Lvl 2: Corporate issuers

1/28

There's no tags or description

Looks like no tags are added yet.

Name | Mastery | Learn | Test | Matching | Spaced | Call with Kai |

|---|

No analytics yet

Send a link to your students to track their progress

29 Terms

Stock dividend

not taxable

does not affect the shareholder’s proportionate ownership

does not change the value of each shareholder’s ownership

favors long-term investors, lower the company’s cost of equity financing

increase the stock’s float, improves the liquidity of the shares and dampens share price volatility

lower stock price will attract more investors

cash dividend affects a company’s capital structure, whereas a stock dividend has no economic impact on a company

Stock Splits

no economic effect on the company

shareholders’ total cost basis does not change

same dividend payout ratio

perfect capital market assumptions

dividend policy should have no impact on its cost of capital

assuming a company has a given capital budget, accepts all projects with a positive net present value + current capital structure and debt ratio are optimal

issue additional common shares in the amount of its capital budget

newly issued shares would exactly offset the value of the dividend

dividend policy matters

investors prefer a dollar of dividends to a dollar of potential capital gains from reinvesting earnings

dividend income has traditionally been taxed at higher rates than capital gains

factors that affect dividend policy

investment opportunities

expected volatility of future earnings

financial flexibility

tax considerations - double taxation; dividend imputation tax system (taxed once); split rate tax (distributed earnings taxed lower)

shareholder preference for current income

flotation cost

fees to issue shares

adverse price impact from increase supply of shares

impairment of capital rule

net value of the remaining assets as shown on the balance sheet be at least equal to some specified amount

Lintner’s model

Expected increase in dividends = (Expected earnings × Target payout ratio − Previous dividend) × Adjustment factor

Adjustment factor = 1 / no. of years the adj will take place

share repurchase methods

buy in open market - flexible - no legal obligation

buy fixed number at fixed price - if more demand, prorate - done quickly

dutch auction - range of acceptable prices - fill lowest first

direct negotiation - premium to market price

impact of share repurchase on EPS

internally financed - increase EPS if the funds would not earn the cost of capital if retained

externally financed - increase EPS if earnings yield > after tax cost of debt

impact of share repurchase on BV per share

BVPS decrease if market price > bv per share

dividend vs share repurchase

high dividend tax - share repurchase have tax advantage

if management views shares as undervalued - share repurchase

share repurchase flexible - not obliged to carry through

offset dilution from employee stock options

increase leverage - change capital structure

dividend coverage ratio

income / dividends

FCFE coverage ratio

FCFE / (Dividends + share repurchases)

principal–agent vs principal–principal

principal–agent - dispersed ownership - weak shareholders + strong managers

principal–principal - concentrated/dispersed ownership + concentrated voting power- strong shareholders + weak managers (minority weak shareholders)

cost of debt

rd = rf + Credit spread

traded debt - YTM - more liquid better

credit rating - YTM of companies with similar credit ratings

infer credit rating with IC ratios, financial leverage ratio

amortizing loan lower cost of debt

Top-Down External Factors

Capital availability - lower cost of capital

market conditions - interest rate, inflation, macro

legal and regulatory consideration - country risk

tax jurisdiction - higher marginal tax rate - greater benefit of using debt

Bottom-Up Company Specific Factors

revenue, earnings , cf volatility - sales risk (uncertainty of price and units); customer concentration risk; financial leverage

asset nature and liquidity - highly liquid assets - lower cost of capital

financial strength, profitability leverage

security features - callability (higher); putable (lower); convertible (lower); cumulative (lower); share class

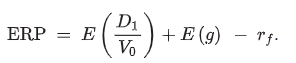

equity risk premium - forward dividend discount model

Macroeconomic Modeling - Grinold-Kroner

ERP = [DY + Δ(P/E) + i + g – ΔS] – E(rf).

Expected capital gain = Δ(P/E) + i + g – ΔS

Expected repricing = Δ(P/E)

Earnings growth per share = i + g – ΔS

g = real economic growth

ΔS = change in shares outstanding

expected inflation

Bond Yield Plus Risk Premium Approach

re = rd + RP,

RP is a risk premium to compensate equity investors for additional risk relative to the risk of investing in the company’s debt

Expanded CAPM

size premium

company specific risk premium

Build-Up Approach

re = rf + ERP + SP + IP + SCRP,

country risk premium (CRP)

CRP = Sovereign yield spread x (Volatility of equity market) / (volatility of bond market)

Restructuring

cost restructuring - outsourcing / offshoring (relocating operations)

balance sheet restructuring - sale leaseback; dividend recapitalization (reduce equity share repurchase with cheaper debt)

Reorganization

leveraged buyout -

comparable company analysis

data readily available

difficult to find comparable

sensitive to mispricing on market

yields fair-trading price ; must add takeover premium to get fair takeover price

comparable transaction analysis

no takeover premium - embedded in multiple

few comparables

exclude old transactions

risk that acquirers over/under paid.

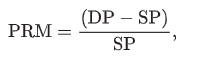

takeover premium

PRM = takeover premium (as a percentage of stock price)

DP = deal price per share of the target

SP = unaffected stock price of the target (one week prior)