Agra spørsmål fra de gule PowerPointene

1/112

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai | Chat |

|---|

No analytics yet

Send a link to your students to track their progress

113 Terms

Scarcity exists

a. when people consume beyond their needs.

b. only in rich nations.

c. in all countries in the world.

d. only in poor nations.

C.

Which of the following would eliminate scarcity as an economic problem?

a. Moderation of people's competitive instincts.

b. Discovery of large new energy reserves.

c. Resumption of steady productivity growth.

d. None of the above because scarcity can not be eliminated.

D.

Which of the following is not a resource?

a. Land.

b. Labor.

c. Money.

d. Capital.

C.

Economics is the study of

a. how to make money.

b. how to operate a business.

c. people making choices because of the problem of scarcity.

d. the government decision-making process.

C.

Microeconomics approaches the study of economics from the viewpoint of

a. individuals or specific markets.

b. the operation of the Federal Reserve.

c. economy wide effects

d. the national economy.

A.

A review of the performance of the U.S. economy during the 1990's is primarily the concern of

a. macroeconomics.

b. microeconomics.

c. both macroeconomics and microeconomics.

d. neither macroeconomics nor microeconomics.

A.

An economic theory claims that a rise in gasoline prices will cause gasoline purchases to fall, ceteris paribus. The phrase "ceteris paribus" means that

a. other relevant factors like consumer incomes must be held constant.

b. the gasoline prices must first be adjusted for inflation.

c. the theory is widely accepted, but cannot be accurately tested.

d. consumers need for gasoline remains the same regardless of price.

A.

An economist notices that sunspot activity is high just prior to recessions and concludes that sunspots cause recessions. The economist has

a. confused association with and causation.

b. misunderstood the ceteris paribus assumption.

c. Used normative economics to answer a positive question.

d. built an untestable model.

A. .

Which of the following is a statement of positive economics?

a. The income tax system collects a lower percentage of the incomes of the poor.

b. A reduction in the tax rates of the rich makes the tax system more fair.

c. Taxes ought to be raised to finance health care.

d. All of the above are primarily statements of positive economics.

A..

Which of the following is a statement of positive economics?

a. An unemployment rate of greater than 8 percent is good because prices will fall.

b. An unemployment rate of 7% is a serious problem.

c. If the overall unemployment rate is 7%, black unemployment rates will average 15%.

d. Unemployment is a more severe problem than inflation.

C.

Which of the following is a statement of normative economics?

a. A minimum wage is good because it raises wages for the working poor.

b. The minimum wage is supported by unions.

c. The minimum wage reduces jobs for unskilled workers.

d. The minimum wage encourages firms to substitute capital for labor.

A.

Select the normative statement that completes the following sentence: If the minimum wage is raised rapidly, then

a. inflation increases.

b. workers will gain their rightful share of total income.

c. profits will fall.

d. unemployment will rise.

B.

In Exhibit A-7, the slope of straight line CD is

a. positive.

b. zero.

c. negative.

d. variable.

A.

As shown in Exhibit A-8, the slope of straight line AB

a. decreases with increases in X.

b. increases with increases in X.

c. increases with decreases in X.

d. remains constant with changes in X.

D.

A shift is a curve represents a change in

a. the variable on the horizontal axis.

b. the variable on the vertical axis.

c. a third variable that is not on either axis.

d. any variable that is relevant to the relationship being graphed.

C.

A change in a third variable not on either axis of a graph is illustrated with a

a. horizontal or vertical line.

b. movement along a curve.

c. shift of a curve.

d. point of intersection.

C

If the demand curve for good X is downward-sloping, this means that an increase in the price will result in

a. an increase in the demand for good X.

b. a decrease in the demand for good X.

c. no change in the quantity demanded for good X.

d. a larger quantity demanded for good X.

e. a smaller quantity demanded for good X.

E.

The law of demand states that the quantity demanded of a good changes, other things being equal, when

a. the price of the good changes.

b. consumer income changes.

c. the prices of other goods change.

d. a change occurs in the quantities of other goods purchased.

A

Which of the following is the result of a decrease in the price tea, other things being equal?

a. A leftward shift in the demand curve for tea.

b. A downward movement along the demand curve for tea.

c. A rightward shift in the demand curve for tea.

d. An upward movement along the demand curve for tea.

B.

4. Which of the following will cause a movement along the demand curve for X?

a. A change in the price of a close substitute.

b. A change in the price of good X.

c. A change in consumer tastes and preferences for good X.

d. A change in consumer income.

B.

Assuming that beef and pork are substitutes, a decrease in the price of pork will cause the demand curve for beef to

a. shift to the left as consumers switch from beef to pork.

b. shift to the right as consumers switch from beef to pork.

c. remain unchanged, since beef and pork are sold in separate markets.

d. none of the above.

A.

Assuming that coffee and tea are substitutes, a decrease in the price of coffee, other things being equal, results in a (an)

a. downward movement along the demand curve for tea.

b. leftward shift in the demand curve for tea.

c. upward movement along the demand curve for tea.

d. rightward shift in the demand curve for tea.

B.

Assuming steak and potatoes are complements, a decrease in the price of steak will

a. decrease the demand for steak.

b. increase the demand for steak.

c. increase the demand for potatoes.

d. decrease the demand for potatoes.

C.

