DYNAMIC / w2

1/23

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

24 Terms

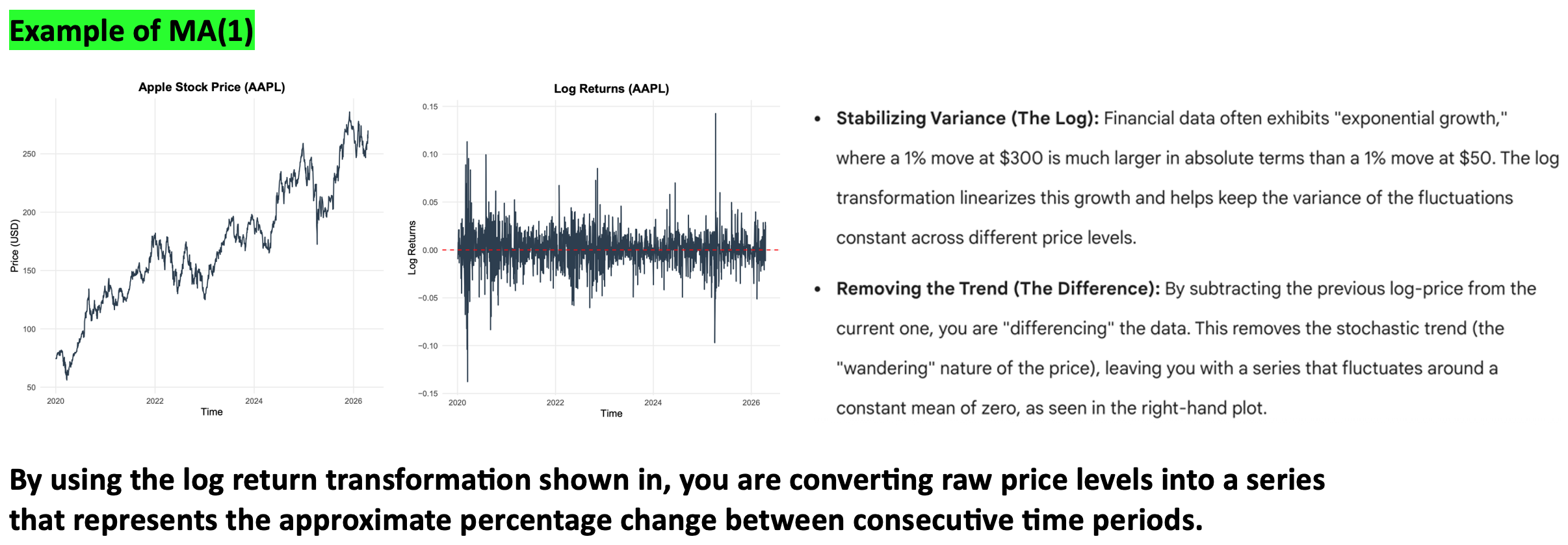

Example of MA(1)

