YEAR 11 ATAR ECONOMICS CONCEPTS AND DEFINITIONS- SEMESTER 1 EXAM REVISION

1/96

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced |

|---|

No study sessions yet.

97 Terms

Economics

The study of how people allocated limited resources to satisfy their unlimited wants.

Three Economic Questions

What to produce? How to produce? How much to produce?

Mico Economics

Understand how consumers and producers make decisions.

Macro Economics

Concerned with the performance of the whole economy.

Positive Statements

Are objective and testable, describing facts about the world.

Normative Statements

Are opinionative and express opinions or value judgements about what should happen.

Opportunity Cost

The value on the best alternative that you give up when making a decision.

Marginal Cost

Extra production costs at one or more units of a good.

Economic Model

Simplified representation of economic reality. Have assumptions and are simplified representations.

PPF: Production Possibility Frontier

Shows the services/goods produced by an economy given the availability of resources and level of technology.

Outward shift

Caused by increase in the factors of production.

Economic Growth

Expansion of an economy's productive potential, the economy can produce more of goods and services across all sectors.

Technological Advancments

Makes it possible to produce more goods with the same factors of production.

Inward Shift

Decreased factors of production.

Market Economy

Type of economic system where price system or systems allocate recourses.

Consumer Goods

Goods that have no future productive use.

Capital Goods

Any good that may be used to help increase future production.

Consumer Sovereignty

Consumers hold the power to influence production decisions based on what goods or services they purchase.

What to produce? (Question)

There is consumer sovereignty, consumers can decide what goods and services will be produced.

How much? (Question)

Level of consumer demand dictates how much of each product should be produced.

How to produce? (Question)

The profit motive of sellers encourages them to produce goods and services as efficiently as possible.

Buyers

Who create market demand.

Sellers

Who create market supply.

Commodity

Something that is being bought or sold.

Voluntary Exchange

People can chose weather or not to participate.

Process

Mechanism or arrangement through which buyers and sellers "meet."

Price

Set by market demand and supply.

Product Markets

Deal with buying and selling of goods and services.

Factor Markets

Deal in buying and selling of factors of production and resources.

Competitive Markets

Large number of buyers and sellers, firm are price takers, very similar (homogenous) products, easy entry into the market (no barriers of entry.)

Non Competitive Markets

Small number of firms, product differentiation, firms are price setters- they have market power, entry into the market is restricted.

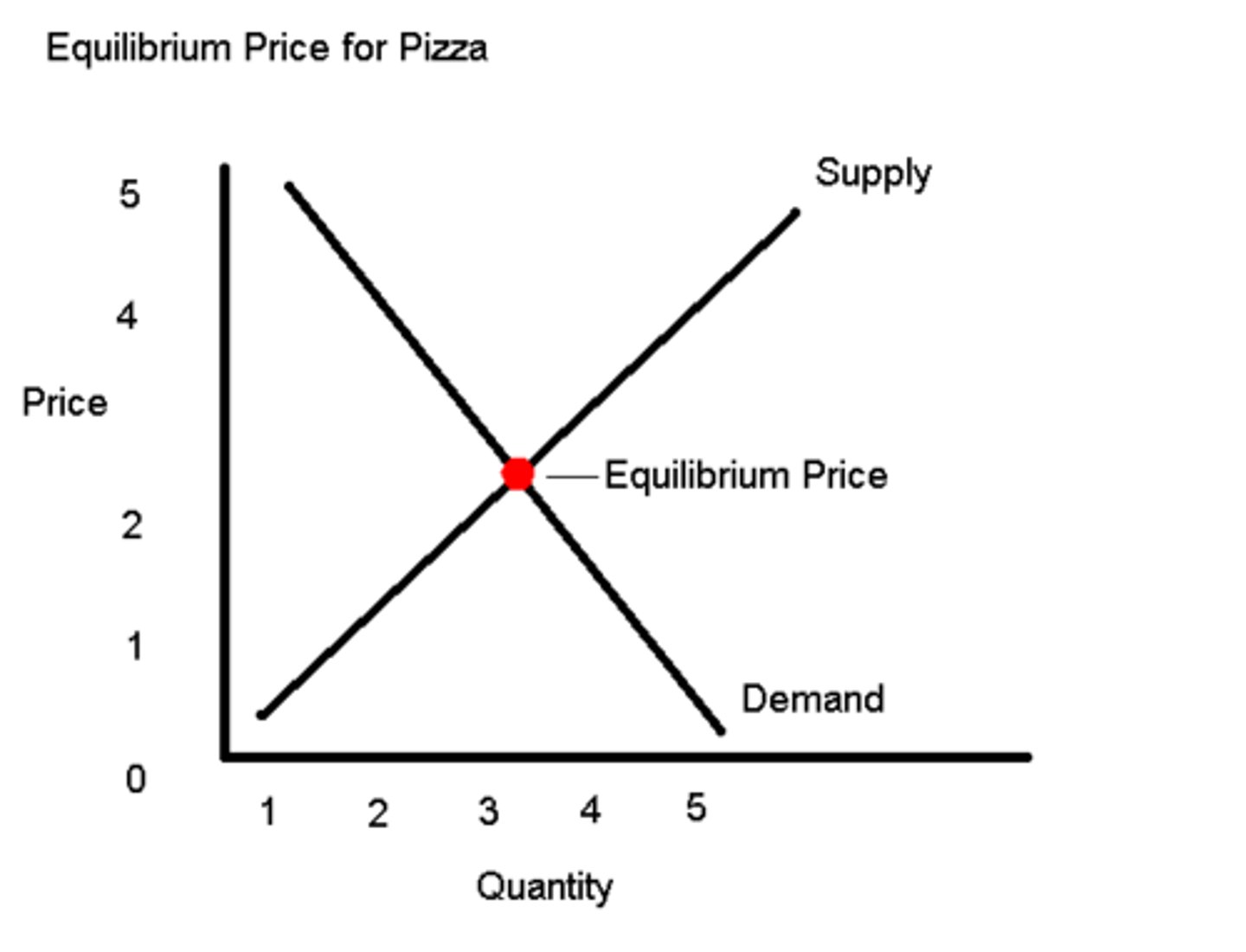

Demand

The quantity of a good or service that consumers are willing and able to buy of a particular price and a particular point of time.

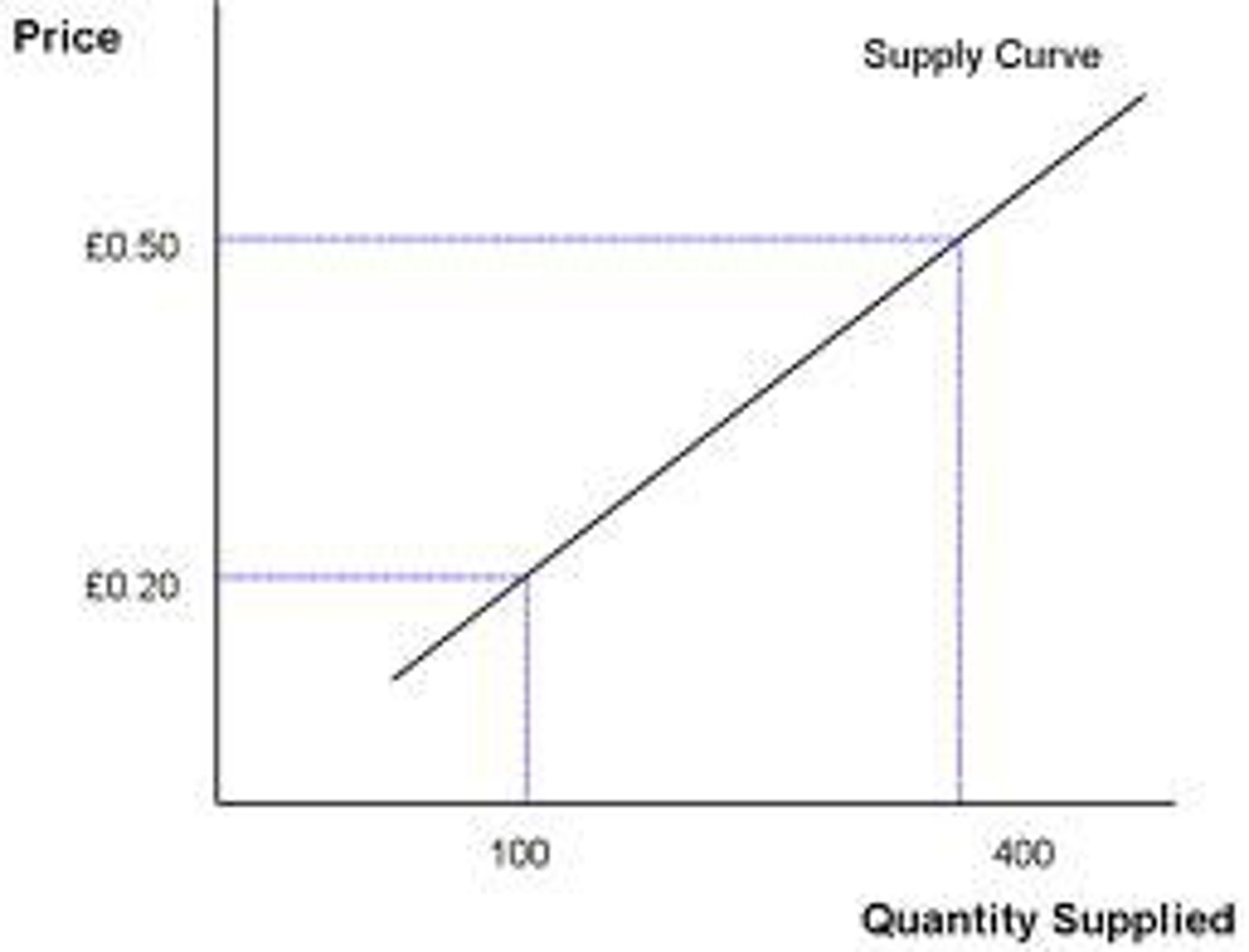

Law of Supply

Increase in the price of goods or services results in an increase producers supply. Positive Relationship.

