SUPA Econ: Chapter 6 (Power of the Invisible Hand)

1/40

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

41 Terms

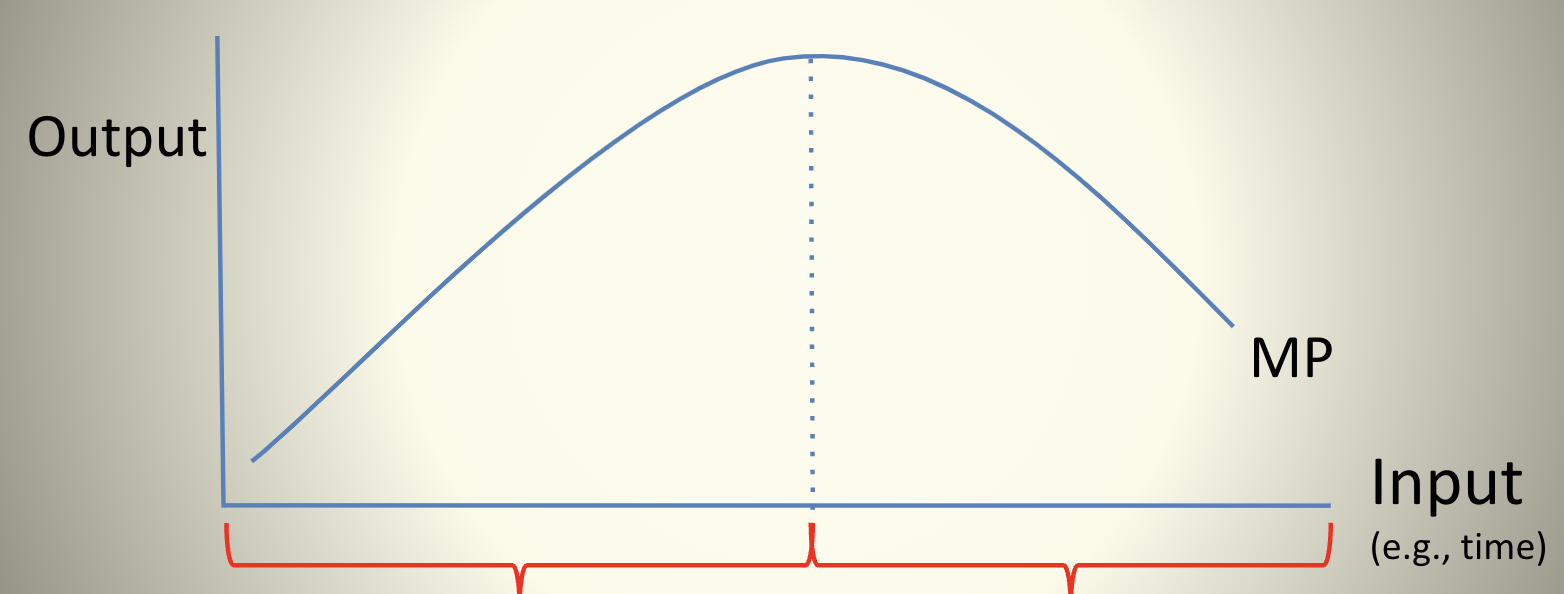

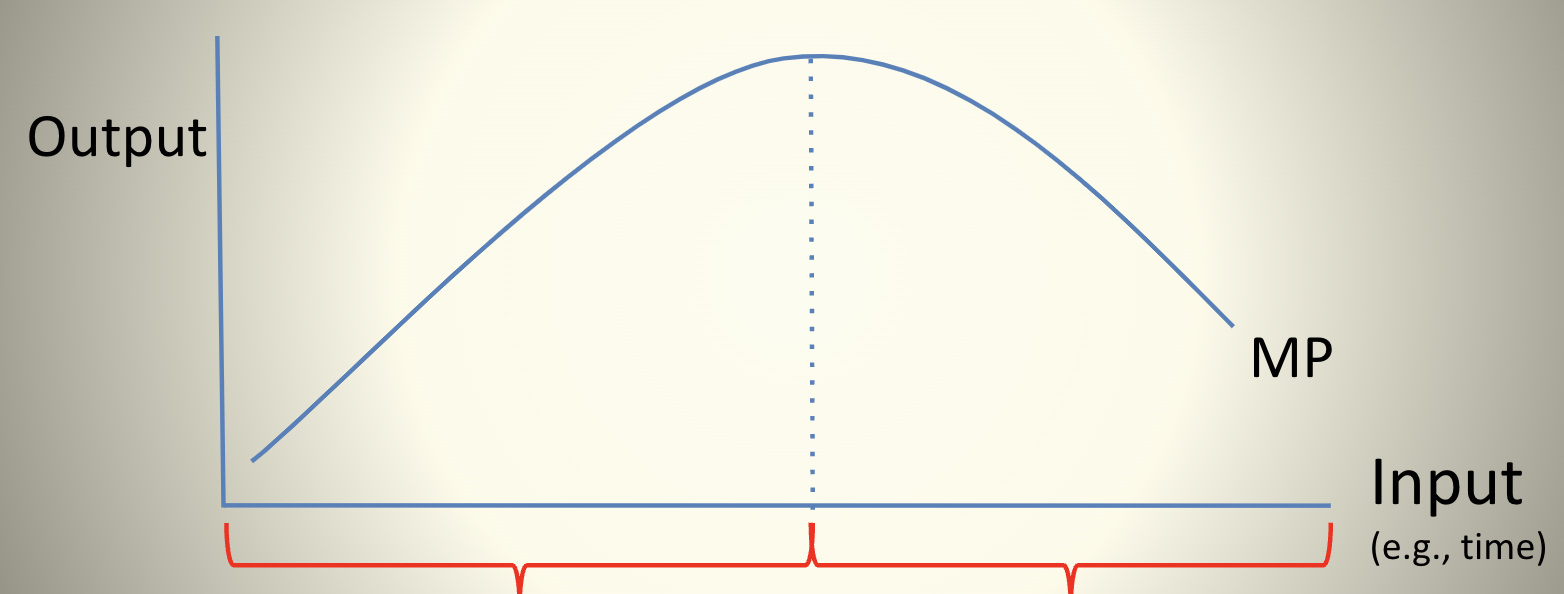

Successive units of input are more productive, so successive units of output

cost less (MC↓)

Successive units of input are less productive so successive units of output

cost more (MC↑)