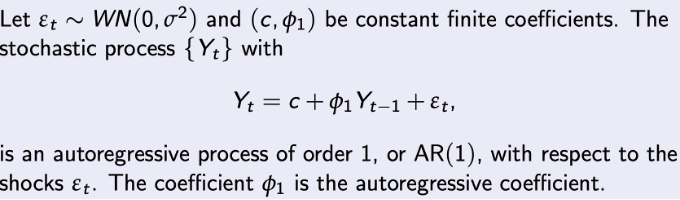

AR(1) process

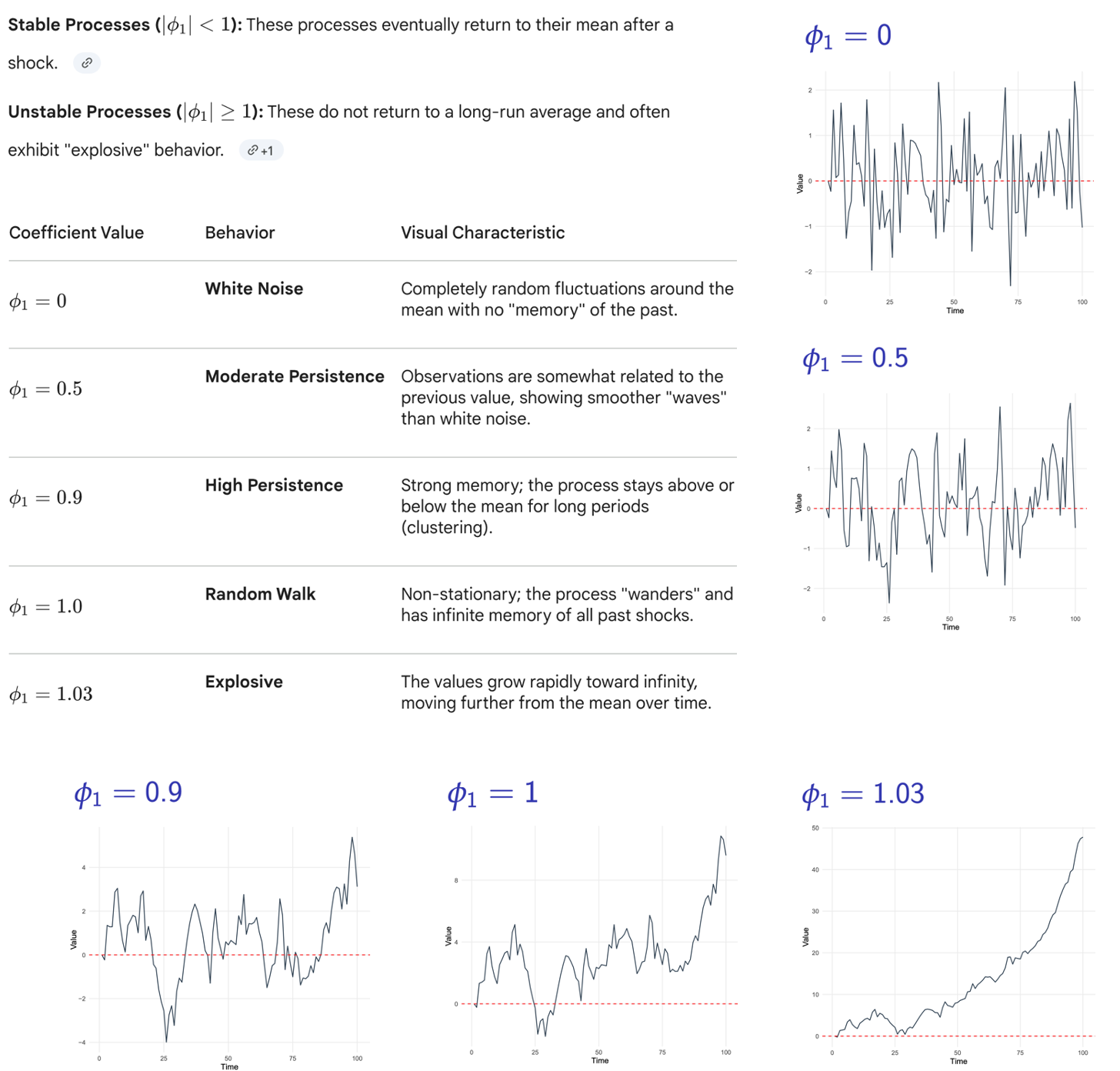

Stable vs Unstable Processes

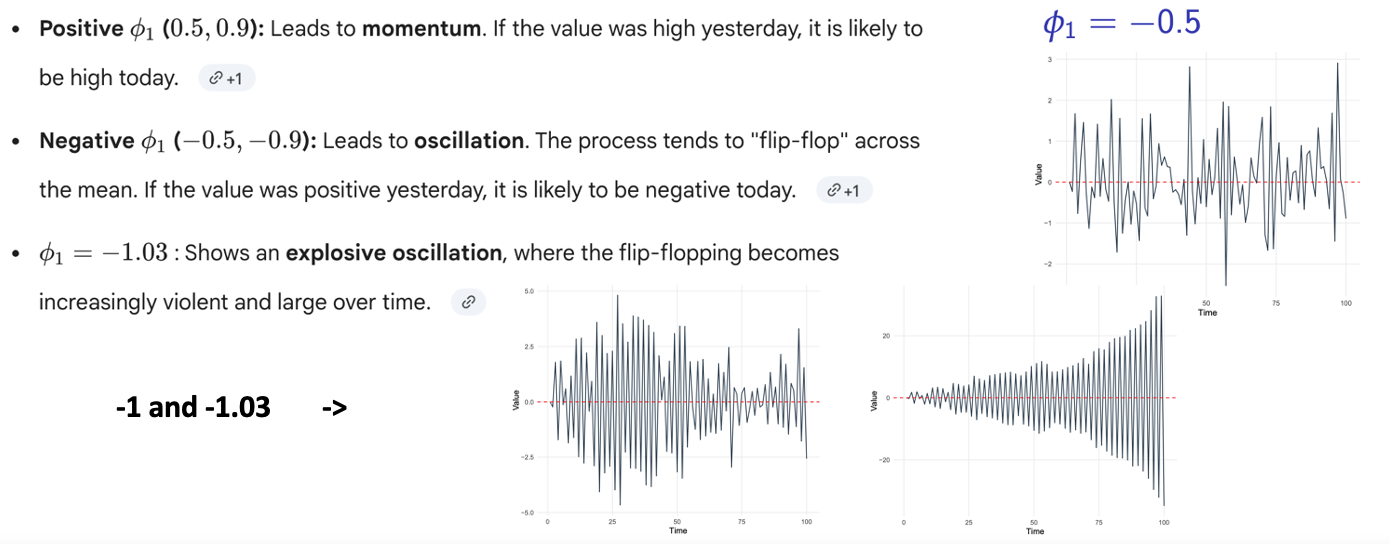

Coefficient Values and their Behavior

Positive vs Negative Coefficient Values

AR(1) process

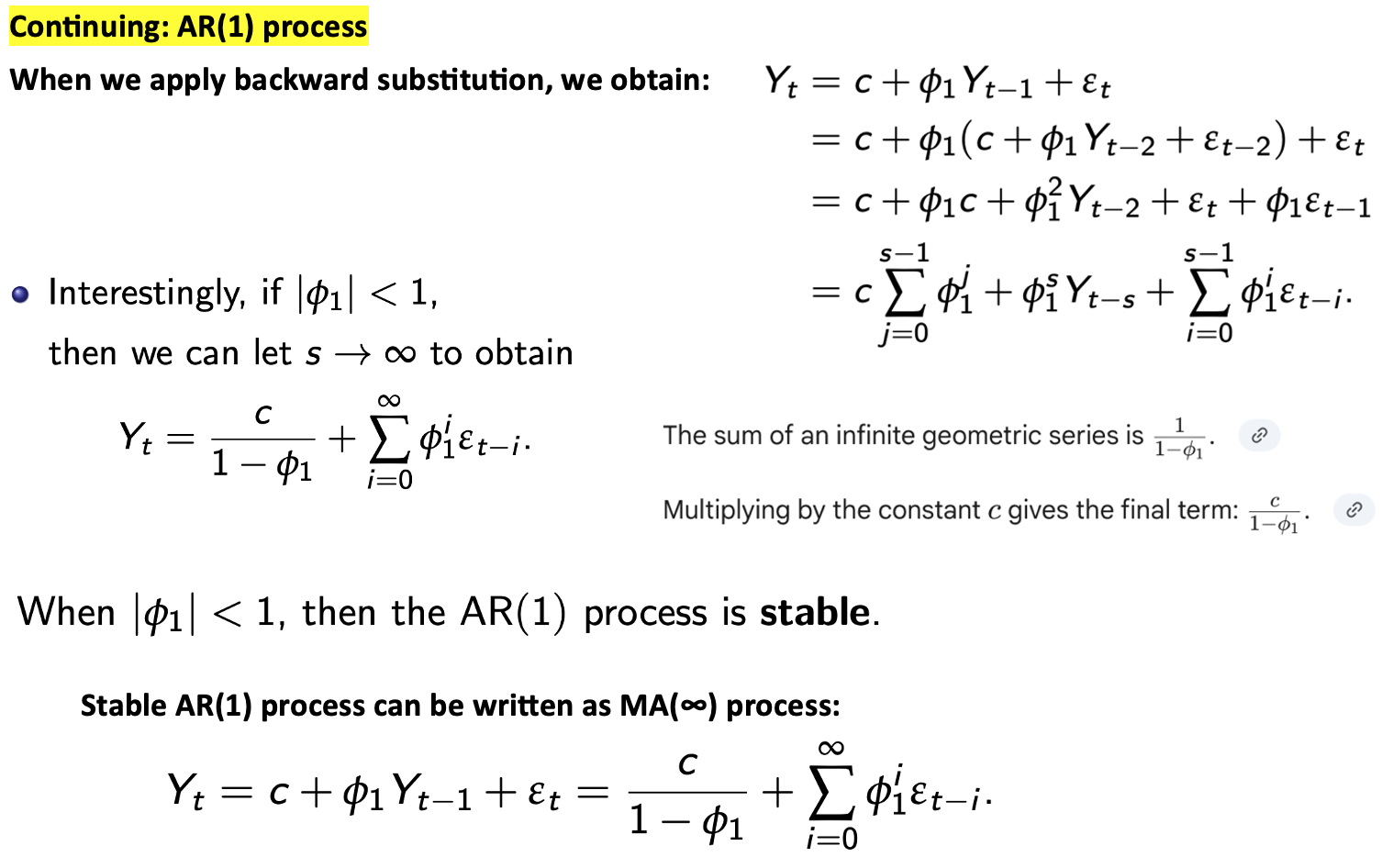

Backward Substitution

