Econ 200 Exam 1 UNL With 100% accuracte solutions + rationales

1/72

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

73 Terms

Microecnomics

the study of the economy at the small-scale level, examning individuals and specific markets

Macroeconomics

the study of the economy at the large-scale level, examining total output, price level, and aggregates measures

resource

any item that is used to produce goods and services

land

all natural resources used in production

labor

all physical and mental activity devoted to producing goods and services

capital

the tools, machinery, infrastructure, and knowledge used to produce goods and services

entrepreneurial ability

the talent or ability to combine land, labor, and capital to produce goods or services

scarcity

inability of limited resources to satisfy unlimited wants

importance of scarcity in economics

scarcity of goods plays a significant role in affecting competition in any price-based market. Because scarce goods are typically subject to greater demand, they often command higher prices as well

opportunity cost

the value of the opportunity that you gave up when you chose an alternative

marginal benefit

maximum amount a consumer is willing to pay for an additional good or service or the additional satisfaction that consumer receives when the additional good or service is purchased

marginal cost

the change in cost that comes from making more of something

marginal decision making

The process of making choices in increments by evaluating the additional, or marginal, benefit against the additional, or marginal, cost of an action.

optimization

maximize overall benefit; marginal benefit > or equal to marginal cost

prodution possibilities frontier (PPF)

a graph that shows the possible combinations of two different goods/services that can be produced with fixed resources

comparitive advantage

the ability to produce a good at a lower opportunity cost than another producer

If in the time it takes you to iron one shirt, you could wash 10 dishes, but in the time it takes your roommate to iron one shirt, she could wash 20 dishes, who has the comparative advantage?

