Final

1/269

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

270 Terms

What is finance?

The allocation of resources across staets of the world over time with uncertainty. In other words: Finance is how a company allocates money, capital, and assets across different possible outcomes and over time with levels of uncertainty.states

What does finance allow you to do with the resources?

Allows you to put resources where they are most needed

How does finance relate to time?

You can either pay now and get money back later or get money now and pay back later

How does finance relate to risk?

The amount you get or pay depends on future circumstances

What is finance not about?

It is not about the use of money at a point in time to buy goods and services or about earning the money through the provision of labor

Why is financial markets needed?

Without financial markets, no projects will be undertaken and money will have 0 return, leading to inefficiency

What makes financial markets beneficial?

People with money at hand will transfer to those with projects, since investment is undertaken the reward will be split among all of us

What are financial contracts?

Contracts that determine how risk and rewards are to be split

What role does banks (financial intermediaries) play in finance?

A bank takes money from savers and passes it to investors with opportunities, charging a fee for this service.

What is personal finance?

Financial transactions that involves individuals or families, aka “households”

Who are the main participants in personal finance transactions?

Households and specialized financial intermediaries (such as banks and financial institutions).

How is technology changing personal finance transactions?

Advancing technology is increasing peer-to-peer financial transactions, reducing reliance on traditional intermediaries.

What happens to the literacy rate as the population get older?

As one get older, they are more literate. The yougest have the lowest literacry rate, but overall, financial literacy in U.S is very low

What does the P-Fin Index (financial literacy test) cover?

It has 28 questions and it covers 8 functional areas:

earning

saving

consuming

investing

borrowing

insuring

comprehending risk

go-to information sources

What is the financial illiteracy US is holding in the recent decade

It is still incredibly high at around 50%. People in America know most about borrowing and saving but does not know much about investing, insurance, and comprehending risk

What can we do about low financial literacy

We can develop our own financial literacy and share it with others, so in a way, finding resources and learn more about it ourselves.

What innocations can help improve the financial decision making system?

Disclosures: Providing clear, relevant information at the moment a financial decision is made.

Nudges: Setting default options that guide people toward better choices while preserving freedom to opt out.

Fintech: Using technology to simplify and automate personal finance tasks.

Fiduciary duty: A legal obligation requiring financial professionals to act in the best interest of their clients, not themselves

Consumer financial protection: Government regulation of financial products and institutions to prevent fraud, abuse, and deception.

What is the Continental Europe Approach?

It focuses on stronger government regulation and greater state provision of financial services to protect consumers and reduce the need for complex individual financial decision-making.

Why does financial knowledge matter?

People who is financially literate:

is more likely to cope wth financial shocks

is less likely to be debt-constrained

is more likely to invest in financial markets

is more likely to save and plan for retirement

What is a hosehold balance sheet?

A statement of all an entity’s assets (things owned) and liabilities (things owed) at a point in time

What are main household assets?

Home equity

Vehicles

Financial asset

Cash, high value items

Savings (retirement, or stocks/bonds)

Inheritance (firms)

Intellectual property

Human capital

Income

Alimony

Payouts

What are main household liability?

Student loans

Taxes

Mortgage, auto loans

Children

What is the difference between financial asset and real asset?

Financial asset are claims on future cash flowers or ownership. Examples include cash, stock, bonds, mutual funds, bank deposits, and cryptocurrencies. Real assets are items with intrisic values.

What is the formula for total asset?

Financial assets + real assets

What is the formula for net worth?

Total assets - total liabilities

What is net worth?

Value of wealth

What are the three types of wealth

Total gross tangible wealth

Net tangible wealth

Real wealth

Financial wealth

What is corporate finance

Corporate finance is the study of firms, seeing how they make their investment decisions (which projects to invest in and the net present value of those projects), financing decisions (debt or equity), and the impact of these decisions on the economy

Who owns and controls corporations?

Shareholders own the corporation and managers control the corporation. The objective of managers is to maximize the value to shareholders but there may have distorted incentives to maximize their own value.

Who are the shareholders?

Founders and descendants (family firms)

Managers (through stock options)

Financial investors (PE firms, hedge funds)

Governments (nationalized firms)

Retail investors (households: 401k, IRAs, etc)

What does the “Firm Investment Decisions & Cash Flows” model illustrate?

illustrates how cash flows move between:

Financial markets (investors)

The financial manager

The firm’s operations

It shows how firms raise capital, invest in projects, generate cash flows, and either reinvest or return cash to investors.

Describe the steps in the “Firm Investment Decisions & Cash Flows” model.

The model describes how cash flows move through the firm in five steps:

Cash is raised from investors (Financing decision): The firm raises capital from financial markets by issuing debt (bonds) or equity (stock).

Cash is invested in firm operations (Investment / Capital budgeting decision): The financial manager invests the raised funds into real assets such as equipment, projects, R&D, or expansion.

Operations generate cash flows: The firm’s real assets produce operating cash flows from business activities. This is where value is created.

4a. Cash is reinvested in the firm: Some of the generated cash is reinvested to support growth or maintain assets.