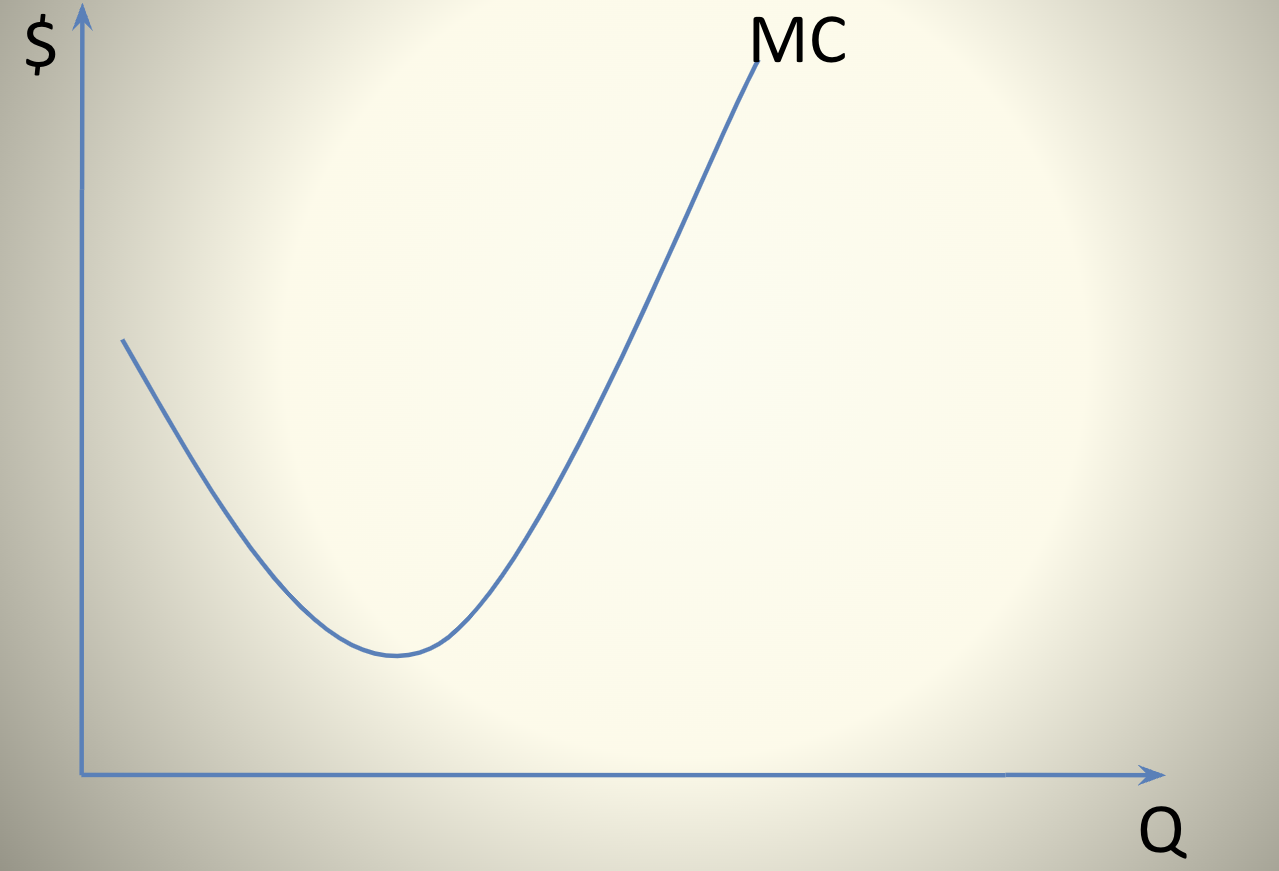

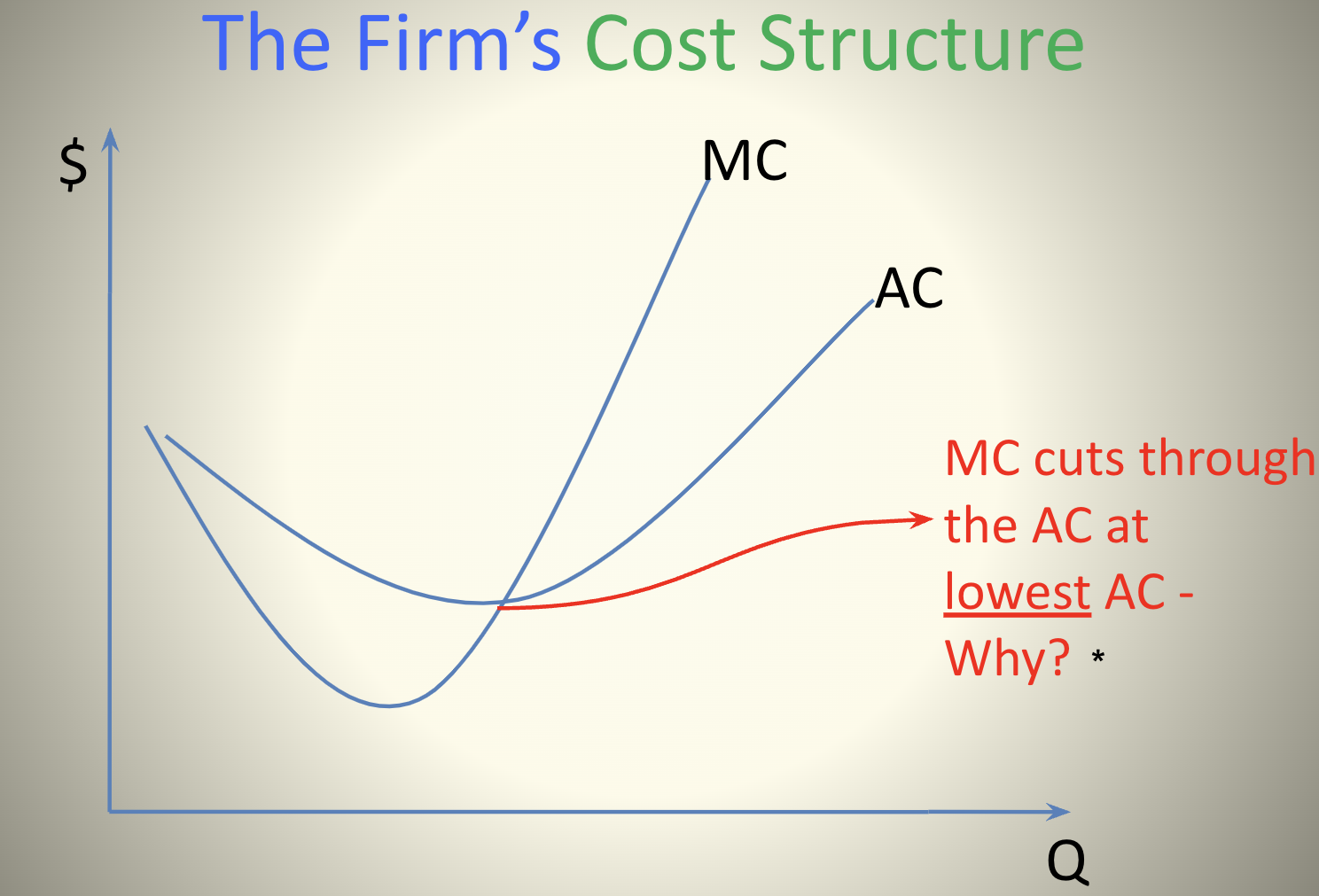

The Firm’s Cost Structure

the MC falls then rises

The ____ sets the price

market

Firm is a ______ _______

Price taker

The Firm under Perfect Competition

No market failure, no market power, Market determines price - firm is a “price taker” It's demand line is perfectly elastic at the market price

Relationship of Average and Margin

The margin always pulls the average in its direction. If the margin is above the average, it pulls the average up. If the margin is below the average, it pulls the average down

Marginal Cost (MC)

How much it costs to make the next unit

Average cost (AC)

generic measure of cost, total cost of production divided by the total units produced

You average 27 hits a season. This year (at the margin) you hit 35. What happens to the average?

it increases

Total Revenue

Price X Quantity (pXQ)

Total Cost

Average Cost X Quantity (ACxQ)

You get profit when

Total Revenue (TR) > Total Cost (TC)

You have a loss when

Total Revenue (TR) < Total Cost (TC)

Variable Costs

costs that change depending on how much you produce (ex. flour, cheese (for pizzas))

Fixed Costs

Costs that generally remain the same, no matter how much you produce (ex. Pizza Ovens)

Profit

Total Revenue (TR) - Total Cost (TC)