Writing as MA(∞) Process

AR(1) process

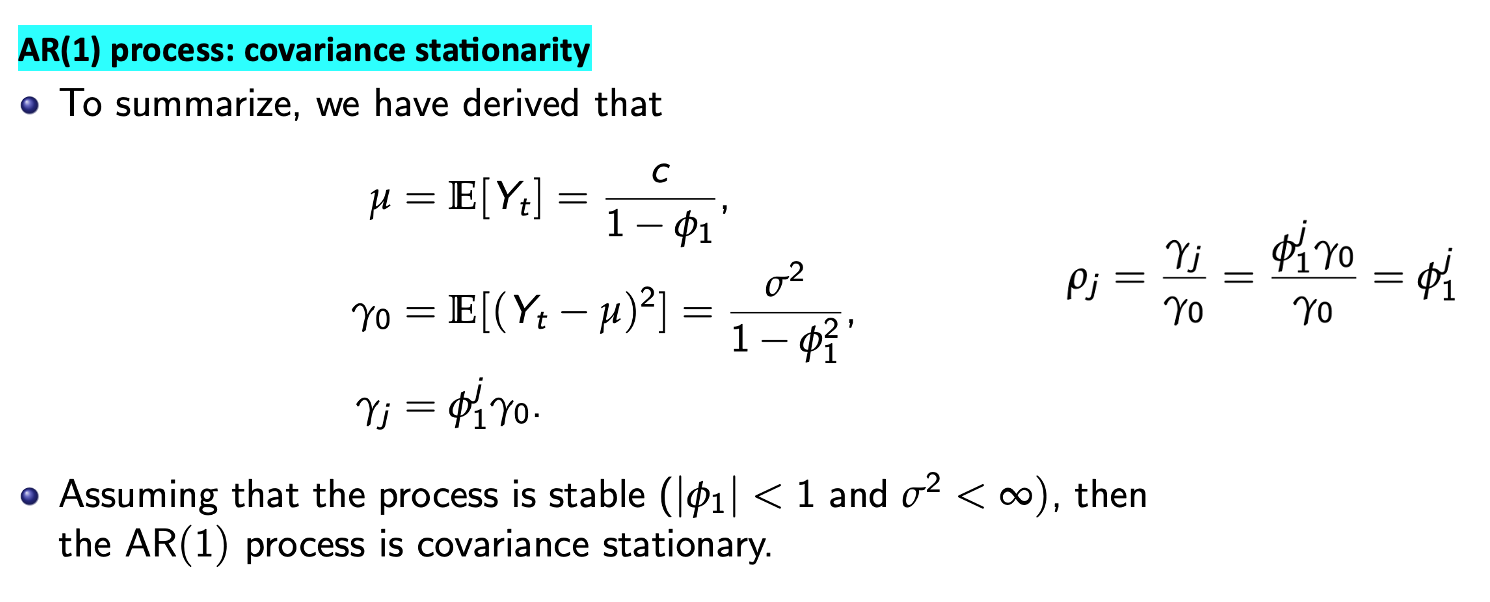

Deriviations + Covariance Stationarity

Initial Conditions

AR(p) Process

AR(p) Process

Example

MA(∞) representation of an AR(p) process

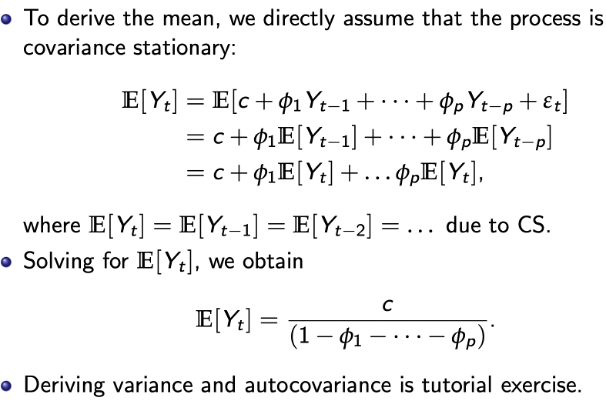

Population moments of an AR(p)

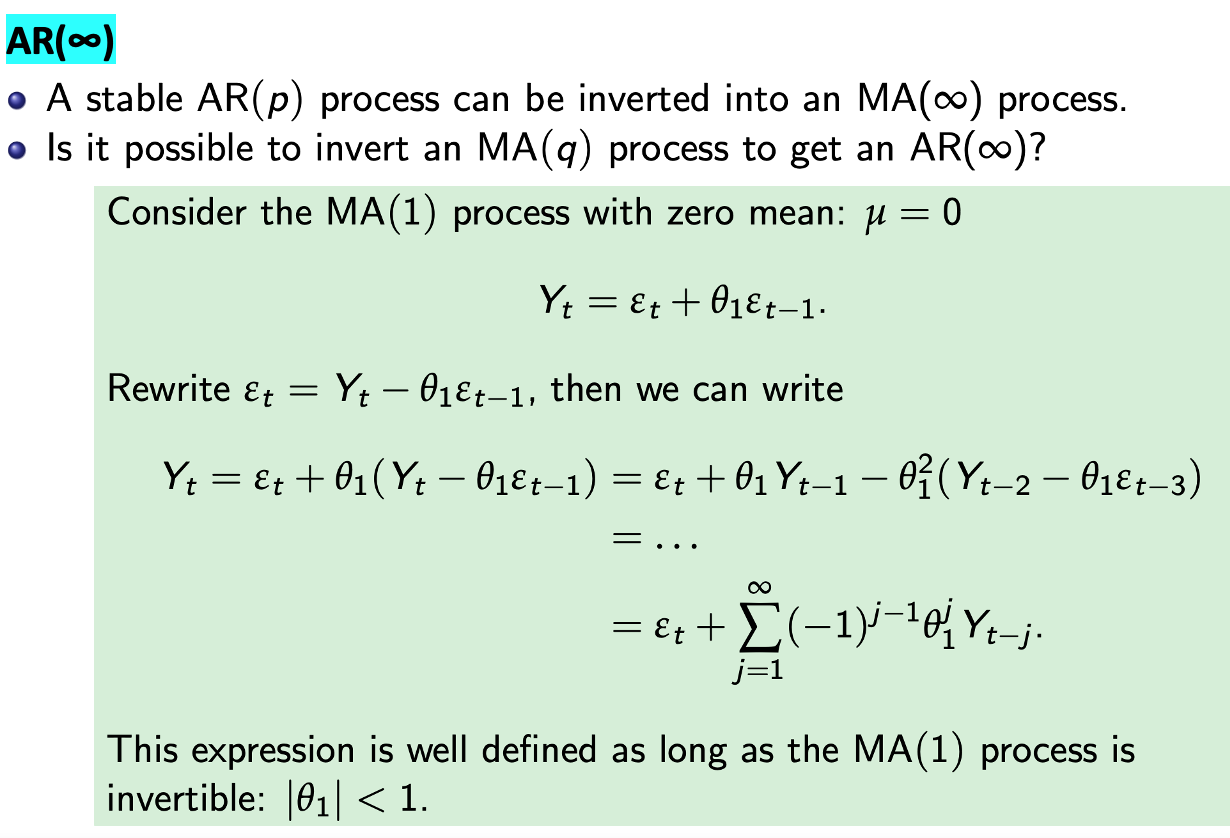

AR(∞)