4b. Cash is returned to investors (Payout decision): Remaining cash is distributed to investors through dividends, share repurchases, interest payments, or debt repayment.

Why do we need corporations?

Corporations exist to efficiently connect wealthy savers (investors) with entrepreneurs who have ideas but lack capital

What is limited liability and why is it important in corporations?

When shareholders and entrepreneurs in a corporation can lose only the amount they invested in the firm and are not personally responsible for the firm’s debts if the project fails. This would encourage investments by reducing their personal financial risk and more investments.

What tradeoffs does limited liability create?

This would lead to entrepreneurs to compensate investors with higher expected returns and distorts incentives of the entrepreneurs to take on too much risk (gambling)

Why do we still need corporations despite the distortion it causes?

Society wants innovation and productive risk-taking.

Human capital is inalienable (we do not allow debt slavery if projects fail).

Legal and regulatory systems exist to reduce distortions and protect investors.

In what ways are households and corporations similar?

They both:

decide when to use resources (today vs later)

decide how much risk to take

decide who bears risk when things go wrong

ar within financial & governmental institutions

Why does valuation matter?

It brings a common unit for compairing plans and it tells us if the plan is fesiable. This is important since financial decision involve in tradeoffs across time and money is valued differently today and in the future.

Why is later payment worth less than payment today?

You could have invested the amount from today’s payment and received some return. The difference is an opportunity cost.

What is interest rate?

The price of shifting resources across time

What is interest rates in savings?

The amount you receive in return for lending your money to someone else (bank). Interest rates may be thought as the rate wich savings grow over time

What is interest rates in borrowing

The amount you pay for using the money. Interst rates may be thought as the rate at which debt grows over time

What is lifetime feasibility cosntraint?

Where the total value of what you consume cannot exceed the total value of what you earn in your entire lifetime

What is the formula to find future value over one period?

FV = PV(1 + i)

What is the formula to find interest rate?

i = (FV - PV) / PV

What is the formula to find the future value over multiple periods?

FV(n) = PV (1 + i)n

What is the formula for finding the present value (discounting) over one period?

PV = FV / (1 + r)

What is the formula for finding the present value (discounting) over multiple period?

PV = FV / (1 + r)T

What is the formula for computing NPV?

NPV = C0 + C1 / (1 + r)

Where C0 represent cost today and C1 represent cost next year

What is CPI?

Consumer price index which measures how much money is needed to buy the same fixed basket of goods over time.

How do you find inflation?

π = (FCPI / PCPI) - 1

Where FCPI is future CPI and PCPI is present CPI

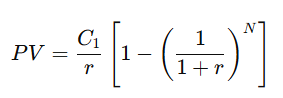

What is an annuity?

Starts at time t = 1

Occurs at regular intervals

Lasts for a fixed number of periods NNN

What is a perpetuity?

A perpetuity is an annuity that lasts forever ( N = ∞ ).

It is an infinite stream of cash flows starting at t = 1.

What is the present value formula for annuity with no growth?

What is the present value formula for perpetuity with no growth?

PV = C1 / r

Where C is the payment per period

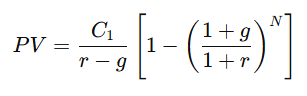

What are annuities with many equal payments (with growth)?

if g < r

What is the formula for growing perpetuity

PV = C1 / (r − g)

How does discount rate reflect the riskiness of cash flows?

Higher r lead to higher risk, lower r lead to lower risk

What is discounting and when do we use it?

It is when we move money backward in time and we use it to compare cost of today to benefits in the future.

What is compounding and when do we use it?

It is when we move money forward in time and we use it to compare the amount today would be in the future.

What is the formula for rate of return?

Returnt = (Pricet − Pricet-1) / Pricet−1

Where Pricet−1 is the price when you bought it and Pricet is the price when you sell

What is gross return?

Gross return = price today / price you paid for it

What is risk premium?

The exta return investors require for taking risk, risk of uncertainty

What is the quation for expected gain//loss

E[gain or loss] = probability(possible outcome)

Add all probability × outcome terms for each possible outcome.

What is variance used for?

Used to measure uncertainty

What is the formula for variance?

Var(X) = E[X2] − (E[X])2

All possible outcomes go though the set

How do I find the standard deviation?

Find the square root of variabce

What is standard deviation used to find?

How much the outcome typically deviate from the expected value, also measure risk or uncertainty

What is the sharpe ratio?

The ratio that measures the average compensation you are getting for an extra unit of valatility

What is the formula for the sharpe ratio?

SR = E(R) / σ(R)

Where each unit of volatilty you take would earn you x unit of expected returns. The larger the ratio the better

What are leveraged returns?

The returns you earn when you use borrowed money to icnrease the size of yoru investments

How does leverage amplifies returns?

Since you borrow money to invest, you invest less initially and get higher gains on average. However, leverage can magnifies both gains and losses

What is risk?

Risk is the covariance with your marginal utility of wealth, so something that hurts you when you most need money.

Why does bad states matter more?

