for buyers

Buy one more if the marginal benefit ≥ price

Shift in demand curve

Occurs when changes to any of these occur: Income, Preferences, Price of related goods, Expectations, Network and congestion effects, Type and number of buyers

Substitute goods

Goods that can replace each other

Complements in production

Goods that are made together

Decrease in Supply

Shift of supply curve to the left

Diminishing marginal product

Marginal product declines as input increases

Fixed costs

Costs that don’t vary based on changes in output produced

Increase in supply

Shift of the supply curve to the right

Individual Supply Curve

Graph plotting the quantity of an item that a business plans to sell at each price

Law of Supply

The higher the price is, the higher the quantity supplied will be

Marginal Product

Increase in output due to additional input

Market Supply Curve

Total quantity supplied by the entire market at each price

Movement along supply curve

As price increases, quantity supplied increases

Perfect competition

Occurs when goods are identical and have many buyers and sellers that are each relatively small within the market

Price taker

A seller who charges the prevailing price because they cannot affect it.

Rational Rule for Sellers in Competitive Markets

Supply one more unit until price ≥ marginal cost

Shift in Supply Curve

Occurs when changes to any of these occur: Input Prices, Productivity and technology, prices of related outputs, expectations, the type and number of sellers

Substitutes in Production

Alternative uses of resources

Variable costs

Costs that vary with the amount of output produced

Equilibrium

A point at which there is no tendency for change, occurs when the market quantity demanded is equivalent to the quantity supplied

Equilibrium Price

Price at which the market is in equilibirum

Equilibrium Quantity

Quantity demanded and supplied when the market is in equilibrium

Market

A setting that brings together buyers and sellers

Market Economies

Each person makes their own production and spending decisions

Planned Economies

Centralized decisions are made about what is produced, how, by whom, and who gets what.

Shortage

When the market quantity demanded is greater than the quantity supplied

Surplus

When the market quantity supplied is greater than the quantity demanded