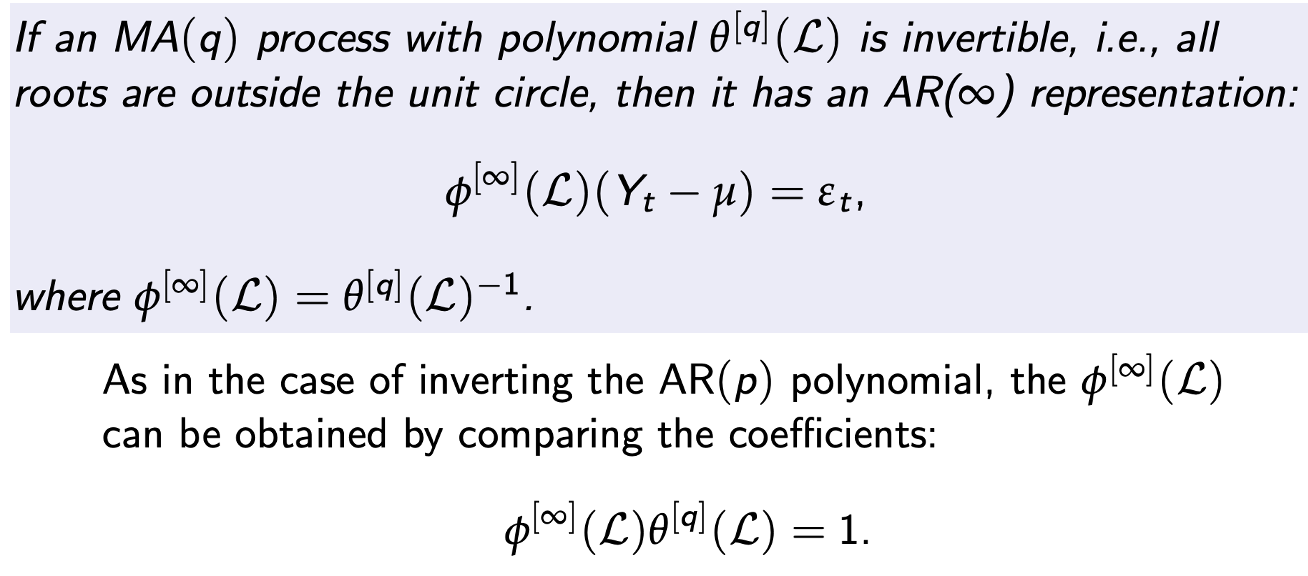

AR(∞) representation of an MA(q) process

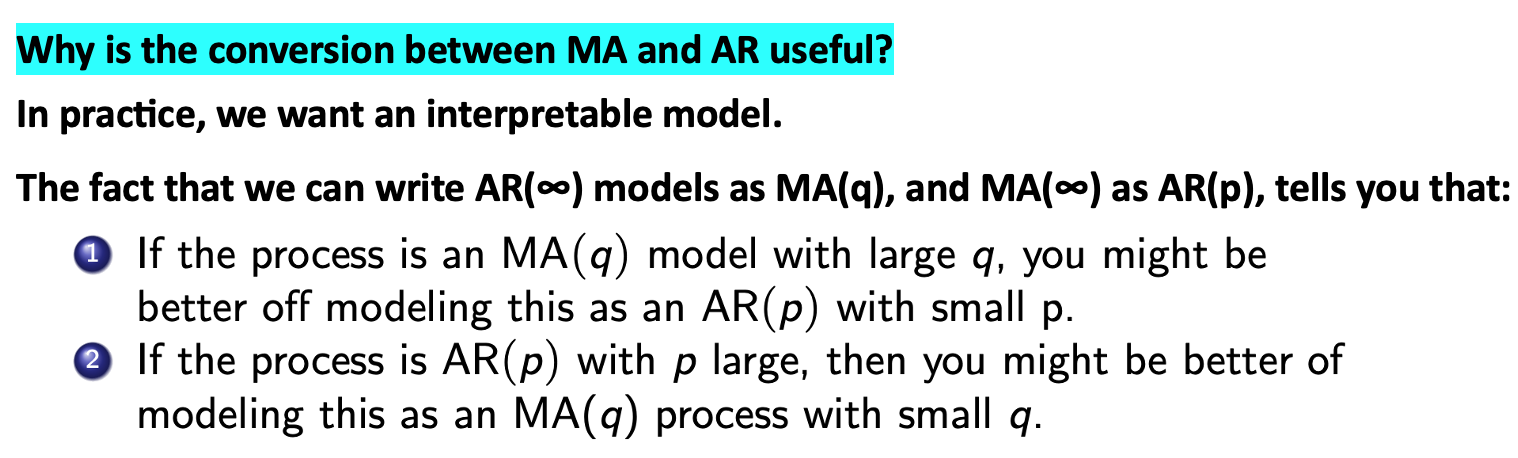

Why is the conversion between MA and AR useful?