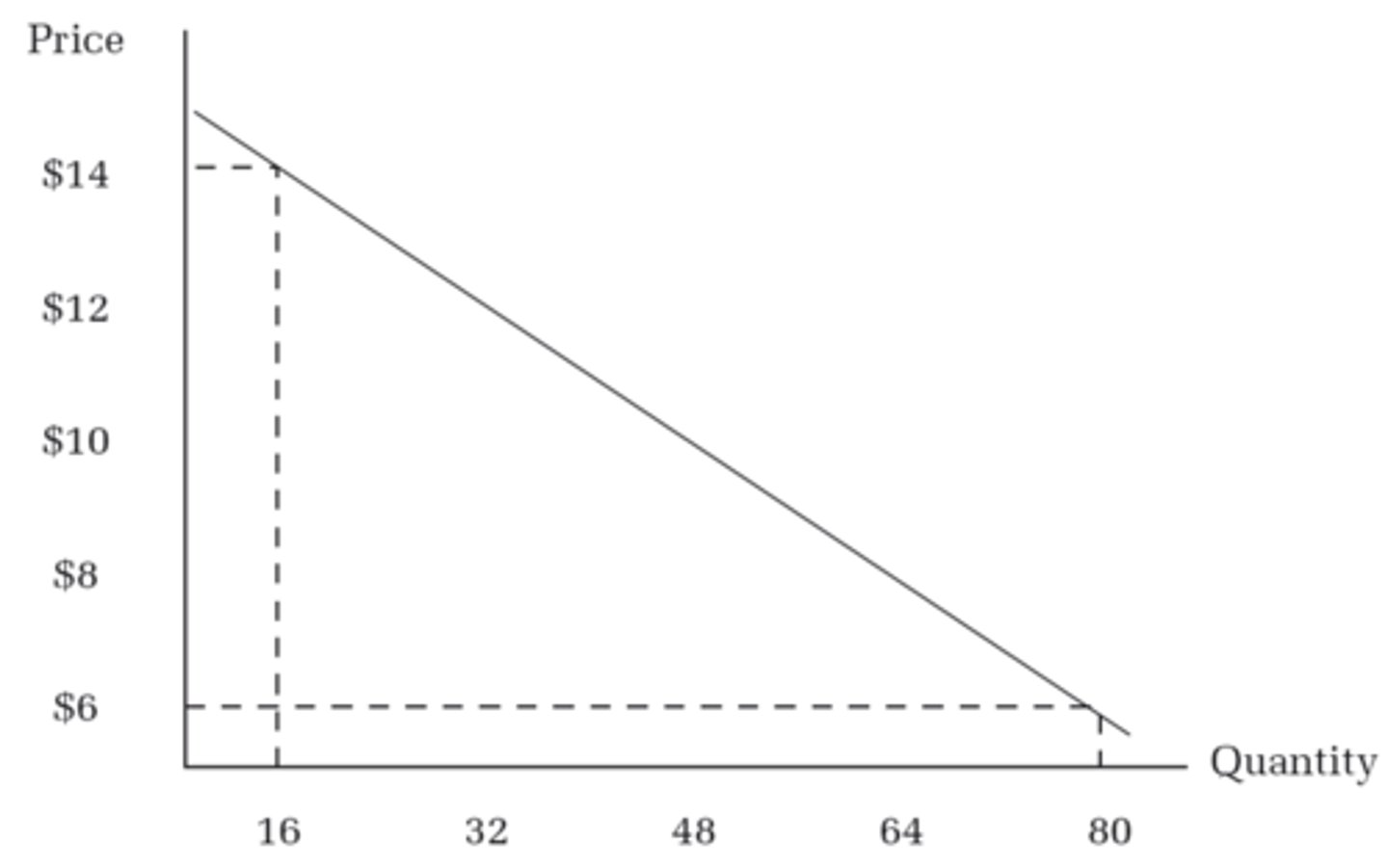

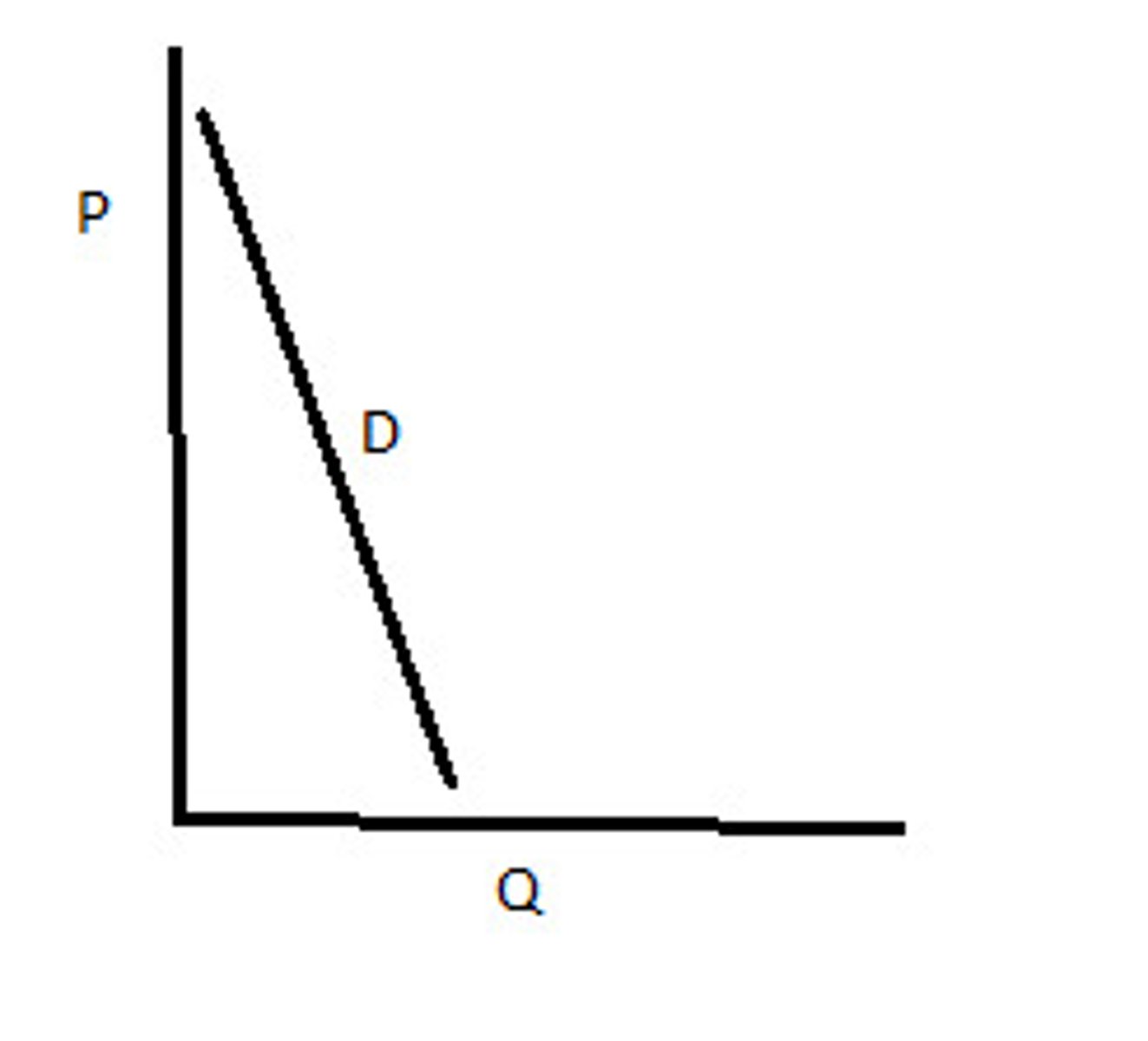

Law of Demand

When the price of a product goes up, the quantity demanded will go down. Inverse relationship.

The Income Effect

When the price of a good rises consumers are not willing to buy as much of the good as their real income or purchasing power has decreased,

The Substitution Effect.

When the price of one good rises other goods become more attractive.

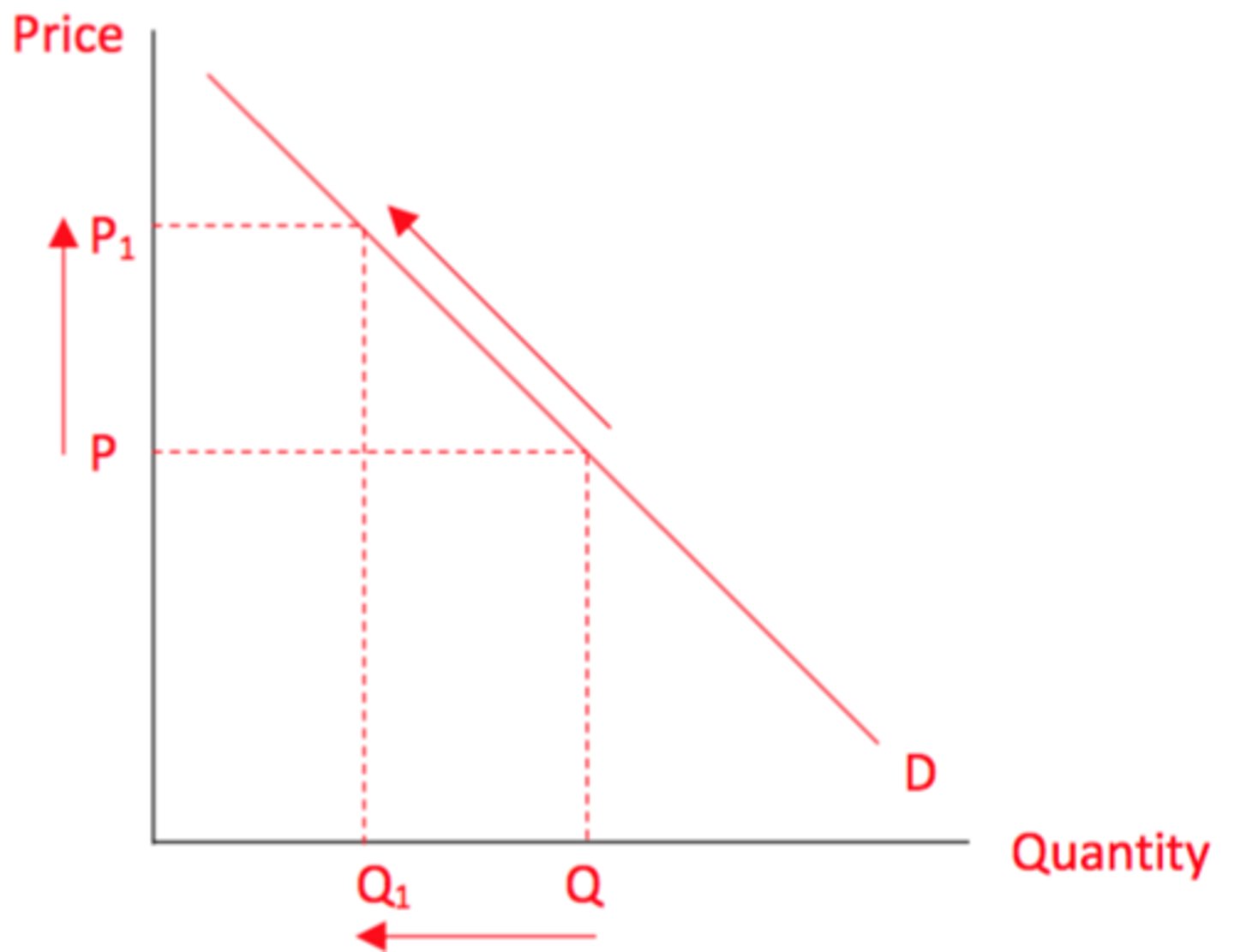

Contraction In Demand

Equals an increase in price, a rising movement along the demand curve.