In bad states, income is low, borrowing is hard, and extra $1 matters more

What risks do people care about and what goes wrong?

Job loss risk

income collapses in recessions

Health risk

large medical expenses

Housing risk

house value falls

Inflation risk

purchasing power erodes

Aggregate recession risk

many bad things happen together

What are assets/contracts that hedge risks?

Job loss risk

Unemployment insurance, severance, emergency savings

Health risk

health insurance

Housing risk

long-term fixed rate mortgage, diversification across assets

Inflation risk

TIPS, inflation -indexed pensions

Aggregate recession risk

gov bonds, cash, social insurance

If an asset hedges an important risk, should we expect it to have a high or low average return?

Assets that hedge important risks have low expected returns. Assets that expose you to bad states must offer high expected returns.

Why do investors care about when an asset pays?

Investors also cares aout when an asset pays because assets taht pay off in bad states are valuable as insurance. Investors who pay more today for these assets will expect a lower average return.

What are assets that have low expected return (insurance-like)

government bonds

inflation-protected sectuities (TIPS)

insurance contracts

Why do risky assets have higher expected returns?

Assets that perform poorly in bad economic states increase overall economic risk. Investors require compensation to hold them and have higher expected returns when doing so

What assets are high expected return (exposed to bad states)?

stocks

housing (especially when leveraged)

entrepreneurial income

These are all assets that bring high expected returns

What is Beta and what does it tell you.

Beta measures how much an asset moves with the market.

βi = Cov(Ri, Rm) / Var(Rm)

It tells you how sentitive an asset is to overall market movement

What is the interpretation of Beta?

β = 1

The asset moves one-for-one with the market. If market goes up 10%, asset goes up about 10%.

β > 1 (High Beta)

The asset moves more than the market.

If market goes up 10%, asset might go up 15%.

If market falls 10%, asset might fall 15%.

0 < β < 1 (Low Beta)

Asset moves less than the market

If market goes up 10%, asset might go up 5%

If market falls 10%, asset might fall 5%

β < 0 (Negative Beta)

Asset moves opposite the market.

If market goes up by 10%, asset goes down 10%

If market goes down by 10%, asset goes up by 10%

Does high beta have higher or lower risk? What about low beta? Why?

Higher beta have higher risk and lower beta have lower risk. This is because risk is valued at how much an asset performs in a bad state. Since high beta falls a lot during bad state, it is riskier.

What is alpha?

Alpha is the difference ebtween asset’s actual return and the return predicted by beta

What does positive alpha mean?

The asset earned more than its risk exposure predicts

What does negative alpha mean?

Asset earned less than its risk exposure predicts

What is a complete market in the Arrow–Debreu model?

A complete market is a theoretical financial market where a security exists for every possible state of the world. This means individuals can trade assets that pay off in specific future states, allowing them to fully insure against all possible risks.

What is an Arrow–Debreu security?

An Arrow–Debreu security is a financial asset that pays $1 if a specific state of the world occurs and $0 in all other states. By combining many such securities, individuals can create payoffs for any possible future outcome.

What does complete market (the Arrow–Debreu model) assume about risk trading?

The model assumes that all risks can be traded in financial markets because a state-contingent security exists for every possible outcome. This allows individuals to perfectly hedge or insure against uncertainty.

In complete markets, what determines asset prices?

Asset prices reflect state-contingent marginal utility, represented by the stochastic discount factor (SDF). Money in states where people value consumption more (such as bad economic states) is priced more highly.

Why do complete markets lead to efficient risk sharing?

Because securities exist for every possible state, individuals can trade contracts that shift income across states of the world. This allows risk to be distributed optimally across individuals so that no one bears unnecessary risk.

Why are real-world markets not complete?

In reality, many risks cannot be insured because of issues such as information problems, moral hazard, adverse selection, and large correlated risks. As a result, markets for some risks never develop.

What does it mean when insurance markets “unravel”?

An insurance market unravels when it collapses or fails to function effectively, often due to adverse selection (high-risk individuals are more likely to buy insurance) or moral hazard (insured individuals take more risks).

Why do real insurance contracts often include deductibles and exclusions?

Insurance contracts include deductibles, partial coverage, and exclusions to reduce moral hazard and insurer risk, and to make insurance markets financially sustainable despite information problems.

What is the key difference between Arrow–Debreu theory and real insurance markets?

Arrow–Debreu theory assumes complete markets where all risks can be insured, leading to efficient risk sharing. In reality, markets are incomplete, many risks are uninsured, and insurance contracts provide only partial coverage.

What is asymmetric information in insurance markets?

Asymmetric information occurs when one party in a transaction has more information than the other. In insurance markets, individuals often know more about their risk level or behavior than insurers do, which can lead to problems like adverse selection and moral hazard.

What does ex-ante mean in insurance markets?

Ex-ante refers to the period before an insurance contract is signed. At this stage, insurers may not observe the true risk type of potential customers, which can lead to adverse selection.

What does ex-post mean in insurance markets?

Ex-post refers to the period after an insurance contract has been signed, when the insurer may not be able to observe the behavior of the insured individual.