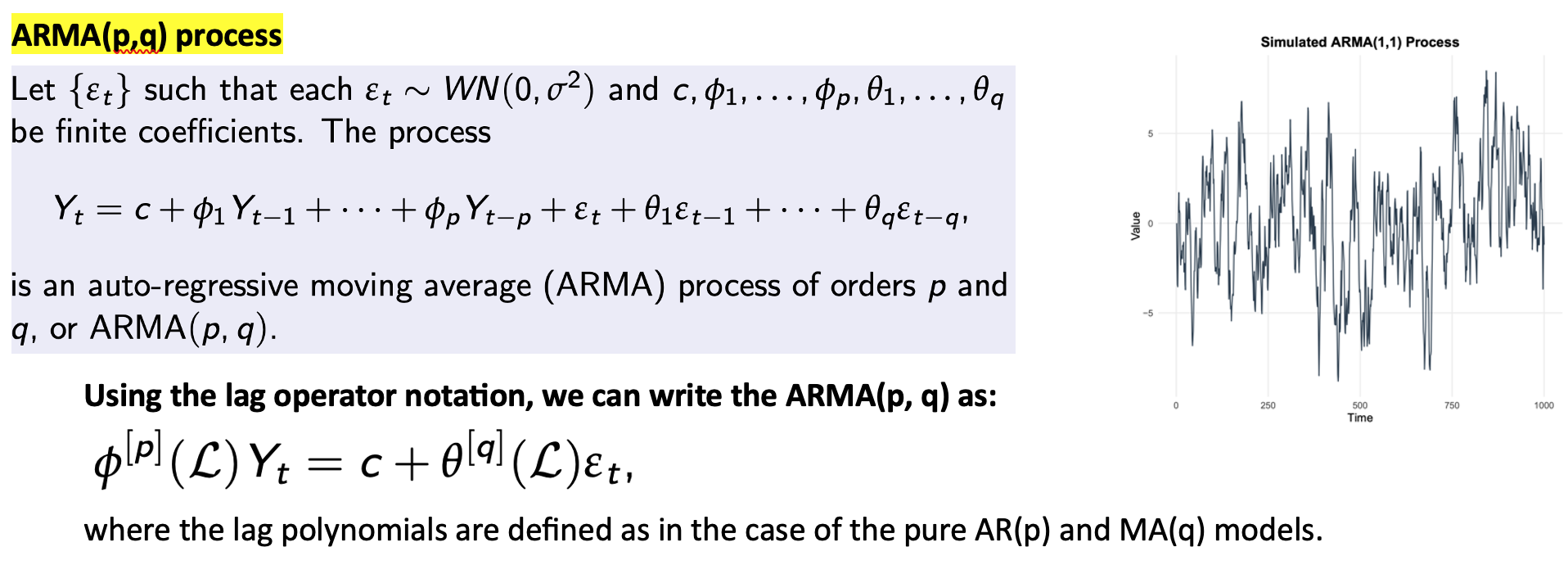

ARMA(p,q) process

ARMA(p,q) process

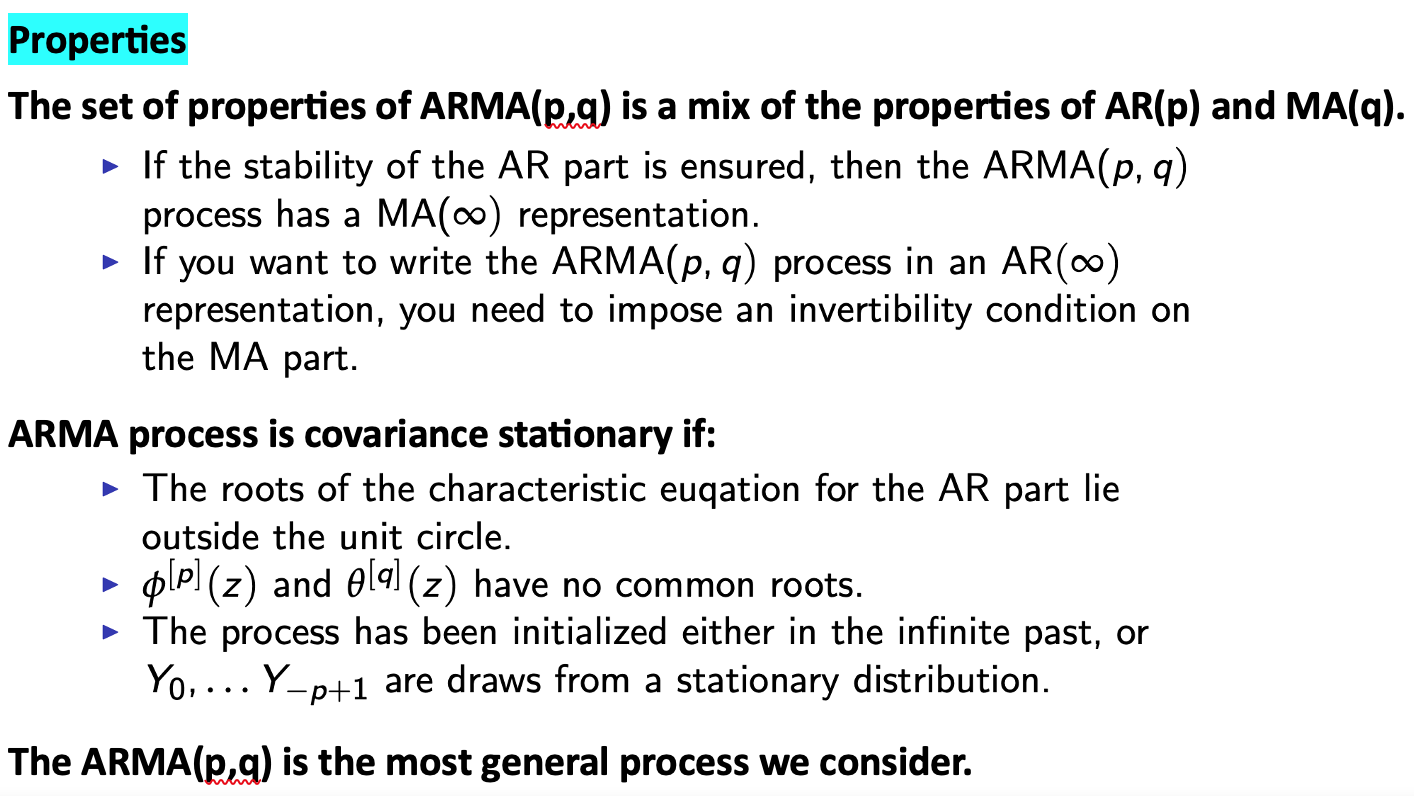

Properties