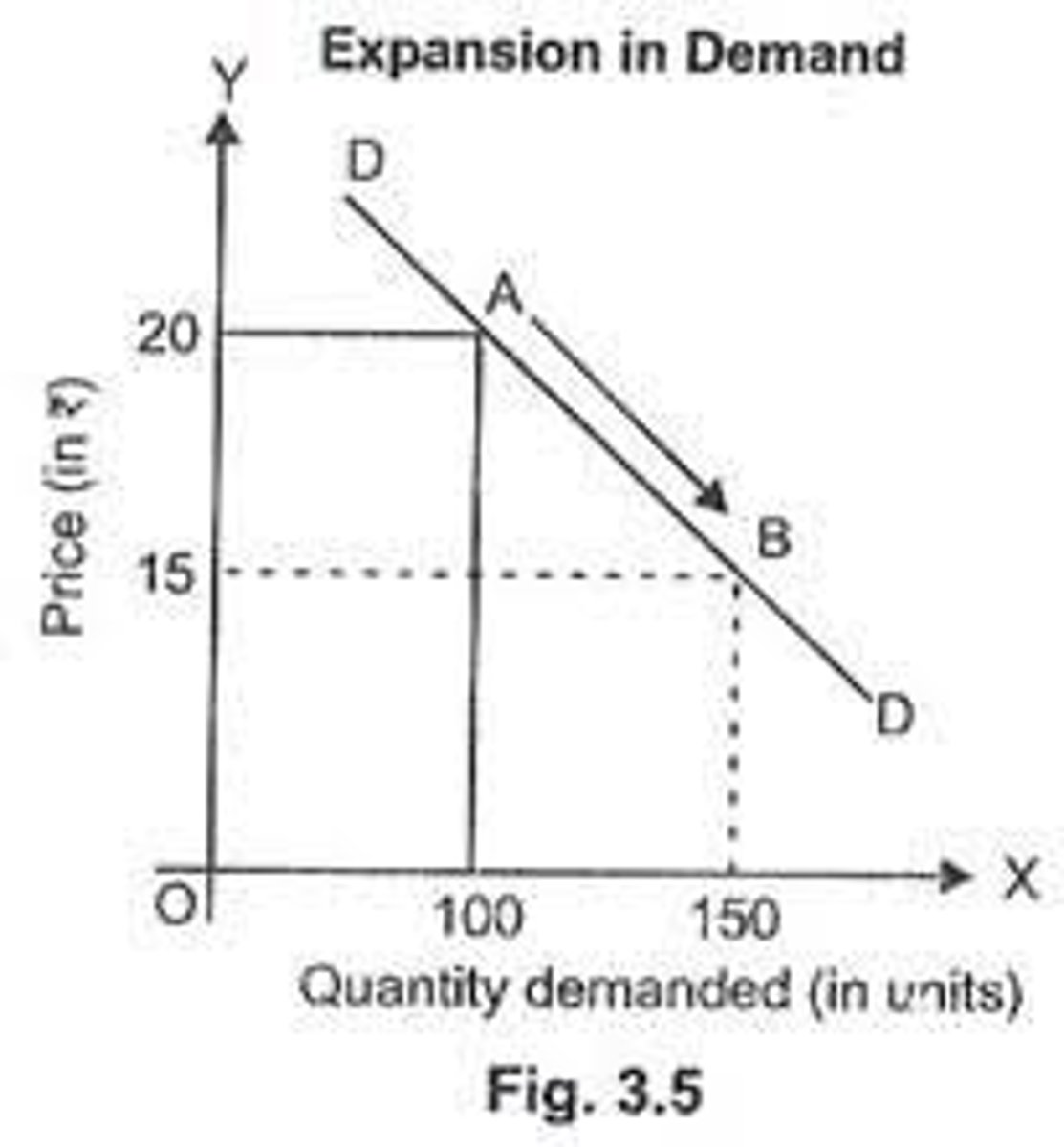

Expansion In Demand

Equals to a decrease in price, a downwards movement along the demand curve.

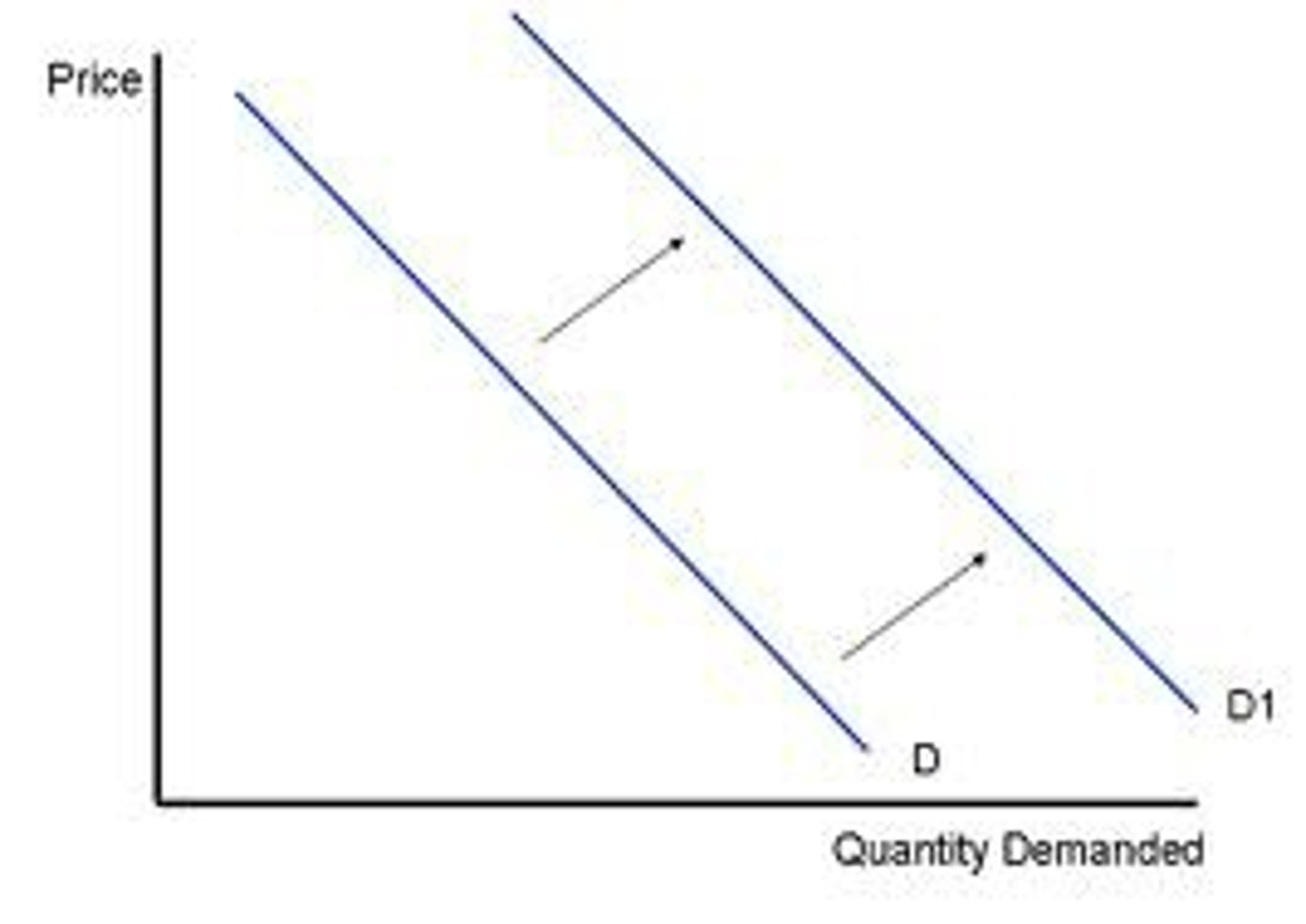

Increase In Demand

A shift to the right is an increase in demand.

Decrease In Demand

A shift to the left is an decrease in demand.

Causes of Shift in the Demand Curve

Levels of disposable, Price of related/substitutional goods, Tastes and preferences, Expectations of consumers, Demographic Factors.

Complementary Goods

Products that align in conjunction with one another e.g. Butter and Toast.

Normal Good

Demand is increased as income rises

Interior Good

Good where demand decreases as income increases.

Supply

The quantity of goods and services producers are willing and able to sell at a particular point in time.