Assuming that steak is a normal good, a decrease in consumer income, other things being equal, will

a. cause a downward movement along the demand curve for steak.

b. shift the demand curve for steak to the left.

c. cause an upward movement along the demand curve for steak.

d. shift the demand curve for steak to the right.

B.

An increase in consumer income, other things being equal, will

a. shift the supply curve for a normal good to the right.

b. cause an upward movement along the demand curve for an inferior good.

c. shift the demand curve for an inferior good to the left.

d. cause a downward movement along the supply curve for a normal good.

C.

An improvement technology causes a (an)

a. leftward shift of the supply curve.

b. upward movement along the supply curve.

c. firm to supply a larger quantity at any given price.

d. downward movement along the supply curve.

C.

Suppose auto workers receive a substantial wage increase. Other things being equal, the price of autos will rise because of a (an)

a. increase in the demand for autos.

b. rightward shift of the supply curve for autos.

c. leftward shift of the supply curve for autos.

d. reduction in the demand for autos.

C.

Assuming that soybeans and tobacco can both be grown on the same land, an increase in the price of tobacco, other things being equal, causes a (an)

a. upward movement along the supply curve for soybeans.

b. downward movement along the supply curve for soybeans.

c. rightward shift in the supply for soybeans.

d. leftward shift in the supply for soybeans.

D.

If Qd = quantity demanded and Qs = quantity supplied at a given price, a shortage in the market results when

a. Qs is greater than Qd.

b. Qs equals Qd.

c. Qs is less than or equal to Qd.

d. Qs is greater than or equal to Qd.

C.

15. Assume that the equilibrium price for a good is $10. If the market price is $5, a

a. shortage will cause the price to remain at $5.

b. surplus will cause the price to remain at $5.

c. shortage will cause the price to rise toward $10.

d. surplus will cause the price to rise toward $10.

C.

2. Which of the following statements if true of a market?

a. An increase in demand, with no change in supply, will increase the equilibrium price and quantity.

b. An increase in supply, with no change in demand, will decrease the equilibrium price and the equilibrium quantity.

c. A decrease in supply, with no change in demand, will decrease the equilibrium price and increase the equilibrium quantity.

d. all of the above are true.

A.

Consider the market for chicken. An increase in the price of beef will

a. decrease the demand for chicken, creating a lower price and a smaller amount of chicken purchased in the market.

b. decrease the supply of chicken, creating a higher price a and a smaller amount of chicken purchased in the market.

c. increase the demand for chicken, creating a higher price and a greater amount of chicken purchased in the market.

d. increase the supply of chicken, creating a lower price and a greater amount of chicken purchased in the market.

C.

An increase in consumer income increases the demand for oranges. As a result of the adjustment to a new equilibrium, there is a (an)

a. leftward shift of the supply curve.

b. downward movement along the supply curve.

c. rightward shift of the supple curve.

d. upward movement along the supply curve.

D.

5. An increase in the wage paid to grape pickers will cause the

a. demand curve for grapes to shift to the right, resulting in higher prices for grapes.

b. demand curve for grapes to shift to the left, resulting in lower prices for grapes.

c. supply curve for grapes to shift to the left, resulting in lower prices for grapes.

d. supply curve for grapes to shift to the left, resulting in higher prices for grapes.

D.

6. If the federal government wants to raise the price of cheese, it will

a. take cheese from government storage and sell it.

b. encourage farmers to research ways to produce more cheese.

c. subsidize purchases of farm equipment.

d. encourage farmers to produce less cheese.

D.