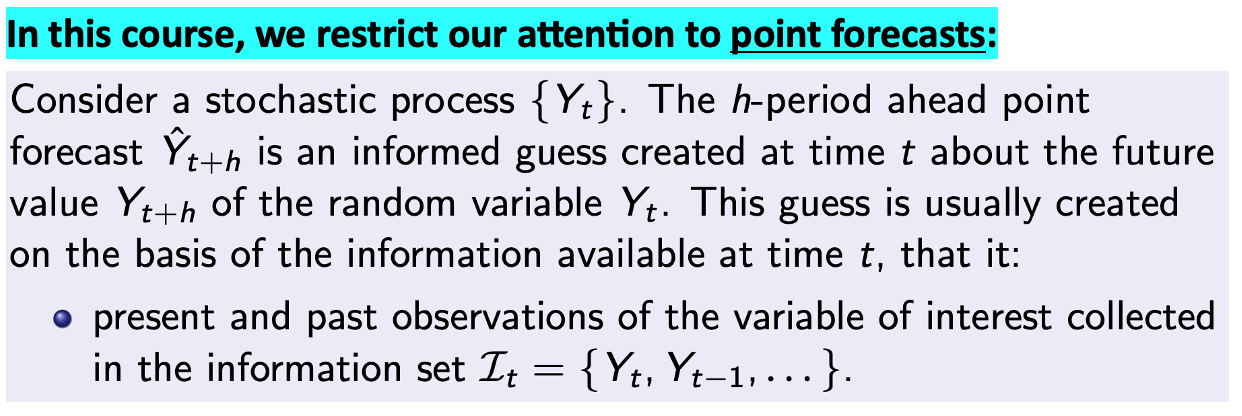

Forecasting

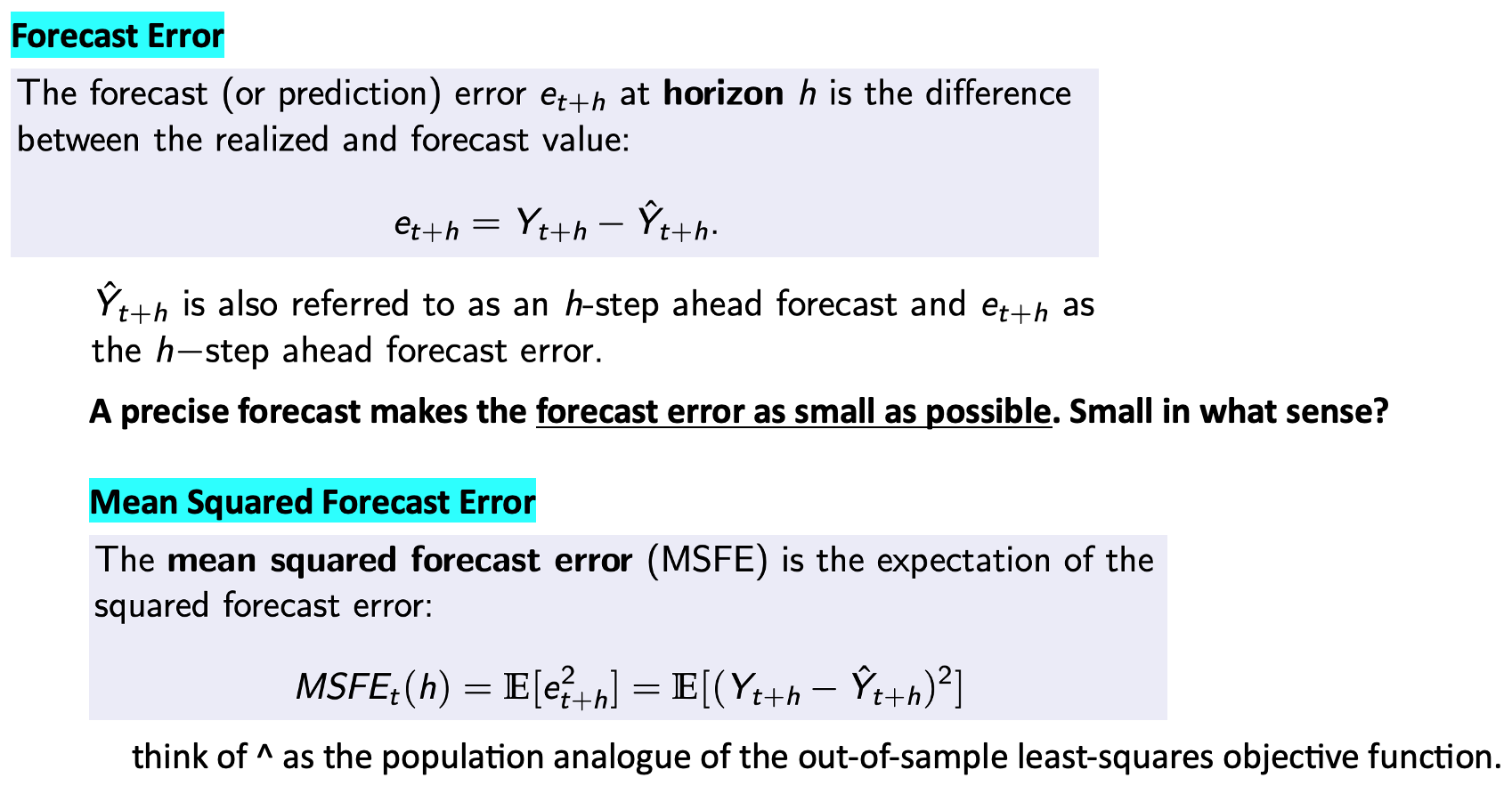

Forecast Error

Mean Squared Forecast Error