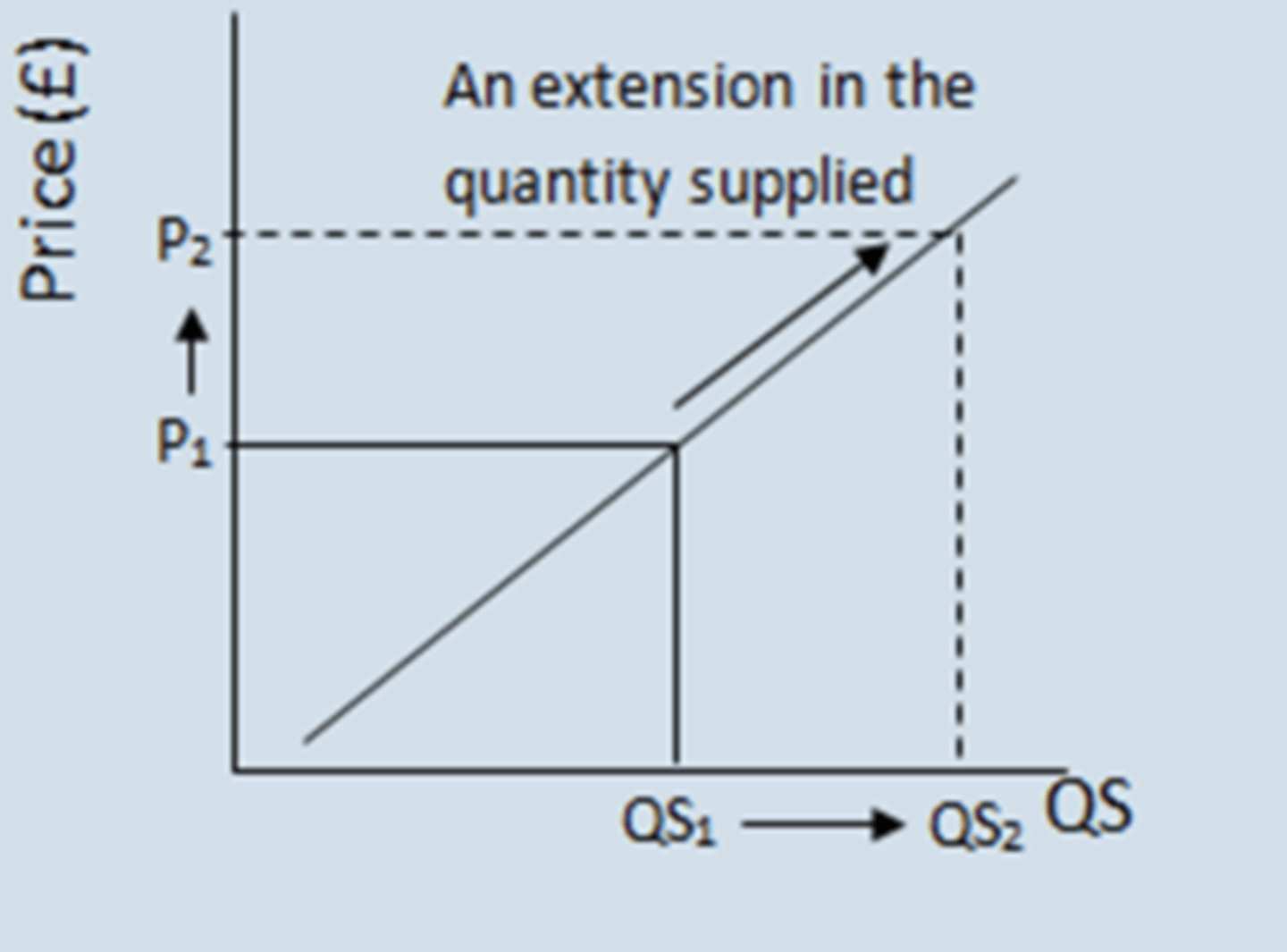

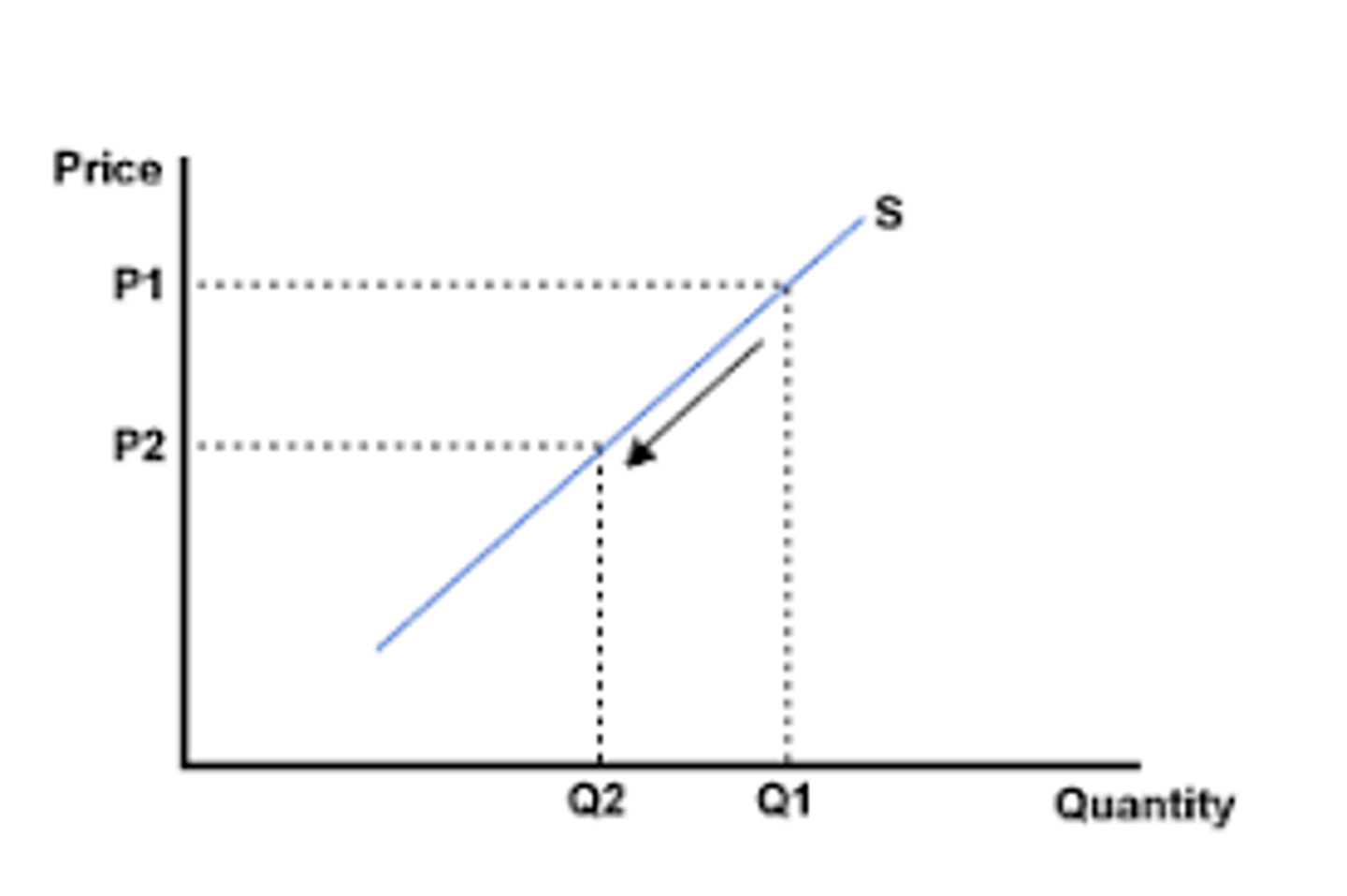

Expansion in Supply

As price rises, amount supplied rises. Directly relative with quantity.

Contraction in Supply

As price decreases, amount supplied decreases. Directly relative with quantity.

Costs of Production

Expected future prices, Number of suppliers, Technology, Events affecting the availability of resources and the supply chain.

Substitutes for Production

If the price of productive substitutes increases then the supply of goods your producing decreases.

Supply Curve

Linear line that directly represents the relationship between quantity supplied and prices.

Demand Curve

Linear line that reflects the relationship between the prices of goods and services and the quantity demanded.

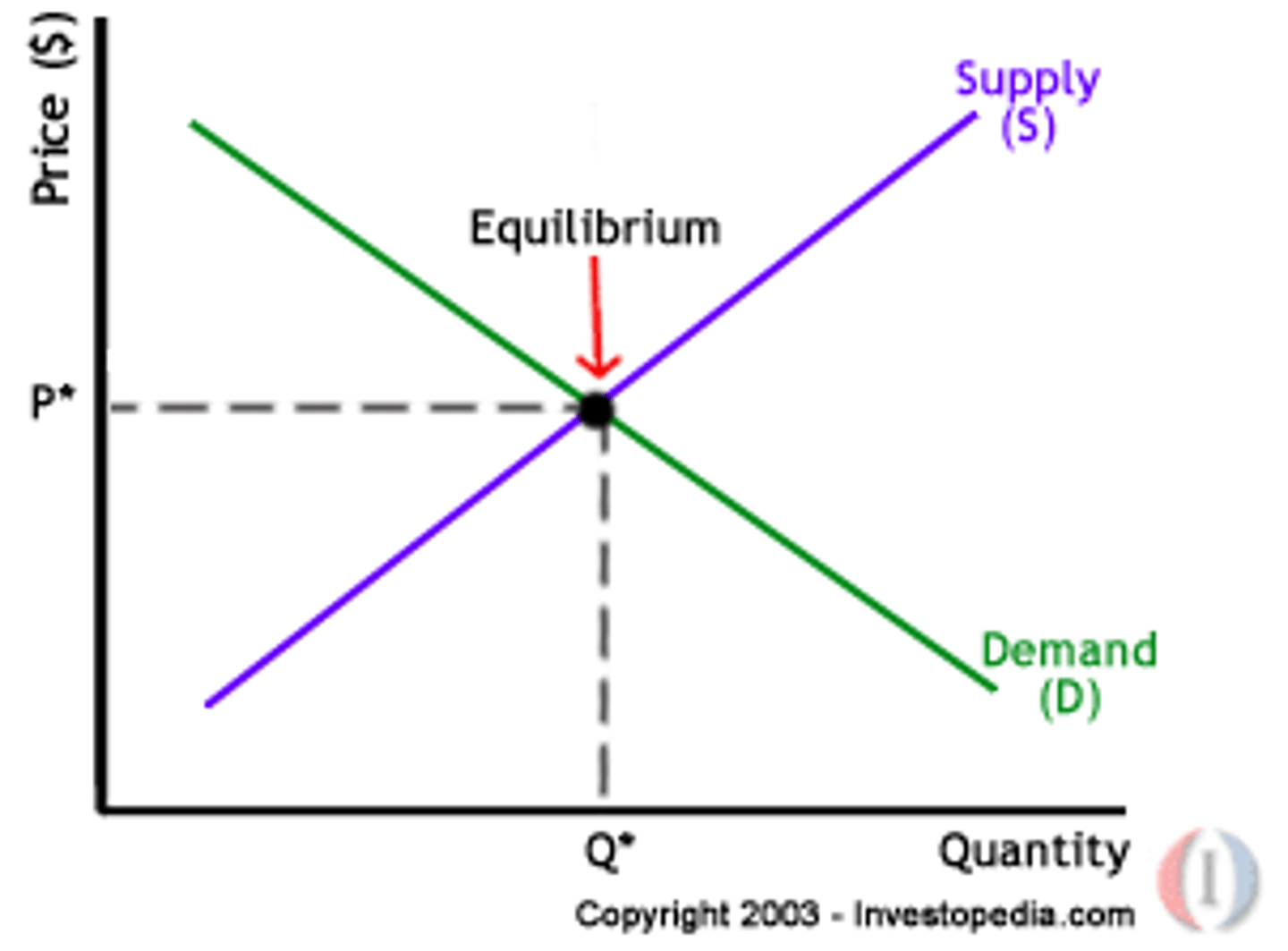

Equilibrium Price

Where the quantity of goods supplied meets the quantity of goods demanded at an intersection.

Equilibrium Quantity

When there is no shortage or surplus of a product in the market. Met at the same intersect as Equilibrium Price.

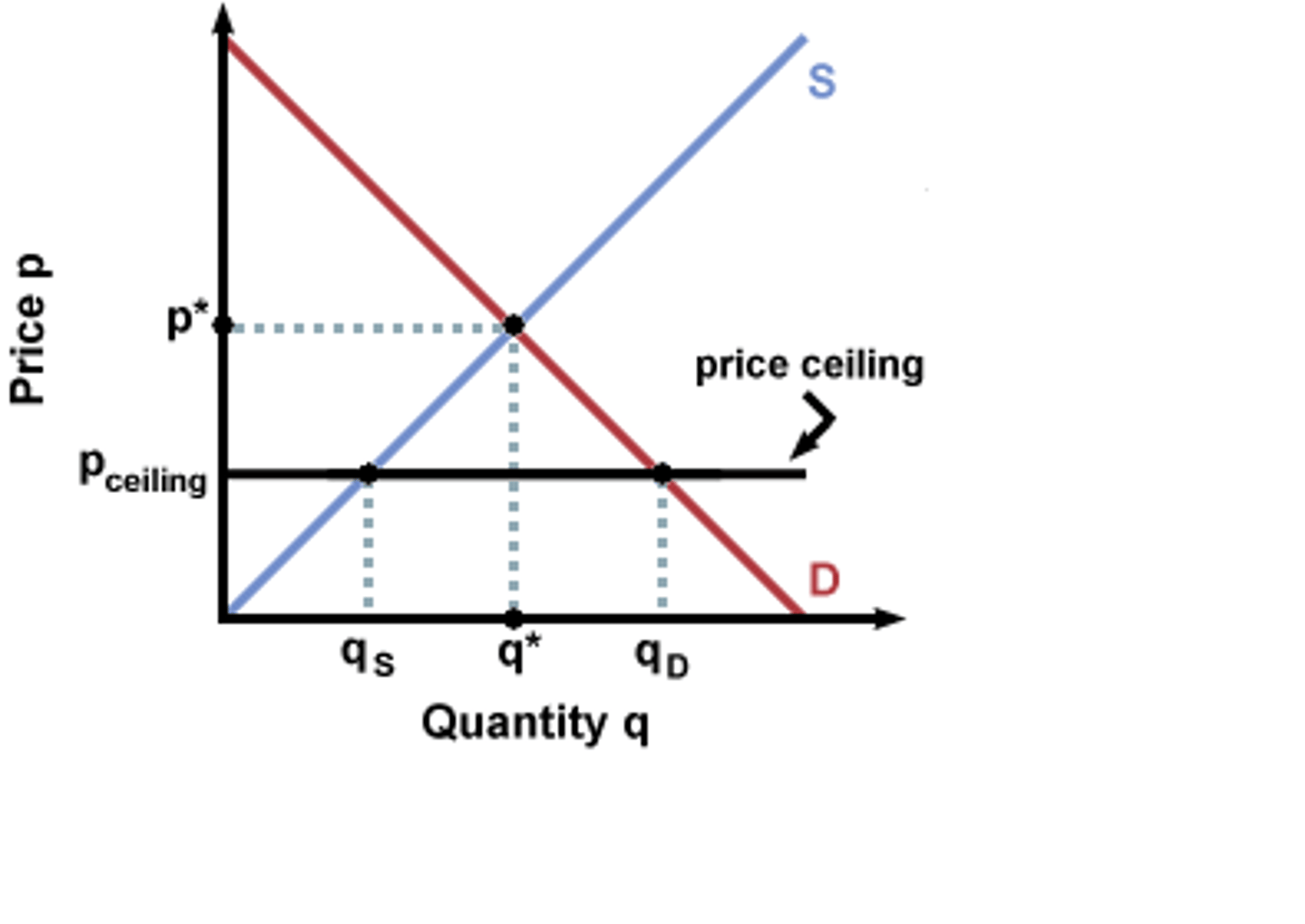

Shortage

When the demand outweighs the supply.