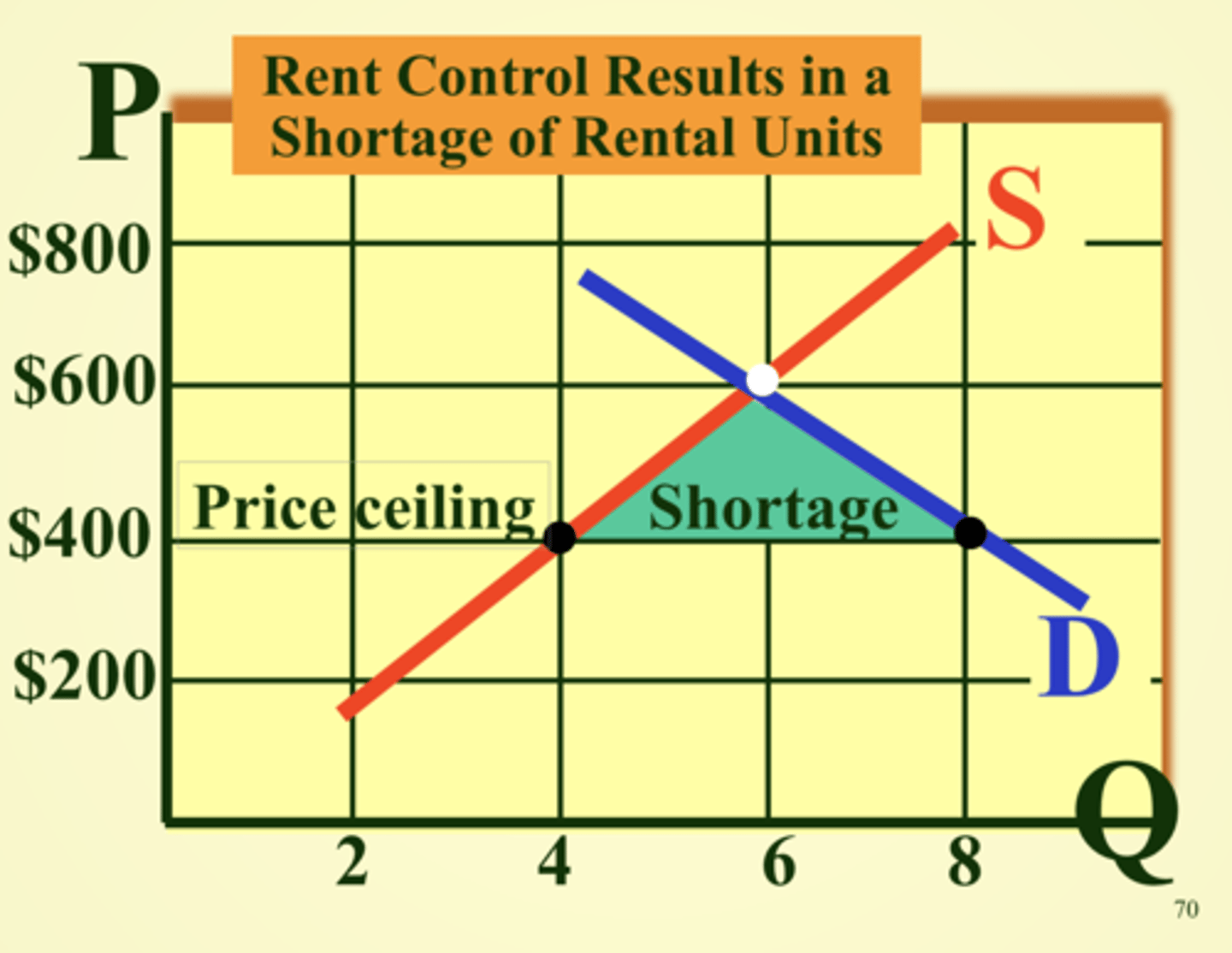

Which of the following is least likely to result from rent controls set below the equilibrium price for rental housing?

a. Shortages and black markets.

b. Deterioration of existing rental housing.

c. The supply of rental housing will increase rapidly.

d. People will demand more apartments than are available.

C.

Suppose the equilibrium price set by supply and demand is lower than the price ceiling set by the government. The result will be

a. a shortage.

b. that quantity demanded is equal to quantity supplied.

c. a surplus.

d. a black market.

B.

A good that provides external benefits to society has

a. too few resources devoted to production.

b. too many resources devoted to its production.

c. the optimal resources devoted to its production.

d. not provided profits to producers of the good.

A.

Pollution from cars is an example of a (an)

a. harmful opportunity cost.

b. negative externality.

c. production dislocation.

d. none of the above.

B.

Which of the following is the best example of a public good?

a. Pencils.

b. Education

c. Defense

d. Trucks

C.

A public good may be defined as any good or service that

a. allows users to collectively consume benefits.

b. must be distributed equally to all citizens in equal shares.

c. is never produced by government.

d. answers a and c above.

A.

If an increase in bus fares in Charlotte, North Carolina reduces total revenue of the public transit system, this is evidence that demand is

a. price elastic.

b. price inelastic

c. unitary elastic

d. perfectly elastic

A.

Which of the following is the result of an increase in total revenue?

a. Price increases when demand is elastic.

b. Price decreases when demand is elastic.

c. Price increases when demand is unitary elastic.

d. Price decreases when demand is inelastic.

B.

You are on a committee that is considering ways to raise money for your city's symphony program. You would recommend increasing the price of symphony tickets only if you thought the demand curve for these tickets was

a. inelastic.

b. elastic.

c. unitary elastic.

d. perfectly elastic.

A.