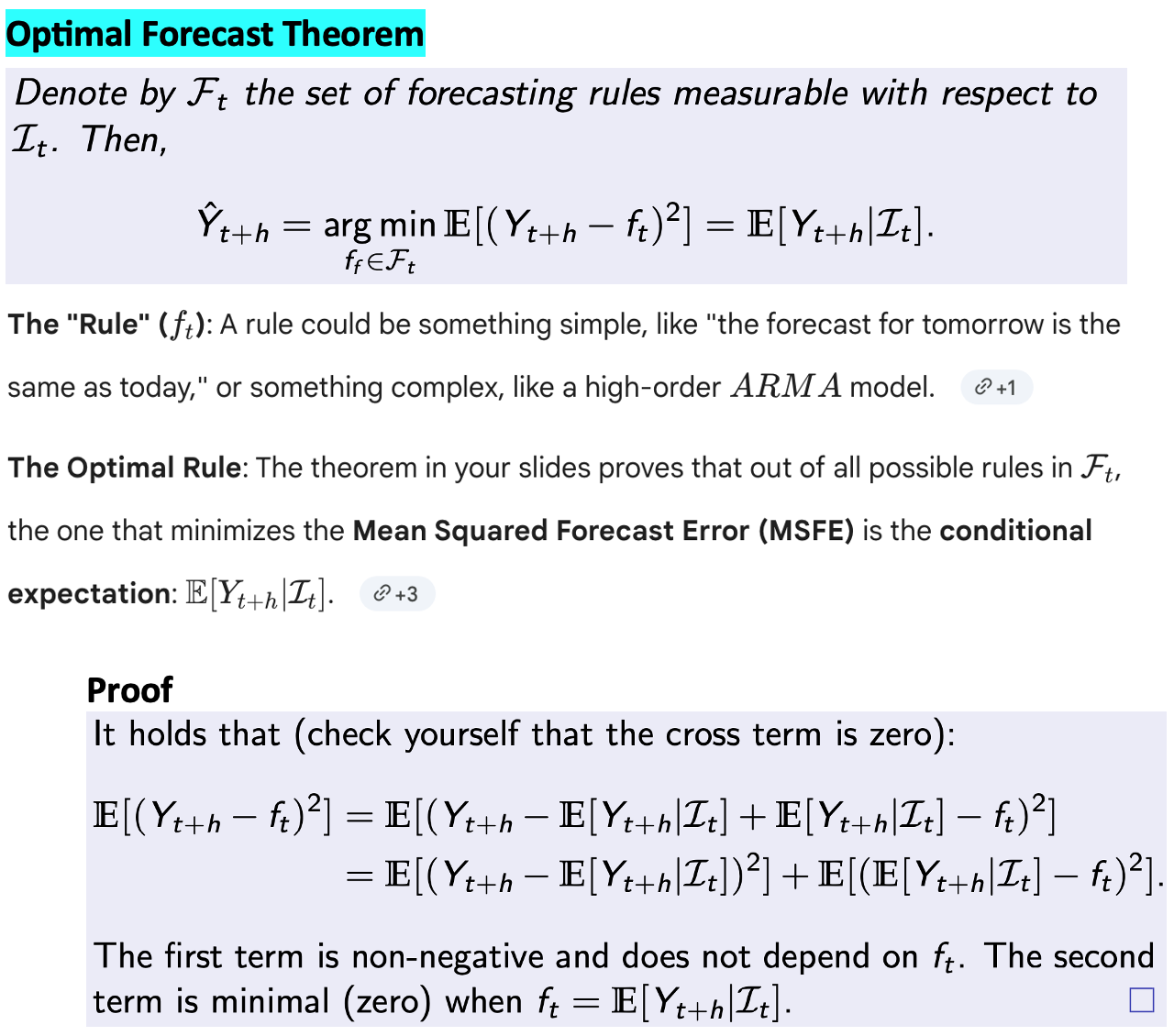

Optimal Forecast Theorem

Example

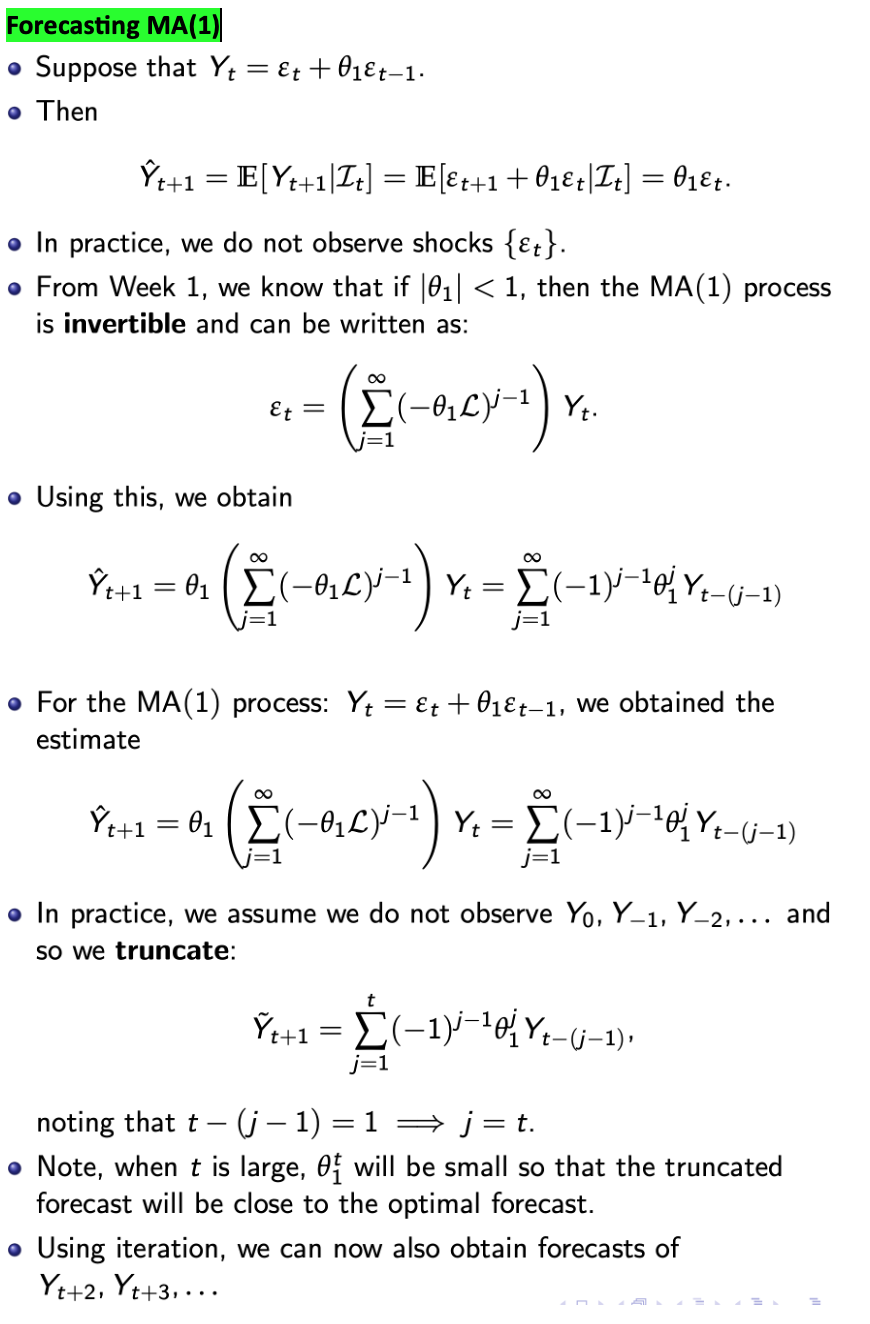

Forecasting MA(1)

Truncate?