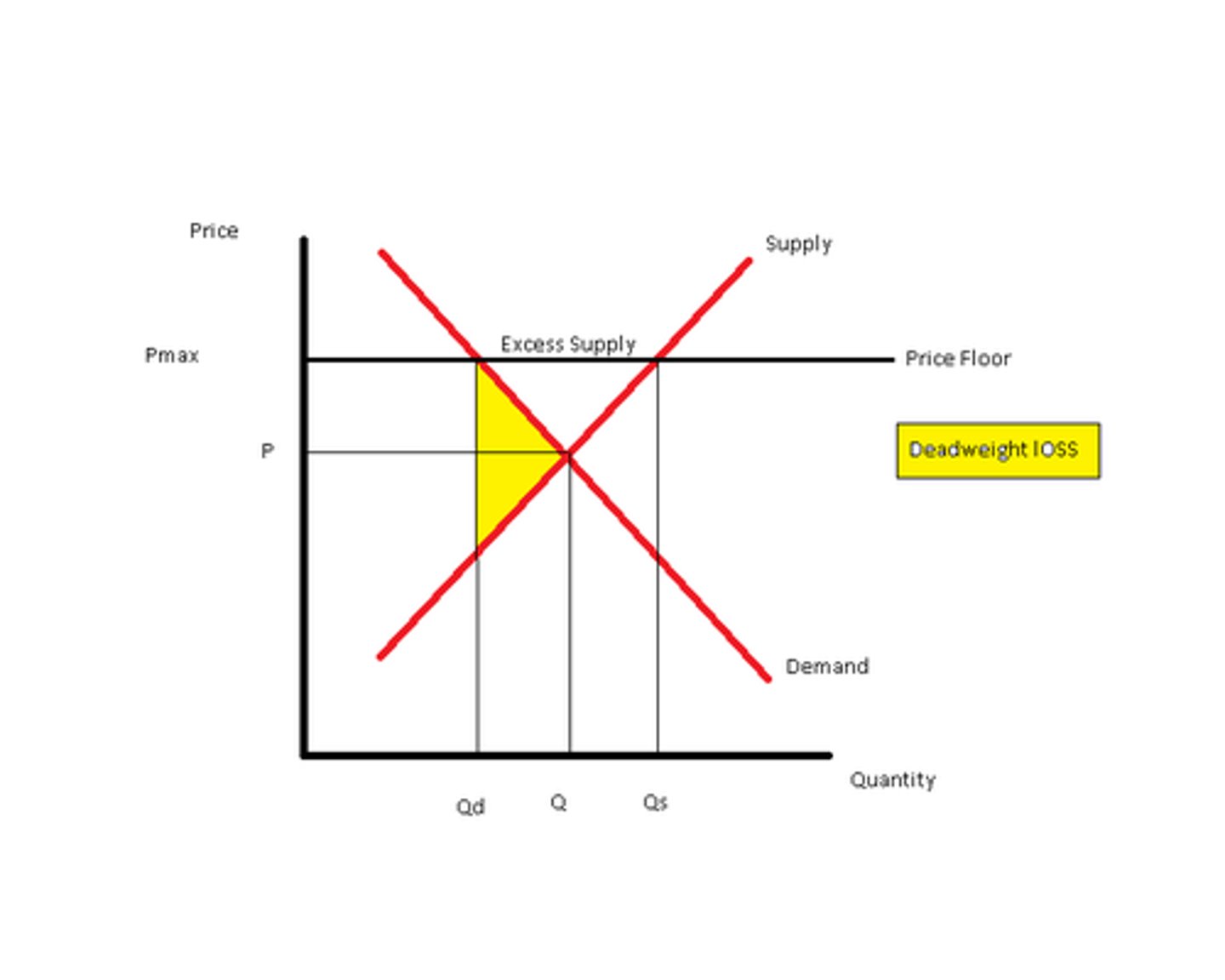

Surplus

When the supply outweighs the demand.

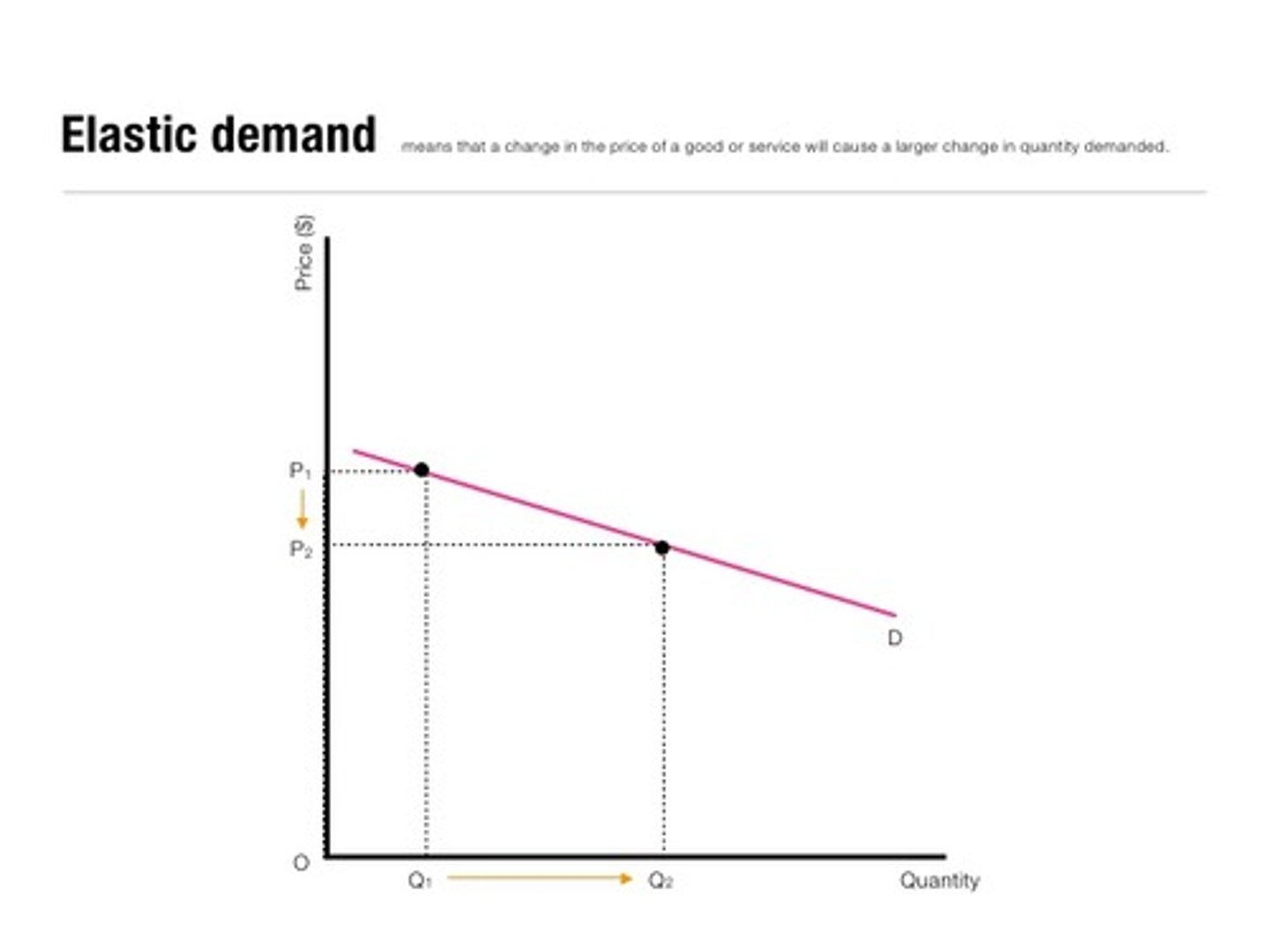

Price Elasticity of Demand

Responsiveness of the quantity demanded to a change in the price of a good or service.

Elastic Demand

Demanded is said to be elastic when a change in price leads to a larger than proportional change in quantity demanded.

Elastic Demand Curve

Smaller change in price leading to a larger change in quantity demanded.

Inelastic Demand Curve

Demand is said to be ________when a change in price leads to a smaller than proportional change in quantity demanded.

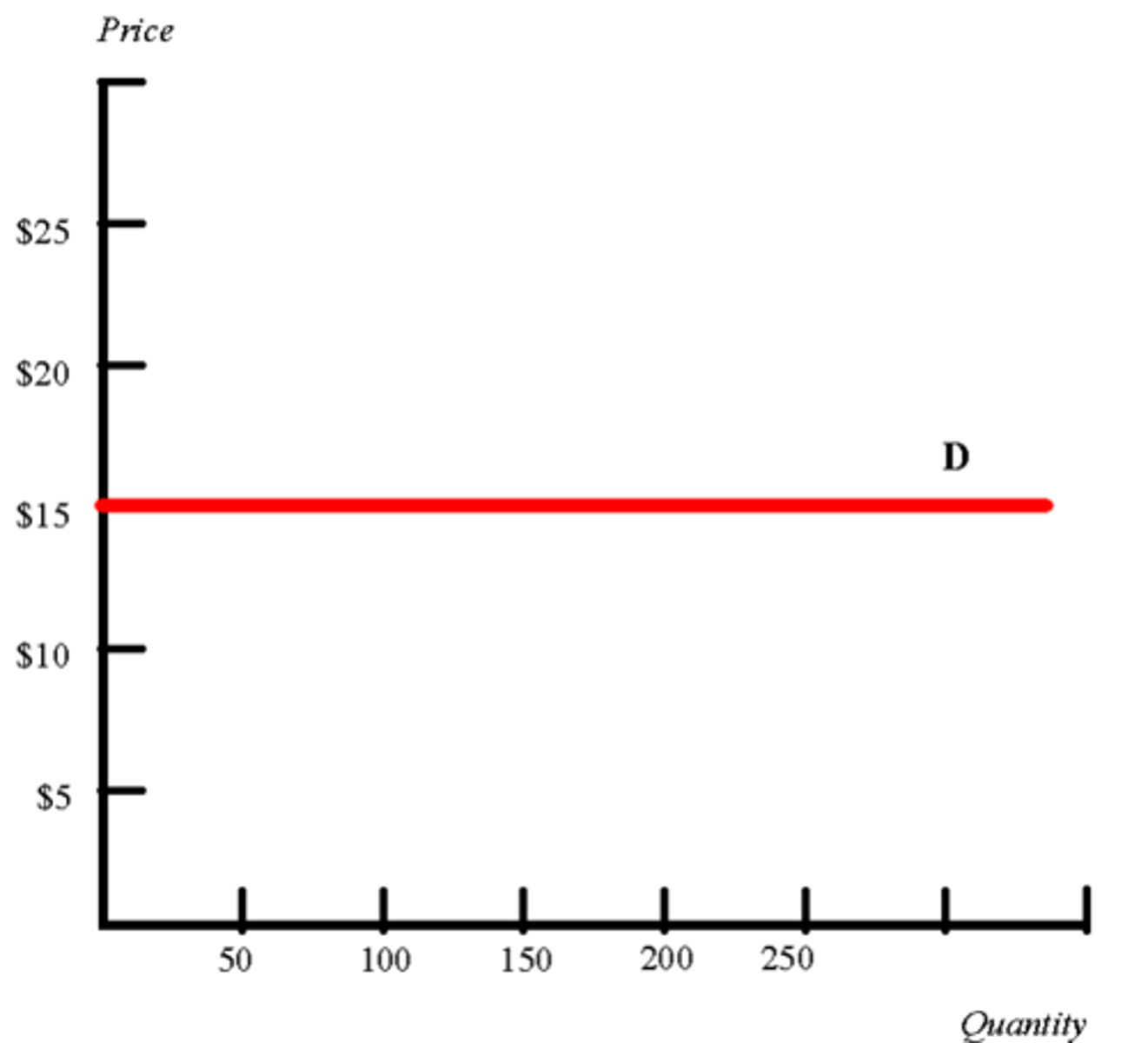

Perfect Elasticity

Any change in price leads to all changes in consumption.