Total cost includes a

normal return (a sufficient return to make it worth staying in business)

any positive profit is good, but

not necessary to stay in business

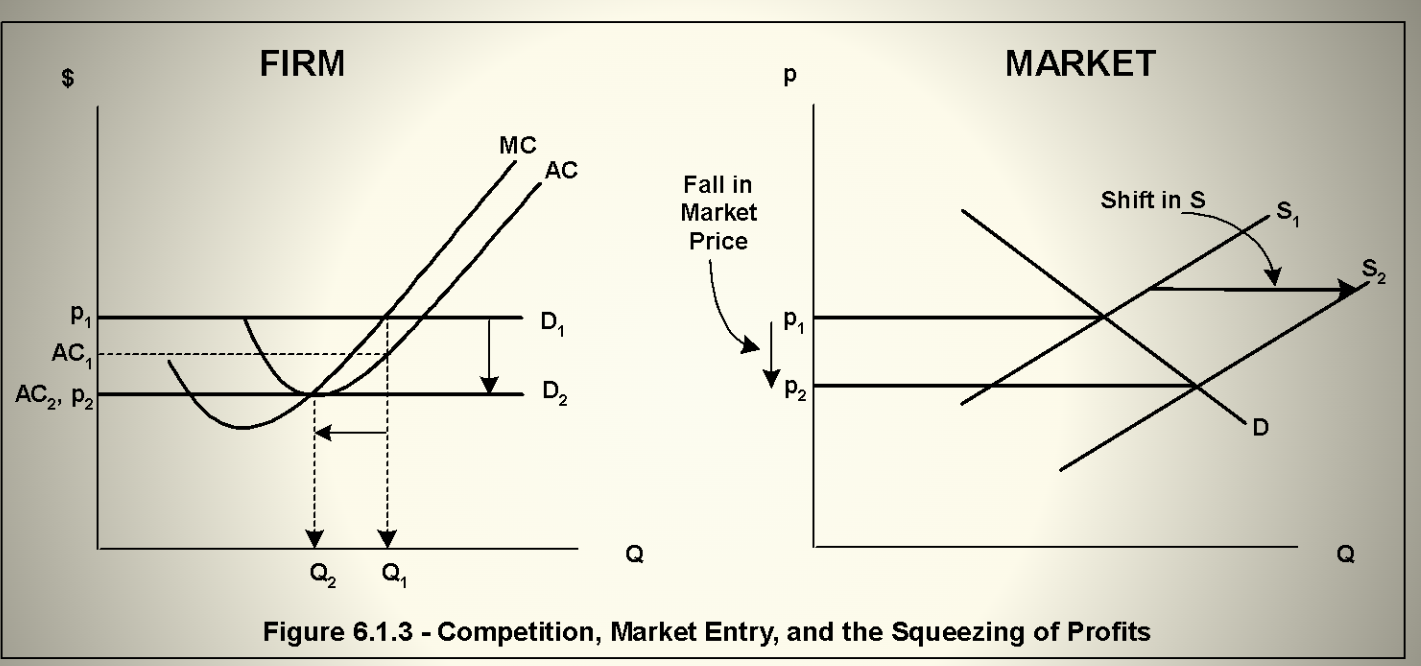

Dynamics of Perfect Competition

Profit attracts competitors, Competitors enter market, Market Supply increases, Market price falls, Falling market price squeezes firm’s profit. This dynamic continues so long as there is any profit to attract competitors.

Firm vs Market Graph

Firm has MC and AC while Market has supply and demand

When Profit is Gone

Firms are mad (they love the profit), but society is served

All firms are forced to

produce at the lowest average cost, the most efficient method production

Firms don’t choose efficiency. They are force to be efficient by

Perfect Competition

How does an entrepreneur get back to a profit-making condition without cheating?