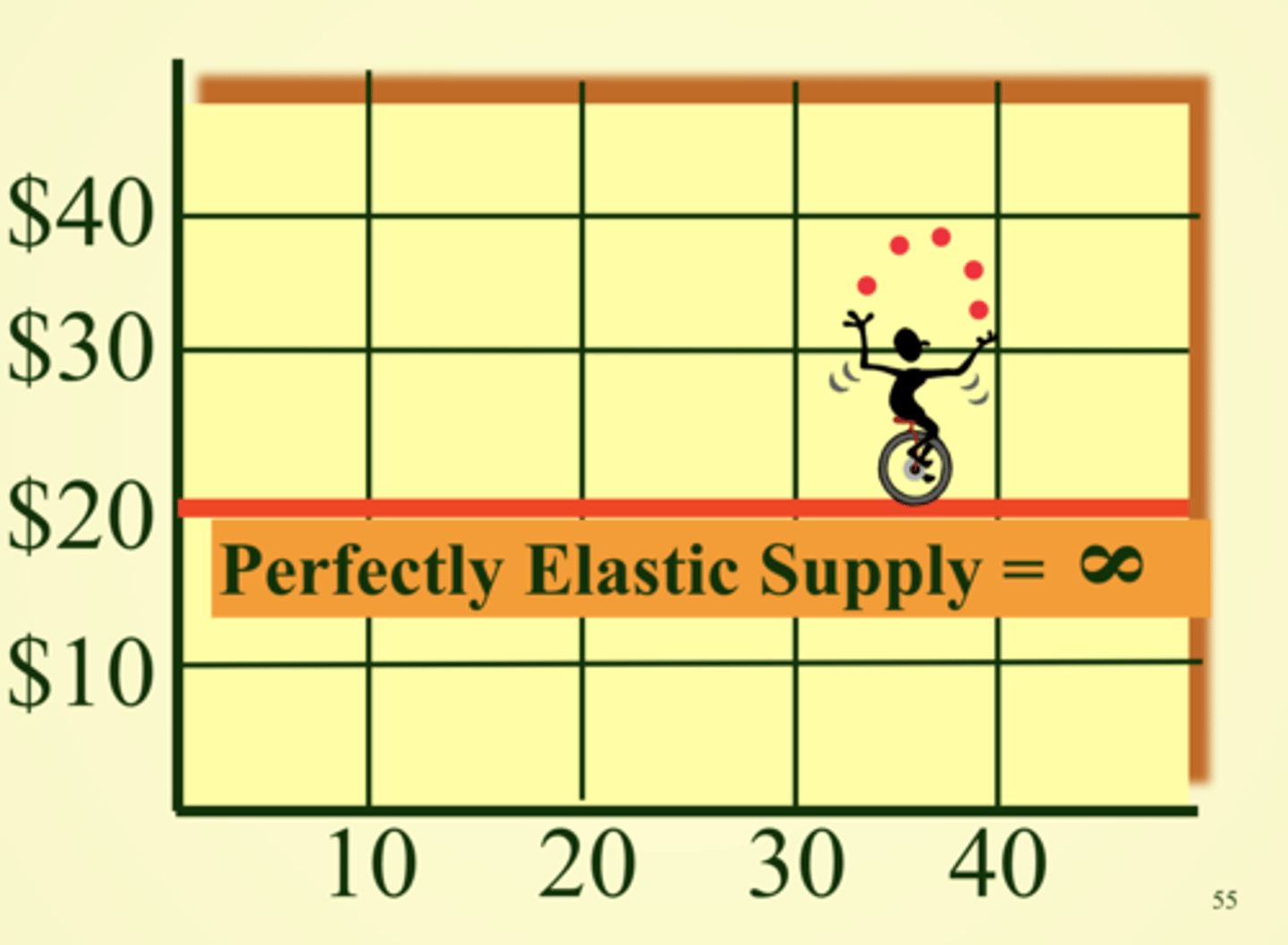

The price elasticity of demand for a horizontal demand curve is

a. perfectly elastic.

b. perfectly inelastic.

c. unitary elastic.

d. inelastic.

e. elastic.

A.

Suppose the quantity of steak purchased by the Jones family is 110 pounds per year when the price is $2.10 per pound and 90 pounds per year when the price is $3.90 per pound. The price elasticity of demand coefficient for this family is

a. 0.33.

b. 0.50.

c. 1.00.

d. 2.00.

A.

If a 5 percent reduction in the price of a good produces a 3 percent increase in the quantity demanded, the price elasticity of demand over this range of the demand curve is

a. elastic.

b. perfectly elastic.

c. unitary elastic.

d. inelastic.

e. perfectly inelastic.

D.

A manufacturer of Beanie Babies hires an economist to study the price elasticity of demand for this product. The economist estimates that the price elasticity of demand coefficient for a range of prices close to the selling price is greater than 1. The relationship between changes in price and quantity demanded for this segment of the demand curve is

a. elastic.

b. inelastic.

c. perfectly elastic.

d. perfectly inelastic.

e. unitary elastic

A.

A downward-sloping demand curve will have a

a. higher price elasticity of demand coefficient along the top of the demand curve.

b. lower price elasticity coefficient along the top of the demand curve.

c. constant price elasticity of demand coefficient throughout the length of the demand curve.

d. positive slope.

A.

The price elasticity of demand coefficient for a good will be less

a. if there are few or no substitutes available.

b. if a small portion of the budget will be spent on it.

c. in the short run than in the long run.

d. all of the above are true.

D.

The income elasticity of demand for shoes is estimated to be 1.50. We can conclude that shoes

a. have a relatively steep demand curve.

b. have a relatively flat demand curve.

c. are a normal good.

d. are an inferior good.

C.

To determine whether two goods are substitutes or complements, an economist would estimate the

a. price elasticity of demand.

b. income elasticity of demand.

c. cross-elasticity of demand.

d. price elasticity of supply.

C.

If the government wanted to raise tax revenue and shift most of the tax burden to the sellers, it would impose a tax on a good with a

a. steep (inelastic) demand curve and a steep (inelastic) supply curve.

b. steep (inelastic) demand curve and a flat (elastic) supply curve.

c. flat (elastic) demand curve and a steep (inelastic) supply curve.

d. flat (elastic) demand curve and a flat (elastic) supply curve.

C.

As an individual consumes more of a given good, the marginal utility of that good to the consumer

a. rises at an increasing rate.

b. rises at a decreasing rate.

c. falls.

d. rises.

C.

The amount of added utility that a consumer gains from the consumption of one more unit of a good is called

a. incremental utility.

b. total utility.

c. diminishing utility.

d. marginal utility.

D.

A certain consumer buys only food and compact discs. If the quantity of food bought increases, while that of compact discs remains the same, the marginal utility of food will

a. fall relative to the marginal utility of compact discs.

b. rise relative to the marginal utility of compact discs.

c. rise, but not as fast as the marginal utility of compact discs falls.

d. fall, but not as fast as the marginal utility of compact discs falls.

A.

Rational consumers will continue to consume two goods until

a. the marginal utility per dollar's worth of the two goods is the same.

b. the marginal utility is the same for each good.

c. the prices of the two goods are equal.

d. the prices of the two goods are unequal.