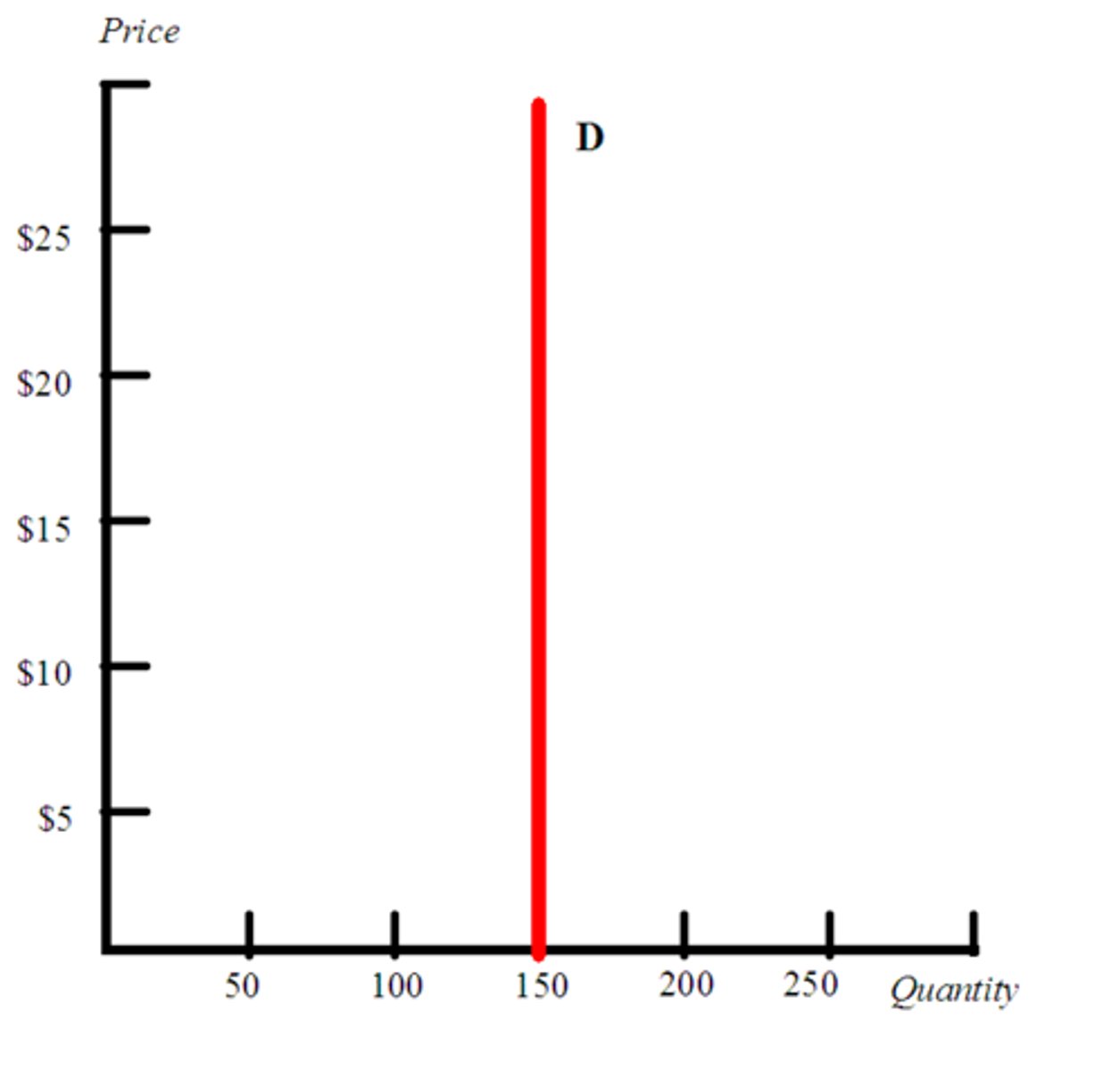

Perfect Inelasticity

Any change in price leads to no change in quantity.

Factors Affecting Price Elasticity of Demand

Availability of substitutes, weather a good is a necessity or a luxury, proportion of income spent, time, definition of market.

Total Revenue Method

Total revenue = price x quantity

Elasticity Coefficient- Point Method

% change in quantity / % change in price = Elasticity Demand Coefficient

Elasticity of Supply

Price elasticity of measures the responsiveness of quantity supplied to a change in price.

Price Discrimination

Refers to firms adjusting their pricing to different consumer groups to boost their total revenue. Firms base their pricing on the different prices elasticity of demand of each consumer groups.

Market Efficiency

A competitive market results from thousands of buyers abd sellers with one another. Producing the goods that society wants at the lowest possible costs.

Marginal Benefit

Additional benefits a consumer gets from each additional good.