you because you only give up 10 dishes while she gives up 20

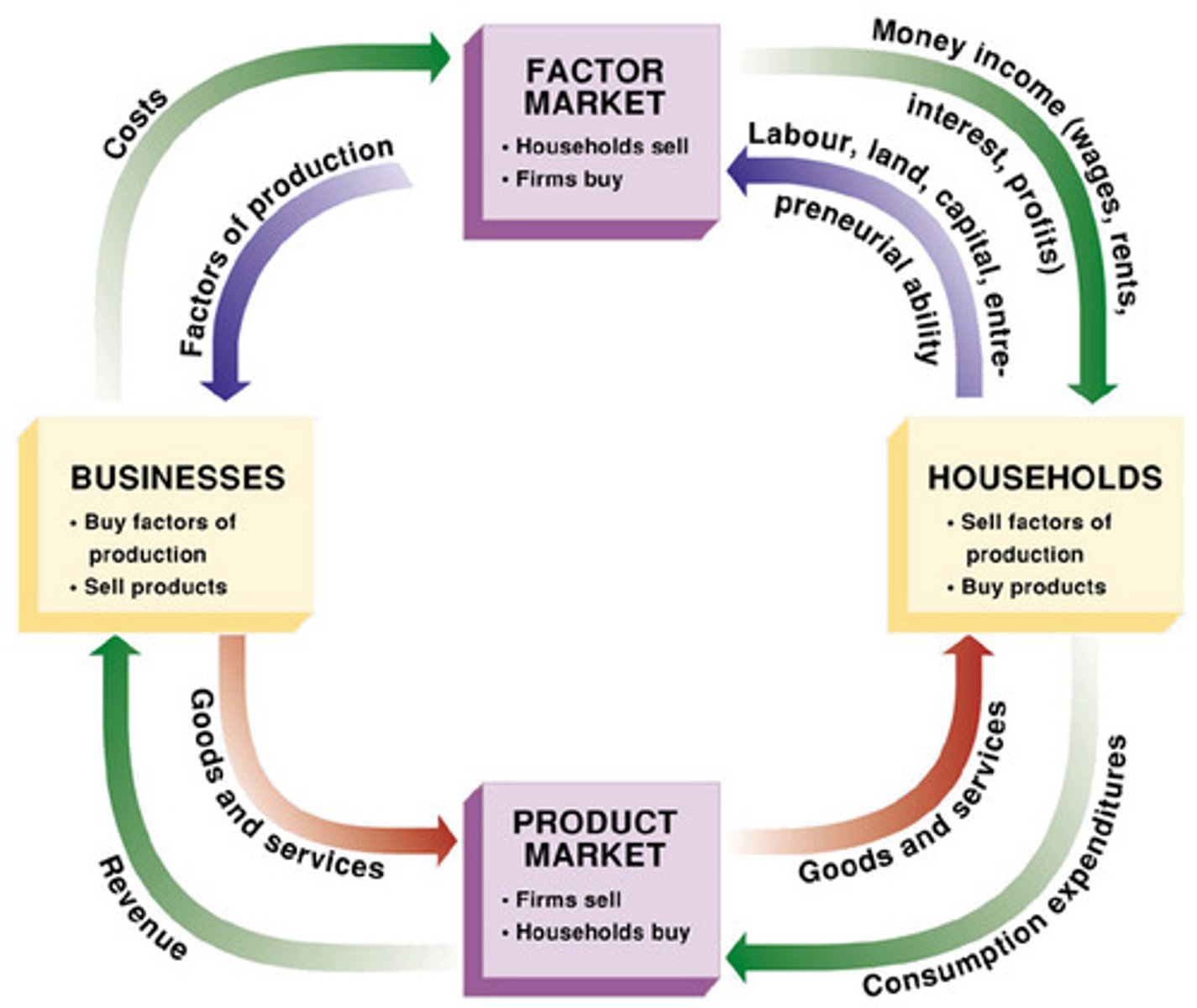

circular flow model

market vs command system

Market economies utilize private ownership of the means of production and voluntary exchanges/contracts. In a command economy, governments own the factors of production such as land, capital, and resources.

prices and quantities traded are determined by

the interaction of buyers and seller in a market

as the price of a good increases, quantity demanded...

decreases (law of demand)

demand curve

a graph of the relationship between the price of a good and the quantity demanded

demand curves are downward sloping due to

income effect, substitution effect, and diminishing marginal utility

income effect

the effect that a change in price of a good has on the purchasing power of income

substitution effect

the effect that a change in the price of one good has on the demand for another (price of coke goes up, demand for pepsi goes up)

diminishing marginal utility

commodities become less valuable as more of them are acquired

a change in demand vs. a change in the quantity demanded.

A change in demand means that the entire demand curve shifts either left or right. A change in quantity demanded refers to a movement along the demand curve, which is caused only by a chance in price

as the price of a good increases, quantity supplied...

increases (law of supply)

supply curve

a graph of the relationship between the price of a good and the quantity supplied

Factors that shift supply

taxes and subsidies placed on businesses, resource costs, and technological changes

a change in supply vs. a change in quantity supplied

a change in supply is a shift of the entire supply curve in response to something besides price;

a change in quantity supplied is a movement along the supply curve in response to a change in price.

equilibrium price

the price at which the quantity supplied equals the quantity demanded

equilibrium quantity

the quantity at which the quantity supplied equals the quantity demanded

shortage

quantity demanded is greater than quantity supplied

surplus

quantity supplied is greater than quantity demanded

increase in supply (rightward shift of supply curve) causes equilibrium price to...

fall

increase in demand causes the equilibrium price to...

rise

A decrease in demand and an increase in supply causes equilibrium price to...

fall

An increase in demand and a decrease in supply will cause equilibrium price to...

rise

price ceiling

a maximum price a which a good can be sold

does a price ceiling above or below equilibrium price affect the market (binding)

below

price floor

a minimum legal price at which a good can be sold (ex: minimum wage)

does a price floor above or below equilibrium price affect the market (binding)