A.

Assume a person's consumption of just the right amounts of pork and chicken is in equilibrium. We can conclude that the

a. marginal utility of pork must equal the marginal utility of chicken.

b. price of pork must equal the price of chicken.

c. ratio of marginal cost to price must be the same in both the pork and the chicken markets.

d. ratio of marginal utility to price must be the same for pork and chicken.

D.

Assume an individual consumes only milk and doughnuts, and he/she has arranged consumption so that the last glass of milk yields 12 utils and the last doughnut 6 utils. If the price of milk is $1 per glass and the price of a doughnut is $.50, we can conclude that the

a. consumer should consume less milk and more doughnuts.

b. price of milk is too high relative to doughnuts.

c. consumer should consume more milk and fewer doughnuts.

d. consumer is in equilibrium.

D.

Suppose an individual consumes pizza and cola. To reach consumer equilibrium, the individual must consume pizza and cola so that the

a. price paid for the two goods is the same.

b. marginal utility of the two goods is equal.

c. ratio of marginal utility to price is the same for both goods.

d. ratio of marginal utility of cola to marginal utility of pizza is 1.

C.

A state of consumer equilibrium for goods consumed prevails when the

a. marginal utility of all goods is the same.

b. marginal utility per dollar's worth of two goods is the same.

c. price of two goods is the same.

d. marginal cost per dollar spent on two goods is the same.

B.

The change in quantity demanded resulting from a change in purchasing power is known as the

a. income effect.

b. substitution effect.

c. law of demand.

d. consumer equilibrium effect.

A.

In exhibit 4, assume Multiplex tickets cost $6 each, video rentals cost $2 each, and bags of popcorn cost $1 each. What is the marginal utility of renting a third video?

a. 6 utils.

b. 8 utils.

c. 10 utils.

d. 30 utils.

A.

In exhibit 4, assume Multiplex tickets cost $6 each, video rentals cost $2 each, and bags of popcorn cost $1 each. Suppose the consumer has $12 per week to spend on Multiplex tickets, video rentals, and popcorn. What combination of goods will give the consumer the most utility?

a. 1 movie, 3 videos, and no popcorn.

b. 1 movie, 2 videos, and 2 bags of popcorn.

c. 1 movie, 1 video, and 4 bags of popcorn.

d. 2 movies, no video, and no bags of popcorn.

B.

Explicit costs are payments to

a. hourly employees.

b. insurance companies.

c. utility companies.

d. all of the above.

D.

Implicit costs are the opportunity costs of using the resources of

a. outsiders.

b. owners.

c. banks.

d. retained earnings.

B.

Which of the following equalities is true?

a. Economic profit = total revenue - accounting profit.

b. Economic profit = total revenue - explicit costs - accounting profit.

c. Economic profit = total revenue - implicit costs - explicit costs.

d. Economic profit = opportunity costs + accounting costs.

C.

Fixed inputs are factors of production that

a. are determined by a firm's size.

b. can be increased or decreased quickly as output changes.

c. cannot be increased or decreased quickly as output changes.

d. none of the above.

C.

An example of a variable input is

a. raw materials.

b. energy.

c. hourly labor.

d. all of the above

D.

Suppose a car wash has 2 washing stations and 5 workers and is able to wash 100 cars per day. When it adds a third station, but no more workers, it is able to wash 150 cars per day. The marginal product of the third washing station is

a. 100 cars per day.

b. 150 cars per day.

c. 5 cars per day.

d. 50 cars per day.

D.

If the units of variable input in a production process are 1, 2, 3, 4, and 5 and the corresponding total outputs are 10, 22, 33, 42, and 48, respectively, the marginal product of the fourth unit is

a. 2.

b. 6.

c. 9.

d. 42.

C.