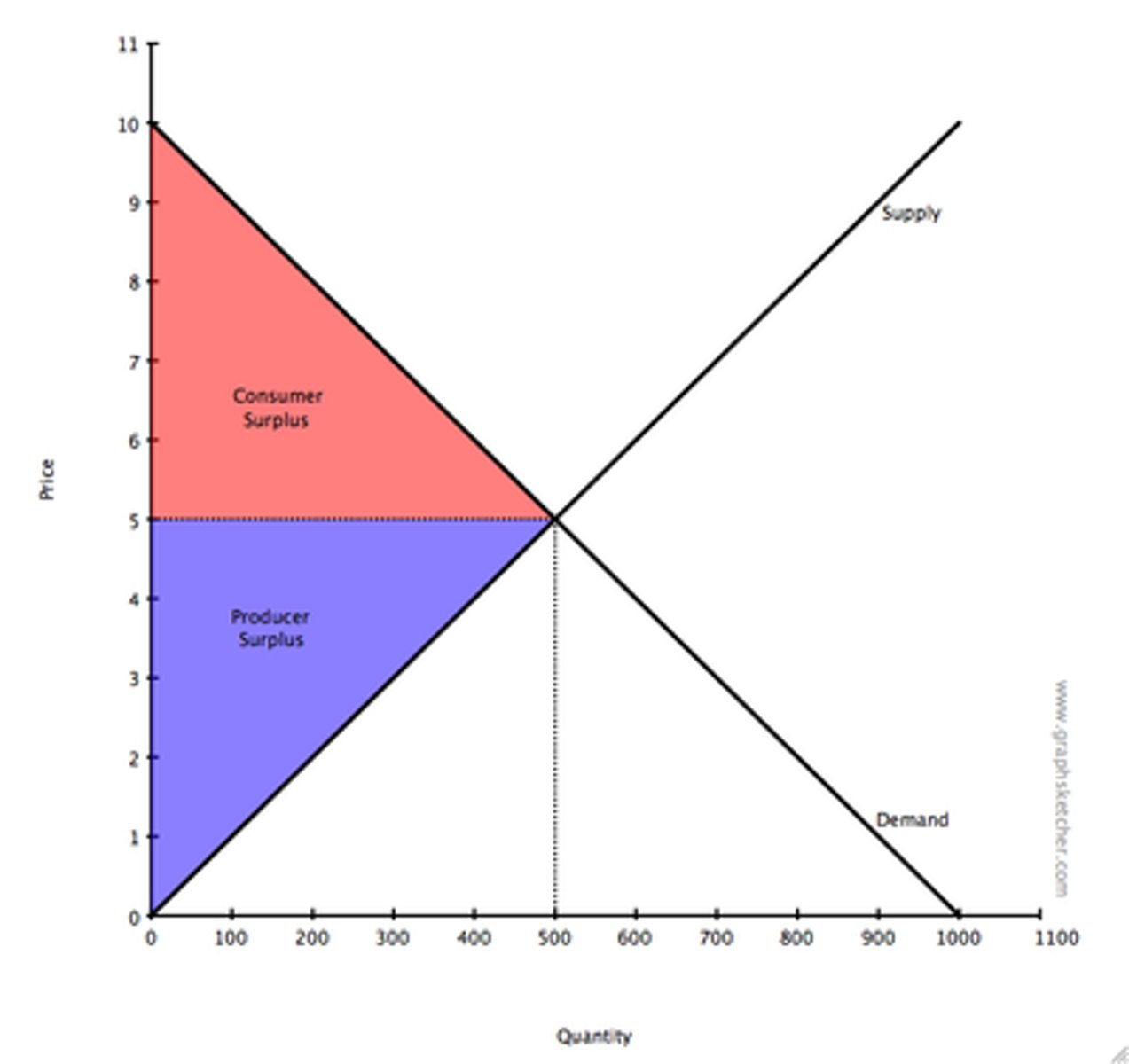

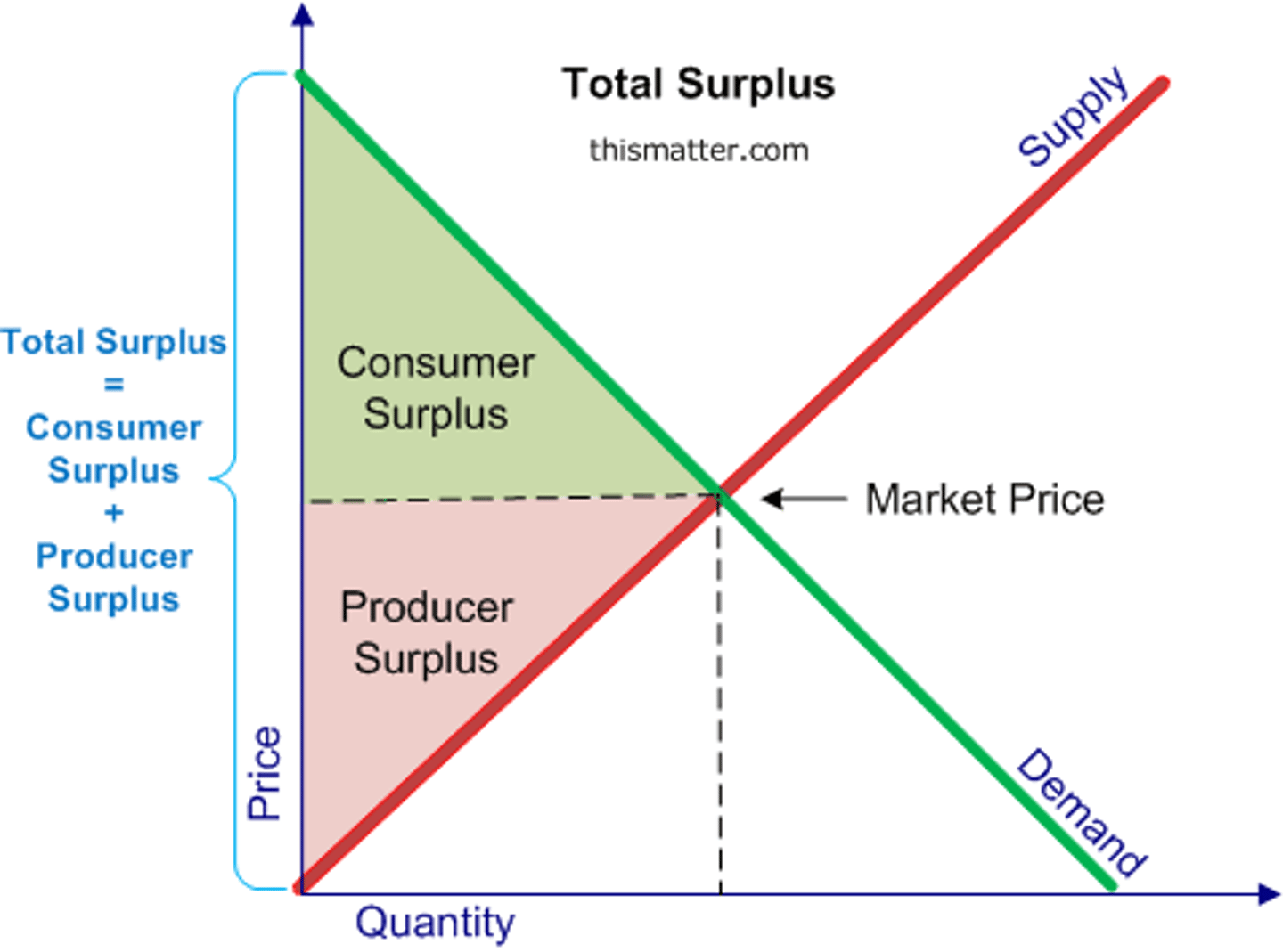

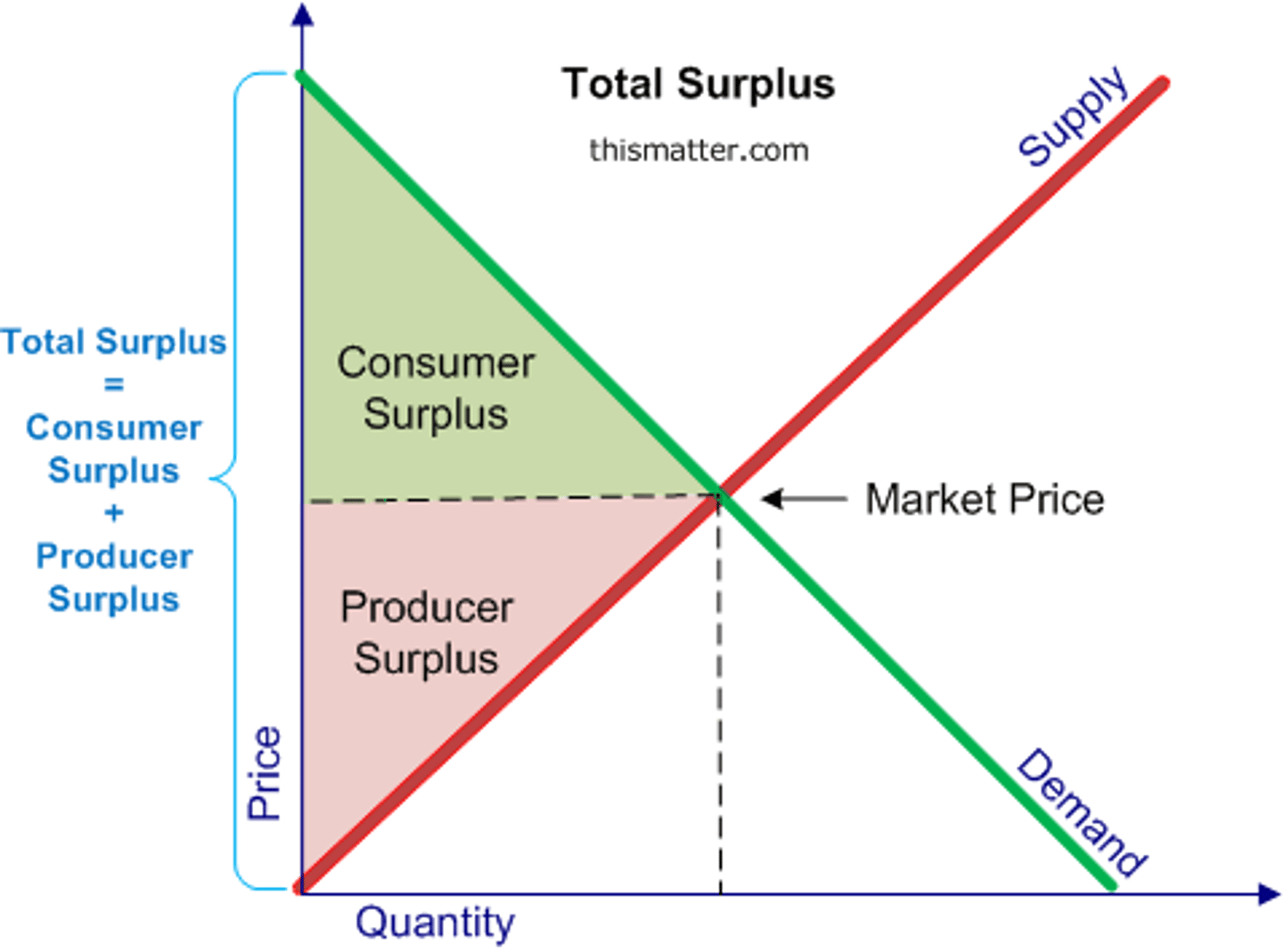

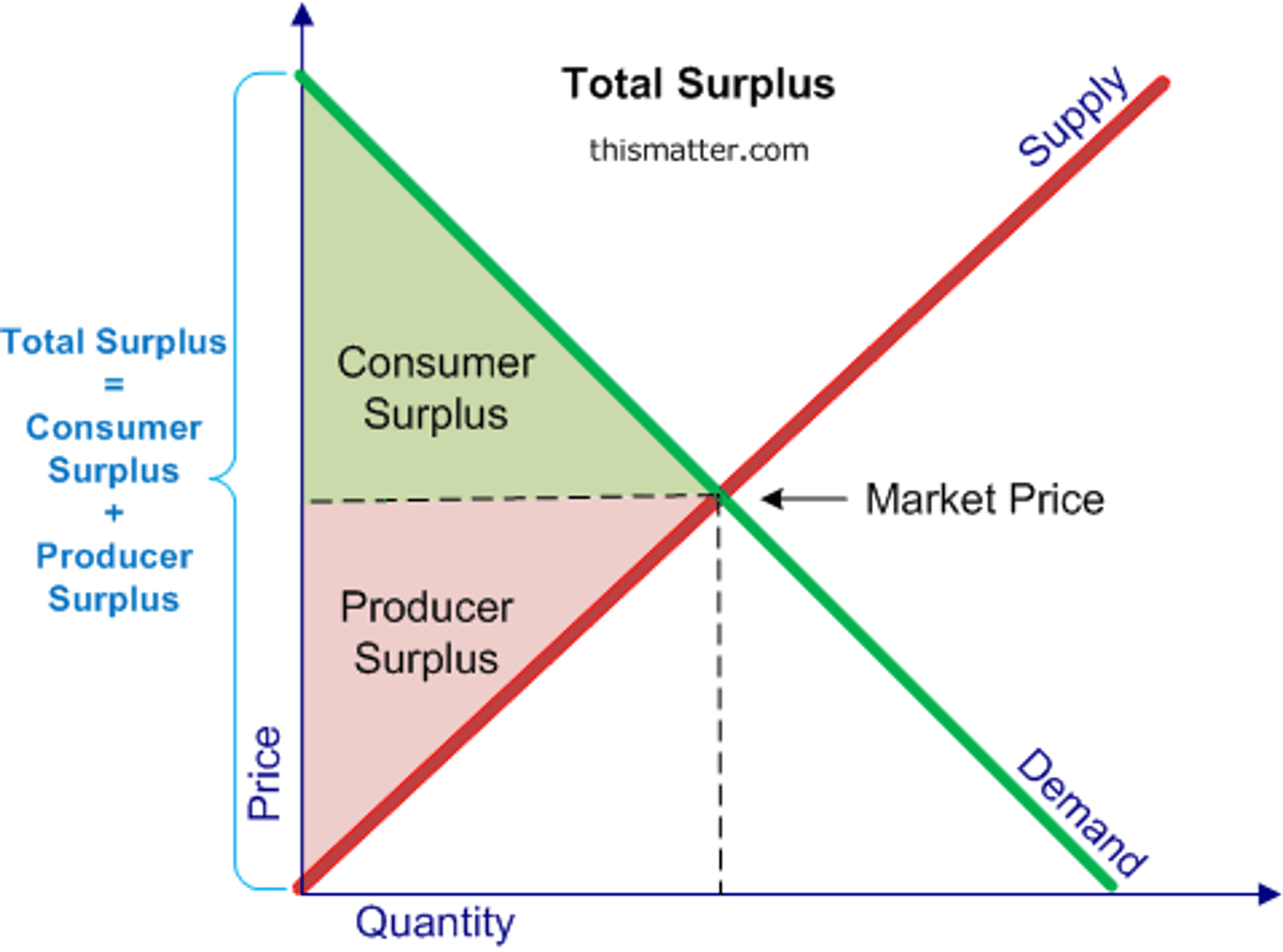

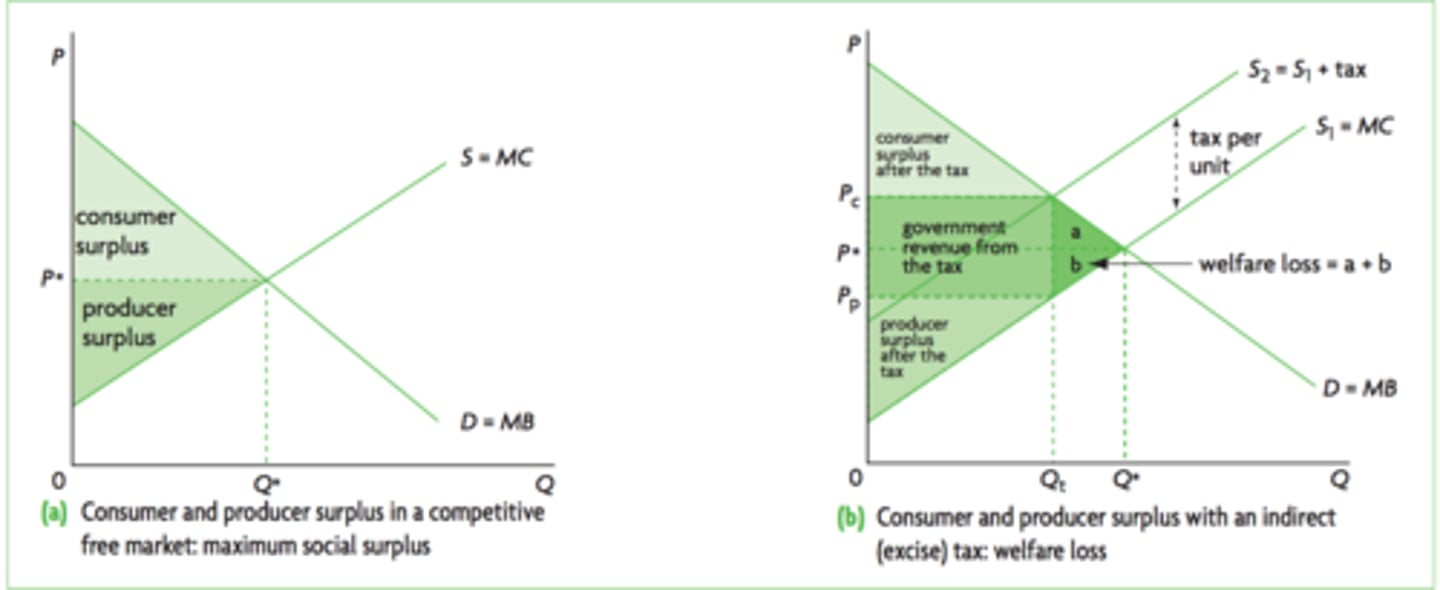

Consumer Surplus

Difference between what a consumer is prepared to pay and what they actually pay in a market.