By being imaginative and innovative, lowering cost structure by coming up with a more efficient way to produce

When firms are experiencing a loss

someone has to go (and someone will)

Firms exiting from the market

shifts market supply left and raises price

Price will rise until

all losses are gone and remaining firms are simply making a normal return

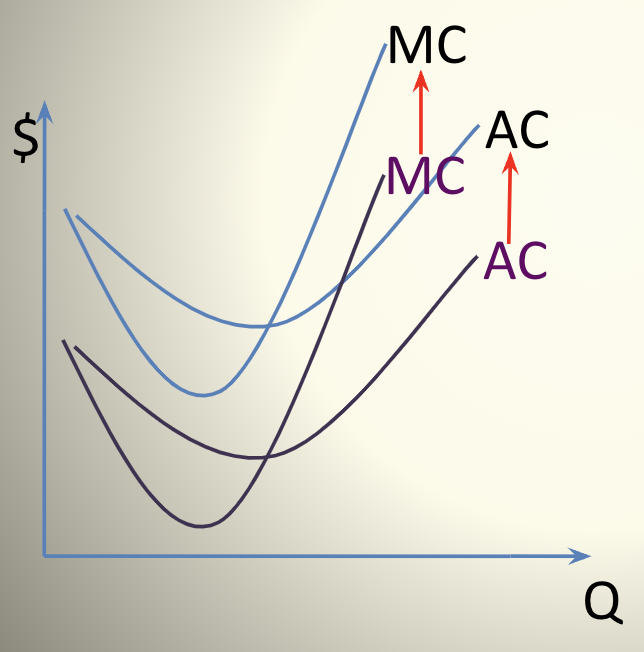

If the cost of inputs go up or the technology gets worse, then

at any given quantity (Q) the MC and AC will go up raising the cost structure

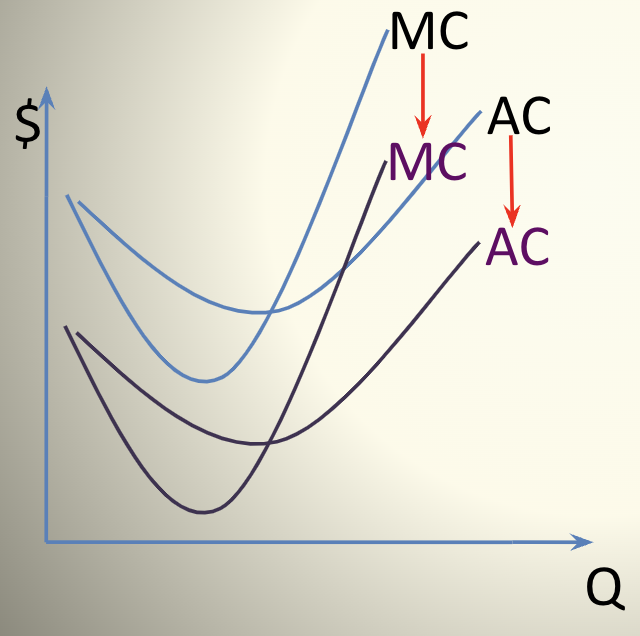

If the cost of inputs go down or the technology improves then

at any given quantity (Q) the MC and AC will go down, lowering the cost structure

Leader firm with lower cost structure

will enjoy a profit until others figure out the new more efficient production technique

The leader’s profit is ephemeral (lasting for a very short time). Competitors will figure out and copy the innovations. So to stay ahead and continue to enjoy a profit requires ever more

innovation

Perfect Competition drives all firms to not only be most efficient but to become

ever more efficient

From a given set of resources we get an

ever growing output (a bigger societal pie)

PC requires __________ _______ to ensure a fair, keen competition (ex: no market power)

Commutative Justice

Does PC ensure Distributive Justice

No. One will get a share proportional to one’s share of the initial endowment, and this initial distribution can be quite unjust. This is a moral, not an economic question.

When profits have been driven to zero by competition

Price = MC = AC (At the bottom of the AC line [includes normal returns] This is the most efficient point)

The self-interested behavior of seeking profits leads to the

most efficient outcome

Markets encourage

creativity and innovation/inventiveness

If you have negative cross-price elasticity, and we lower the price of hamburgers, what happens?

If you have a negative cross-price elasticity and lower the price of hamburgers, the demand for the complementary good (like french fries or soda) will also increase

Total Cost

Total Costs = Variable Cost + Fixed Cost