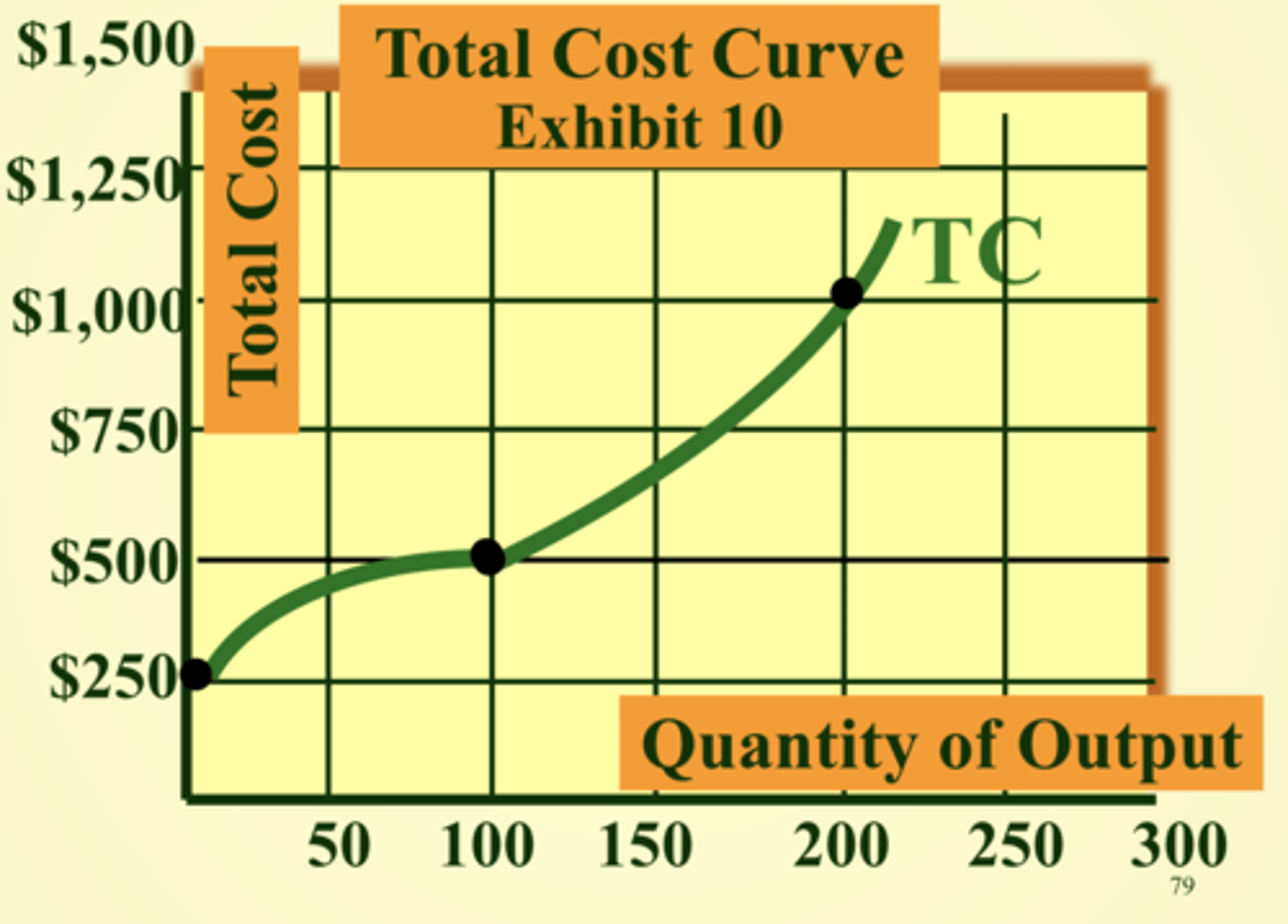

The total fixed cost curve is

a. upward sloping.

b. downward sloping.

c. upward, and then downward sloping.

d. unchanged with the level of output.

D.

Assuming that the marginal cost curve is a smooth U-shaped curve, the corresponding total cost curve has a (an)

a. linear shape.

b. S-shape.

c. U-shape.

d. reverse S-shape.

D.

If both the marginal cost and the average variable cost curves are U-shaped, at the point of minimum average variable cost, the marginal cost must be

a. greater than the average variable cost.

b. less than the average variable cost.

c. equal to the average variable cost.

d. at its minimum.

C.

Which of the following is true at the point where diminishing returns set in?

a. Both marginal product and marginal cost are at a maximum.

b. Both marginal product and marginal cost are at a minimum.

c. Marginal product is at a maximum and marginal cost at a minimum.

d. Marginal product is at a minimum and marginal cost at a maximum.

C.