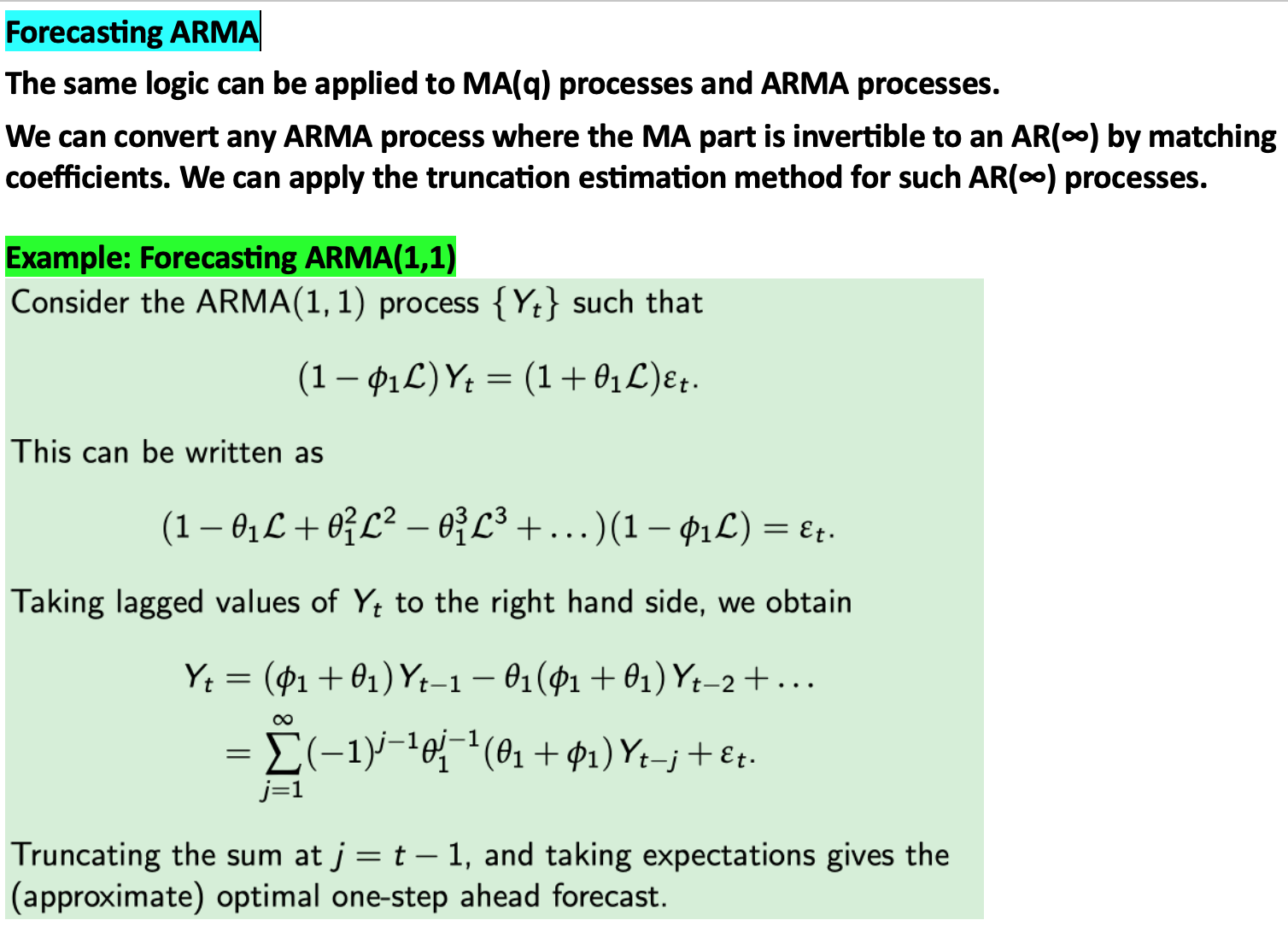

Forecasting ARMA

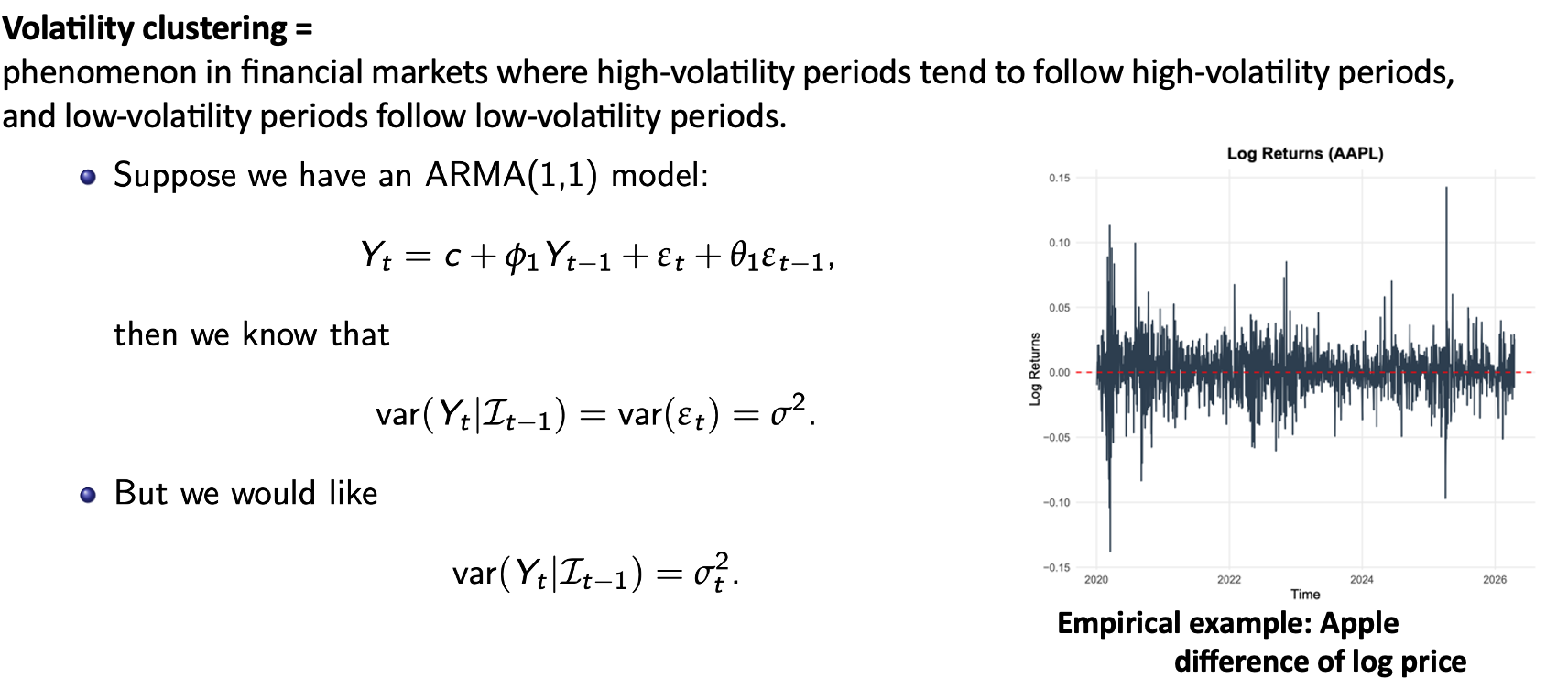

Volatility clustering

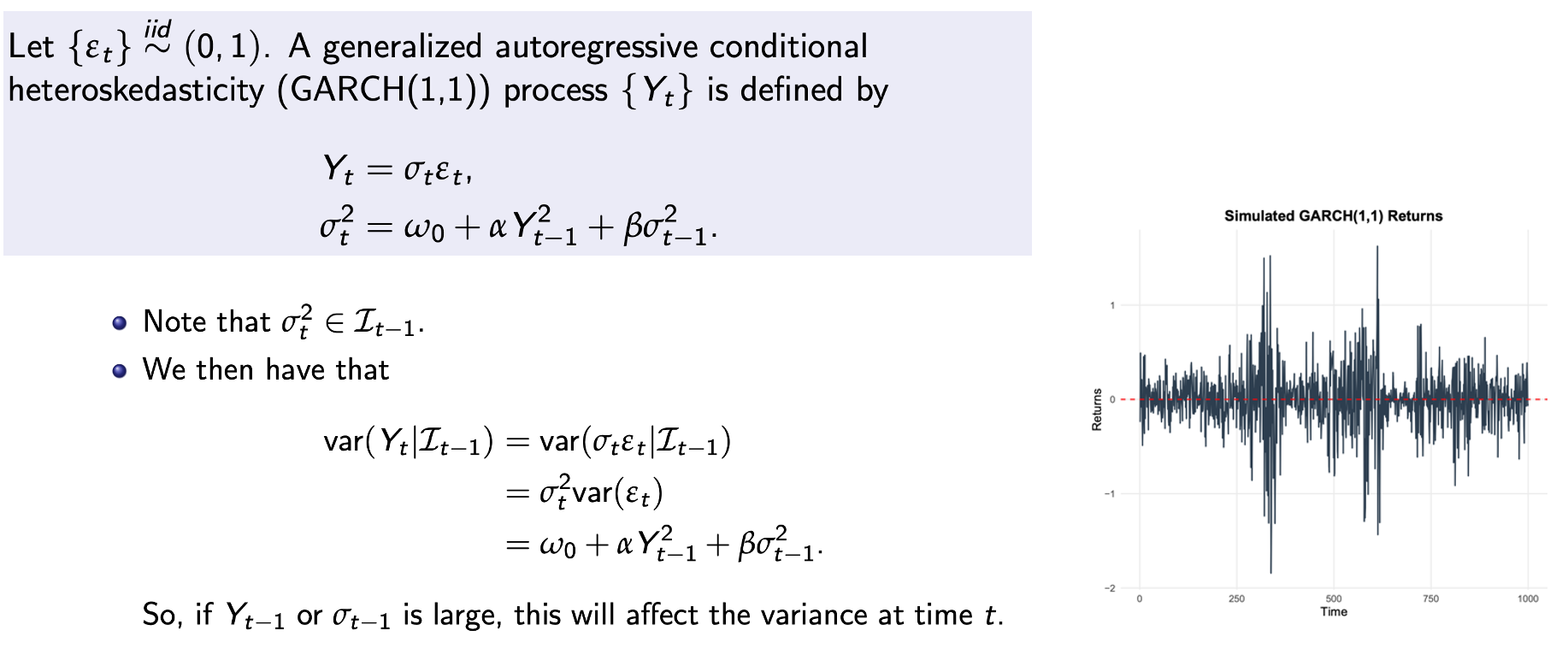

GARCH(1,1)

Intermediate Summary