Producer Surplus

Difference between what a producer is prepared to sell a product for compared to what they sell it for.

Total Surplus

Is the consumer and producer surplus combined.

Deadweight Loss

When total surplus is reduced because of either under or over production.

Price Ceiling

Legislated maximum price that sellers are allowed to charge in a market. BELOW equilibrium price.

Price Floor

Legislated minimum price that sellers are allowed to charge in a market. ABOVE equilibrium price.

Taxes (Indirect)

Governments can levy taxes to raise revenue so that they can spend on worthwhile projects that improve efficiency of the economy.

Elasticity Impact on a Tax

More inelastic demand is, the greater the tax revenue.

Subsidy

A payment by the government to a film in order to increase output.

Market Share

A firms sales expressed as a proportion of total sales in the market.

Concentration Ratio

Market share of the biggest firm.

Price Gauging

When a firm excessively increases price unfairly, taking advantage of demand.

Market Failure

When resources are not allocated efficiently- total surplus not maximised.

Monopoly

Extreme type of imperfect market with just one dominant firm.

Duopoly

A market with two dominant firms.

Olipology

A market with a few dominant firms.

Market Power

When a buyer or seller in a market has the ability to exert significant influence over the quantity of goods and services or price.

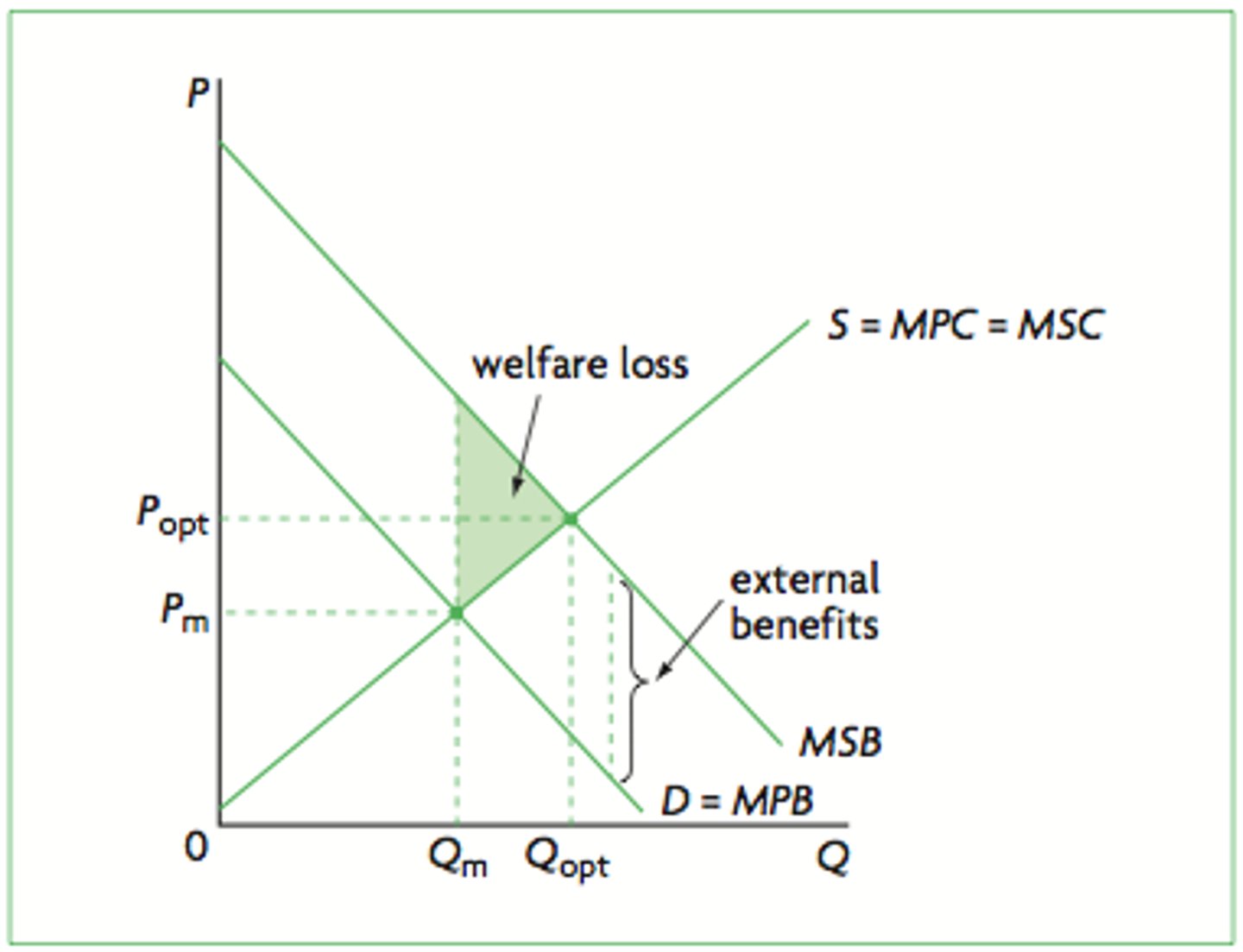

Positive Externality

External benefits to society from either production or consumption.

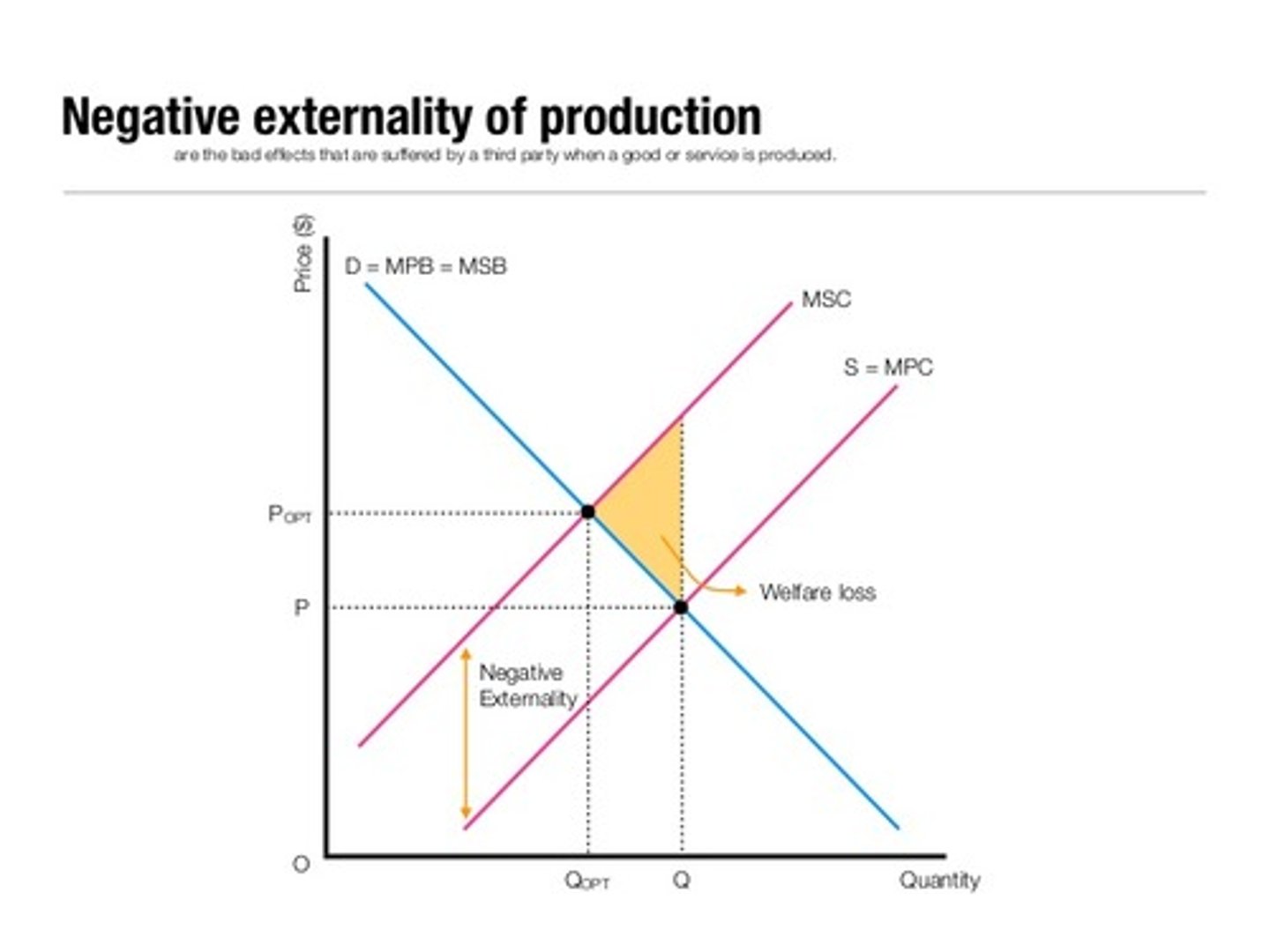

Negative Externality

External costs to society from either production or consumption.

Externalities

External side affect of all economic activity in an economy.

Private cost/benefit

cost/benefit to buyers + sellers.

External cost/benefit

cost/benefit to third parties.

Imperfect Market

When equilibrium is not being met and deadweight loss is being present. Represented mostly by monopoly, duopoly markets.

Rival Goods

A good where one consumer can prevent the simultaneous consumption for other consumers. E.g. drinks and food

Excludable Good

When a good or service can be limited to customers that only pay for it. E.g. Clothes and Shoes

Club Good

A good or service that is excludable but non-rival. When individuals can be prevented from consuming them however, their consumption does not reduce their availability to others. E.g. Netflix

Private Goods

A good where the ownership is restricted to a group, or an individual that has purchased the good for their own consumption. E.g. Computer

Negative Production Externality

When the production of a good or service causes harm to a third party.

Positive Production Externality

When the production of a good or service causes benefit to a third party.