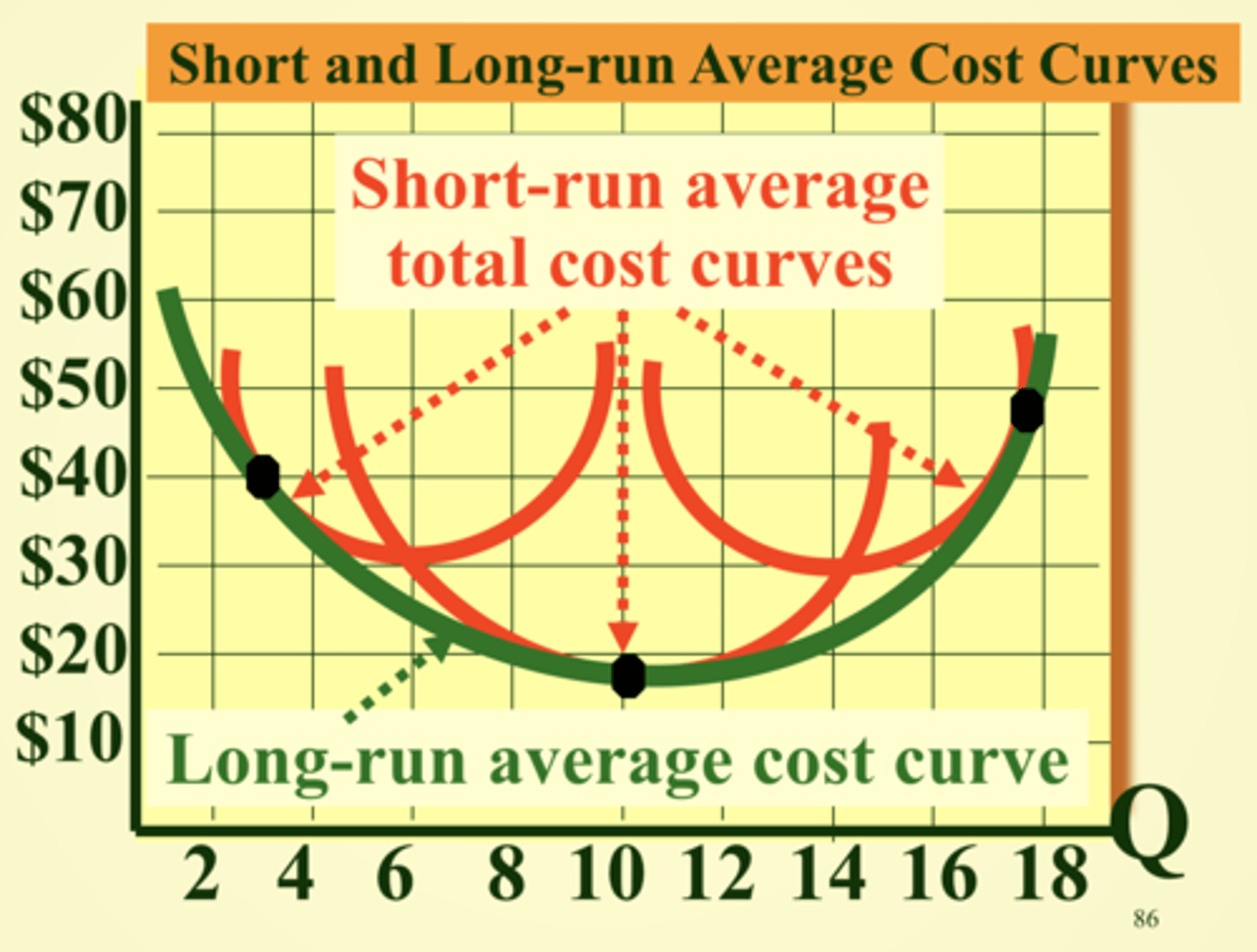

Each potential short-run average total cost curve is tangent to the long-run average cost curve at

a. the level of output that minimizes short-run average total cost.

b. the minimum point of the average total cost curve.

c. the minimum point of the long-run average cost curve.

d. a single point on the short-run average total cost curve.

D.

Suppose a typical firm is producing X units of output per day. Using any other plant size, the long-run average cost would increase. The firm is operating at a point which its

a. long-run average cost curve is at a minimum.

b. short-run average total cost curve is at a minimum.

c. both (a) and (b) are true.

d. neither (a) nor (b) is true.

C.

The downward-sloping segment of the long-run average cost curve corresponds to

a. diseconomies of scale.

b. both economies and diseconomies of scale.

c. the decrease in average variable cost.

d. economies of scale.

D.

Long-run diseconomies of scale exist when the

a. short-run average total cost curve falls.

b. long-run marginal cost curve rises.

c. long-run average cost curve falls.

d. short-run average cost curve rises.

e. long-run average cost curve rises.

E.

Long-run constant returns to scale exist when the

a. short-run average total cost curve is constant.

b. long-run average cost curve rises.

c. long-run average cost curve is flat.

d. long-run average cost curve falls.

C.

A perfectly competitive market is not characterized by

a. many small firms.

b. a great variety of different products.

c. free entry into and exit from the market.

d. any of the above.

B.

Which of the following is a characteristic of perfect competition?

a. Entry barriers.

b. Homogeneous products.

c. Expenditures on advertising.

d. Quality of service.

B.

Which of the following are the same at all levels of output under perfect competition?

a. Marginal cost and marginal revenue.

b. Price and marginal revenue.

c. Price and marginal cost.

d. All of the above.

B.

If a perfectly competitive firm sells 100 units of output at a market price of $100 per unit, its marginal revenue per unit is

a. $1.

b. $100.

c. more than $1, but less than $100.

d. less than $100.

B.

Short-run profit maximization for a perfectly competitive firm occurs when the firm's marginal cost equals

a. average total cost.

b. average variable cost.

c. marginal revenue.

d. all of the above.

C.