above

elasticity

a measure of how responsive one variable is to a change in another variable

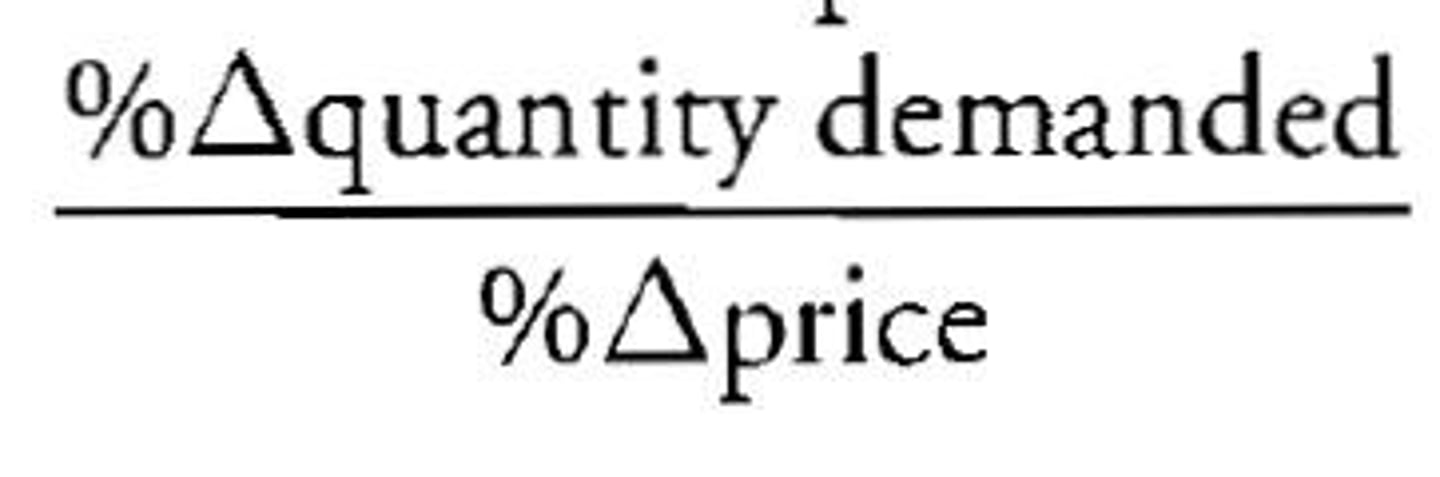

price elasticity of demand

A measure of how responsive demand for a product is to changes in price

price elasticity of demand equation

E > 1

elastic

E < 1

inelastic

E = 1

unit elastic

why does the elasticity of demand change along a linear demand curve?

the linear demand curve uses changes in price and quantity while elasticity uses percentage changes in price and quantity

total revenue

Price x Quantity

if demand is elastic, an increase in price will ___________ total revenue

decrease

if demand is inelastic, an increase in price will ___________ total revenue

increase

Goods with substitutes have _______ demand

Elastic - Goods with close substitutes tend to have more elastic demand because it is easier for consumers to switch from that good to others

goods that are viewed as luxuries have _______ demand

elastic

Describe the relationship between private and social benefits and costs.

Social costs take into account private costs and externalities that come as a result of a given economic decision

private marginal cost

the cost to the producer of an additional unit of a good or service

private marginal benefit

the benefit to the consumer of an additional unit of a good or service

external marginal cost

the cost of an additional unit of a good or service that is imposed on people other than the producer

external marginal benefit

the benefit of an additional unit of a good or service that is enjoyed by people other than the direct consumer of the good or service

positive externality

a benefit that is enjoyed by a third-party as a result of an economic transaction

negative externality

the harm, cost, or inconvenience suffered by a third party as a result of an economic transaction

rival

consumption of a good by on person reduces the quantity available for consumption by others

excludable

people can be prevented from consuming a good

private good

rival and excludable

public good

nonrival and nonexcludable

free rider problem

when a good is nonexcludable, people will choose to consume the good without paying for it (ex: firework show)

marginal benefit of preventing pollution

reduction in health expenditures and increased quality of life

marginal cost of preventing pollution

opportunity cost of money used because it could be used to fund education, homelessness, national defense, etc.

optimal level of pollution

marginal benefit and marginal cost are equal

property rights

the exclusive right to determine how a resource is used

market failure

a situation in which the market fails to produce the efficient level of output

poorly defined property rights causes

market failure because there is no solution that meets the needs of all parties involved