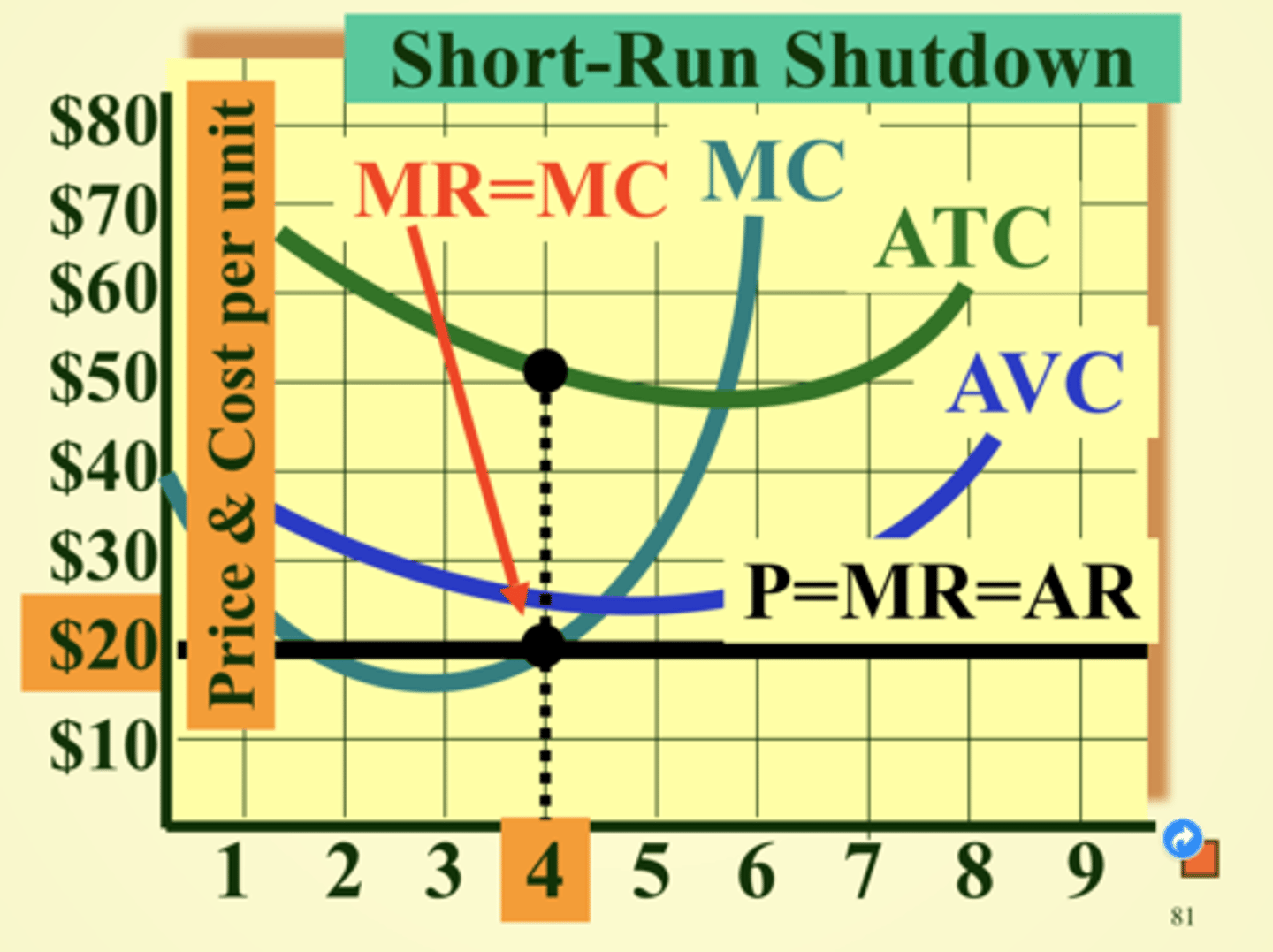

A perfectly competitive firm sells its output for $100 per unit, and the minimum average variable cost is $150 per unit. The firm should

a. increase output.

b. decrease output, but not shut down.

c. maintain its current rate of output.

d. shut down.

D.

A perfectly competitive firm's supply curve follows the upward sloping segment of its marginal cost curve above the

a. average total cost curve.

b. average variable cost curve.

c. average fixed cost curve.

d. average price curve.

B.

In long-run equilibrium, the perfectly competitive firm's price equals which of the following?

a. Short-run marginal cost.

b. Minimum short-run average total cost.

c. Marginal revenue.

d. All of the above.

D.

In a constant-cost industry, input prices remain constant as?

a. the supply of inputs fluctuates.

b. firms encounter diseconomies of scale.

c. workers become more experienced.

d. firms enter and exit the industry.

D.

Suppose that , in the long run, the price of feature films rises as the movie production industry expands. We can conclude that movie production is a (an)

a. increasing-cost industry.

b. constant-cost industry.

c. decreasing-cost industry.

d. marginal-cost industry.

A.

17. Which of the following is true of a perfectly competitive market?

a. If economic profits are earned, then the price will fall over time.

b. In long-run equilibrium, P = MR = SRMC = SRATC = LRAC.

c. A constant-cost industry exists when the entry of new firms has no effect on their cost curves.

d. All of the above.

D.

A monopolist always faces a demand curve that is

a. perfectly inelastic.

b. perfectly elastic.

c. unit elastic.

d. the same as the market demand curve.

D.

A monopoly sets the

a. price at which marginal revenue equals zero.

b. price that maximizes total revenue.

c. highest possible price on its demand curve.

d. price at which marginal revenue equals marginal cost.

D.

A monopolist sets

a. the highest possible price.

b. a price corresponding to the minimum average total cost.

c. a price equal to marginal revenue.

d. a price determined by the point on the demand curve corresponding to the level of output at which marginal revenue equals marginal cost.

e. none of the above.

D.

Which of the following is true for the monopolist?

a. Economic profit is possible in the long-run.

b. Marginal Revenue is less than the price charged.

c. Profit maximizing or loss minimizing occurs when marginal revenue equals marginal cost.

d. All of the above are true.

D.

For a monopolist to practice effective price discrimination, one necessary condition is

a. identical demand curves among groups of buyers.

b. differences in the price elasticity of demand among groups of buyers.

c. a homogeneous product.

d. none of the above.

B.

What is the act of buying a commodity at a lower price and selling it at a higher price?

a. Buying short.

b. Discounting.

c. Tariffing.

d. Arbitrage.

D.

Under both perfect competition and monopoly, a firm

a. is a price taker.

b. is a price maker.

c. will shut down in the short run if price falls short of average total cost.

d. always earns a pure economic profit.

e. sets marginal cost equal to marginal revenue.

E.

1. An industry with many small sellers, a differentiated product, and easy entry would best be described as which of the following?

a. Oligopoly.

b. Monopolistic competition.

c. Perfect competition.

d. Monopoly.

B.

Which of the following industries is the best example of monopolistic competition?

a. Wheat.

b. Restaurant.

c. Automobile.

d. Water service.

B.